Man… what a week!

The biggest rate hike since 1994, an implosion in the crypto space, and JGB yields blowing up.

It’s starting to feel like the summer of 2008.

That sickening feeling you get that the tail risks are starting to build.

But when and where exactly it blows up, you have no clue.

I hate to say I told you so – but here on Financial Horse, I’ve been going on and on since Jan 2022 about how tightening liquidity will wreck financial markets this year.

Well – it’s playing out exactly as I described so far.

Given how things are playing out, it’s probably wise to start doing a bit of homework on what Dividend Stocks I want to buy if (when) the liquidity event hits.

Rules: 5 Best Dividend Stocks to buy in 2022’s Market Crash

Picture this.

We are now in Dec 2022.

The Fed Funds Rate is at 3.5%.

Stocks and financial assets have been crushed (or are in the process of getting crushed).

What do you buy, and at what price?

I’ll try to be as realistic as I can with the price targets. Nothing absurd like DBS at $5.

5 Best Dividend Stocks to buy in Singapore in 2022

1. Netlink Trust

Current Price: $0.93

Dividend Yield: 5.5%

Netlink Trust as a dividend stock is boring as hell.

I mean look at it’s share price, it has literally gone nowhere for 2 years.

But with my dividend stocks, the more boring the better.

As long as the share price is stable, it pays a good dividend, I am happy.

Netlink Trust owns most of the fibre connections in Singapore, and they “rent” out the connections to service providers like M1 or Singtel to use.

So every month that you use a fibre connection for internet at home, you’re paying “rent” to Netlink.

It’s the REIT of fibre connections.

Problems with Netlink Trust as a Dividend Stock

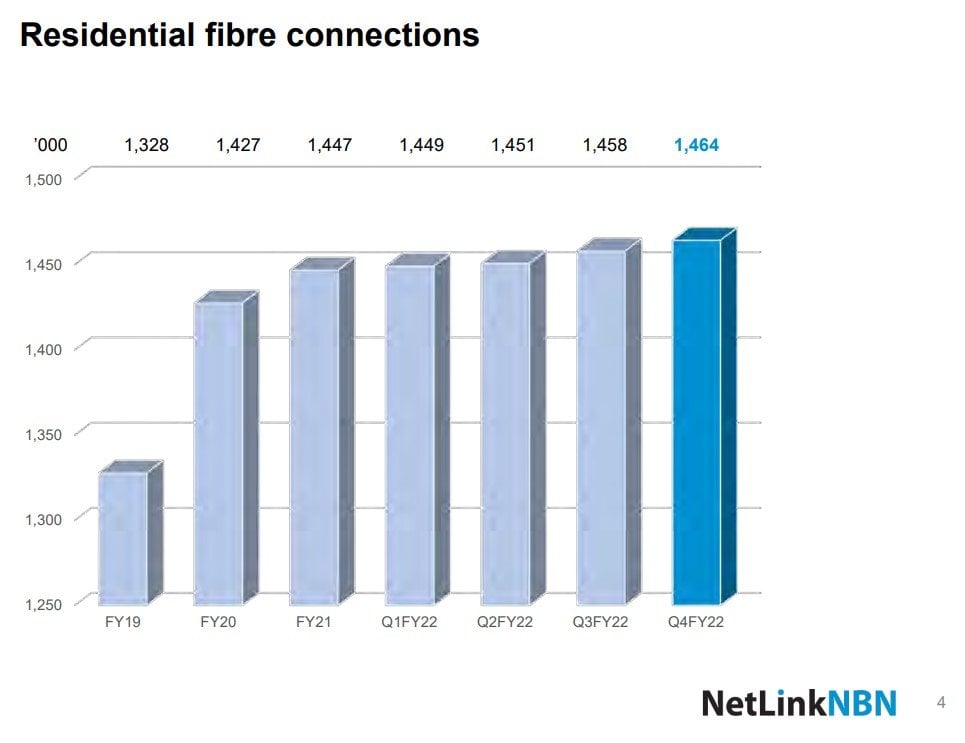

The problem though is that with a business like that, there’s only 2 ways to grow: (1) more users, (2) higher prices per user.

(1) is out because most of Singapore is already on fibre, so you’re basically just tracking population growth at this point:

(2) is also out because internet prices are tightly regulated in Singapore, and Netlink cannot raise prices without IMDA approval.

At best you’re looking at low single digit increase in prices each year.

That’s good for internet users, bad for Netlink investors.

Any tail risks?

A lot of you have been writing in with concerns about Netlink Trust’s rising expenses.

And yes absolutely – I agree this is a big tail risk.

If the underlying fibre has some issues that require big capex from Netlink, the dividend could get cut.

But I mean, there’s really no free lunch in this world.

If you want a dividend yield above the risk free, you have to accept some level of risk with it.

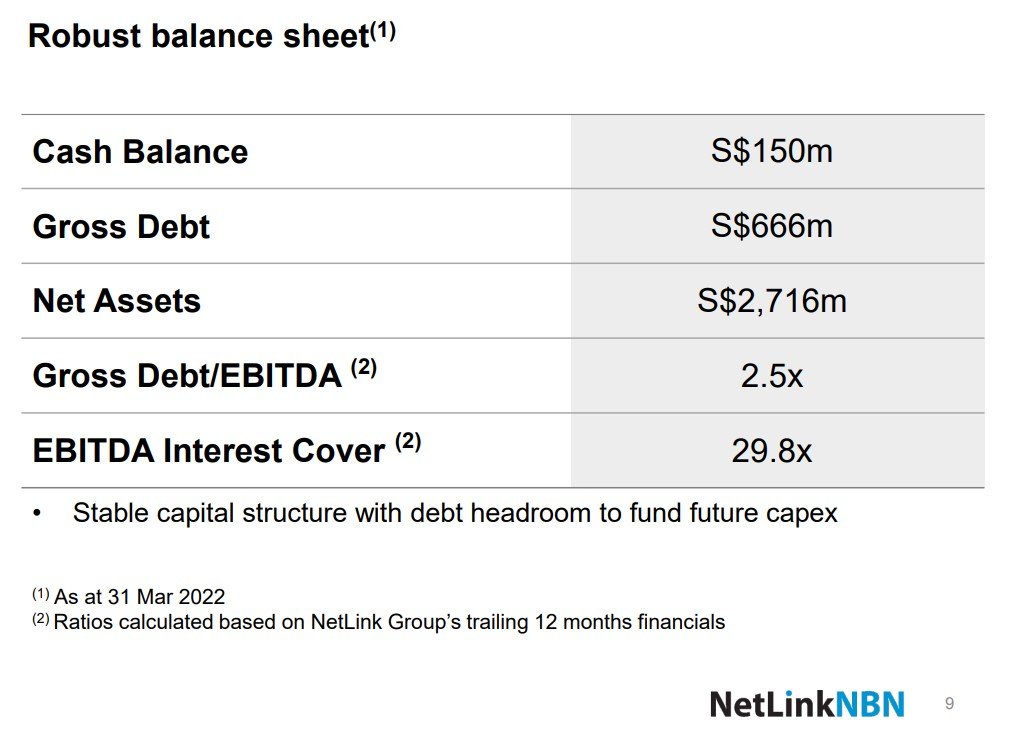

Netlink Trust does have a pretty rock solid balance sheet though, so that helps.

My Target Price for this Singapore Dividend Stock?

The tricky part about Netlink is figuring out the right price to buy it at.

The lowest that it went during the March 2020 liquidity crunch was $0.80.

If it goes there (6.4% yield) I am probably backing up the truck.

But more realistically, I think $0.85 might be good enough for me. At that price, it works out to a 6% yield.

That’s similar to what I’m getting on my Class B Astrea 7 Bonds, and broadly speaking I think the risk associated with both is somewhat similar.

Class B Astrea 7 is probably safer from a micro perspective (because of the diversification), but you do take on USD FX risk in exchange.

DBS Bank

Current Price: $30.11

Dividend Yield: 4.7%

Price/Book: 1.35x

I don’t think DBS Bank needs any introduction.

It’s the biggest bank in Singapore, Temasek backed, and probably one of the best ways to invest in Singapore’s economy.

Oh… and did I mention that it pays a 4.7% dividend yield at current prices?

That’s REIT levels of yield.

Will DBS Bank cut its dividend in a recession?

I always get the question of whether DBS Bank will cut its dividend in a recession.

I don’t know what you guys are smoking, but in my mind the answer is a resounding hell yes.

You see banks are a tail risk kind of business.

In the good times you make truckloads of profit lending out money at a spread (against your borrowing cost).

In the bad times though – your borrowers default.

So that $1 billion loan you were making 1% spread a year on? You only recover $100 million, and you eat a $900 million loss.

Just look at what happened to DBS’s dividend in 2020:

And don’t forget COVID 2020 wasn’t even all that bad (from a loan default perspective) because the government stepped in and bailed out the entire economy with emergency support.

DBS currently has a 50% dividend payout ratio.

If we get a real recession, and we don’t get the same level of policy support we did in 2020, things can get ugly.

What price would I buy this Dividend Stock at?

I still remember writing an article about selling DBS Bank earlier this year.

DBS Bank was trading at $36 then, and I said that at low 20s I would be a buyer.

I remember being laughed out of the room then.

Well… who’s laughing now?

For the record though, I still don’t know for certain if DBS Bank will go back to the low 20s.

Much will depend on the inflation outlook in 2H 2022, which still isn’t very clear right now.

All I know is that the last time I backed up the truck, DBS was below $20.

Book value is $22, so if it goes anywhere near there I would consider buying (approx. 6.5% yield at those prices, assuming no dividend cut).

If it doesn’t, I’ll probably just hold my existing position and buy the REITs instead.

Will DBS Price drop more?

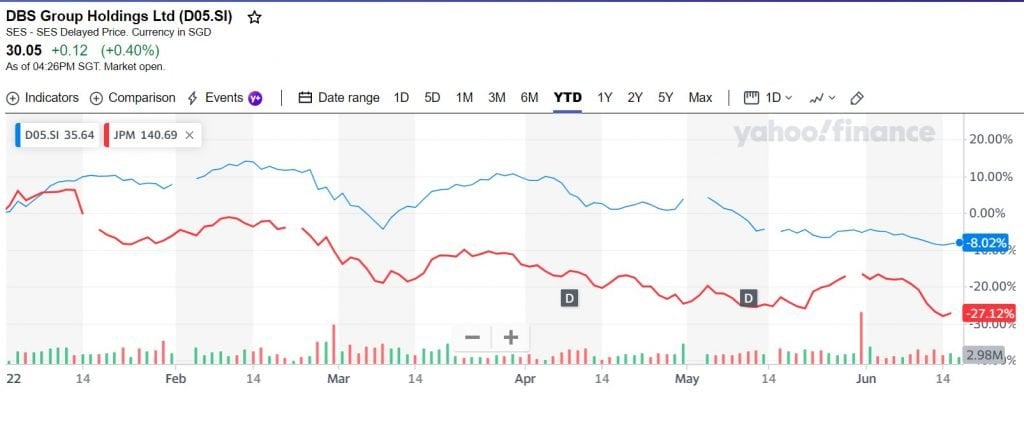

Food for thought – here’s the year to date chart of DBS (blue) against JP Morgan (Red).

DBS is massively outperforming JP Morgan, down 8% vs 27% for JP Morgan.

Is Piyush that much better a CEO than Jamie Dimon? Or do DBS prices need to come down?

You tell me.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Shell PLC

Current Price: GBP2,227.50

Dividend Yield: 3.4%

Okay I cheat.

Shell isn’t exactly a Singapore dividend stock.

But I wanted to add a dividend stock that can hedge inflation in the event that inflation refuses to come down.

And the options were either Olam, or going international. I went with the latter.

In my mind – Oil is the purest hedge on inflation.

Oil powers the entire physical economy. Everything goes back to oil.

Need bunker to power your cargo ships? Gasoline to air freight cargo? Petrol to drive your trucks and cars? Diesel to drive your farming tractor?

Heck, even the fertilizer to grow crops comes from the Haber process which requires natural gas (and loosely linked to oil).

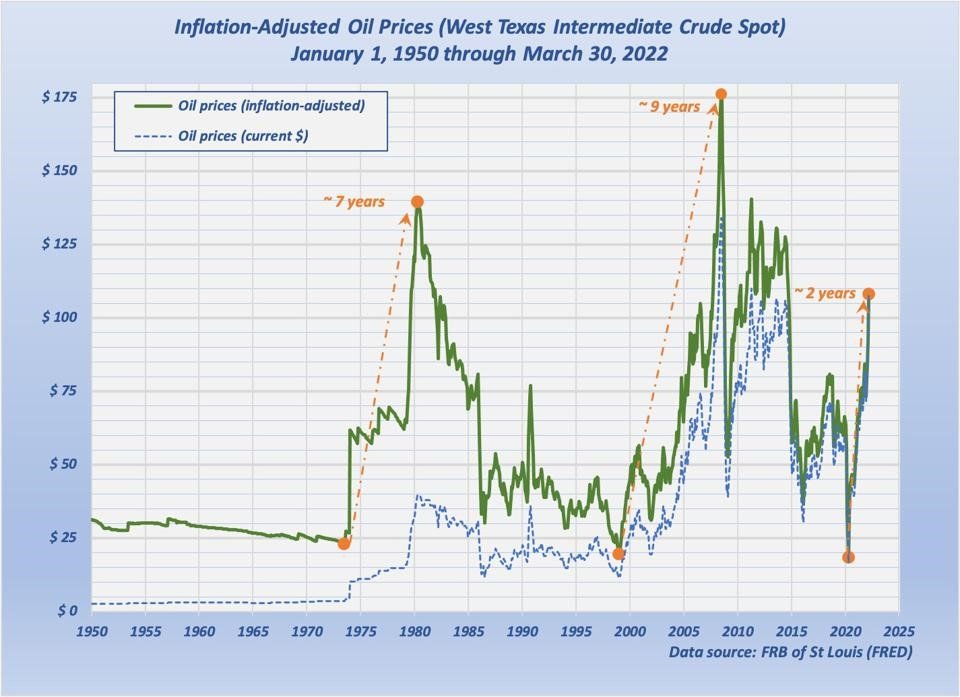

But FH… Oil Prices are at record highs

If you look at the long term oil price charts, you’ll find they are close to all time highs.

But if you adjust those numbers for inflation, the charts tell a very different story:

The 2 previous mega cycles for oil, in the 1970s and 2000s, lasted almost an entire decade.

We’re only 2 years into the current oil cycle, which indicates there could be more room to run.

Structural Demand-Supply mismatch

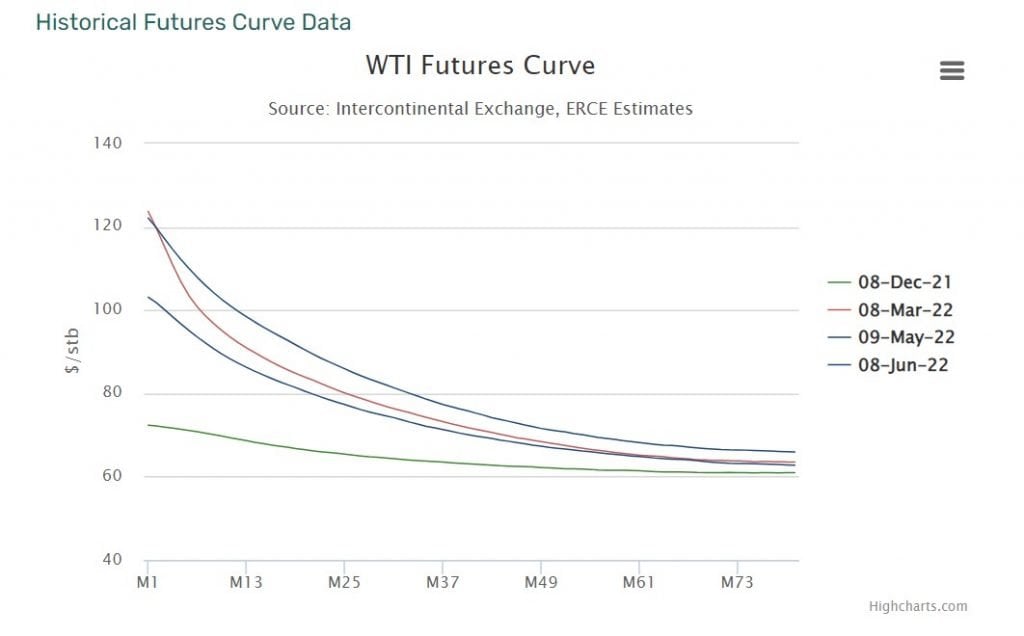

This is the oil futures chart, which shows you how the market is pricing oil from tomorrow all the way to 6 years out.

And from Dec 2021 until now, the price of oil for immediate delivery has soared from $70 to $120. But the price of oil for delivery in 5 years out?

Barely even budged.

Oil Producers make decisions on long term prices

Imagine you’re an oil executive.

Any new investment in oil supply will not come online for at least 3 to 5 years.

And the market is telling you that oil prices in 3 to 5 years are still very low.

At the same time, politicians keep going on and on about ESG and how net zero emissions is the way of the future.

Are you really going to go to your board and ask for approval for that new $5 billion dollar oil rig that only comes online in 5 years?

Get out of here.

Will oil stocks drop?

But that’s the mid term, 3 – 5 year picture.

In the immediate, 6 – 12 months ahead, we still have a very aggressive Federal Reserve, and a very real chance of global recession.

Personal view – I think commodities and real estate are the last domino to fall in this cycle.

If (when) that happens, I would be looking to buy.

I think oil in particular could do very well this decade, because of underinvestment in supply. All the Russian sanctions are really not helping either. And I don’t think the transition to green energy will be as straightforward as made out to be.

It’s tough to call how much the price can drop, so I’m just going to play by ear for this one. Patreon followers will get regular updates on my thinking on Patreon.

Other Dividend Stocks to invest in Oil?

I picked Shell because if you buy the London listed stock there is no dividend withholding tax for Singapore investors.

And price wise it hasn’t appreciated as much as the US oil majors like Exxon or Chevron.

If you really wanted to be cute the China oil plays like CNOOC or Petrochina are worth looking at too.

There is China risk, and sanctions risk, but they do trade at a discount to their international peers.

CapitaLand Investment

Current Price: $3.62

Dividend Yield: 4.1%

Full disclosure that I’ve taken profit and sold my entire position in CapitaLand Investment.

I like the stock, and the dividend is decent at 4.1% too.

But I still think real estate is going to be one of the last dominos to fall in this cycle.

As a real estate investor there’s nothing you fear more than rising interest rates, and the pace of increase this year is the fastest its been in 25 years.

Doesn’t hurt to cash out and watch things play out a little.

What price will I buy this Singapore Dividend Stock?

But at the right price, I could be tempted to buy back in again.

My target price is $3, which would work out to a 5% yield.

It’s probably a bit aggressive being a 20% drop from here.

But like I said, I really don’t know how things are going to play out.

I’m just going to stay nimble here.

If CapitaLand Investment sells off, I buy it. If the REITs sell off instead, I buy the REITs instead.

I’ll take my cues from the market for this one.

Ascendas REIT

Current Price: $2.76

Dividend Yield: 5.4%

Okay I get that Ascendas REIT is not a dividend stock but a REIT.

But frankly, this list just didn’t feel right without including a big name REIT in it.

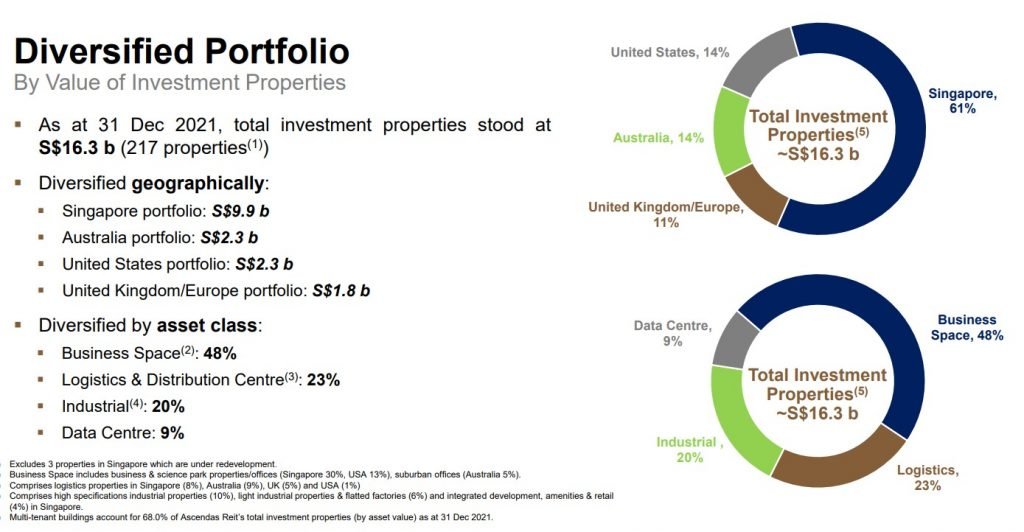

The bulk of the portfolio is Singapore industrial properties, which is exactly what I wanted to get exposure to as I’m underweight this asset class.

The line in the sand for me is 6% yield, which is about $2.5.

I would be watching closely for that price, which corresponds to the bottom in 2018.

That said, in a true market crash there’s no telling how low prices can get.

Ascendas REIT went as low as $2.2 in March 2020, so that’s another level to watch.

5 Best Dividend Stocks to buy in Singapore in 2022

To sum up, the 5 Best Dividend Stocks to buy in Singapore in 2022:

- Netlink Trust

- DBS Bank

- Shell (or other oil major)

- CapitaLand Investment

- Ascendas REIT

Why buy Singapore Dividend Stocks?

The thinking behind dividend stocks of course, is that these tend to be mature, cash flow heavy businesses.

In a decade that may be inflationary (potentially stagflationary) in nature, dividend stocks are a good hedge.

Unlike growth stocks, the dividend (and cash flow) provides a bottom for stock prices.

That said, I don’t think dividend stocks are the only way to play the eventual recovery.

At some point, tech stocks could be a good buy too. As are commodities, gold, growth, small cap, crypto etc.

If you’re keen, you can check out my stock / REIT watchlist on Patreon. Will be updating it this weekend given how much prices have moved, and will revise all my personal price targets as well.

You also get access to my full personal portfolio.

Closing Thoughts: When to buy?

It’s been a monster of an article, so I want to wrap up.

Been getting a lot of questions on when the market will bottom.

What I will say, is that I think we’re very close to peak rates. I think after this final flush out, we’re probably close to cycle high for yields.

If you want to long bonds as a tactical trade, the time may come soon.

But it’s not so straightforward to extrapolate from there to the bottom in equities.

In 2008 equities didn’t bottom until 1.5 years after the peak in rates.

How long it takes in 2022/2023 – I frankly have no clue. Nobody does.

You will need to monitor how the tail risks play out in the months ahead. Key would be the inflation outlook, and how the Fed responds.

As always though – will be sharing my views on Financial Horse every step of the way! So stay tuned!

As always, this article is written on 17 June 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Wrong date bro. Unless you’re from the future

“As always, this article is written on 18 Sep 2022 and will not be updated going forward.”

Thanks for the spot, have corrected!

Hi FH,

Do you think this crash will be worse than 2020 March?

Do you mean in terms of magnitude, speed of decline, or length of decline?

March 2020 was a very quick crash because the economy went from 100 to 0, and then from 0 to 100 from all the Fed QE. The current one is a more traditional bear market driven by tightening monetary policy, albeit with inflationary elements thrown in.

So the response to both will need to be different. I would expect this crash to be more drawn out.

Great article, FH! I think we will have time to buy-in…this correction is much needed given the excesses of recent years and the Fed cannot help because of inflation so my guess is that this will be a 2001 dotcom type bust which will play out over the next 1.5 years. I suspect we may be looking at a peak to trough of 50% or even more in the US market. Unfortunately, there seems to be nowhere to hide. Bonds hit by rising interest rates, Cash hit by inflation. Singapore stocks have held up pretty well so far and China stocks have been hit already so may actually be a safer place to be than other markets. But overall, hang on to seatbelts for the next 1.5 yrs and be prepared to wait 3-5 years for partial recovery, up to 8 years for full recovery.

Next one to go could be crypto. It has shown itself to be neither an inflation hedge, a volatility hedge, a store of value or a medium of exchange in this crisis. Warren Buffett, Ray Dalio, Jim Rogers, Ben Bernanke, Christine Largarde, Bill Gates et al are all on record saying it is worth a grand total of zero and this crisis may prove them right. Agree that last to fall will likely be commodities and property although I think residential property will fall first and we will see a meaningful correction by end of next year. When mortgage rates go above 4% by next year, investors will find that rental cannot cover interest and 30,000 new apartments will be completed and ready to rent before end of 2024. With new apartments so tiny compared to the ones they replaced and thus unattractive for renters and the economy likely to be in recession within the next 2 years, it is questionable if the rental demand is there.

If not, owners will be stuck with empty apartments and paying 4% mortgage interest so we could see a perfect storm for property.

Agree with your picks with the caveat that I still think one should look more international for opportunities rather than being too local market focused. The big sale is coming…will people have money to buy? Opportunities for wealth destruction and creation are both side by side.

Well, after the events of the past week, it looks like Crypto has gone as well! And will go further as the year plays out. 😉

Interesting point on residential property – do you mean SG or US residential? I actually thought SG residential property may hold up comparatively better because the supply constraints are still very strong.

Agreed on international, I deliberately kept this article more “local” as that is what most readers ask for. For the Patreon content it tends to be more international in nature.

Hi FH,

I actually mean SG residential. There is a tsunami of completions of previous Enbloc condos hitting us by 2024 with 30,000 new completions so supply will be plentiful very shortly. The supply constraints is last 1-2 years is a short term one due to supply from Enblocs taken off the market and late completions of replacement condos due to Covid.

So while developers land banks are depleting, the actual conpleted condos will be hitting us soon in a big wave. Look at recent BT article for figures each year from now till end of 2024. We start seeing first impact 2H this year, a big surge next year and the final surge in 2024. 30,000 new condos being completed and handed over. Or if unsold, developer ABSD sales will follow.

That’s very interesting, will take a closer look at the supply figures. Thanks for rasing this CMC!

Valid comment however this holds for new condos/BTO which due to ABSD for condos and ownership restrictions for BTOs are mainly limited to Singaporeans.

The rental market is out of sync with buy/Sale segment and is so high now, because of foreigners/ PRs who are renting as they cannot buy (BTO) or are holding off buying (Condos) due to higher ABSD levied.

You might point out that what is new in this, higher ABSD has been there for significant part of last 10 years.

What has changed now is exodus from HKG of HNWIs who are ready to pay highest rent. So I would expect rental to stay high in the short term and may match the higher mortgage payments for rented apartments/ Investment properties. However for self stay apartments things may get difficult with higher mortgage rates in coming years.

That’s a fantastic observation, thank you for highlighting this point. I have similar views as well – for rental to stay strong in the short term, and house prices to hold up generally. But mid term, I think the increasing supply and rising interest rates are quite a potent headwind.

Dear FH,

Another great article from you. Easy to read & to the point. Thank you.

Regarding Netlink Trust, i think they might be having a meeting with IMDA this year, i think they need to nail down the next 5 year price for Year 2023 to 2027 soon. Depending on the outcome of their discussion, maybe this sleepy stock price might move a bit before it goes dormant again. Agree with you. As long as it is stable, boring is a good thing.

Cheers

Thanks for raising this! Quite a few readers have pointed this out too.

Agree that any potential sell-off, whether driven by IMDA news or macro level events, could be a good opportunity to add.

Hi FH. What do you make of the compression in spreads between SREITs and Singapore government bonds. Is there a mis pricing there?

Yes, I think REIT yields will need to go up in response. Might see the blue chips like Ascendas at 6% yield before this cycle is over.

Hi FH,

Did you consider Keppel Infrastructure Trust? It’s dividend yield is more than 6%, and its business model very resilient. Whether recession or not, it’s services are required, and I would imagine the prices are already locked in for long periods, although I may be wrong. The one thing to look out for may be costs, as energy costs are escalating, and there may be a margin squeeze.

No KIT is one of those BTs that I’ve never taken a closer look at, so I cannot really comment. Been hearing good things about it though, so I probably should.

DBS dropped like all other shares bec of inflation and interest rate hikes and recession fears. As financial writer I cannot believe you got the cheek to use this to support that you advised on the spot many months back. You are a real joke.

This was the exact concerns I wrote about back earlier this year though: https://financialhorse.com/is-it-time-to-sell-dbs-bank-stock/

Although back in Jan/Feb this was pre-Ukraine war. Which only made the situation worse…

One more dividend stock: ST engineering… Increased stable dividend and the company decide to change to quarterly payout instead!

Also, Astrea 4.35% is now near to $1 par price.. if drop to below $1, perhaps can go for this bond until it is redeemable or back to $1.05 again?

Yes ST Engineering has been on my watchlist for the longest time too, but never pulled the trigger. Agree that at the right price it could be a very interesting pickup!

Agree on Astrea, lots of interesting opportunities are starting to open up. Downside risk is that if prices go down further, the capital is locked in until it is redeemed next year. So is the return of ~4-5% acceptable for a one year holding in the scenario? Given how the next 6 months may play out?

Hi FH,

Will Astrea 4.35% definitely redeem next year or is there a risk that they will not redeem since they have an option to pay an additional 1% and redeem in 2028?

In a high interest rate environment, perhaps they would not redeem? I recall reading something along the lines that they may have to redeem if the funds set aside for the A-1 tranche have already been realized but am not sure.

Hi CMC,

The way their waterfall is structured – all the money received goes into the reserve account to pay off the Class A Bonds. So even if they choose not to pay (assuming the legal docs allow them to elect to do so), they cannot use the money for any other means.

So yes – it would appear there is an arbitrage opportunity in buying the Class A at 1.018, and getting the coupon + principal back next year!