So I was reading the CapitaLand Integrated Commercial Trust 3Q 2021 Business Update this morning.

And man, the slide deck was an absolute treasure trove of information on the Singapore commercial real estate scene – both retail and office.

I figured I’d share my key takeaways here, and hopefully you’ll find it useful.

I’ve never done a post like this before so I’d love to hear your feedback. Do you want more of such posts, or do you want changes to the format – just let me know in the comments!

3 Key Takeaways from CICT’s 3Q 2021 Business Update (CapitaLand Integrated Commercial Trust)

I’ll keep the takeaways at a high level to trends in Singapore commercial real estate, and not so much on CapitaLand Integrated Commercial Trust specifically.

We’ll start with the retail business.

Singapore Retail Market

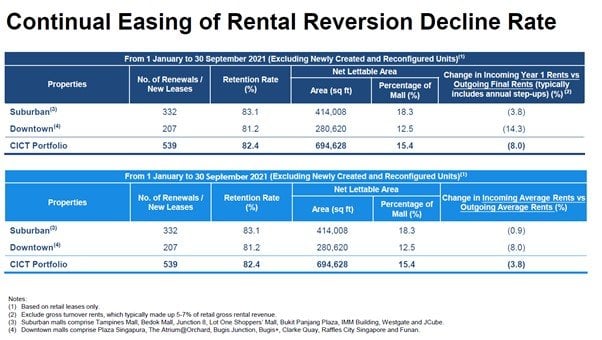

Rental Reversion still declining

Rental reversion for retail leases is still on the decline.

For those newer to real estate, rental reversion is the difference between (1) the rent for new leases and (2) the expired leases.

So this means that the new retail leases are being signed at a rental that is lower than the previous lease.

Where it gets interesting, is the details:

The Year 1 Rents are lower than the Average Rents

This means that landlords are using this as a carrot to sign leases.

They are likely giving tenants a lower first year rent, which then increases over time.

It’s a win-win because tenants get a lower upfront rent and gives them time to stabilize their business.

While landlords get committed occupancy (instead of leaving it vacant), and they also get built in upside going forward.

The only problem I can foresee is if the COVID situation doesn’t clear up. Then tenants would be locked into rising rental obligations, when their core business isn’t improving.

Rental Reversion is much stronger for Suburban than Downtown

New leases for suburban malls are being signed at just 0.9% below the outgoing average rents.

Whereas Downtown malls are being signed at 8% below outgoing average rents.

At the risk of pointing out the obvious, suburban malls are doing much better than central malls right now because of the work from home trend.

I don’t expect this to last forever though, at some point we’ll probably all start going back to the offices again.

So there could be some trading opportunity here if you’re into that. Some variation of the sell the recovery trade where instead of shorting data center REITs you short suburban malls REITs and long central mall REITs.

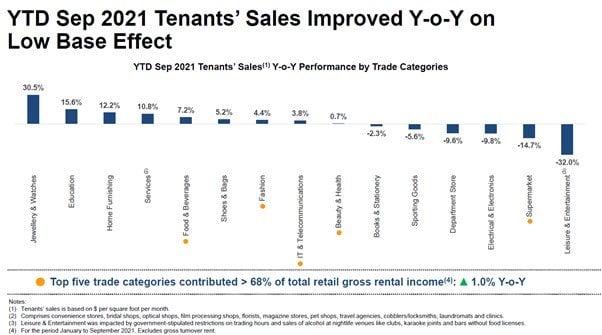

Tenant Sales recovery much stronger than Footfall recovery

Tenant Sales are at 83% of 2019 average (down 17%).

Whereas Shopper traffic is at 59% of 2019 average (down 41%).

This was really interesting for me – it suggests that shoppers are becoming more efficient with their trips.

They’ll still make a trip to the mall if they want to purchase something (hence the recovery in tenant sales), but they won’t go to the mall just to walk around and hang out anymore.

At least that’s how I see it.

You can argue that maybe tenants have adapted better to the post-COVID reality, to sell goods that people actually want to buy. Possible too.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Some Retail Sectors are getting decimated

Tenant sales for certain trade categories are getting decimated.

The big ones are department stores and entertainment, down 9.6% and 32% respectively. That’s massive, and suggests changing consumer patterns.

This looks to be a structural trend and not just a COVID thing.

If you’re a department store owner or entertainment owner, this would be really worrying.

Some other sectors like electronics and supermarkets are down on a year on year basis, but this is probably because of strong base effects – 2020 a good year for supermarket and electronics due to work from home.

The sectors doing well, are:

- Jewelry and Watches (30.5%)

- Education (15.6%)

- Home Furnishing (12.2%)

- Services (10.8%)

- F&B (7.2%)

A lot of this again could be due to low base effects.

But the 30.5% increase in Jewelry and Watches is worth looking into.

Anecdotally, I’m hearing that luxury watch stores are having an absolute roaring business – Rolexes are sold out at almost every authorized dealer now, and you can’t buy one unless you buy other watches first. Even on the resale market they’re going for a hefty premium over the official price.

This makes sense when you tie it back in with record high house prices and COE prices. The people who are doing well from COVID, are doing really well with a lot of disposable cash to spend.

At the same time, supply just can’t keep up.

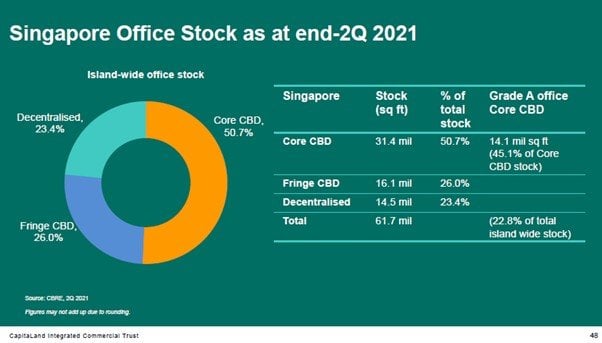

Singapore Office Market

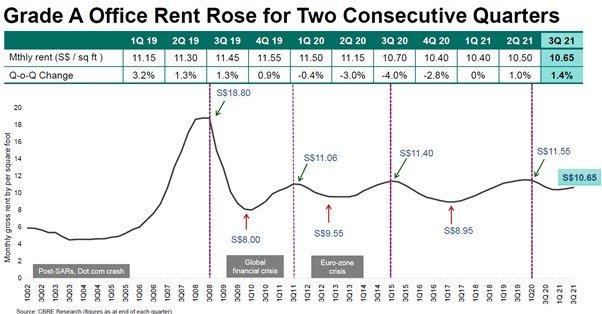

Rental Reversion is improving (but below pre-COVID)

Grade A CBD office spaces seem to have bottomed out in 1Q 2021, and have been on a gradual increase ever since.

The rental rates are definitely still below pre-COVID, but it seems that the worse may be behind us.

This was interesting for me.

We hear so much doom and gloom about the office space, and yet Grade A office rents are recovering nicely.

Strong Leasing Demand from Tenant Expansion

As it turns out – much of the demand is coming from 3 areas:

- Technology

- Consulting

- Finance

And within that, a big portion of the demand is driven by expansion.

A lot of the short term leasing demand has been driven by China tech firms like Bytedance and Tencent, so it’s interesting to see if this trend will keep up.

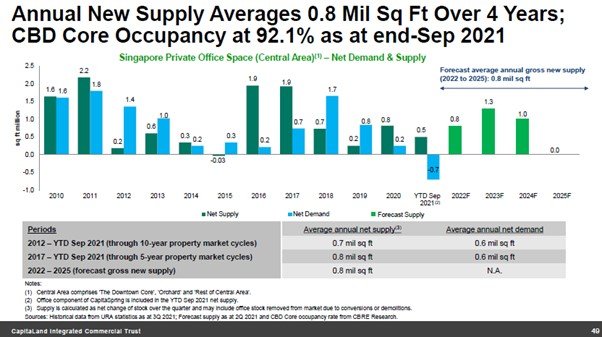

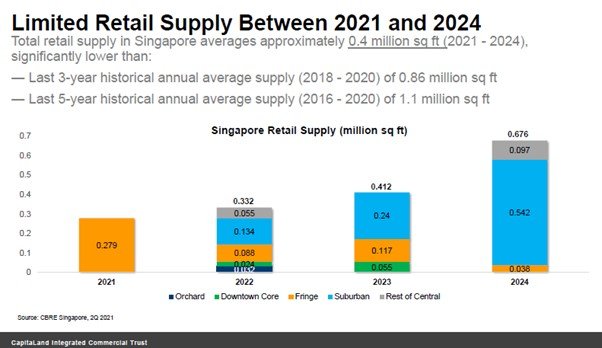

New Supply of Office / Retail space is limited

While demand is resilient, new supply going forward is also quite limited.

We don’t see a lot of potential new supply coming online the next 3 years.

Turns out this is true for retail as well:

So if there is a strong recovery in 2022 for Singapore post-COVID, there could be quite strong recovery in rentals if demand picks up strongly and supply stays low.

A reader has very kindly reached out to share the following article from EdgeProp that shares more information on Office price trends in Singapore.

Really good article which kind of confirms the conclusions from CICT too – that Grade A Office space is on a recovery trend, but the lower quality office spaces are not doing well.

Makes sense too – if you’re going to pay for an office these days it has to be a Grade A one, otherwise you’ll just get the employees to work from home.

Closing Thoughts

You can argue that the big REITs like CICT always try to present information favourable to them, which is why I’ve tried to keep only to the hard data here, and not so much the forecasts.

And the data seems to suggest that the worst may be behind us for COVID, and the path forward is one of recovery.

Whatever the case – love to hear what you think! Did you draw different conclusions from the data?

*Stocks MasterClass Launch Promo ends on 31 October!*

Sign up now and get freebies worth $500:

- 3 Months Subscription to the Highest Tier of Patreon (worth S$200). Get full access to the FH Stock Watch, FH Portfolio, and Premium Exclusive Articles!

- Complete e-Book on How to Invest in REITs (as a Singapore Investor) (worth S$200).

- Complete e-Book on How to Invest in Private Real Estate in Singapore (worth S$100).

Our launch promo is always the best promo – so don’t miss it! Find out more here!

Tenant Sales are just 83% of 2019 average (down 27%).

Thanks for the spot! Have just corrected it should be down 17%

Thanks, like the format and key takeaways

Readable analysis connects. True investors sieve fluffs so don’t bluff. Keep up good work and you be one up !

Thanks! Glad you like it. Looks like feedback is positive will look to do more of such pieces going forward.

Thanks! I agree with the other readers who have commented. Like short updates such as these and find them useful.

I can confirm via anecdote that rental for grade A office space is being renewed at a higher rate! Demand from the tech firms is indeed a key driver, according to our landlord…

Great! Will look to do more of this where I think there is value add.

Thanks for confirming – great to have some on the ground confirmation of the trend.