I received a great question from a Patron recently:

Hi FH,

So I’ve lucked out after working a few years in tech and got a job at one of the FAANGs. My salary increased exponentially as a result, I am looking at 16k/month (this is before including the stock components).

I’m also awarded an additional $100k USD of stocks that will be vested across 4 years.

I’m 30 yo.

No debt, no property.

I plan to get married in 1-2 years time, so I need to keep in mind the big home purchase that will be coming up.

I was invested in equities last year but have gone full cash since.

I have 100k in CPF and 100k split as follows:

- 75k cash (previously in stocks, currently in money market funds)

- 25k income (bonds + REITS)

I’m currently spending about $2k a month. This means if my lifestyle doesn’t inflate, I’ll soon be sitting on quite a bit of cash from my income that I’m not sure what to do with.

In terms of how to spend/invest in salary, I’m thinking of the possibility of using a part of it to purchase a condo now. This is since resale HDBs might get more expensive in 1-2 years, and BTO is already out of the question due to income ceiling. After mortgage I’ll still have money to invest.

Is this a good plan, or are there better ways to plan this?

In particular I am choosing between:

- Buy property now

- Invest my salary into SSBs/REITs/stocks first given the market lows then cashing out to buy property in 2024 when I get married.

I’d like to know if you were in my shoes how would you allocate/invest this monthly salary?

Also – Should I cash out on the FAANG stocks when they vest every year or keep them for as long as possible?

$20k/month Salary, $240,000 a year

First off – congratulations to the FH Patron.

Some quick numbers:

- $16,000 a month base salary

- $3,000 a month in FAANG shares (vesting each year)

Throw in employer CPF and you’re looking at a $20,000 a month nominal salary.

Or $240,000 a year.

Fantastic stuff for a 30 year old.

How much cash do you need for the Condo?

It wasn’t clear what kind of condo he was looking to buy.

I suppose if you want something comfortable and can last you until you have a kid of two, you probably want something around the $2 million range.

At this price, you can get:

- 1200 sqft resale condo at 1600 – 1700 psf

- 900sqft brand new condo at 2200psf (approx. new launch prices)

If you’re tight on cash maybe you can go lower, but I suppose at $20,000 a month salary this shouldn’t be a big problem.

How much cash upfront?

With a $2 million condo, you’re looking at:

- $500,000 cash for deposit (assuming you borrow the max 75%)

- $70,000 for stamp duty and expenses

- $120,000 for reno and appliances

If you rent it out first – then you probably only need $600,000 cash upfront.

He has $200,000 cash saved up

The Patron has $200,000 cash saved up now.

He needs to save another $400,000.

Let’s assume the wife contributes $200,000.

That leaves a $200,000 shortfall.

How long to save up another $200,000?

Currently he makes $240,000 a year nominal.

Deduct off:

- Tax (20-30k)

- Expenses (2k a month, 24k a year)

- CPF-SA/Medisave (not accessible)

It means he can save about $180,000 a year.

To cover his $200,000 shortfall, would take approx. 1 year – or mid 2023.

Can he afford the 2 million condo today?

Many people mix this one up – but you always look at personal circumstances first, before you look at macro and price trends.

No matter how attractive the investment may be, you don’t make it if you cannot afford it.

From the analysis above, buying a $2 million condo now is probably a bit of a stretch for him. He just doesn’t have the cash at the moment.

He will in a year or so though.

If he decides to buy a cheaper $1.5 million condo though, he would need about $425,000 upfront (excluding reno because he can rent it out first).

At $425,000, he already has half of it saved up, so if his spouse contributes about $200,000 he can go out and buy the property tomorrow.

So it’s probably workable at $1.5 million if he wants.

My views on how the next 1 – 2 years may play out?

To sum up my views on how the next 1 – 2 years may look like, I see:

- Rising interest rates, with sticky inflation

- Terminal interest rates of possibly 4.5% (US)

- This will crush risk assets

- At some point, Feds will have to find a way to live with inflation, otherwise the pain will be too much to bear

This means:

- Short term bearish on risk (with the exception of inflation hedges)

- Mid term you must take some risk to hedge inflation

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

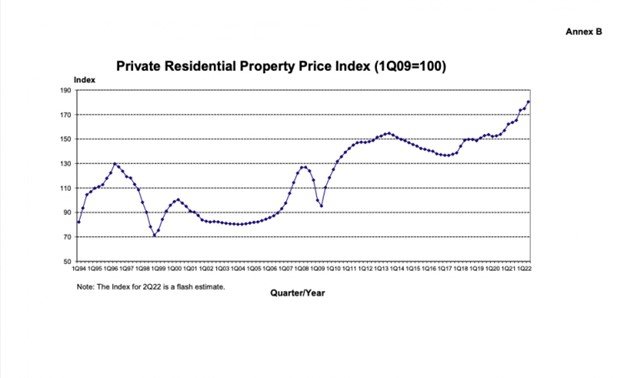

Will Singapore property prices go up or down?

So that’s the super high level picture from 10,000 ft.

But let’s zoom in – How does Singapore property perform within this backdrop?

On the one hand you have rapidly rising interest rates and an impending global recession.

On the other hand you have a very strong labour market, very tight housing supply, and soaring cost of construction.

To further complicate matters, demand/supply is artificially controlled by the government, while TDSR ratios mean that every buyer can afford it with a comfortable cushion.

And if prices drop – the government can dial back on cooling measures.

So while most people are calling for a property market crash due to rising interest rates, I’m really not so sure about this one.

My Personal Views on Singapore Real Estate?

I think it’s a genuinely tough call, that can go either way.

Gun to my head – I probably say that prices go up / stay where they are.

But sometimes in investing you should know when to not make a call.

And I think this is one of those times.

I don’t think you want to speculate on where Singapore property prices are going in the short term.

It’s kinda like oil.

I think oil is going higher with a 3 – 5 year timeframe. But where oil will be in 6 months, I frankly have no clue.

I see Singapore property the same way.

You want to play the long term secular trend, not the short term price fluctuation.

Will stock / REIT prices go up or down?

This is equally tricky.

But at least you don’t have to worry about the Singapore government intervening.

As shared last week, you probably need to split it up by asset class.

I think long duration assets like growth tech or Treasuries probably go down further with rising rates, but may bottom at some point.

Inflation hedges like oil could do well though.

I think there are lots of opportunities in this market, for the selective investor. I just wrote an article on Patreon this week on where value lies in this market.

But the tricky part – is that he needs his money in 2024 to buy the property.

If you buy stocks / REITs now, will you be able to cash out within 1 – 2 years at a profit?

Not an easy call.

It will depend on your skill as a trader.

What would I do?

For obvious reasons, this should not be taken as financial advice.

If this were me though, in the exact same situation?

I think I would start looking at properties now. And if I find one that I like and is decently priced (and that I can afford), I just buy it.

Sure I can try to wait for 2023/2024 and see if rising rates hit the property market, but if I get the call wrong I may be buying at even higher prices.

I probably wouldn’t want to take the bet on this one.

Not when it comes to my matrimonial home.

Rest of the money?

Even if I take a $1.5 million mortgage, I still have $9,000 a month left after expenses and tax.

That’s pretty decent, almost $100,000 a year to invest.

And what that cash, I would actively invest.

I probably hold elevated cash positions in the short term, and look to deploy that cash selectively over the next 12 months.

What exactly to buy?

Much will depend on the inflation outlook, and how and when the Feds respond.

You can also check out my views on where value lies, and what stocks / REITs I’m keen to buy on Patreon.

But hey – that’s just me.

What if you want to time the Singapore property market? Or don’t find a property you like?

Okay what if the Patron doesn’t find any property that he likes?

Or what if he wants a $2 million property instead.

Or what if he wants to try to time the market, and buy in 2024 instead?

In such a case, I think there are 2 options:

- Active invest

- Put it all in cash

Active Invest

I truly, truly don’t know if you can buy and hold a basket of stocks today, and cash out in late 2023/early 2024 at a profit.

Sure, there is value in this market now. Lots of great buys if you know where to look.

But there is very likely to be a global recession in 2023.

So you don’t want to get greedy holding onto them for too long.

If you only had a 1 – 2 year timeframe, I think you probably need to active invest.

Be careful with what you’re buying, watch the macro signals carefully, and be aggressive in cutting risk.

Long story short – this is a tricky path.

You may be a good software engineer, but you need to decide if you are as good a trader.

Put it all in cash

If you’re not confident with your ability to active trade, then I say why take the risk?

Why gamble your future, and your ability to buy your matrimonial house, on your ability to trade?

Many people do this because they have no choice.

They need to earn the cash to afford the house.

But for this Patron, he literally can chuck all his income into a bank account or SSBs, and still have completely no problem buying the house in 2024.

It’s a win vs win more kind of situation.

You know, when Brazil is up 3-0 against Germany but they decide to go all out and make it 10-0.

Sure maybe you pull it off. But maybe you throw the whole game?

Why take the risk?

Downside of playing it safe – Inflation is a silent killer

The downside with playing it safe of course, is that if inflation is sticky, you might be running uphill here.

You save another $200,000 but the house price goes up by $200,000.

And you’re back to square one.

So yeah, I completely get that is a downside.

So between the two paths, only you can decide for yourself which is more suitable.

Closing Thoughts: Cash out on FAANG stocks… or hold?

The final question was whether to cash out on the FAANG stocks when they vest.

Now for obvious reasons there are a ton of decisions for him to be made above.

For eg. what house to buy, when to buy, how to invest the rest of the money etc.

This decision needs to be made in conjunction with those.

For me though? I think I would cash out.

I don’t think FAANG stocks today have the same upside they had 10 years ago.

If I were working in a FAANG today, I think they’re just a maturing business at this point. It’s hard to see the stock doing a 5x from here.

Okay maybe you keep the stock as a sense of loyalty to your employer, to help you perform your job better.

That’s completely fine.

But from a pure returns standpoint?

I think if I were a 30 year old today with the rest of my life to invest, there’s probably better places to deploy the cash.

This decade is shaping up to be very different from last decade, and I wouldn’t see a need to have so much of my net worth tied up in the FAANG.

But hey – I don’t know which FAANG this is.

There are some that more equal than the others. So who knows.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

As always, this article is written on 23 July 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.