I received the following question recently:

Hi Financial Horse,

I am XXX, 33 old years, just started to invest.

I have currently invested about $250,000 since the beginning of this year when the market decline. As crisis is around the corner, I try to do dollar cost averaging in small amount.

My current portfolio is down about -19%, but I am all right with it because I have only invested about $250,000, and I still have $1.25 million cash haven’t invest and DCA yet.

I am planning to invest $800,000 – $2.0 million each year back into my portfolio depending on the performance of my business too.

The reason I choose to do 100% equity investment is because I am 33-year-old and I don’t intend to take out the funds until 20 years later.

I also all right with the market volatility, my equity investment target is hope to build a $50 million – $100 million 25 years from now.

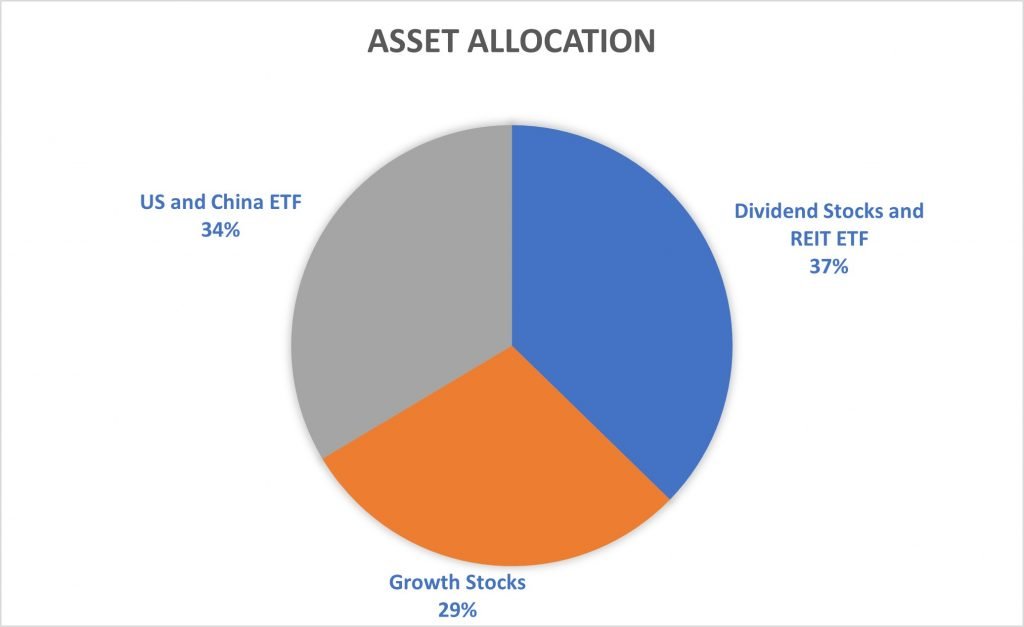

I am currently looking to invest in the following asset allocation:

- Dividend stocks and REITS ETF (Syfe) – $500k

- 11 individual growth stock (mostly are blue chip giant) – $550k

- USA and China ETF – $450k

Look forward to hearing from you soon and wishing you a pleasant day ahead.

The asset allocation proposed by the reader is set out below (I stripped out some of the purchase amounts for confidentiality reasons):

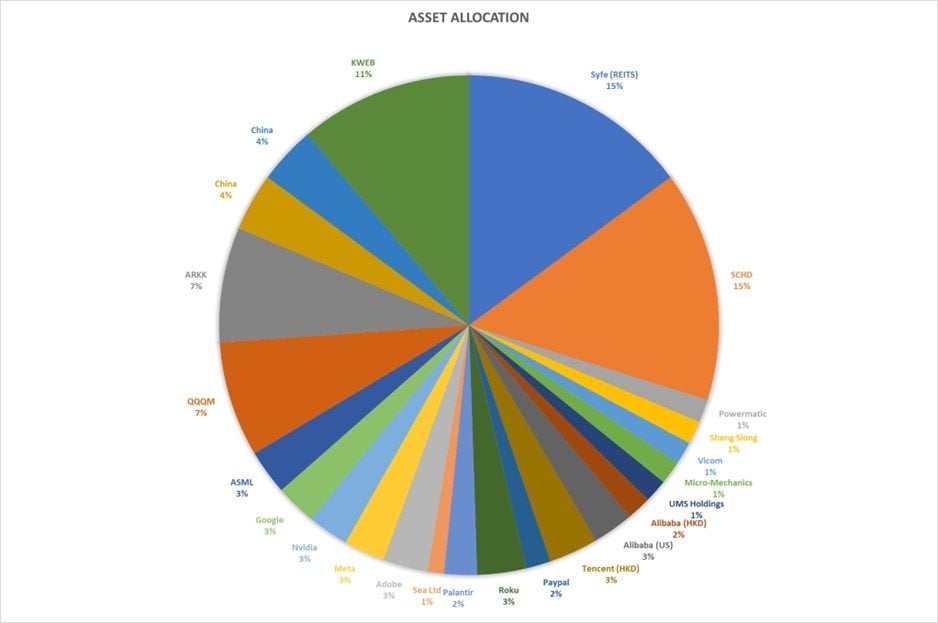

1) Dividend stocks and REITS ETF (Syfe) – $500k

- Syfe (REITS) $200,000

- SCHD $200,000

- Powermatic $20,000

- Sheng Siong $20,000

- Vicom $20,000

- Micro-Mechanics $20,000

- UMS Holdings $20,000

2) 11 individual growth stock (mostly are blue chip giant) – $550k

- Alibaba (HKD) $21,300

- Alibaba (US) $35,500

- Tencent (HKD) $42,600

- Paypal $21,300

- Roku $42,600

- Palantir $28,400

- Sea Ltd $14,200

- Adobe $39,050

- Meta $35,500

- Nvidia $35,500

- Google $35,500

- ASML $39,050

3) USA and China ETF – $450k

- QQQM $100,000

- ARKK $100,000

- China $50,000

- China $50,000

- KWEB $150,000

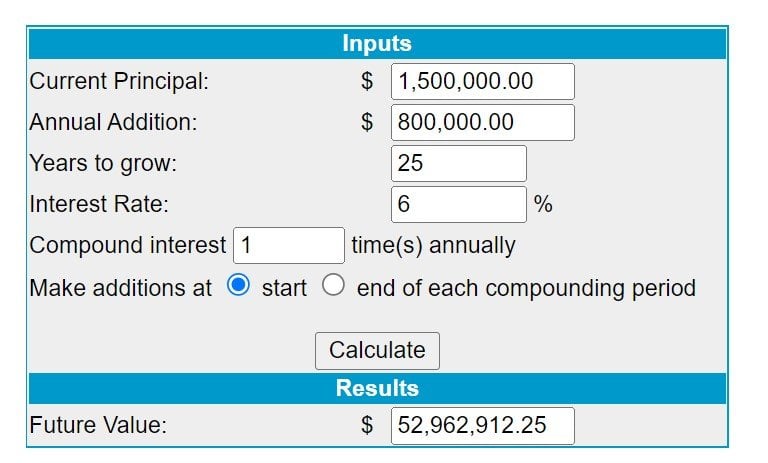

33 year-old earning $800,000 a year – How much annual returns to achieve $50 million in 25 years?

Let’s assume he starts with $1.5 million, and invests an additional $800,000 for the next 25 years (lower end of the numbers provided).

At a 6% return a year, he will end up with $52.9 million after 25 years.

In other words, he just needs to achieve 6% returns a year on his investment portfolio, while investing the $800,000 a year, and he will achieve his goal after 25 years.

So that should be our starting position.

Be careful investing like it’s 2012…

In last week’s article, I cautioned against investing like it’s 2012.

A lot of you asked me what I meant by that.

What I meant, was to not fight yesterday’s battles.

My fear is that when the time comes, investors are going to buy assets that benefit from low inflation and low interest rates.

Think tech, growth stocks, REITs etc.

When I saw this portfolio, that was the immediate thought that jumped into my mind.

If you bought this portfolio back in 2012, you would have made a ton of money over the next 10 years.

Invest for the future, not the past

BUT – this portfolio is designed to last 25 years.

This portfolio will need to last until the middle of this century.

With a long tech, long growth, long REITs portfolio like this, you are betting that the next 25 years will look a lot like the past 10 years.

Now I have my own views on what this decade will look like (higher interest rates, sticky inflation), and many of you may not agree with me.

But you need to at least be alive to the possibility that the future may look very different from the past.

How would I invest… in 2022?

Now designing a static portfolio that can preserve wealth, and still achieve 6% returns over the next 25 years, is not easy.

It’s why you always hear of rich descendants losing their wealth over a lifetime – it’s much harder to hold onto money than you think.

Now as an investor, there are 2 key risks that we face:

- Losing money (the principal we start with)

- Not generating enough returns to achieve our goals

Most people focus on (2), but in reality, I encourage you to start thinking about (1) first.

Focus on not losing money, and the rest will take care of itself.

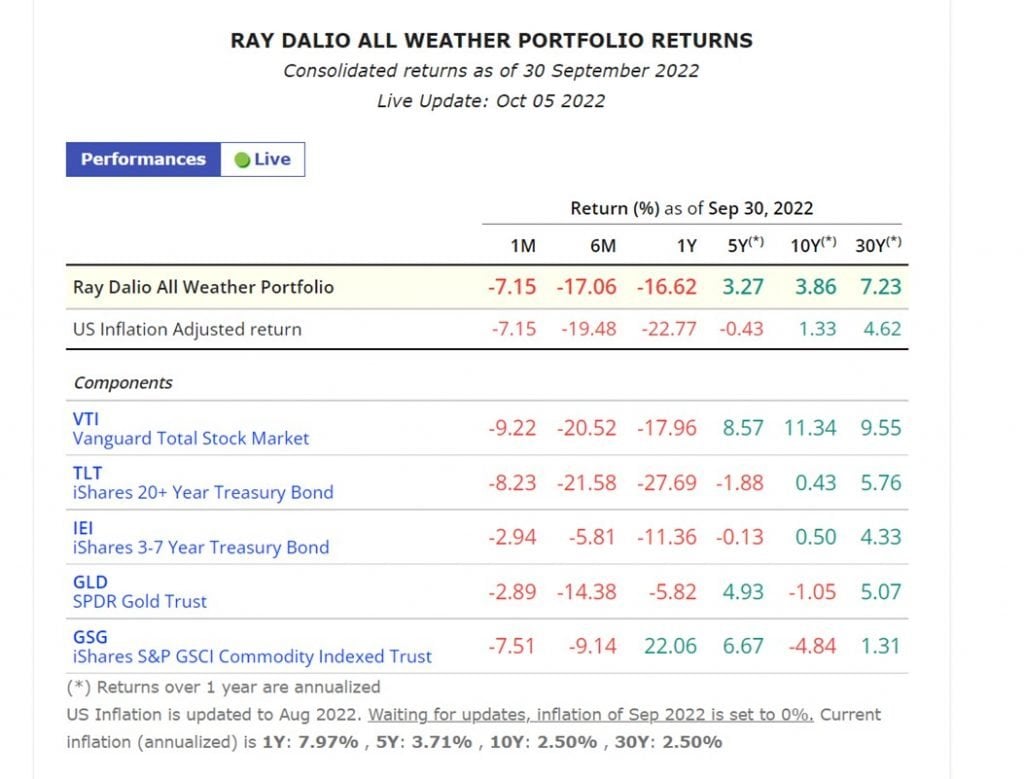

Long Term Asset Allocation – All Weather Portfolio

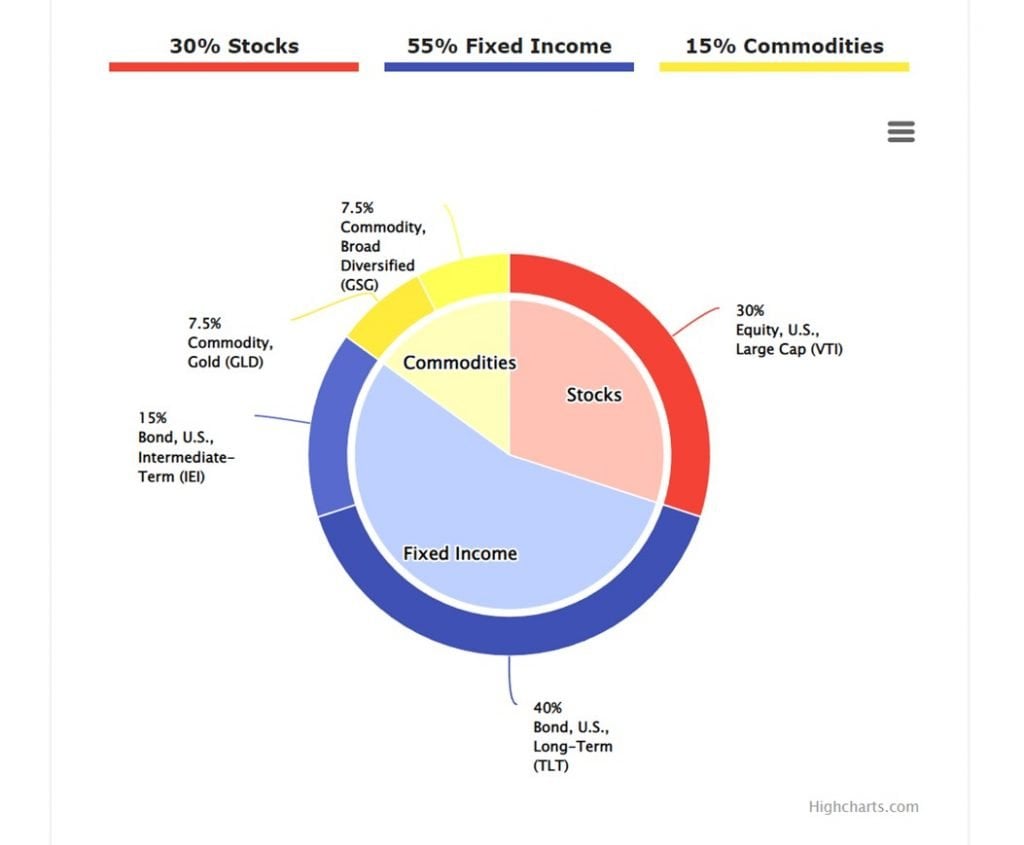

If you’re designing a portfolio to last 25 years with minimal intervention, the best place to start might be Ray Dalio’s All Weather Portfolio:

The thing to note about the all-weather portfolio is that it is designed to perform well over ultra long term periods.

Think 10 – 100 year periods.

Which means that in the short term (2 – 3 years), it can, and will underperform.

This year being a good example – where rising interest rates have crushed the long bond position, and the all-weather is down a whopping 17%.

The all-weather is also designed for US investors, which would make less sense for Singapore based investors as it exposes us to significant FX risk.

Win big, lose big…

Now I know the reader asked for a 100% equities portfolio.

But if you asked me, I really don’t see myself running a pure equities portfolio in a scenario like that.

If you’re Stanley Druckenmiller and you can read global macro like a book, while making big gutsy bets to back it up, then yeah of course go 100% equities and layer on leverage on top.

But for us mere mortals, I think if you’re starting with a $1.5 million portfolio at age 33, and reinvesting $800,000 – $2 million a year the next 25 years.

Do you really need to take on that kind of risk?

It seems to me that much of the risk already comes from the business income, on being able to earn that $800,000 – $2 million a year the next 25 years.

So to double down on risk on the investments, looks like a win big, loss big kind of move to me.

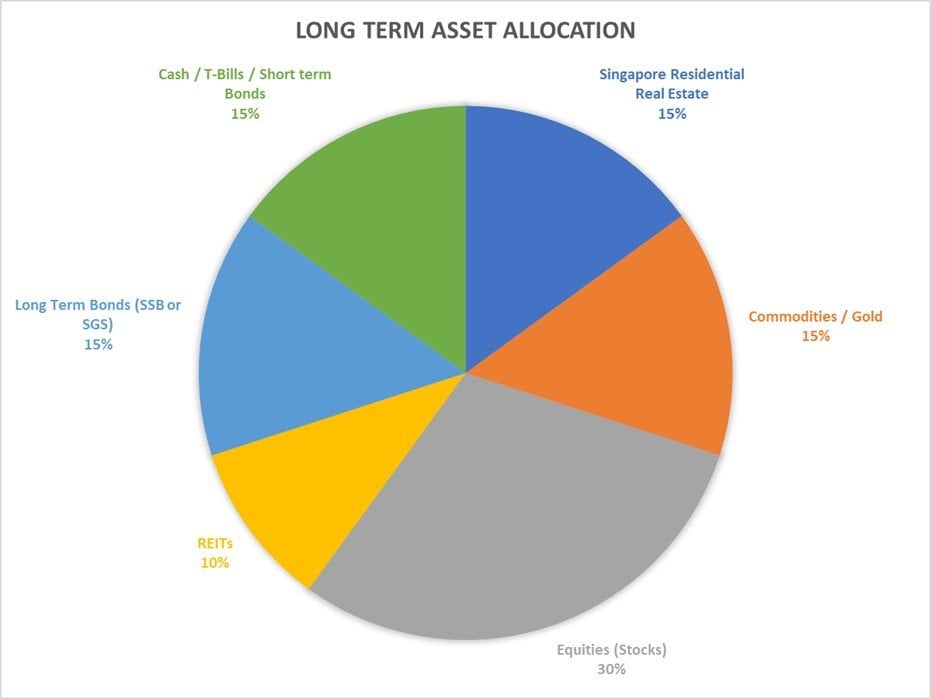

How would I do it? Invest for the next 25 years as a Singapore Investor?

If this were me, I would mix in a number of asset classes, looking something like this:

|

Asset Class |

Percentage (%) |

|

Singapore Residential Real Estate |

15.00 |

|

Commodities / Gold |

15.00 |

|

Equities (Stocks) |

30.00 |

|

REITs |

10.00 |

|

Long Term Bonds (SSB or SGS) |

15.00 |

|

Cash / T-Bills / Short term Bonds |

15.00 |

|

Total |

100.00 |

How to invest a portfolio like this? (as a Singapore Investor)

Using a hypothetical $100 million portfolio, heavily simplified:

- Singapore Residential Real Estate – $15 million

- Commodities / Gold – $15 million

- Commodities ETF (GUNR) – $12 million

- Gold ETF (GLD, GDX) – $3 million

- Equities (Stocks) – $30 million

- S&P500 (SPY) – $15 million

- STI – $5 million

- Hang Seng Index – $5 million

- Stock Pick – $5 million (or more depending on the individual)

- REITs – $10 million

- CICT – $5 million

- Ascendas REIT – $5 million

- Note: Alternatively one can just buy a REIT ETF or Syfe REIT

- Long Term Bonds (SSB or SGS) – $15 million

- Long Term Singapore Government Securities – $15 million

- Cash / T-Bills / Short term Bonds – $15 million

- Cash – $2 million

- Fixed Deposit – $3 million

- T-Bills – $10 million

General Thought Process on the investment portfolio

Let me share some quick thoughts on the thought process.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Why 15% allocation to Singapore Residential Real Estate?

I know some of you love Singapore Residential Real Estate, some of you hate it.

Some of you are going to say 15% is too much allocation, some are going to say 15% is too little.

What I will say, is this.

If you’re a Singapore investor, looking to preserve (and grow) wealth over the next 25 years, residential real estate is something you need to at least consider.

But whether the right allocation is 15%, or 40% – only you can answer for yourself.

Property is not liquid, transaction costs are very real, and if you are living in it it’s a big inconvenience to cash out.

Some of you may want to live in a GCB, and some are happy with a HDB (and a huge investment rental portfolio).

To each his own.

Singapore Residential Real Estate from an investment perspective?

Yes, interest rates are going up, and this will put pressure on prices.

But look beyond the short term – demand-supply dynamics are tightly controlled, while TDSR and cooling measures mean local buyers are not overextended.

With real estate, you get to borrow up to 75% of the property valuation.

You will pay higher interest rates, but after adjusting for inflation, I still think you come out on top over a 25 year period.

I do not see interest rates staying significantly above inflation for extended periods, the pain for the global economy would be unbelievable.

Why Commodities?

If we do indeed get inflation and debasement of fiat currency, commodities is probably the place I want to be (the other of course is real estate and stocks, but those come with their own complexities – rising interest rates for one).

Regular readers know that I think the demand for commodities this decade will go up.

The world is splitting into 2 blocs, and governments are going to finance a lot of infrastructure investment to make that happen. Not to mention the move to green energy.

Government spending is price inelastic and inefficient, and will crowd out the private sector.

All while a decade of underinvestment into commodities means supply cannot increase dramatically.

Commodities might just be the play of the decade for me.

I plan to write an article on Patreon on how to invest in commodities the coming week, you can sign up here if you’re keen.

Stock Pick or ETF

Now while I used primarily ETFs to illustrate the portfolio above, stock picking is perfectly fine as well.

Whether you stock pick or ETF, and how much to allocate to each, will depend on your level of sophistication.

If you’re new to markets, I suggest to put the bulk of your money in ETFs, and a small amount to stock pick and learn from your mistakes.

If you’re a financial markets veteran, then well, you’re probably better placed to decide than me.

If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates have moved there.

At S$15 a month you get the premium weekly market updates like this one.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get my full personal portfolio.

Don’t be penny wise pound foolish.

Think about how much you may have lost this year.

And how much you will lose in the next 12 months if you start buying too early.

Too much cash?

This is probably a legitimate concern.

Almost 30% of the portfolio is locked up in short term cash or long term bonds.

The thinking here is that if I am pulling in $800,000 to $2 million a year in disposable income, I am taking a lot of risk elsewhere just to earn that income.

Whether it’s a business or a high flying day job, there is a risk that income dries up one day.

To protect against that, and to allow me to continue taking risks, I want a healthy cash buffer.

Specific Comments on the Reader’s 100% Equity portfolio (Singapore Investor)

But hey this is just me.

If you want to YOLO into a 100% equity portfolio, frankly I can understand why.

Some of you may think my asset allocation is unduly conservative.

You will stay rich, but you won’t become filthy rich.

That’s a perfectly legitimate concern.

With that in mind, I wanted to share my views on the reader’s hypothetical 100% equity portfolio:

- Don’t invest like it’s 2012

- Too concentrated for a 25-year portfolio (unless actively managed)

- 24 Counters is on the high side

Don’t invest like it’s 2012

I talked about this above.

In investing, be careful of linear thinking.

Many investors look at the past 40 years of falling interest rates, and come up with a portfolio that does well in that climate.

And they backtest it from 1980 to today.

But the big macro cycles are cyclical, and last 30 – 40 years each time.

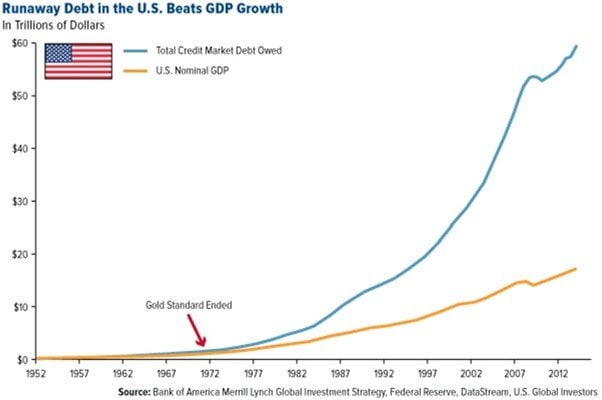

My view is that the long term debt cycle for the west, that started in the 1970s after President Nixon took the US off the gold standard.

That cycle is over.

And ever since COVID in March 2020, we’ve started a new long term debt cycle, with higher interest rates, and higher inflation.

In historical terms, don’t invest like it’s 2012.

Invest like it is 1950.

Too concentrated for a 25-year portfolio (unless actively managed)

Building on the point above – I just think this portfolio is too concentrated, to last 25 years.

This portfolio is long REITs, long tech, long growth.

It is a bet on interest rates and inflation staying low.

Sure, maybe you are right on this the next 5 years.

But will you be right on this for the next 25 years?

If you want to run a concentrated portfolio like this, you must be prepared to active invest.

You must be prepared to cut positions and reposition if global events prove you wrong.

If you don’t want to active invest, then you need to diversify.

You want exposure to the boring, ah-gong stocks.

Think banks, dividend plays, commodity plays, real estate, gold etc.

24 Counters is on the high side

For what it’s worth, I think 24 counters is too high for a retail investor.

It is not easy to keep track of the happenings of 24 different stocks, while still working on your day job or business.

Use ETFs to your advantage here.

If you want exposure to energy but don’t want to stock pick, just buy XLE.

Even if you want to stock pick, you can just buy S&P500 to form the bedrock of your portfolio, then layer on specific names on top.

Closing Thoughts: Do you want to get rich, or not be poor?

Think about it this way.

You need to invest all of your net worth over the next 25 years, in A or B:

- A has a 20% chance of 10x return, 80% chance of 90% loss.

- B has a 80% chance of 3x returns, 20% chance of 30% loss.

Which do you pick?

Do you want to get rich, or do you want to not be poor?

Of course in real life the choices are not black and white, but your answer to this question, says a lot about who you are.

It will depend on your life goals, and the amount you start out with.

Someone who is earning millions a year may not be satisfied with a mere $20 million in retirement, so he may want to double down on risk.

That’s perfectly fine.

Whereas a salary worker earning median wage may be satisfied with a HDB and car into retirement, and if his day job and savings can provide that security, why take unnecessary risk?

Perfectly fine too.

In investing – there is never a right or wrong. There is only what works for you.

So figure out who you are, and what you want out of your life.

Then invest accordingly.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Disclaimer: The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH,

These 2 lines seems contradictory:

1) Now I have my own views on what this decade will look like (higher interest rates, sticky inflation), and many of you may not agree with me.

2) I do not see interest rates staying significantly above inflation for extended periods, the pain for the global economy would be unbelievable.

Additionally, what % inflation did you consider for this line:

You will pay higher interest rates, but after adjusting for inflation, I still think you come out on top over a 25 year period.

Thank you!

I think it’s envisaging a situation of negative real rates.

Think inflation at 4%, interest rates at 3%.

That’s negative real rates, but in a climate of higher inflation higher rates.

Hi Horse, great post once again. I totally agree with your current mindset, as yields go up and stay high for at least the next 6 months, we should be spending time thinking ahead, the next 5 – 10 years etc.

On commodity underinvestment, the cuts by OPEC+ this week shows us just how inflexible commodities are right now. Any bump in the market, be it lesser supply or more demand, the market reacts instantly and looks the way it was in the first half of this year. And the Fed already said, they can only control demand. When this bout of inflation subsides (ok let’s not debate about whether its sticky or not), central banks are going to have to face up commodity supply side shortages. And what they decide to do, coupled with what governments decide to do, are going to define the next 10 years for us. A bumpy ride indeed!

Exactly right. OPEC+ this week was a gamechanger.

Powell wants to crush inflation by crushing demand, but OPEC+ showed they can easily cut supply too…

I think the most interesting thing is, what business is your reader in? I am curious to know what business yields 800K a year, which I can then either encourage my kids in the direction of, or to buy a business in that field. At 800k a year, his household would be among the <100 people in Singapore (cf. Singapore Household Income Statistics).

If I made 800k a year, I would definitely go for gated long-short hedge funds, art and overseas farmland. These go up even in down markets, and are oblivious to bear markets. Check out the returns on the art market at masterworks.io. Not to mention, bragging rights.

I believe he runs a business. It was shared in the email that he wrote in.

I think this chap is irritating. if he has so much money, he would have his own agents and financial consultants working for him. why disturb you? i thought FH is for the masses. masses so rich now? i damn poor sia

I suppose its just a way of getting alternative opinions. In any case, the answer here is helpful even for those with different levels of wealth, as it forces a more holistic thinking to wealth and net worth.

Why would anyone invest in STI any more? It goes sideways permanently. Sg economy has peaked just like many other developed nations. It is still primarily a banking /wealth hub after so many years of trying to diversify its economy. It will never produce a hugely *profitable * tech company like FANG. Neighbors like vietnam and Thailand are rising. You should go for DBS and blue chip reits.

Why real estate and not pure reits? Real estate is a headache to manage plus high fees , maintenance, the need to find tenants , illiquidity etc. you cannot get high returns since the govt will do cooling from time to time which sounds something like what China would do, I.e. govt intervention of “free market”.

Why not invest directly into infra ETF and green ETF since u think green energy is the way forward. But honestly I doubt we will move very quickly to green energy as it is still too costly for large developing nations . With high inflation or stagflation, moving to green is also hard for developed nations. Green infra development will be very slow for developed nations since labor cost is high. So far the leaders are no action talk only except China. Even trump/republican backed out of green deal. What do you think? Most green ETFs hold a large percentage of car makers like Tesla , Nio , etc and infra /energy providers which wont generate much profits going forward due to intense competition. But I ‘d probably still buy a small amount on battery related ETF since EVs will be in hot demand this decade and battery tech has some moat.

Yeah fair points.

I think this asset allocation was designed more to convey the idea on how to allocate wealth. And not so much the exact names. I do agree that there is room to improve on the stock / REIT picking.

In any case, someone who is realistically investing 30-50m in capital markets should probably look at getting a family office, it might become more efficient that way execution wise.

Hi FH, can do an article on SATS?

Ok, will look into it.

It looks ridiculous for someone making 800k/yr to get advice from public …unless he is talking about CNY…anyhow he already had the plan and who are we to say he is incorrect since he already more successful than 99.9% of us….obviously he seen something that we don’t :p

Siao lang prob just faking it. 800k a year is Crazy Rich Asian lmao.

U read ST? Businessman lost 18m in 8 years trusting investment advice from his bankers. Lots of rich but gullible people around, that’s why scammers having field day.