CapitaLand Integrated Commercial Trust (CICT) is Singapore’s largest retail and commercial (office REIT).

So their quarterly financial results are a treasure trove of information for investors who want to track the status of Singapore retail / office rents.

I was going through CICT’s Q1 2022 financial results recently, and I wanted to share some of the key takeaways I had.

This is an exclusive Patreon article. If you found it useful, do consider signing up as a Patron and receiving more exclusive articles like this.

You also get access to my full REIT and stock watchlist (with price targets), and full personal portfolio to check out how I am positioned for the coming downturn.

3 Key Takeaways on Singapore Retail

Let’s start with Retail:

- Suburban malls still outperforming Downtown malls… but early signs of change

- Sector Recovery is what you would expect from re-opening

- Retail supply going forward is limited

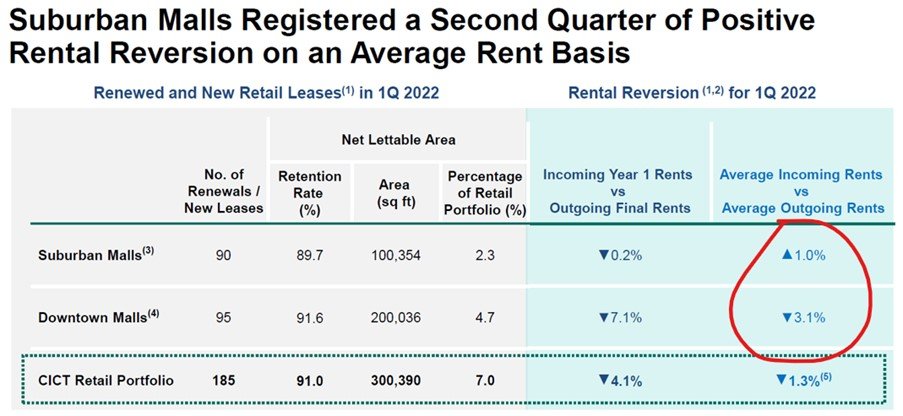

Suburban malls still outperforming Downtown malls… but early signs of change

Rental reversions for suburban malls are still outperforming downtown malls.

Breaking it down:

- New leases for suburban malls are being signed at an average of 1.0% above their outgoing rents.

- While new leases for Downtown malls are being signed at 3.1% below their outgoing rents.

For now at least, it seems that there is higher demand for rental in suburban malls than downtown malls.

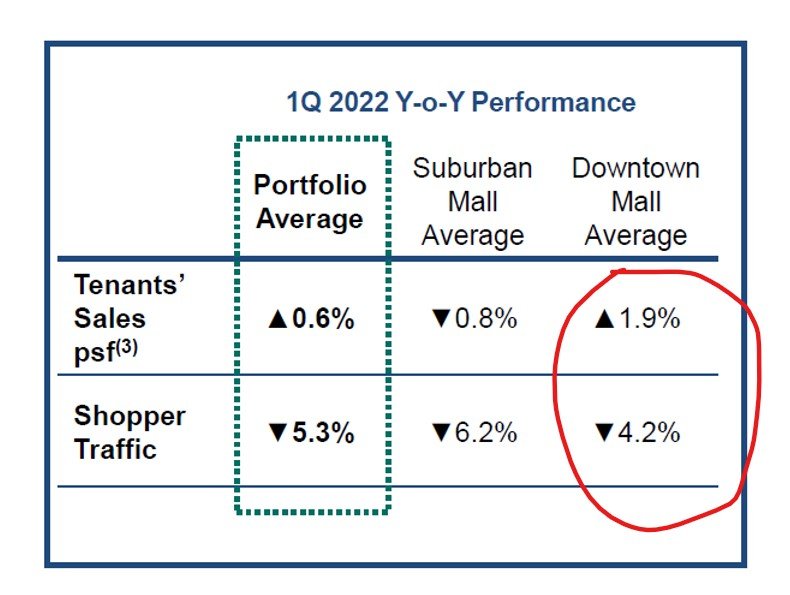

But don’t forget these are Q1 numbers, before Singapore started to really open up.

As investors we’re always more concerned with what happens going forward.

And digging around for more clues – we start to see that Downtown malls are starting to improve both in tenant sales and shopper traffic, even in Q1.

Remember that rental rates are a lagging indicator, while tenant sales/shopper traffic is a forward indicator.

So there are some early signs from tenant sales/shopper traffic that downtown malls will recover more strongly going forward, as the reopening continues to play out, and more people return to office.

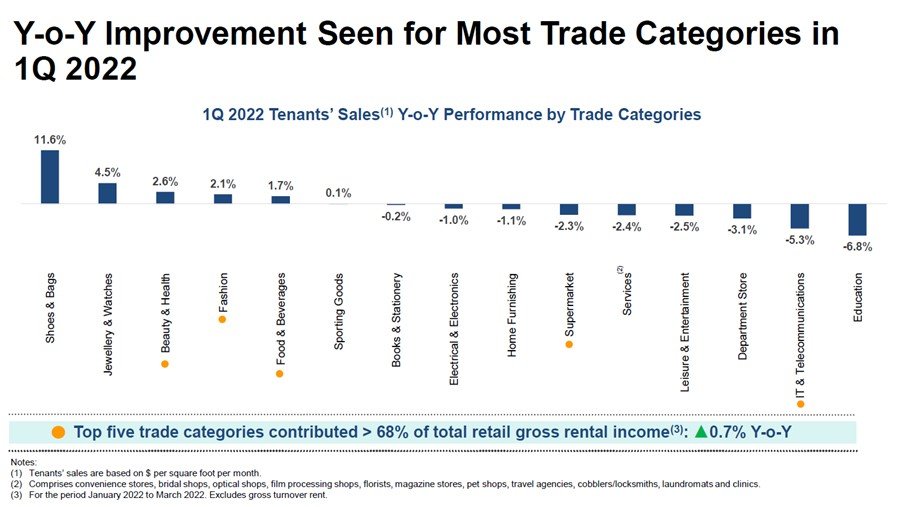

Sector Recovery is what you would expect from re-opening

The trade sector recovery is exactly what you would expect from a reopening.

It’s the exact opposite of the COVID trade.

Things that did very poorly during COVID – fashion, F&B, beauty, are all recovering very strongly.

While stuff that did well during COVID – supermarkets, technology, are not doing so well.

Another interesting tidbit of information is that a lot of the new retail tenants for CICT’s portfolio are new to market.

So despite all the doom and gloom about the death of retail, people are still pretty keen to start new retail businesses.

The tenant mix is exactly as you would expect – F&B, Beauty and Fashion being the 3 largest categories respectively. These are the tenants that pay the highest rent, which is good to have to maximise rental income for the REIT.

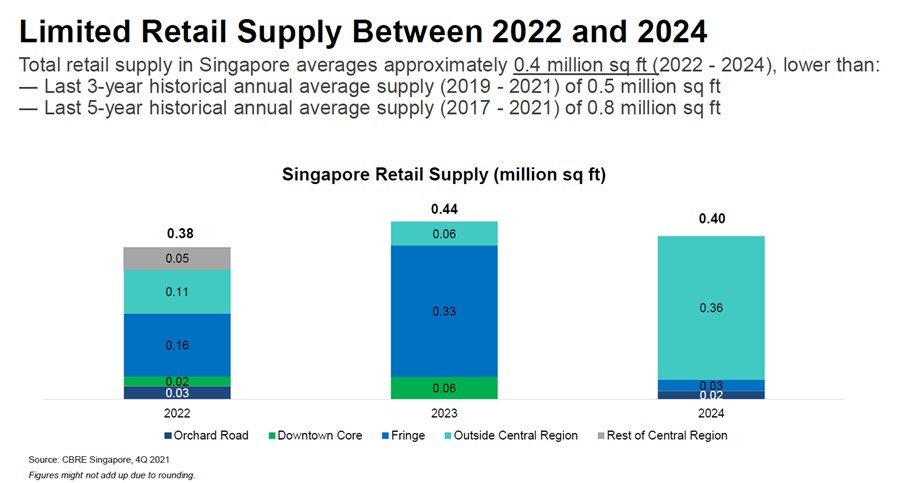

Retail supply going forward is limited

Retail supply over the next 3 years is pretty muted, at 0.4 million sq ft a year from 2022 – 2024.

This compares with the past 5 years which averaged about 0.8 million sq ft.

So at least from a supply side, investors can rest easy as there is no glut of retail supply coming to crash rental rates.

3 Key Takeaways on Singapore Office

Moving on to Office Space:

- Grade A office recovery rent continues

- Strong demand from Tech, Banks, Energy/Commodities

- Increasing supply of office space over the next 3 years

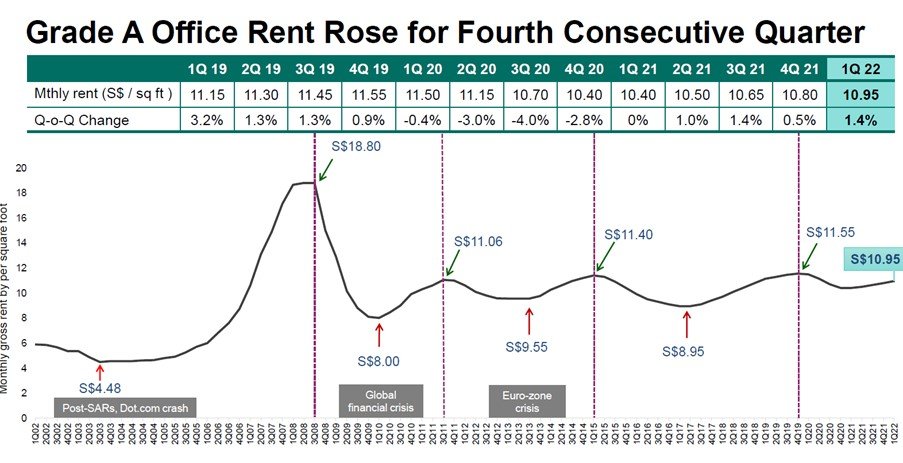

Grade A office recovery rent continues

Despite all the talk about the death of the office, Grade A office rents are still holding up very strongly.

We’re not back to pre-COVID levels just yet, but rents holding up at S$10.95 psf are very strong indeed.

Strong demand from Tech, Banks, Energy/Commodities

The demand from office space comes mainly from:

- Tech

- Banks

- Energy/Commodities

This horse is old enough to remember a time 2 years ago in the depths of COVID when banks were cutting office space in a bid to cut costs, and it was all doom and gloom for banks. Funny how things turn so quickly once interest rates start moving.

Tech is interesting. With the ongoing collapse in tech valuations, I wonder if this will eventually flow over into their demand for office rental, as they are forced to cut back on costs.

Energy/Commodities making a comeback is also another sign of the changing times. After 10 years of collapsing commodity prices, they are suddenly overflowing with cash flow.

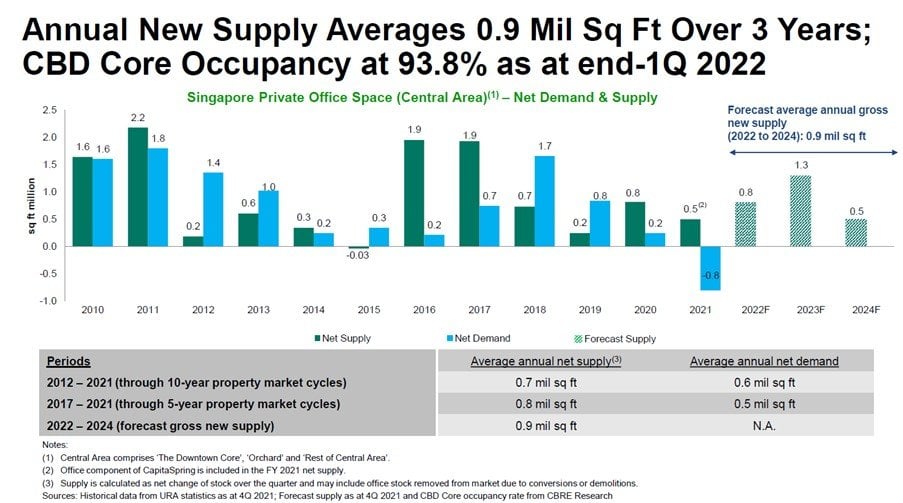

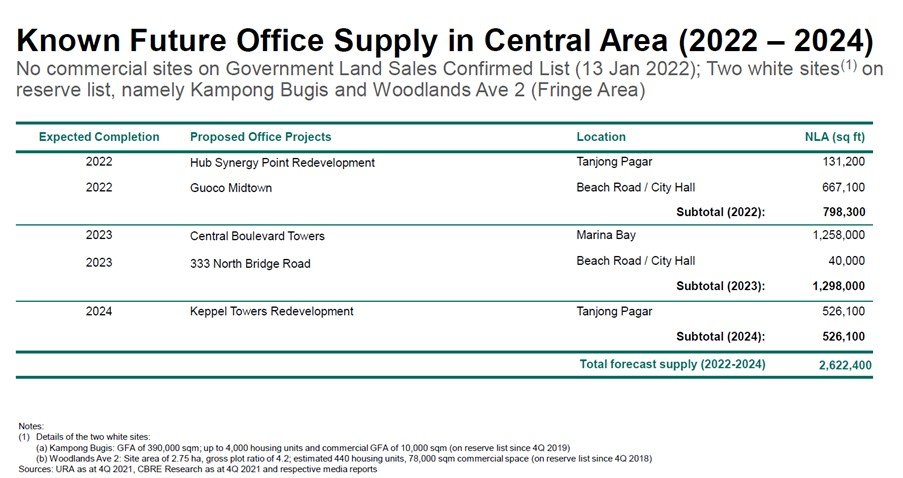

Increasing supply of office space over the next 3 years

Unlike Retail, office space going forward will increase slightly to 0.9 million sq ft a year going forward.

This compares to 0.8 million sf ft per year over the past 5 years.

CICT estimates average annual net demand of 0.5 million sq ft the past 5 years.

Which means that demand may outpace supply at least in the near term.

This is slightly troubling. One wonders if the market can absorb 0.9 million sq ft a year going forward, especially given the weakening global economy.

Key question in my mind – Outlook going forward

Looking at CICT’s financials, all the numbers generally paint a rosy story.

Retail and Grade A office rents are holding up well, and the continued reopening in Q2 will provide a further tailwind for rentals.

But ultimately, all of this is backward looking.

And the key question in my mind, is what is not in the slides.

How well will CICT’s rents, and it’s real estate valuations, hold up in a year of rapidly rising interest rates, sticky inflation, and potential global recession?

Will rents drop due to reduced demand from a global recession?

Will real estate cap rates get compressed due to rising rates?

At current price of $2.23, CICT trades at a 4.66% yield and 1.078x book value.

Is that a sufficient margin of safety for the growing stormclouds in the macro environment?

Personally I last added to CICT in the $1.9-2.0 range, which was a 5% yield and book value.

CICT is also one of my largest REIT positions, so I don’t see an urgent need to add at these prices.

If it goes back to 5-10% below my last buy in, I might consider adding again. That works out to about $1.8+.

As always, love to hear what you think!

This is an exclusive Patreon article. If you found it useful, do consider signing up as a Patron and receiving more exclusive articles like this.

You also get access to my full REIT and stock watchlist (with price targets), and full personal portfolio to check out how I am positioned for the coming downturn.

Dear FH

Thanks for the succinct article. I have held this for years and this is one of the most diversified and good quality REIT here that has fared reasonably well

The grade A office rental reversions will be going up over 11$ in this inflationary environment, high quality city center CBD office space will retain value and the book value will also go up

This will be partially but significantly offset by negative reversions in fringe and non core office properties as a result of the future pipeline of office space- there will be a flight to quality!

As regards retail, the opening up plus overall increased sales will help and offset the rate increases to a big extent

In case of a recessions, which is unlikely barring another major macro or black swan event, the anticipated rate hikes will not happen!

Overall ok

However at 2.20 plus, I will stay away and for leveraged instruments like REITS, I would argue that we need at least a 5.5 percent yield with this one to add

Of course, this is because at this point of time, I see better value taking the recession risk on my chin, by adding to the banks

The banks offer not only a reasonably secure 4.5% yield but also prospect of a 10-25% capital appreciation

Apart from Ascendas, FLCT and MIT and perhaps CLCT(risky though), no other SG REIT is on my radar now. Even these come with big risks of sudden equity dilution etc etc with their never ending purchase sprees which most often destroy shareholders value

Regards

Garudadri

Great comment as always Garudadri.

5.5% yield (CICT) is a big drop from current prices – would be about 1.9? Not sure if it will go there, but agree that would be a good price to add.

Interesting that you find the banks a good investment with capital appreciation, I was actually thinking of taking profit there. I suppose you are of the view that we will see sustained higher rates (and higher inflation) for the rest of this decade? Vs the view that after the current peak in interest rates the Feds will cut back to zerobound?