I was reading the latest quarterly financial results for CapitaLand Integrated Commercial Trust (CICT) and Frasers Centrepoint Trust (FCT) recently.

They are an absolute treasure trove of information on the Singapore commercial real estate market, so I highly recommend that investors take a look every quarter.

In any case, I wanted to share my 3 key takeaways in this article:

- Suburban malls still performing very well

- Tenant Sales have surpassed pre-COVID

- Office Rental market is still recovering

1) Suburban malls still performing very well

I was pretty surprised by this one actually.

I would have expected that after the COVID work from home trends played out, and people started returning to offices, suburban malls would underperform downtown malls.

But interestingly – this dynamic has not played out at all.

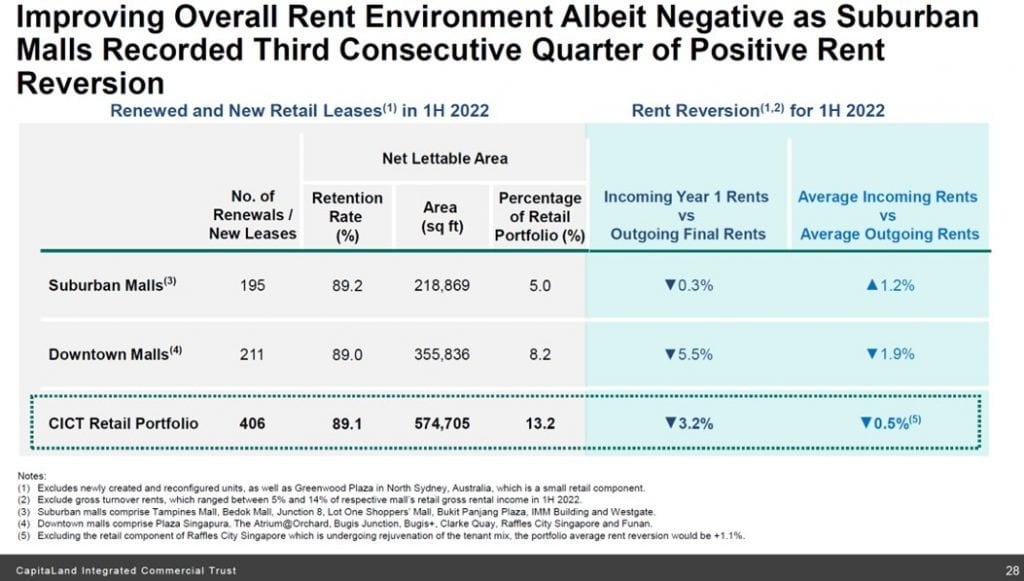

From CapitaLand Integrated Commercial Trust’s results:

- Average incoming rents for Suburban malls are up 1.2% from outgoing rents

- Average incoming rents for Downtown malls are down 1.9% from outgoing rents

This is especially start in incoming Year 1 Rents vs outgoing final rents, where Downtown malls are down 5.5% (vs 0.3% for Suburban).

Landlords still need to offer a big discount to entice new tenants for downtown malls.

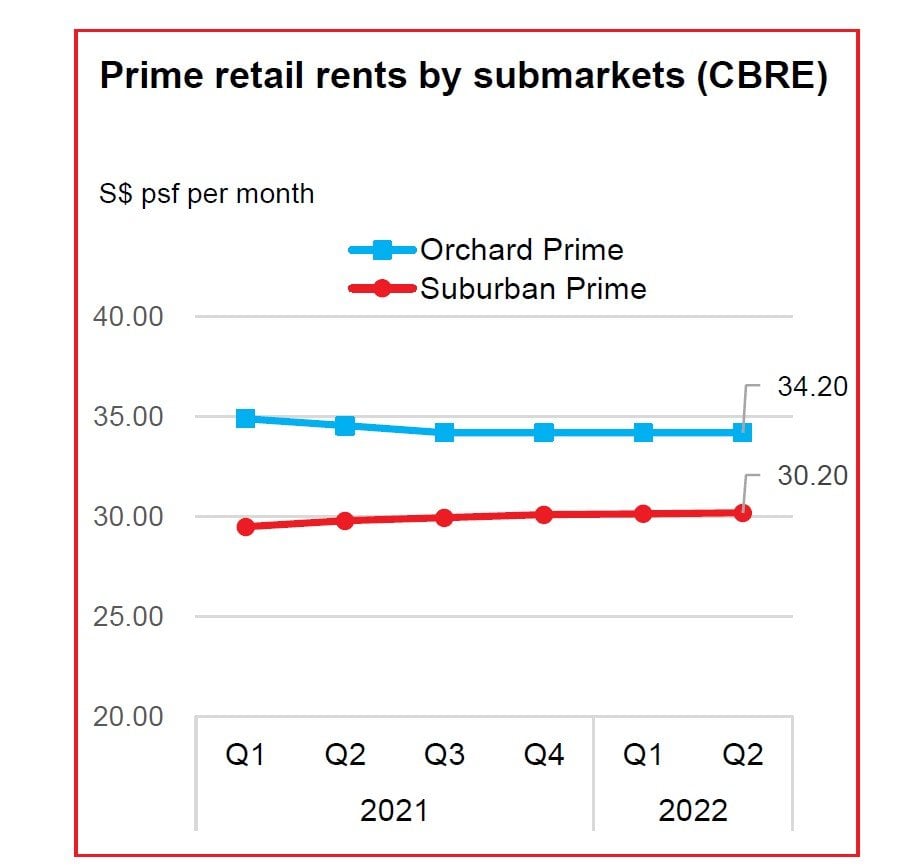

Frasers Centrepoint Trust’s results has this very helpful chart from CBRE which backs up this dynamic.

Rents for central malls have been declining for the past 1.5 years, while suburban malls have been going up:

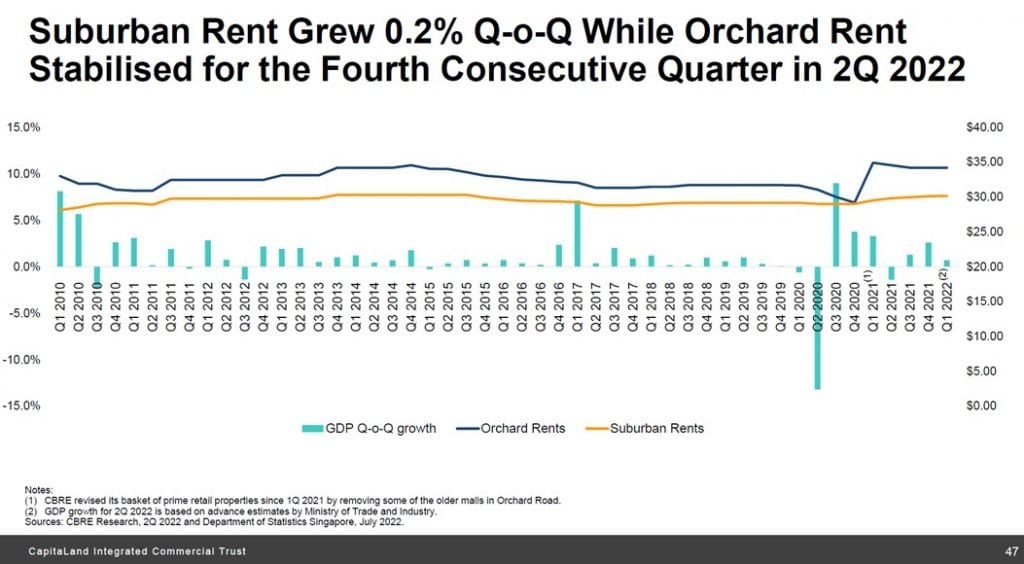

This is backed up by data from CICT as well:

I suppose you could argue that the COVID reopening trend only really started in Q2 2022.

So we may only see this dynamic (of downtown malls outperforming) play out over the next few quarters.

Especially as tourism starts to recover.

I’m not so sure though.

A lot of companies are starting to announce permanent flexi-work arrangement, with 1 – 2 days work from home each week.

So it’s possible that this whole work from home trend may stay for a while, and that this suburban mall trend is not going to reverse.

But let’s see.

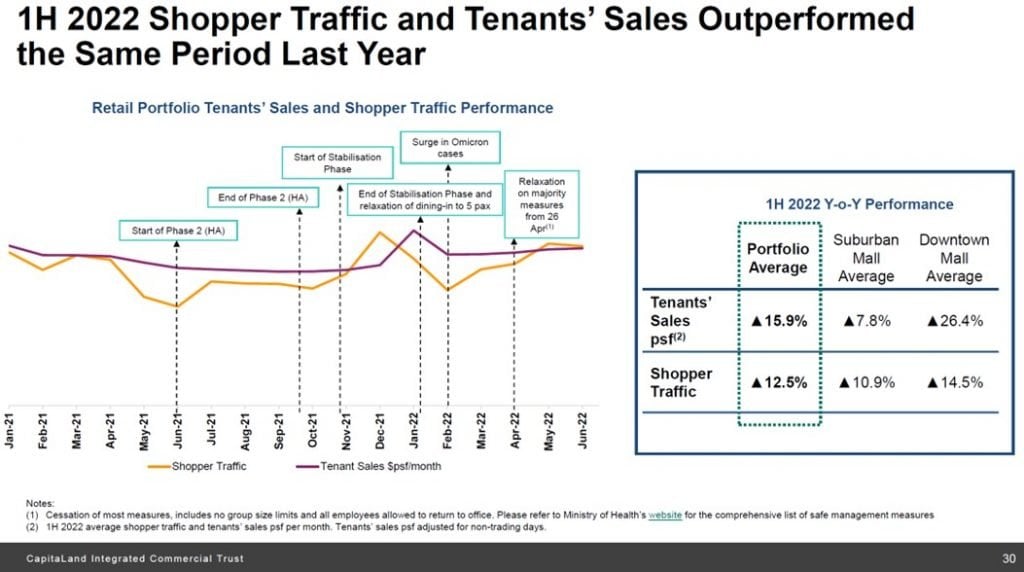

2) Tenant Sales have surpassed pre-COVID

Tenant sales and shopper traffic have all recovered very strongly.

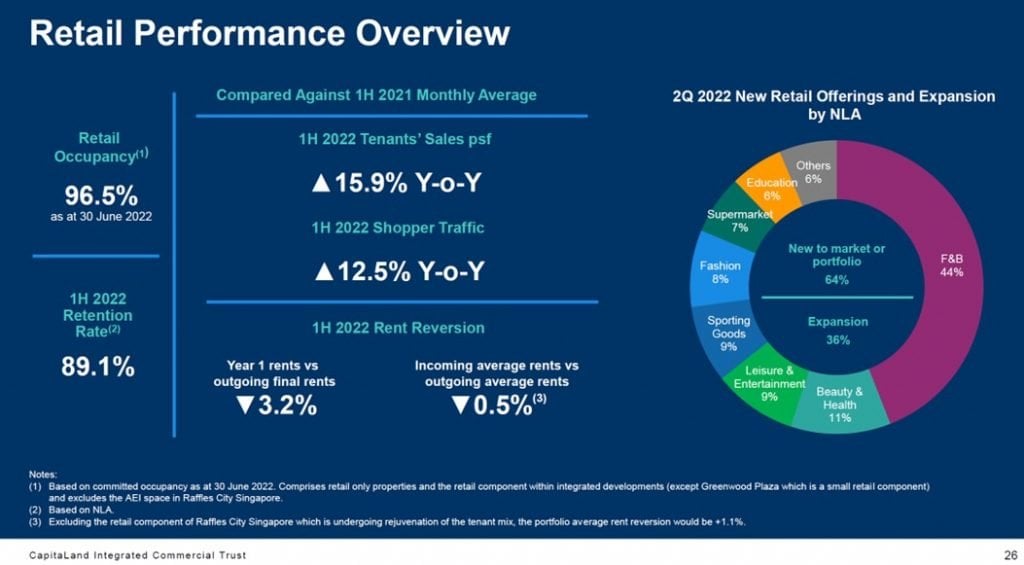

For CapitaLand Integrated Commercial Trust in 1H2022:

- Tenant sales are up 15.9% year on year

- Shopper traffic is up 12.5% year on year

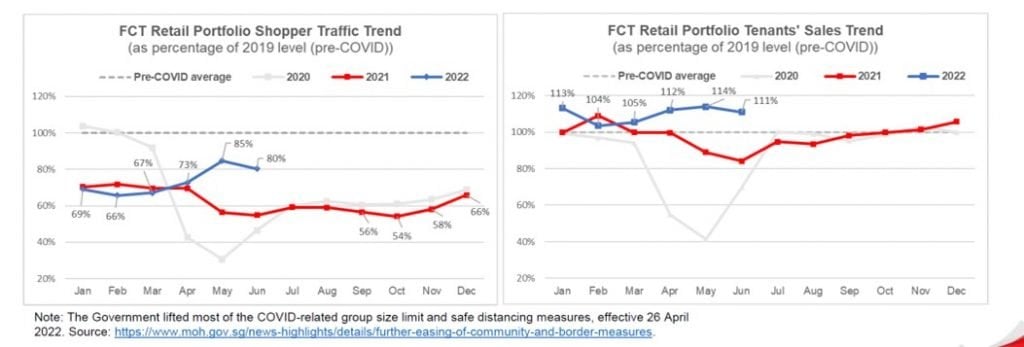

For Frasers Centrepoint Trust in 1H2022, both tenant sales and shopper traffic are up quite significantly from 2021, especially in Q2 after the COVID reopening.

An interesting tidbit is that while shopper traffic is still below pre-COVID trends, tenant sales have already surpassed pre-COVID.

This suggests that people are cutting out the non-essential trips to the mall.

They won’t go to the mall just to hang out.

They go to the mall only if they intend to actually spend money.

Which I suppose is not necessarily a bad thing for a landlord.

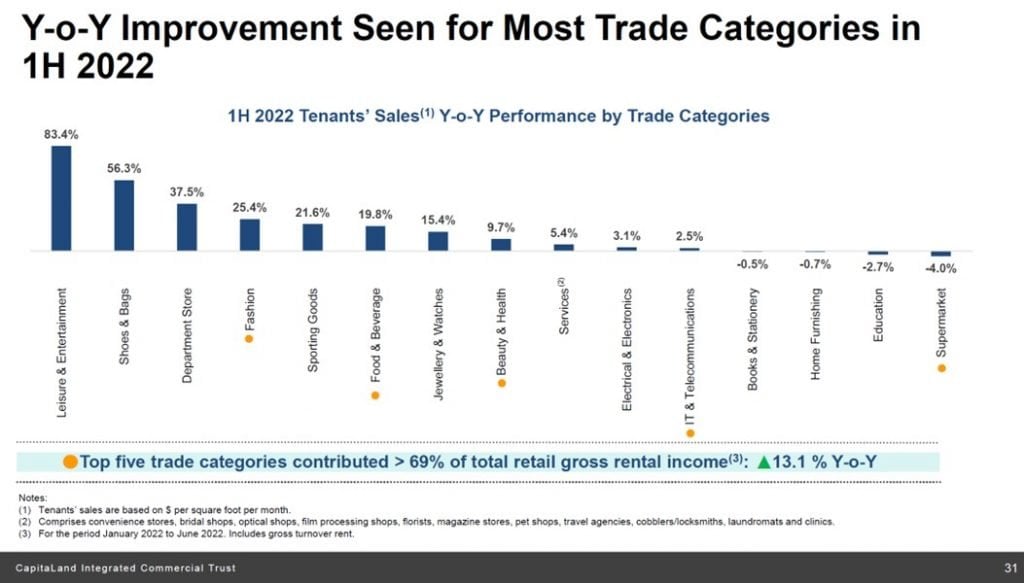

Which trade categories are performing the best?

In terms of which categories benefitted the most, it’s pretty much as you would expect.

Leisure & Entertainment is up the most with a whopping 83.4% year on year increase.

Fashion, sports, F&B, department stores, beauty, are all doing well too.

Worse off at the stay at home trades – supermarket, IT, books, furniture.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

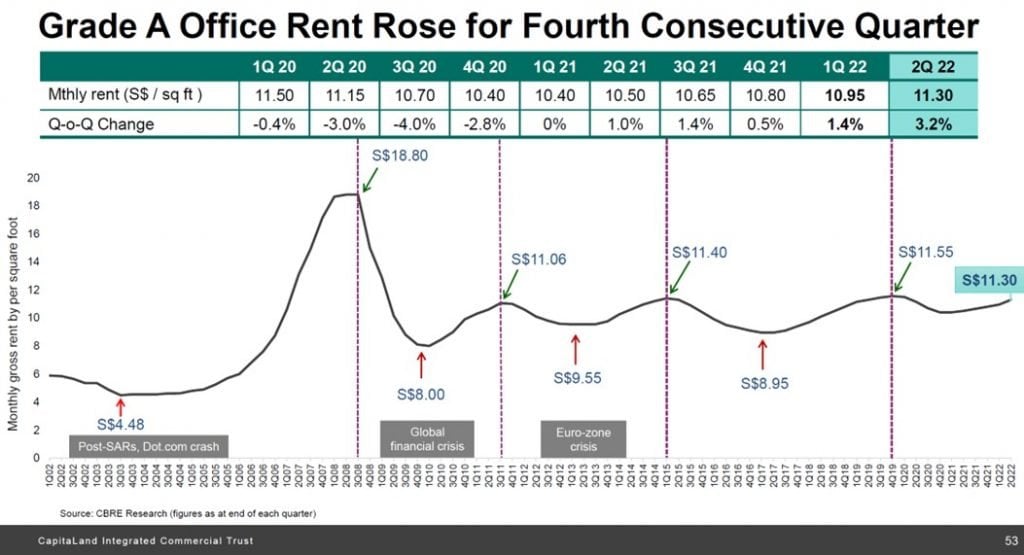

3) Office Rental market is still recovering

Much has been said about the death of the office.

But when you look at Grade A office rents, they are holding up very well.

Up 3.2% quarter on quarter for 2Q 2022 for CapitaLand Integrated Commercial Trust.

This one was in line with my expectations.

I expected Grade A Office Rental to continue to perform well post-COVID.

The way I see it – companies will cut out non-essential space.

So the back office at Changi Business Park etc can work from home or switch to flexi working.

But your frontliners who need that swanky new office space at Marina One to meet clients?

I doubt they are cutting that space.

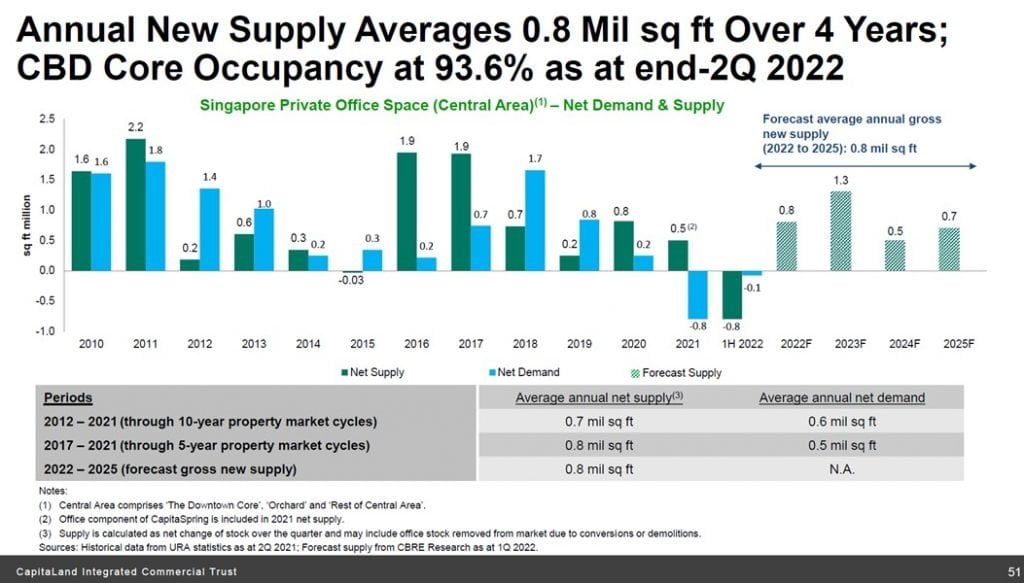

At the same time – New office space is quite limited also, so there is no need to worry about a glut of supply.

From the CapitaLand Integrated Commercial Trust results:

With a stable domestic economic outlook, return-to-office recovery and limited new supply in the pipeline, CBRE Research expects Core CBD (Grade A) office rents to grow 8.3% for 2022, compared to 3.8% for 2021.

I’ve been constructive on Grade A office space for a while too, so I am inclined to agree with them.

Key takeaways on the CICT / FCT quarterly results?

I think the key takeaway for me is that despite all the talk about an impending global recession – very little of this is showing up in the data.

Both retail and office rents are still growing very nicely, and consumer / business spending is holding up.

Sure, you can argue that all this is lagging data, and that this will change in the quarters ahead, as rising interest rates start to bite.

I don’t disagree.

In July 2007, the then Citigroup CEO said:

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

Very similar dynamic played out in 2008 as well, when rentals held up very well, until suddenly they didn’t.

Is the same thing going to happen in 2022/2023?

Are the Feds going to continue hiking us into a recession?

Or are they going to flip dovish and allow inflation to rage?

Whatever the case, it seems that for now at least – the music is still playing. And consumers, and businesses, are still dancing.

As always – love to hear what you think!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try here.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Thanks FH

Nice summary and agree with your views

Few things here- Firstly, there is a “perception” that both goods as well as services at downtown malls are much more expensive than suburban malls. There is an element of truth here

From the retailers point of view, this would be necessary to protect their margins

The problem is that the custom can only be provided for the downtown mall by either higher income customers at their work spot areas or more realistically, by foreign visitors. The takings of the downtown malls will go up with higher rents following only next year when tourists return in big numbers after China relaxes

Secondly, from an investment point of view, both are still fairly or dare I say, slightly overpriced if I take into account the potential interest rate trajectory

Both become buyable at around 205 and 225 and below though still with some downside risks

Finally, the MERCATUS deal needs to be seen

If either of these or a consortium goes for that mega buy, there will be big equity dilution for certain

I hold both but will not add as I am preparing to shell out if they issue rights for this

Regards

Garudadri

That’s a great comment Garudadri. Agree with most of the points you raised.

Yes I have been tracking Mercatus closely as well. If anything I would be inclined to favour CICT as the eventual winner, as they are one of the few (with the financial muscle of the sponsor) to take on this deal.

The problem though, is pricing. With rapidly rising rates (3.5% by year end), weakening global economy, I wonder if the winner of this deal may actually turn out to be the loser if they bid at too high a price. Especially since they will need to do a big EFR into what might be quite weak risk appetite later this year…

Whatever the case, I am aligned with you. I am holding elevated cash positions for now, and letting the market play itself out. If there are good opportunities, I will be adding.