Happy Chinese New Year to all readers!

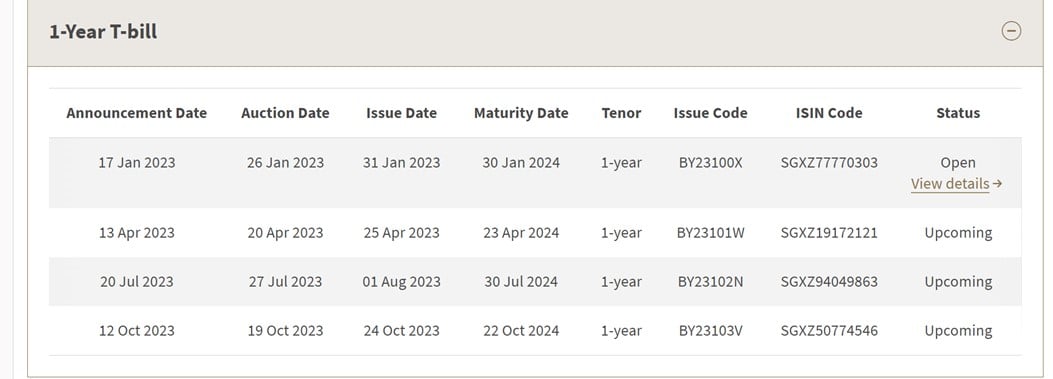

In case you missed it – we’re going to get a 12 month T-Bills auction this month.

12 month T-Bills are incredibly rare – this is one of only four in 2023.

So if you want to apply, make sure to get your cash applications in by 9pm on 25 January.

I wanted to discuss my yield projections in this article, and why I think yields may come in lower than expected.

Yield on the 12 month T-Bills may not be good

If you’ve walked past a physical bank branch this week you’ve probably seen long queues.

Those queues are not for people trying to get new notes, they are for people trying to buy 12 month T-Bills with CPF-OA.

Crazy stuff.

Now if you’re going to spend an hour in the queue just to buy T-Bills with CPF-OA.

You’re going to want to make sure you get an allocation no matter what.

Which means you might submit a low bid, say 3.0%, just to ensure that you get allocated (instead of wasting an hour of your life).

If enough people do this, the yield on the 12 month T-Bills starts getting wonky.

Especially when there are only four 12 month T-Bills in 2023…

What is the estimated interest rate on the 12 month T-Bills?

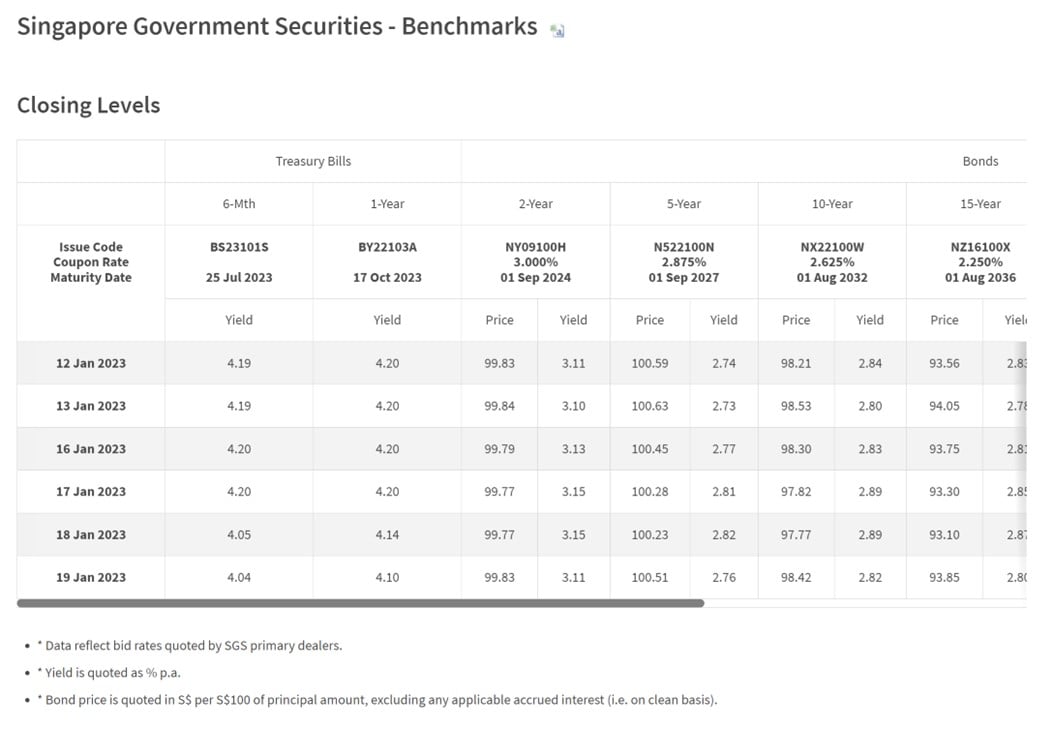

Latest SGS yields are at 4.1%.

The problem is that the global interest rate trend has been firmly down the past few weeks.

And all the recent T-Bills auctions have seen cut-off yield come in below market yields.

Coupled with the (anecdotally) insane demand for the 12 month T-Bills from CPF-OA applications, I think you’ll probably see yields come in below 4.1%.

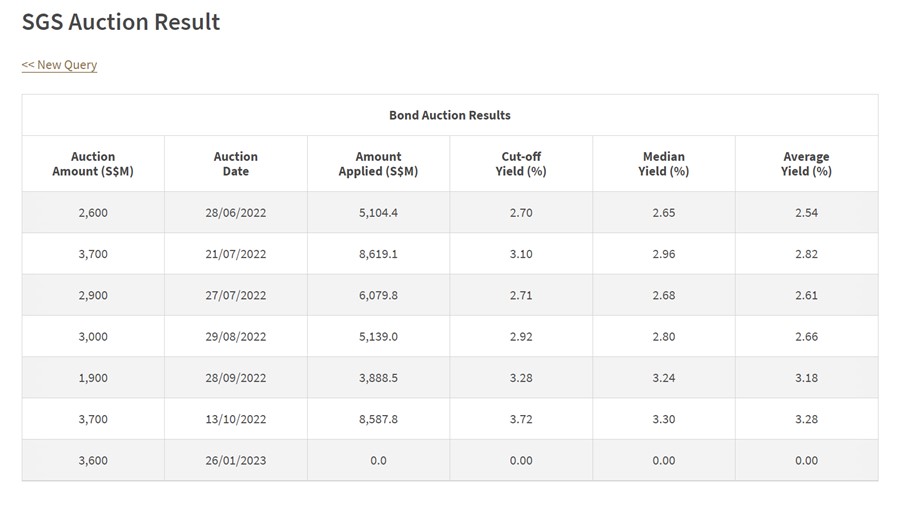

Historical 12 month T-Bills auction data

For reference, here’s the historical data for the 12 month T-Bills going back to mid 2022.

The most recent 12 month T-Bill was on 13 October.

Market yield back then was about 3.57%, and cut-off yield came in firmly above that at 3.72%.

That said, this was back in October when interest rates were on a clear uptrend and the Feds were hiking 75bps per hike.

I’m not so sure you see the same this time around.

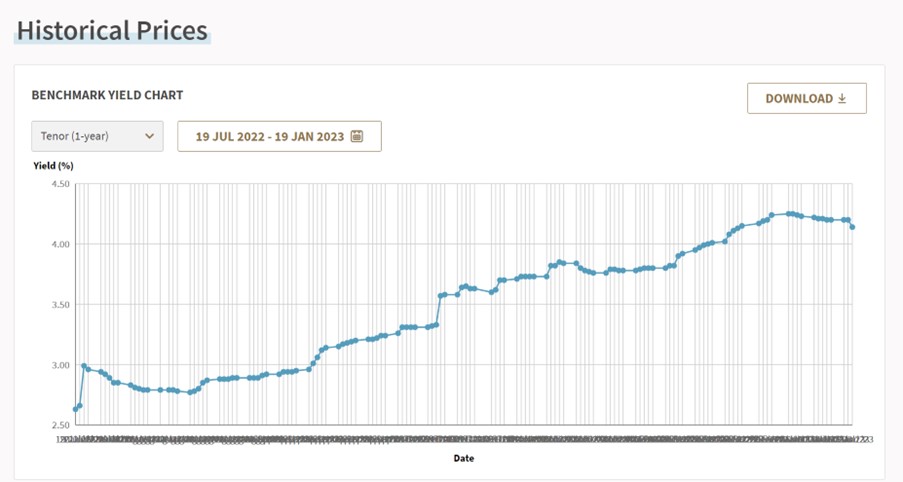

Looking at market pricing, you can see yields start to come down a bit the past month or two:

My estimate for the next 12 month T-Bills yield – 3.9% – 4.1%

The 12 month T-Bills in my view are a lot harder to call than the 6 month T-Bills.

Firstly because they are so rare, and secondly because I suspect there will be higher retail demand (especially from CPF-OA) which could skew the numbers.

Gun to my head, I would say maybe 3.9% – 4.1%.

But I do think there is a risk it comes in even lower than that.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you buy a 12 month T-Bill instead of 6 month T-Bills? To lock in interest rates?

The considerations if you’re buying with CPF-OA are quite different and you can see my analysis in yesterday’s article (spoiler alert: they are very close).

But what if you’re buying with cash?

Are 12 month T-Bills a better buy than 6 month T-Bills?

Answer will depend on where interest rates (for T-Bills) go after 6 months

Now the answer to this question will depend on where interest rates are after 6 months.

If interest rates go to 5.0% by mid 2023, then for obvious reasons you’ll look like an idiot locking in at ~4.0% for 12 months.

Whereas if interest rates go to 3.5% by mid 2023, then you’ll look like a genius.

So where will interest rates for T-Bills be in 6 months time, in June 2023?

Answer will depend on where interest rates (for T-Bills) go after 6 months

Now the answer to this question will depend on where interest rates are after 6 months.

If interest rates go to 5.0% by mid 2023, then for obvious reasons you’ll look like an idiot locking in at 4.2% for 12 months.

Whereas if interest rates go to 3.5% by mid 2023, then you’ll look like a genius.

So where will interest rates for T-Bills be in 6 months time, in June 2023?

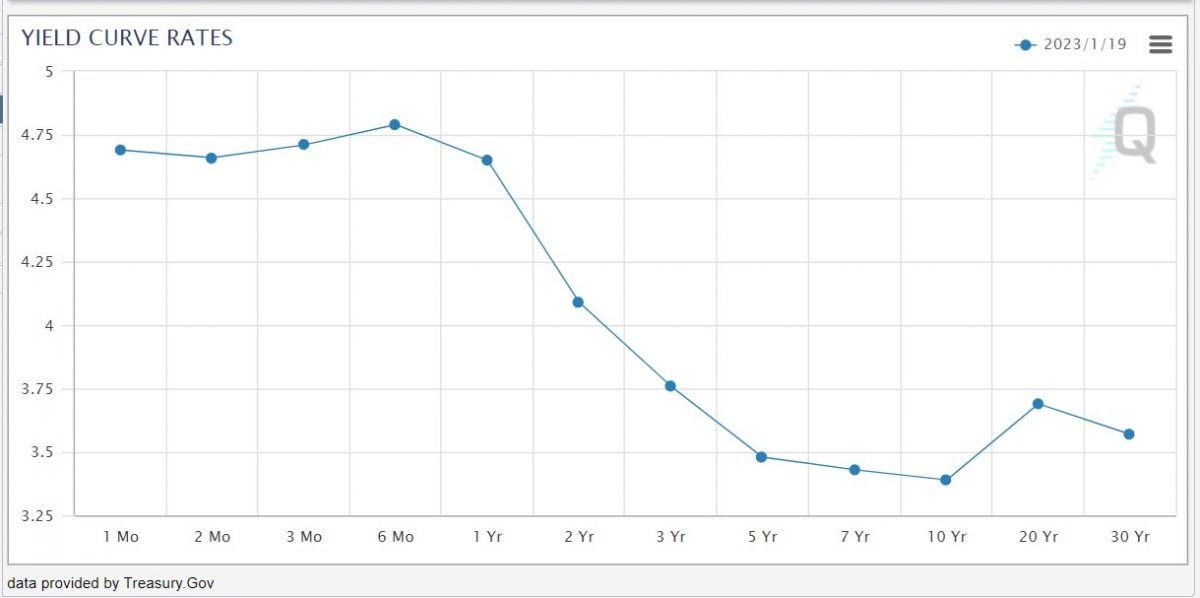

Where does the market think interest rates will be in 6 – 12 months?

This is what the market thinks.

Market thinks interest rates will be slightly higher in 6 months time, but slightly lower in 12 months time.

In other words – market is expecting interest rate cuts at the 6 – 12 months mark, but only a small cut.

Although if you ask me, I think the market may be overly optimistic about the pace of interest rate cuts.

I think interest rates may stay up longer than the market is pricing in.

The only way we get rate cuts earlier is if (1) market crashes, or (2) we get a deep recession.

On (1) – stocks are actually going up in 2023 so far, not going down.

Little reason to panic for the Feds.

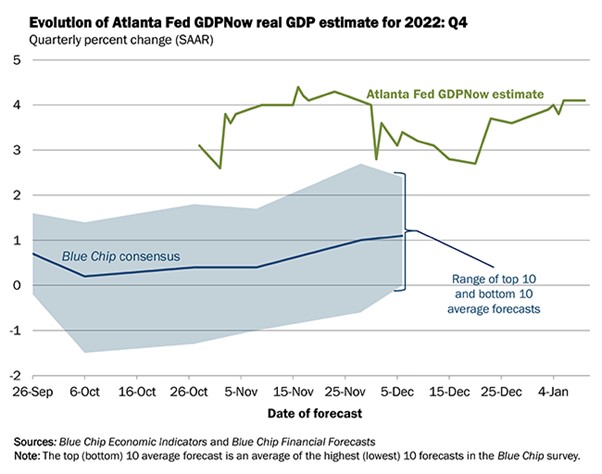

On (2) – latest GDP Now is showing the US economy still well in growth.

A recession will come if we stay on this path, but not as soon as people are expecting.

So FH… Will you buy the 6 month T-Bill or 12 month T-Bill?

Looking at the above, I think I still prefer the 6 month T-Bills.

Probably the main consideration for me right now is that T-Bills cannot be easily exited before maturity.

So I’m not super keen to lock up money in a 12 month T-Bill, unless I get a premium on the interest rates.

Especially since my current view is that interest rates should still be high in 6 months.

And looking at current market pricing, it looks like the 6 and 12 month T-Bills will have quite similar interest rates, with the added risk of 12 month T-Bills coming in low because of CPF-OA demand.

So yeah… probably prefer the 6 month T-Bill for now.

What about Fixed Deposit – makes sense to lock in a longer duration?

Of course, the thinking is fundamentally different for Fixed Deposit because FD can be broken any time.

So with FD I think the opportunity cost of locking it up is a lot lower, because worst case you can just break it.

Will I be bidding for the 12 month T-Bills?

For what it’s worth, I think I’ll probably still throw in a bid.

I mean it’s Chinese New Year, why not try my luck right.

Competitive Bids for T-Bills only?

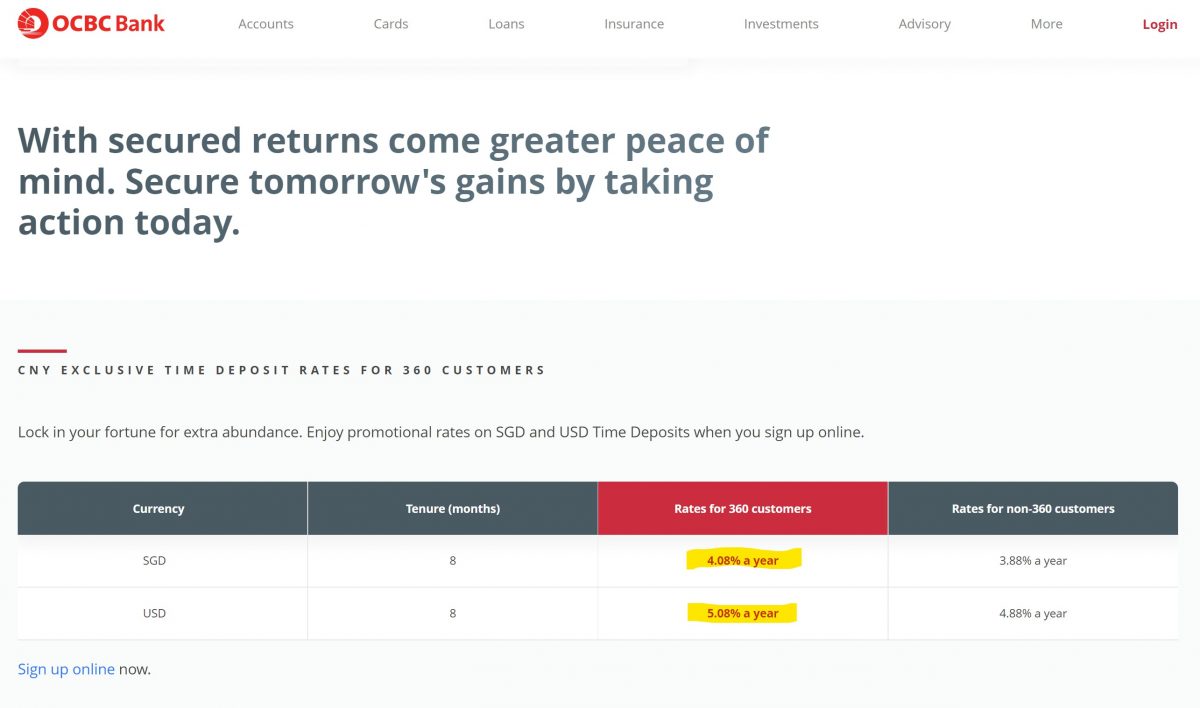

But I’m definitely going to be doing a competitive bid, because I dont see any point in having my cash tied up for 12 months at some low interest rate.

Especially not when I can get 4.08% on an 8 month OCBC Fixed Deposit these days.

I can see why those using CPF-OA to bid would want to bid lower (see my article on the analysis for those using CPF to buy).

But I think for cash bidders, there’s really a lot of options out there in terms of Fixed Deposit that pays above 4.0%.

With 4.08% from a local bank in OCBC, I really don’t think it makes sense to be bidding below that.

Especially when Fixed Deposit can be broken any time for easy liquidity.

But I mean – it’s your money really.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH, the last 1-Y T Bill (BY22103A) trades at 4.08% on 20/1/2023. Is it logical to infer that the upcoming one will not go beyond 4.08% then, barring any wild surprises? Thanks.

Yes – I think that’s fair. Although given the latest market trends I think the yields on this 12m T-Bills should come in on the lower end of the range I gave.

I am a little confused with the T-Bill trading. The 4.08% is what was traded between investors (buyer-seller). How then does the 4.08% translate into traded price and how does the seller gained anything since the buyer had gotten the payout right at the start? Appreciate any sharing, thanks.

They buy at a discount to face value.

Correct me if I am wrong, if I as a buyer wishes to sell $100k of my 1-Y T Bill (BY22103A), I have to sell at a rate of 4.08%. This would translate to me only getting paid $96982 = $100k – $3018 (100K x 4.08% p.a. but for 270 days only since maturity is on 17 Oct 2023)?

Didn’t check your numbers specifically but your concept is right – you buy at a discount.