A lot of you enjoyed last week’s 3 Key Takeaways on Singapore’s Retail / Office Outlook.

So I figured I would continue the format this week.

These are shorter than our Saturday deep dives, yet allow me to share my insights on standout events for the week.

Whether you love it or hate it, just share in the comments below so I can improve the format going forward! ????

*Stocks MasterClass Launch Promo ends on Sunday, 31 October!*

Sign up now and get freebies worth $500:

- 3 Months Subscription to the Highest Tier of Patreon (worth S$200). Get full access to the FH Stock Watch, FH Portfolio, and Premium Exclusive Articles!

- Complete e-Book on How to Invest in REITs (as a Singapore Investor) (worth S$200).

- Complete e-Book on How to Invest in Private Real Estate in Singapore (worth S$100).

Our launch promo is always the best promo – so don’t miss it! Find out more here!

Basics: What is going on? Why is the new consortium outbidding Keppel for SPH?

This week I wanted to talk about the Rival Offer for SPH.

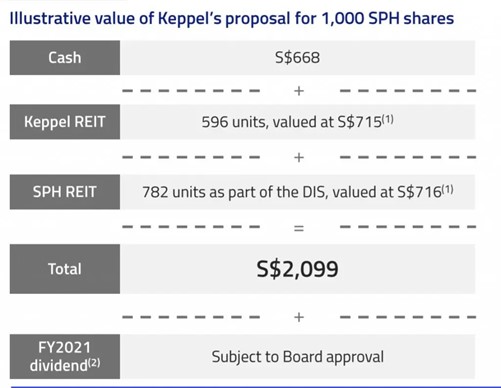

You know how Keppel offered $2.099 per share to privatise / buy out SPH back in August 2021?

Well, Cuscaden Peak has now swooped in with a $2.10 all cash offer for SPH.

The ownership for Cuscaden Peak is:

- 30% – Adenium Pte. Ltd. (“APL”) (a wholly-owned subsidiary of CLA Real Estate Holdings Pte Ltd (“CLA”))

- CLA is an independently managed portfolio company of Temasek Holdings (Private) Limited.

- 30% – Mapletree Fortress Pte. Ltd. (“MFPL”) (an indirect, wholly-owned subsidiary of Mapletree Investments Pte Ltd (“Mapletree”))

- Mapletree is an independently managed portfolio company of Temasek Holdings (Private) Limited.

- 28% Hotel Properties Limited (HPL)

- 12% Ong Beng Seng (managing director and majority shareholder of HPL)

New Offer is better than Keppel’s Offer? All Cash Deal!

At first glance of course, the new offer looks to be better than Keppel’s offer.

Keppel was offering to buy out SPH with a mix of cash, Keppel REIT units, and SPH REIT units.

Whereas the new Offer is pure cash, which is obviously superior.

You take out the uncertainty over how the REIT units will trade in the interim, and you also avoid any dilution on the REITs short term.

It’s why Keppel REIT’s price went up after this was announced.

The price is also $0.001 higher, but the big one for me is the all cash offer.

3 Key Takeaways on the Rival Offer for SPH

3 Key Takeaways for me:

- New Consortium has better synergies with SPH?

- $34 million break fee for Keppel?

- Will Keppel walk away?

New Consortium has better synergies with SPH?

The big question now is whether Keppel is going to come back with a higher offer.

To answer that, we need to understand how much each party can pay. Which is determined by who has better synergies with SPH.

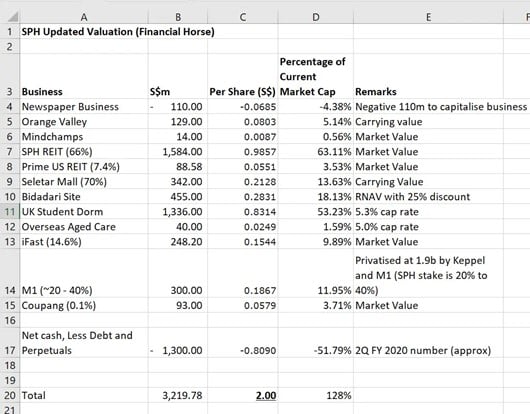

You can see the main assets held by SPH below (from my valuation done earlier this year), it’s basically a mix of real estate and infrastructure assets.

Synergies with Keppel

Keppel has really good synergies because the real estate assets of SPH can go into Keppel Land and Keppel REIT, while the infrastructure assets synergise well with Keppel Infrastructure (which co-owns M1 and part of the Genting Lane Data Center with SPH).

So I can see why the deal makes sense for Keppel.

Synergies with New Consortium

The new consortium is equally interesting.

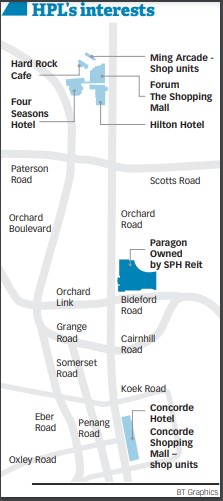

Hotel Properties Limited is a real estate player, which runs hotel chains such as Four Seasons, Hilton International, InterContinental Hotels Group and Marriott International. It also manages its own portfolio of hotels under brands such as Hard Rock Hotels and Concorde Hotels & Resorts.

More interestingly, it owns a bunch of properties along Orchard Road, so they synergise well with Paragon (SPH REIT’s crown jewel).

The Temasek Entity (CLA Real Estate) owns property group CapitaLand, real estate assets in Australia and investments in the life sciences sector, and is the majority owner of CapitaLand Investments (the development arm of CapitaLand).

Whereas Mapletree is Mapletree Group, which owns and runs the Mapletree Group of REITs.

So this new consortium can easily break SPH up for parts – with the real estate assets split amongst them.

Interestingly, I think there may be even better synergies for the new consortium than for Keppel.

And with 3 parties on board, the financial demand for each player is not as significant. Risk exposure is significantly lower for each of them.

So from a theoretical perspective, I would think that this new consortium can pay a higher price than Keppel.

$34 million break fee for Keppel?

Keppel’s buyout offer has a $34 million break fee.

In other words – if SPH turns down Keppel’s offer for another offer, they need to pay Keppel $34 million.

So Keppel now needs to decide whether they want to improve their offer.

They can either:

- Keep the Cash + Keppel / SPH REIT offer, but up the price, or

- Switch to all cash, and increase the price above $2.10

Of course if they do, the new consortium has the right to improve their offer as well.

And then SPH needs to decide whether to (1) accept Keppel’s offer, or (2) pay the $34 million break fee and accept the new offer.

That said, when the acquisition size is $3.4 billion, I doubt if they will make the decision based on a $34 million break fee.

Will Keppel walk away?

The big question now is whether Keppel is going to come back with a revised offer and spark off a bidding war.

But the fact that this consortium has backing from both CLA Real Estate (owned by Temasek) and Mapletree is very interesting to me.

This suggests that there could be some deeper, behind the scenes action I am not privy to.

It would make more sense to me for Keppel to collect the $34 million break fee and walk away, and let the new consortium buy out SPH, and then break it up and distribute.

I could be wrong though.

Like I said, I don’t know what I don’t know here.

I’m sure there are plenty of frantic discussions going on this weekend.

It would be really interesting to see what happens next.

Love to hear your thoughts!

*Stocks MasterClass Launch Promo ends on Sunday, 31 October!*

Sign up now and get freebies worth $500:

- 3 Months Subscription to the Highest Tier of Patreon (worth S$200). Get full access to the FH Stock Watch, FH Portfolio, and Premium Exclusive Articles!

- Complete e-Book on How to Invest in REITs (as a Singapore Investor) (worth S$200).

- Complete e-Book on How to Invest in Private Real Estate in Singapore (worth S$100).

Our launch promo is always the best promo – so don’t miss it! Find out more here!

Think the only takeaway is how poorly managed SPH has been.. buying all sorts of assets without a clear strategy & direction. Leading to significant discount on NAV (remember when it was near $1?).. and shown so clearly when both bidders for SPH are looking to buy at near NAV, break it up into pieces and derive synergistic value from the parts.

At one point (many moons ago) SPH was S$6.50 per share.

Agree with you. Badly managed end up with a rojak portfolio which I think only someone as big and diversified as Temasek can manage the split and allocate to the different sons. Probably hard to attract anyone else to bid. Got to think what to do with rojak assets after winning the bid.

Ya true, that’s a good takeaway too haha.

Some weird stuff going on here recently. It’s hard to see the logic of Keppel Infrastructure Trust owning M1 (which is a poorly performing business), and now this deal where two Temasek controlled groups “bidding” against each other. SPH has long appeared to be mish-mash of businesses with mediocre performance and lack of focus. A lack-lustre media business and an also-ran property business. Hopefully, the successful bidder will break it up and extract some value.

It looks like whoever wins, they’re likely to break it up for parts to realise the synergies. Charlito raised a good point below on this showing how rojak the portfolio is.

It’s not Keppel Infrastructure Trust but Keppel DataCentre Reit that invested in M1. It’s another complicated arrangement by Keppel. KDC will get 11% return through the bonds or perpetual securities, not really a direct investment. Another unknown company actually invested in M1. Something like that, can’t remember too complicated details. LOL. So you need to verify the details.

I think for the next few years the property business is a better bet than most other businesses. Given that SIA abd the aviation sector will be a drag on TH properties will contribute to alleviating the drag

Actually I would have thought that aviation will do well in the coming years (from an earnings perspective) because of the recovery, at least when compared to the COVID levels. Property did very well the past 10 years, but I’m starting to have some doubts on how well it can perform going forward, relative to other asset classes.