REITs have fallen out of fashion recently.

Lots of interest over growth stocks, China stocks, Crypto, but very little for REITs.

I love REITs, and they form a key part of my portfolio, so I wanted to address that today.

We’ll look at the 5 best small to mid cap Singapore REITs to buy now (in 2021).

To mix things up – No CapitaLand or Mapletree REITs, and 5% yield minimum.

Why only Small to Mid Cap Singapore REITs? Why no CapitaLand or Mapletree?

Now I get it.

Nobody wants to read a list of “Top 5 REITs to buy in Singapore” where the top 5 REITs are:

- Mapletree Commercial Trust

- CapitaLand Integrated Commercial Trust

- Ascendas REIT

- Mapletree Industrial Trust

- Mapletree Logistics Trust.

The large, blue chip REITs have been covered to death, and everybody knows about them.

In fact the last time I wrote an article on the best REITs to buy, I received a suggestion to “diversify away from writing about ah gong reits all the time?”.

Point taken :,(

So if you want a safe, 4% yielding blue chip REIT backed by a Temasek co, you can check out our previous article.

For today’s REIT list, we’re going to mix it up:

- No CapitaLand, Mapletree or Frasers REITs

- More than 5% yield (trailing twelve month).

There’s no free lunch in investing

You do need to know however, that there’s no free lunch in investing.

If you want a higher yield, you have to take on more risk.

There’s a reason why I keep talking about CapitaLand and Mapletree REITs on Financial Horse. They’re safe, they have a good sponsor, and they make money.

That’s why I buy so much of them.

But, for investors who already own a portfolio of “ah-gong” REITs, and are looking to add in more risk to their portfolio (barbell approach), you’ve come to the right place.

Sidenote on Barbell Approach: The way you do it is that you assemble a portfolio of safe blue chip REITs on one hand, and the riskier higher yielding small cap REITs on the other. And you weight the allocation to each depending on your risk appetite – to give you your desired yield and risk.

BTW – we share commentary on Singapore Investments every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

5 Best Singapore REITs to buy now (Small – Mid Cap REITs) (2021)

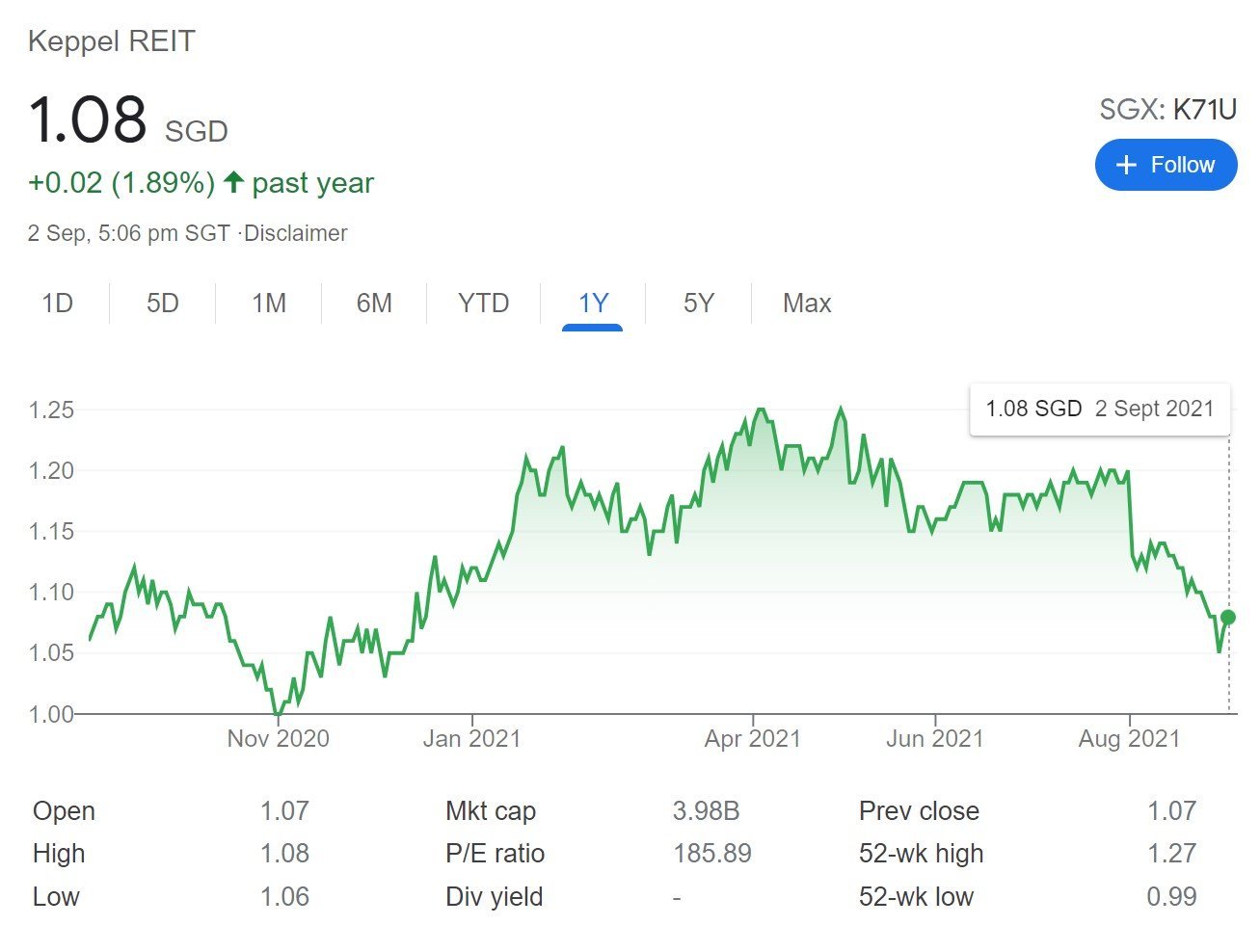

Keppel REIT

Market Cap: $3.98b

Price/Book: 0.78

Trailing 12 month yield: 5.51%

Leverage: 35.2%

Occupancy: 96.5%

I know, I know.

Keppel REIT? Has FH lost his mind?

Personally I’m not a fan of Keppel REIT too.

I’ve never been a fan of their portfolio, and I’ve never liked the sponsor.

But then Keppel went ahead and announced they were buying SPH with $1.1 billion in Keppel REIT unit.

That’s a massively dilutive transaction, and Keppel REIT promptly sold off 15%.

There’s a saying in real estate where “There’s no such thing as bad real estate, only a bad price”.

At today’s price, Keppel REIT is probably worth looking at.

What I like about Keppel REIT?

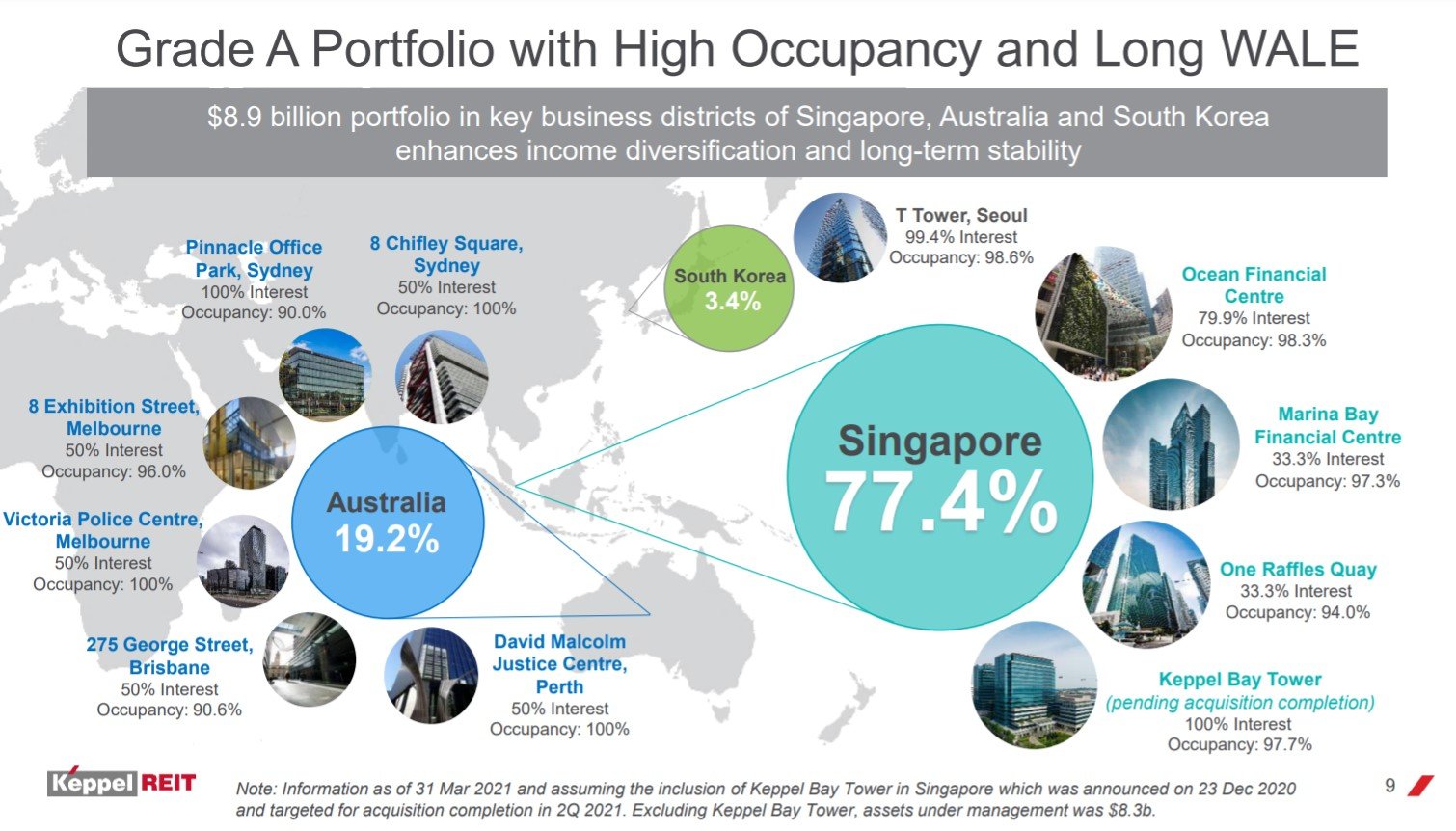

Decent Office Portfolio

It’s not exactly a best in class portfolio like CICT, but it’s still a very solid office portfolio.

77% of Keppel REITs assets are in Singapore – big names like Ocean Financial Centre, Marina Bay Financial Centre, One Raffles Quay, Keppel Bay Tower.

With the rest spread between Australia and Korea.

Operational results are decent, with a broadly diversified tenant base.

What I don’t like about Keppel REIT?

Keppel as a Sponsor

I’ve never been a big fan of Keppel as a Sponsor. I think they’re fine, but not CapitaLand or Mapletree level.

Case in point – Keppel REIT recently acquired Keppel Bay Tower from their Sponsor (Keppel), with income support!

Sure the deal is DPU accretive (but NAV dilutive) even without rental support, but I never like it when a REIT does an acquisition with income support. You never really know if the yield will stabilise post-income support.

CEO Resigns

The CEO also recently announced that he would be resigning “to pursue other opportunities” which was interesting to say the least.

Dilutive impact from SPH Acquisition

And the big one – Keppel bought SPH for S$2.20 billion, to be satisfied with S$1.08 billion in cash and the remainder in units of Keppel REIT.

That’s $1.156 billion of Keppel REIT shares moving into the hands of SPH shareholders, who may just decide to sell them on the open market.

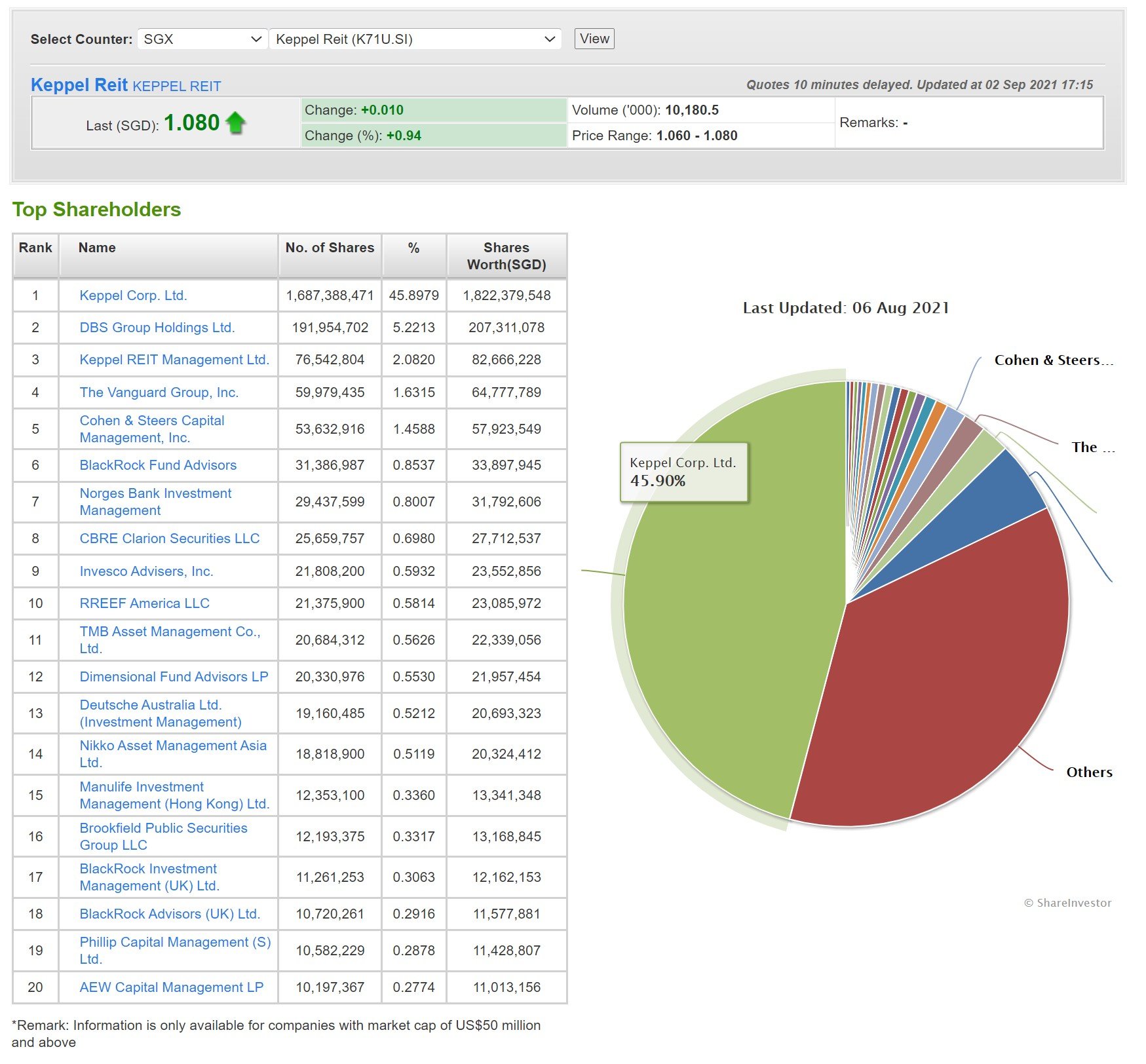

After this – Keppel’s stake in Keppel REIT will drop from 45.9% to 20%.

That’s massive, and shouldn’t be underestimated.

But price is good?

Because of all this – the price has sold off, and Keppel REIT is now trading at a 22% discount to book, and a 5.5% trailing yield.

The office exposure is going to be weak in the next few quarters because of COVID work from home trends, but at this price it could be worth averaging into a position.

Although the more cautious investors might want to wait for post SPH acquisition. Who knows what the SPH shareholders are going to do with their newfound Keppel REIT units?

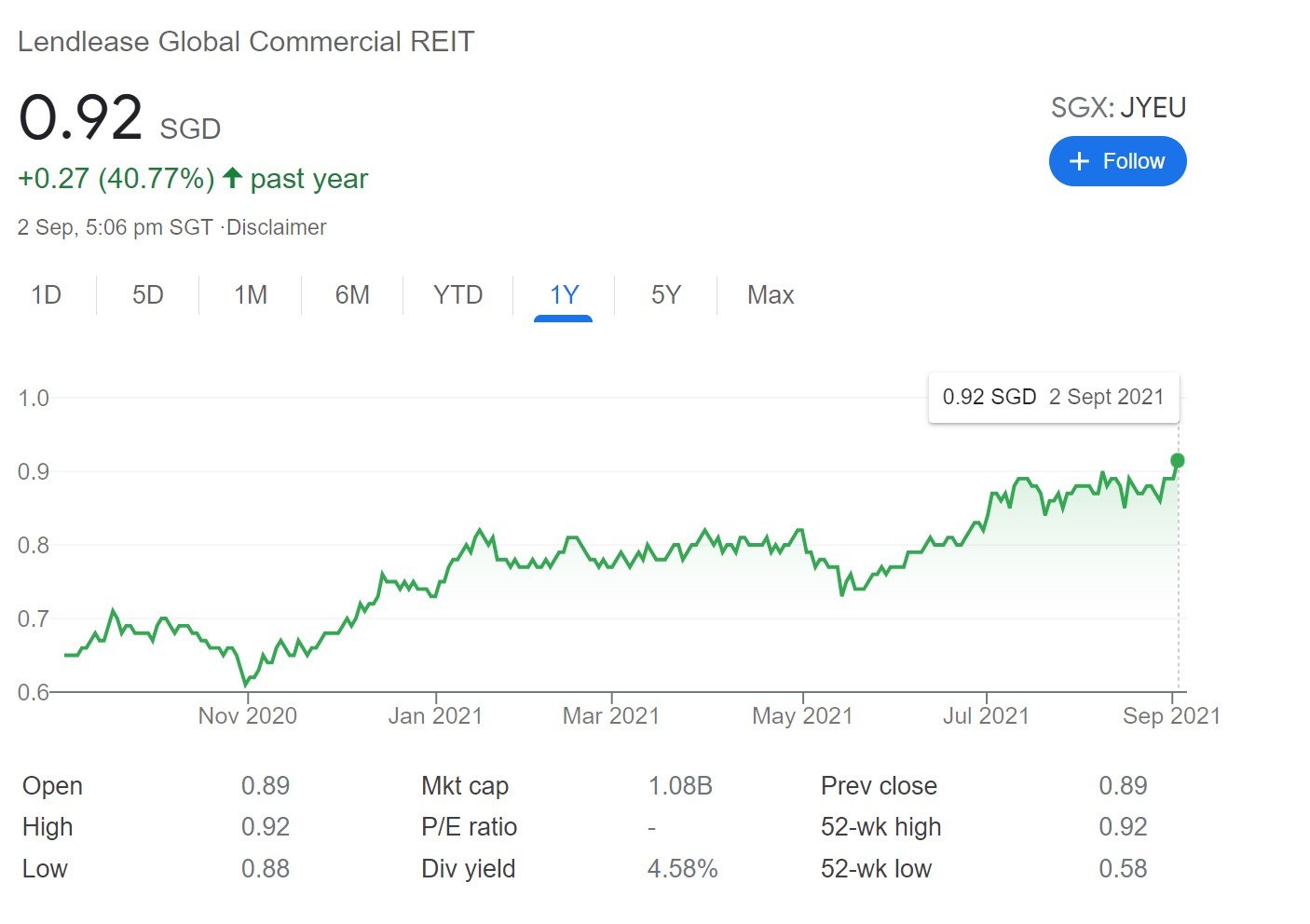

LENDLEASE Global Commercial REIT

Market Cap: $1.08b

Price/Book: 0.93

Trailing 12-month yield: 5.25%

Leverage: 35.2%

Occupancy: 99.8%

What I like about Lendlease REIT

All 3 properties held by Lendlease REIT are great:

- 313@ Somerset, retail mall in Singapore

- Sky Complex, Grade A office in Milan

- Jem, retail mall in Singapore

313@ Somerset, retail mall in Singapore

313@Somerset is probably one of the better malls in Orchard today.

Very strong tenant mix, very unique target audience (younger crowd), and no single large anchor tenant exposure (unlike Starhill Global REIT with Takashimaya).

Direct link to Somerset MRT, and plans to redevelop the Grange Road open air carpark. What more do you want?

Always packed when I’m there too, but could just be me.

Sky Complex, Grade A office in Milan

Real estate is a local business, and not being Italian, I really cannot judge how good Sky Complex is.

That said it’s locked into a long term lease to Sky Italia (12 + 12 year), which provides very good stability – almost like a bond.

Jem

Jem – Need I say more?

Lendlease REIT will hold a stake of up to 31.8% in Jem going forward, which was overwhelmingly approved by unitholders. That’s about the strongest mandate I’ve ever seen.

Jem is just a fantastic mall, and if Lendlease REIT can hold 100% even better.

Pipeline

With Lendlease as the sponsor, there’s also a strong pipeline:

- The rest of Jem

- Paya Lebar Quarter

- Parkway Parade

All great malls.

What I don’t like about Lendlease REIT

The only problem with Lendlease REIT is the price.

I liked Lendlease REIT a lot more when it was in the 70s and 80s range, which it was at for much of the past 12 months.

But once the Jem acquisition was announced, I suppose it’s fair that this REIT should trade at a premium to book.

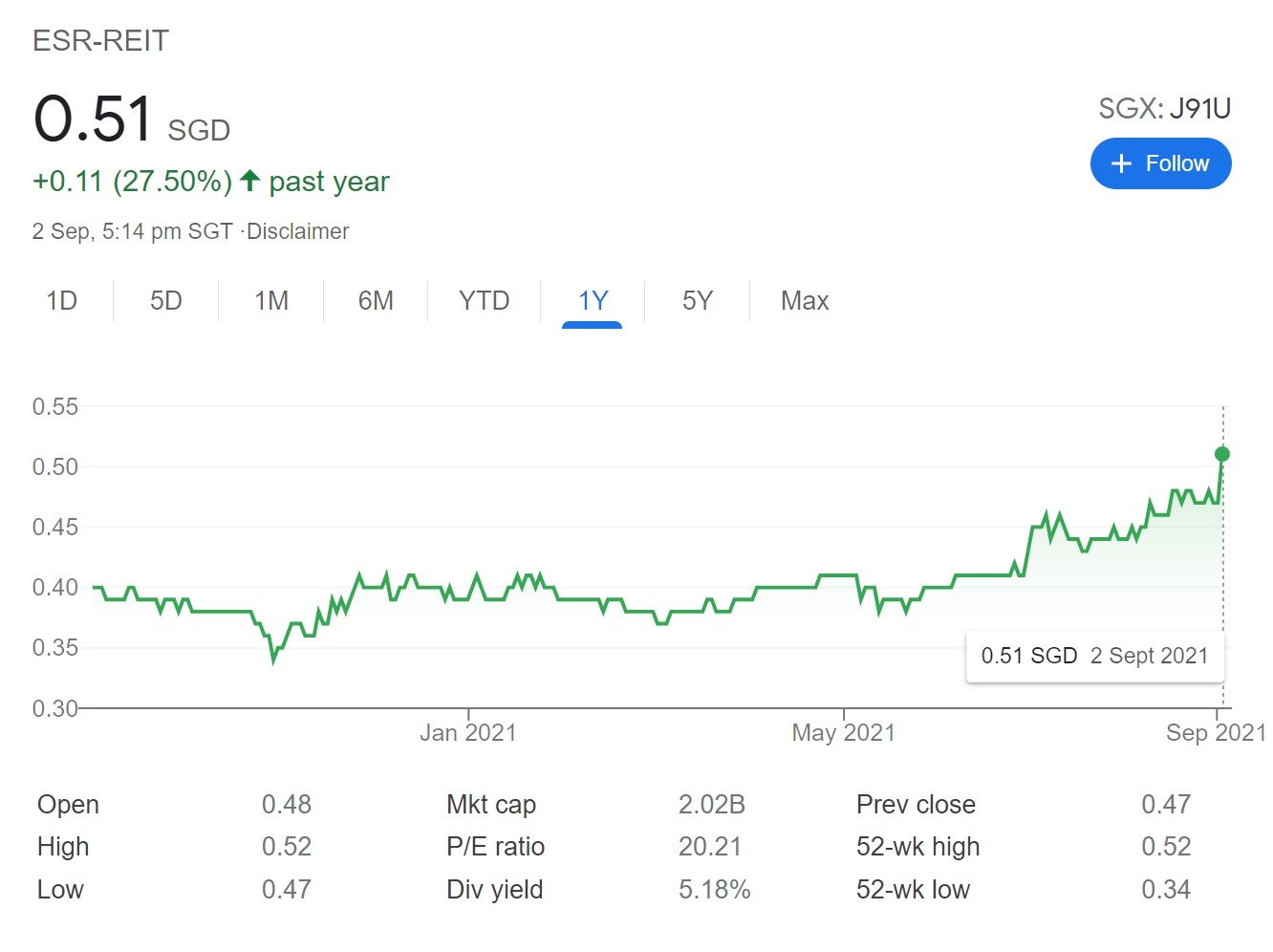

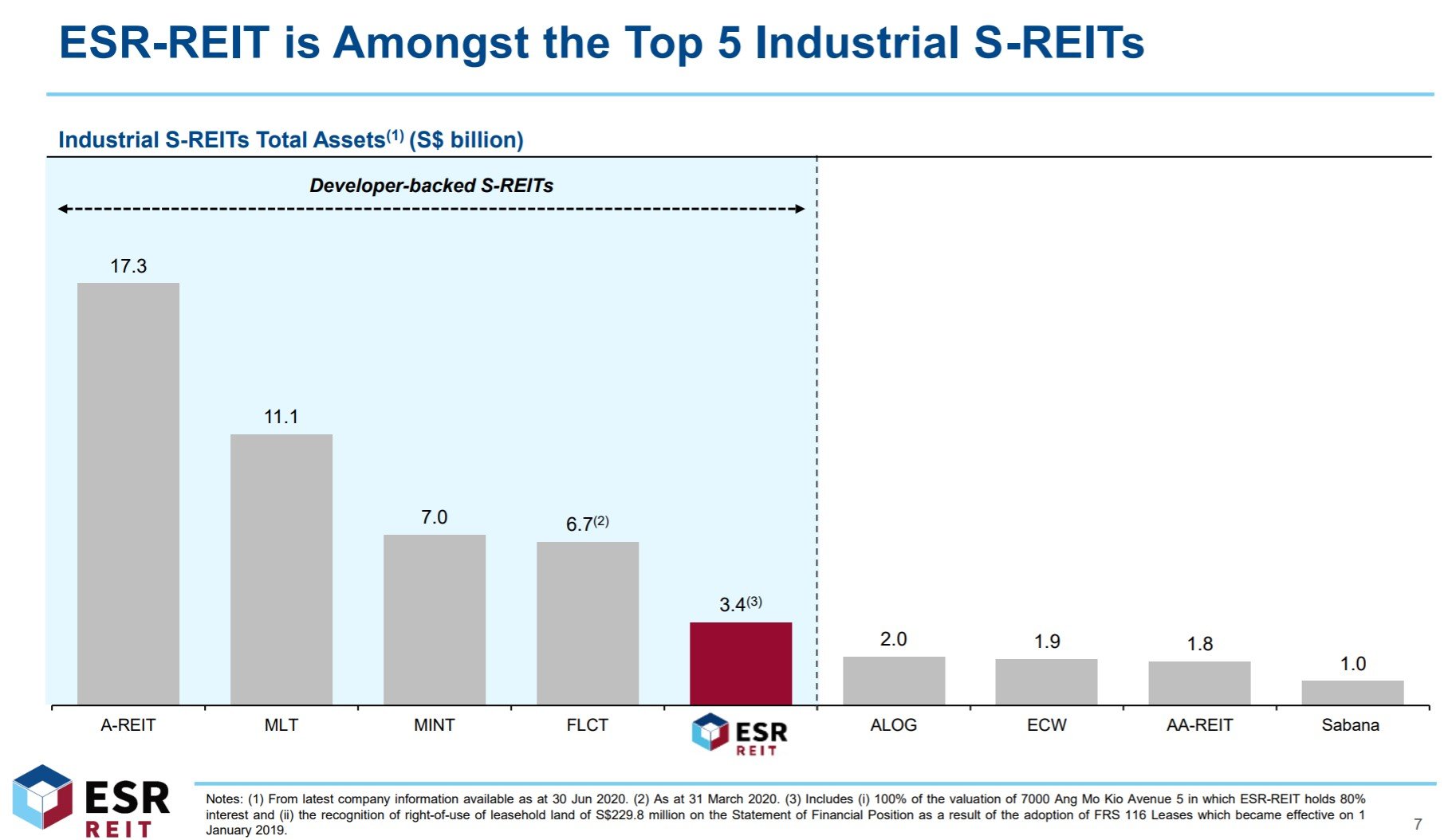

ESR REIT

Market Cap: $2.02b

Price/Book: 1.17

Trailing 12 month yield: 6.38%

Leverage: 41.4%

Occupancy: 91.7%

What I like about ESR REIT

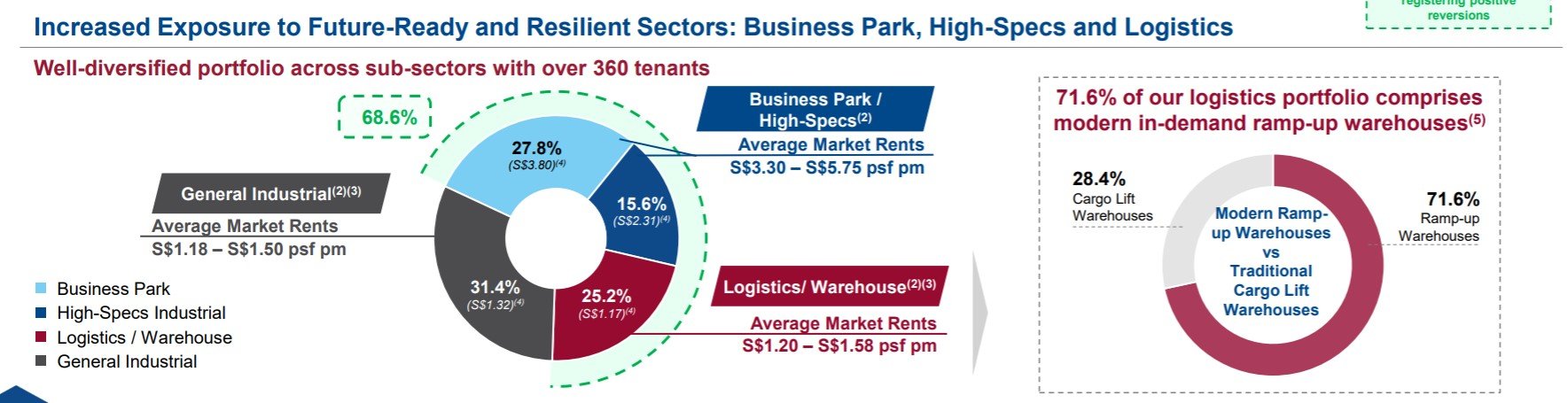

Logistics Exposure in Singapore

Logistics is really hot right now.

All that ecommerce demand has driven a lot of demand for logistics space.

For ESR REIT – 68% of the portfolio is split among Business Parks and Logistics space, so it benefits from such tailwinds.

The bulk of the portfolio is Singapore (2.2% Australia).

To give you an idea of how hot logistics is – ARA Logos Logistics Trust and AIMS APAC REIT are up around 58 per cent and 26 per cent respectively this year.

Both of which are significantly smaller than ESR REIT.

What I don’t like about ESR REIT

Sponsor (both a good and a bad)

The Sponsor ESR, recently announced a US$5.2b deal to buy ARA to create the world’s third-largest listed real estate asset manager.

ESR merging with ARA – I know most of you will have strong views on this deal. You’re either going to love it or hate it.

Personally, I’m in the camp of 1 + 1 = 2. If you merge it, it can’t be any worse than before right?

And scale is everything in today’s world, so there may even be a small net positive.

Yield is good

To put things in perspective, Mapletree Industrial Trust trades at a 4.4% yield, while Ascendas REIT has a 4.88% yield.

By contrast, ESR REIT is at a 6.1% forward yield today.

There’s really no free lunch in this world. There’s some drawbacks to ESR REIT, but you do get a higher yield to compensate for the risk.

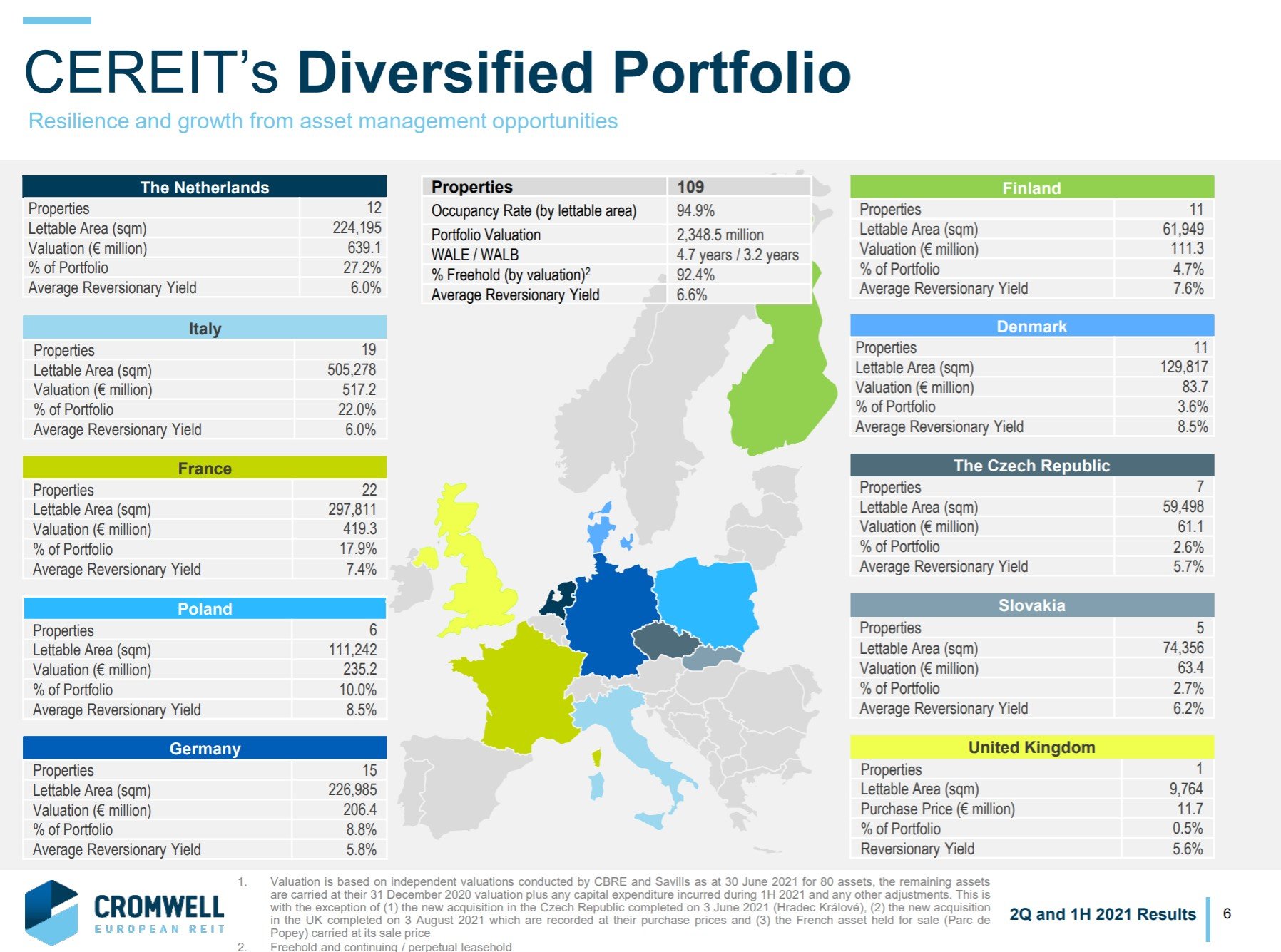

Cromwell European REIT

Market Cap: S$2.2b

Price/Book: 1.00

Trailing 12 month yield: 6.91%

Leverage: 35.8%

Occupancy: 94.9%

What I like about Cromwell REIT

Exposure to Europe + Logistics

Cromwell REIT offers exposure to 2 big trends – Europe, and Logistics.

Logistics we talked about above, there’s just a huge tailwind for logistics globally given the ecommerce boom.

Europe on the other hand, is a tricky one.

My personal view, is that despite all the doom and gloom, Europe may actually do well in the short term. Europe is reopening, monetary policy is very supportive, and economic growth is picking up. All good signs.

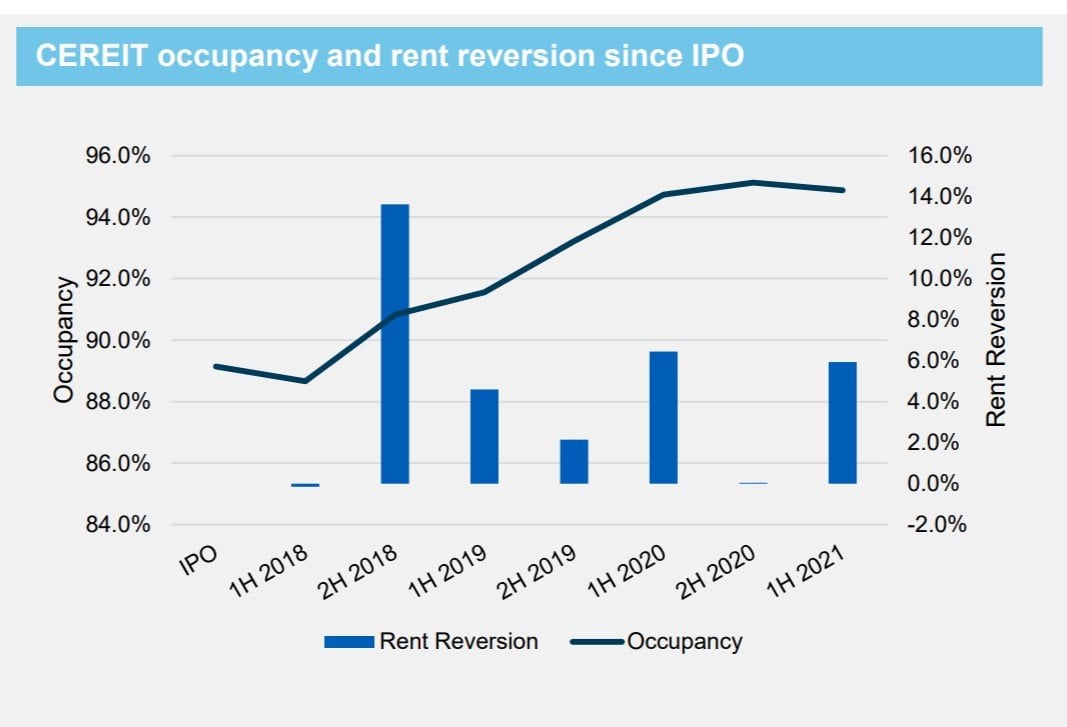

Generally done well since IPO

Despite all the naysayers, Cromwell REIT has also done very well since IPO

What I don’t like about Cromwell REIT

Hard to assess the quality of assets

The problem though – all the assets are located in Europe.

Us being located in Singapore, we really cannot assess the quality of the assets the way a local can.

I’ve heard from certain investors that the assets are actually very high quality, and very modern. But I can’t confirm this.

Sponsor – Cromwell Property Group

Cromwell Property Group is a commercial real estate investment and management company with operations in Australia, New Zealand and Europe. The Group is in the ASX 200 list. At December 2020, Cromwell had a market capitalisation of $A2.3 billion, a direct property investment portfolio in Australia valued at $A3 billion and total assets under management of $A11.6 billion across Australia, New Zealand and Europe.

So they’re an Australian property player, with about A$11 billion of assets.

They’re no slouch, but they’re no Mapletree either.

6.9% yield is very strong

For all the risks – you do get a very strong 6.9% yield though.

But do note there is FX exposure for Cromwell REIT – you’re taking on Euro/SGD exposure.

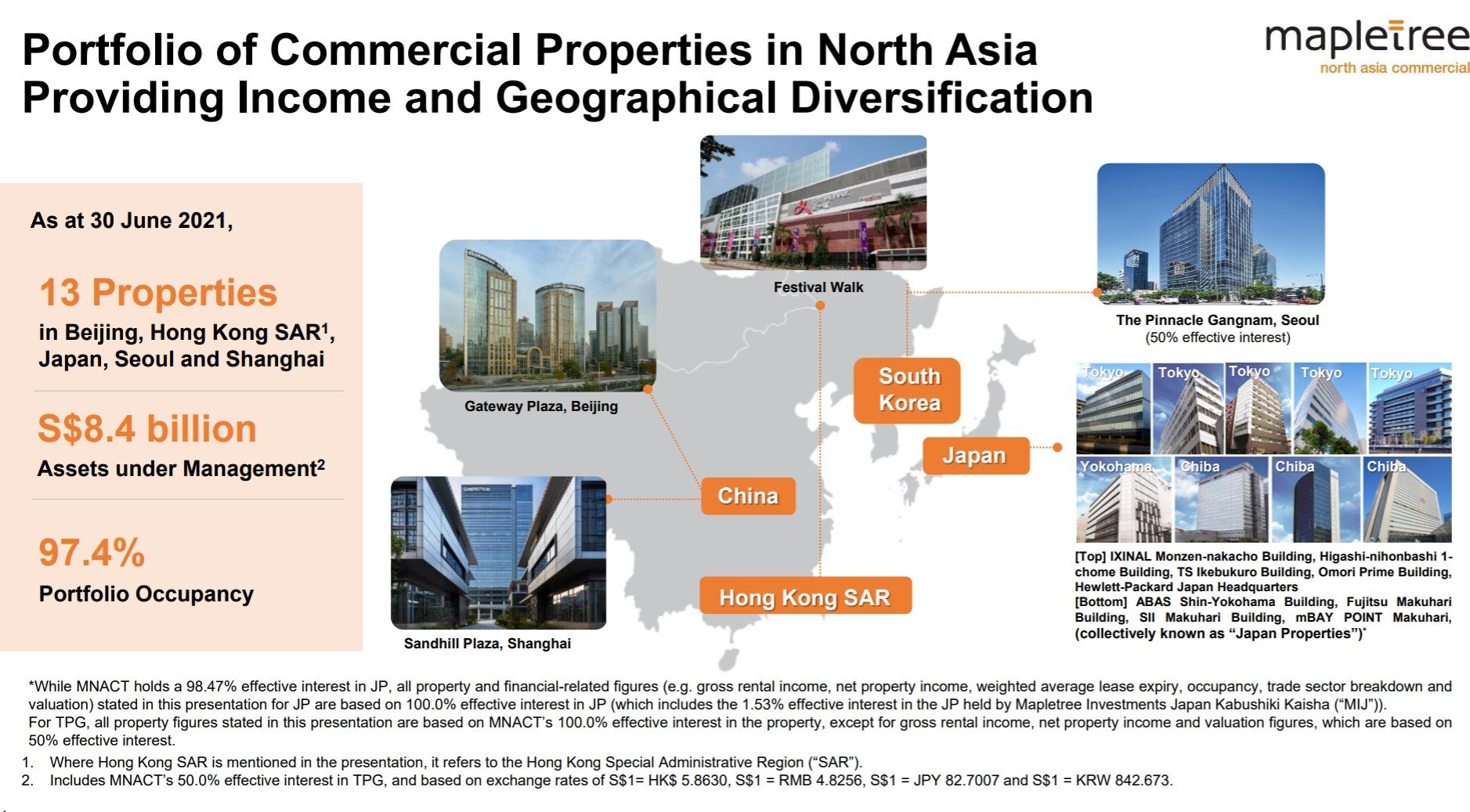

Mapletree North Asia Commercial Trust (MNACT)

Market Cap: S$3.5b

Price/Book: 0.79

Trailing 12-month yield: 6.2%

Leverage: 41.8%

Occupancy: 97.4%

I know I said no Mapletree on this list.

But for the last slot, it came down to Mapletree North Asia Commercial Trust vs Starhill Global REIT.

Both offered very similar yields, and at current pricing I thought Mapletree North Asia Commercial Trust was the better REIT.

But anyway I’ll include both, and you can decide for yourself.

What I like about Mapletree North Asia Commercial Trust

Broad exposure to North Asia across asset classes

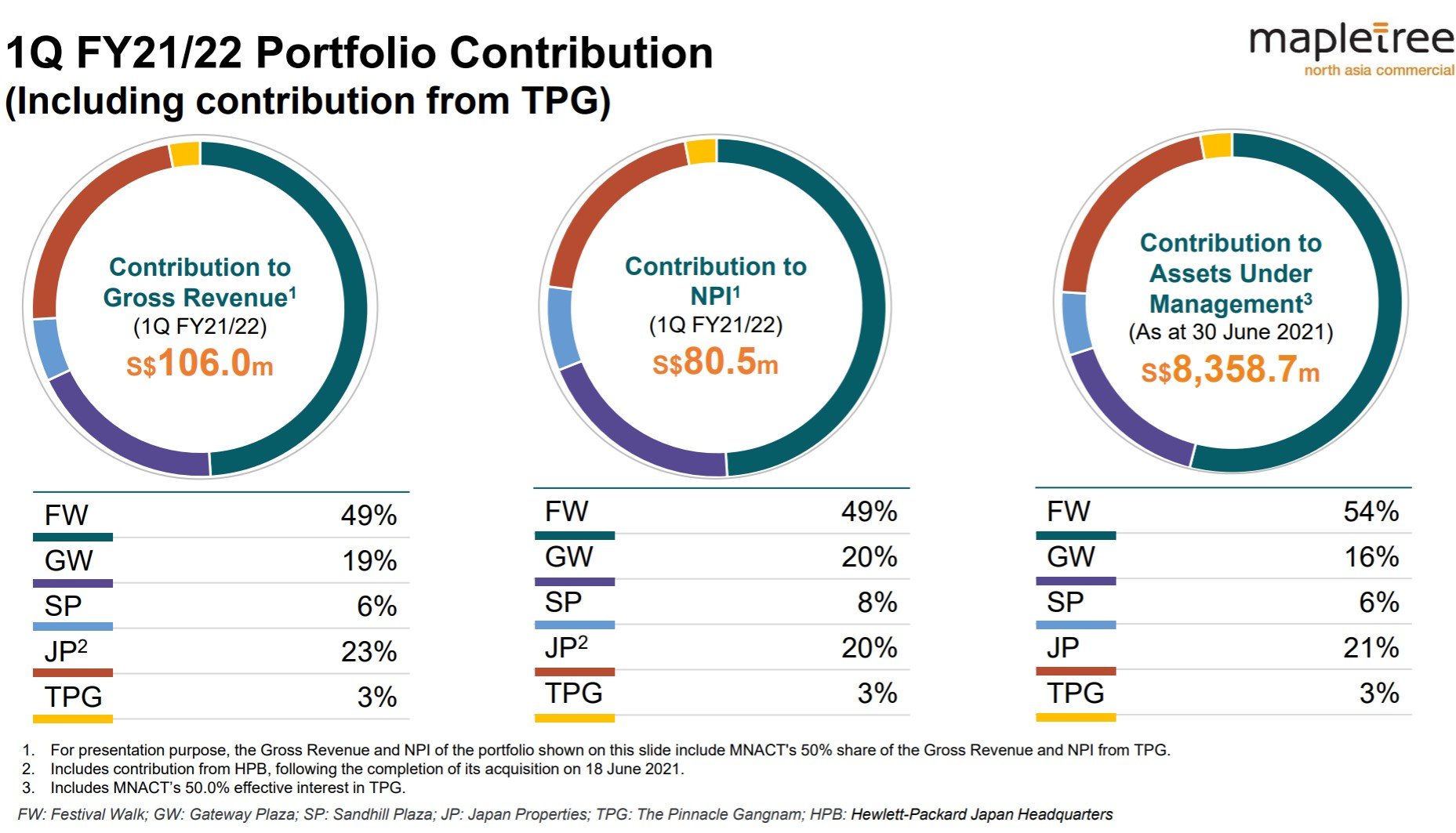

Mapletree North Asia Commercial Trust’s allocation is:

- 50% Hong Kong (Retail)

- 25% China (Office)

- 21% Japan (Office)

- 3% Korea (Office)

Pretty broad exposure to a mix of retail and office assets in North Asia.

FW: Festival Walk (HK); GW: Gateway Plaza (Beijing); SP: Sandhill Plaza (Shanghai); JP: Japan Properties; TPG: The Pinnacle Gangnam (Korea);

What I don’t like about Mapletree North Asia Commercial Trust

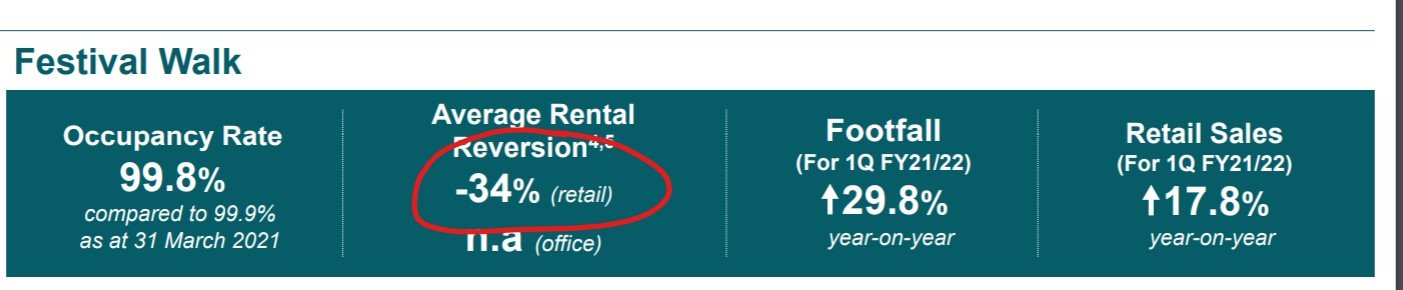

Rental reversion is an absolute disaster

The problem though, is that none of the assets are really best in class.

And it shows in the rental reversion, which is an absolute disaster:

Negative 34% and negative 27% for the 2 biggest assets in this REIT!

That’s really bad.

Mapletree + Decent yield

On the plus side, you get Mapletree as a sponsor, and a decent 6.2% yield.

Hong Kong should start to improve going forward too, so it’s possible the rentals have bottomed out.

But definitely a big point to watch.

Starhill Global REIT

Market Cap: S$1.4b

Price/Book: 0.74

Trailing 12 month yield: 6.56%

Leverage: 35.9%

Occupancy: 95.5%

What I like about Starhill Global REIT

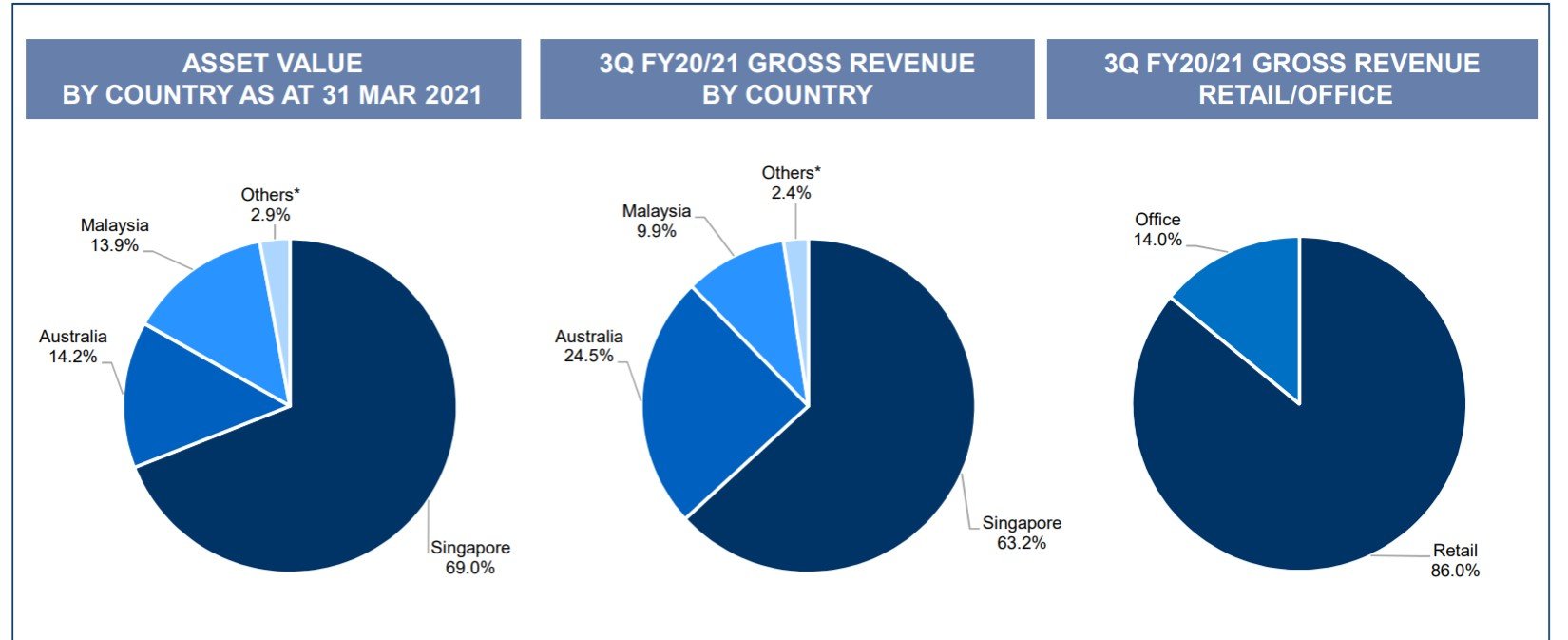

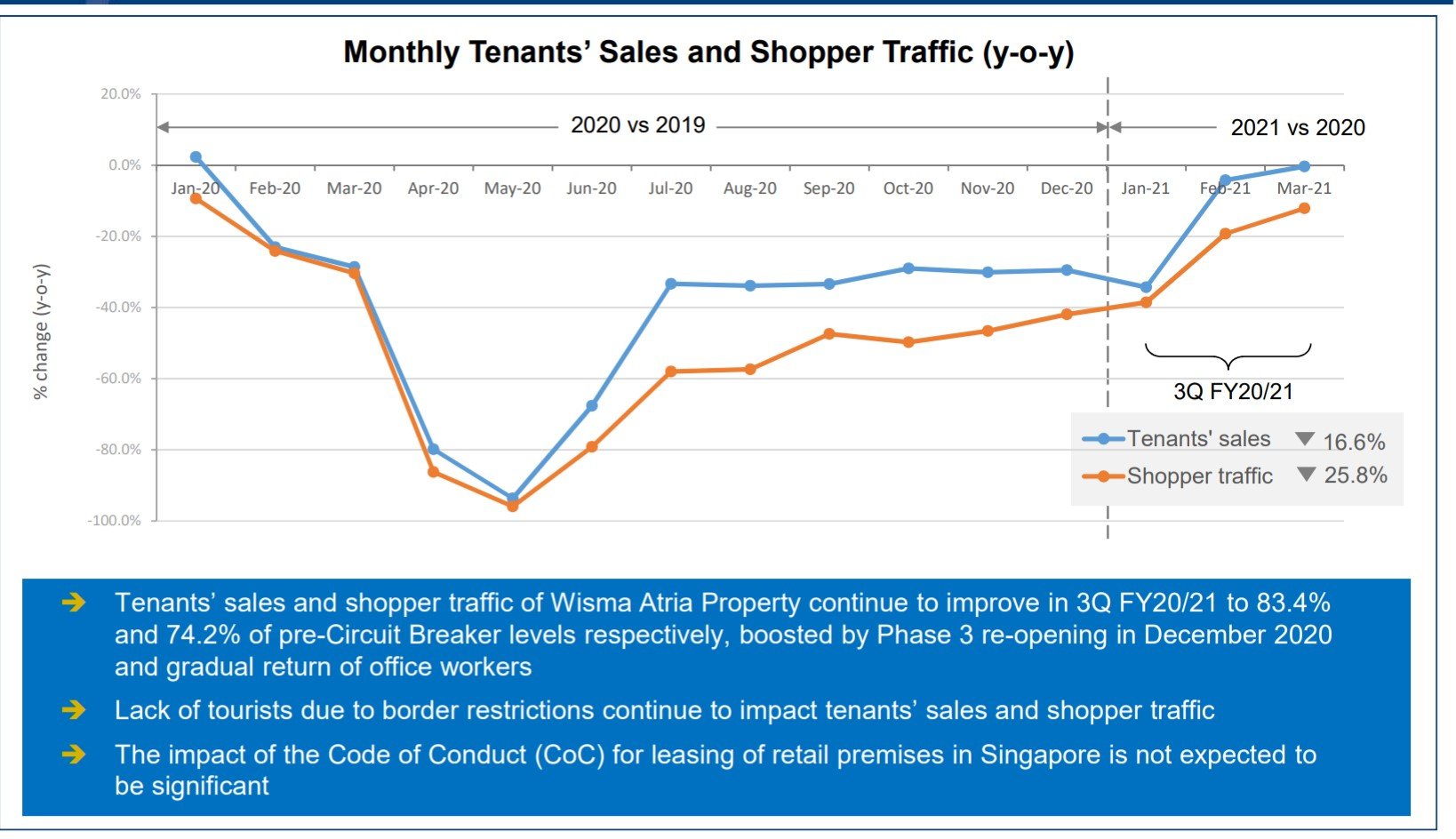

Broad exposure to Singapore retail which is recovering

69% of the assets are in Singapore, and spread among 2 properties – Ngee Ann City, and Wisma Atria.

The tenant sales numbers below are pre-Phase 2 Heightened alert, but they still show a pretty remarkable recovery from COVID lows.

What I dislike about Starhill Global REIT

I know many investors out there think that Wisma and Ngee Ann City are old, unsexy assets that will not do well going forward.

And Ngee Ann city has big exposure to 1 anchor tenant (Takashimaya).

But remember the saying – no such thing as bad real estate, only a bad price?

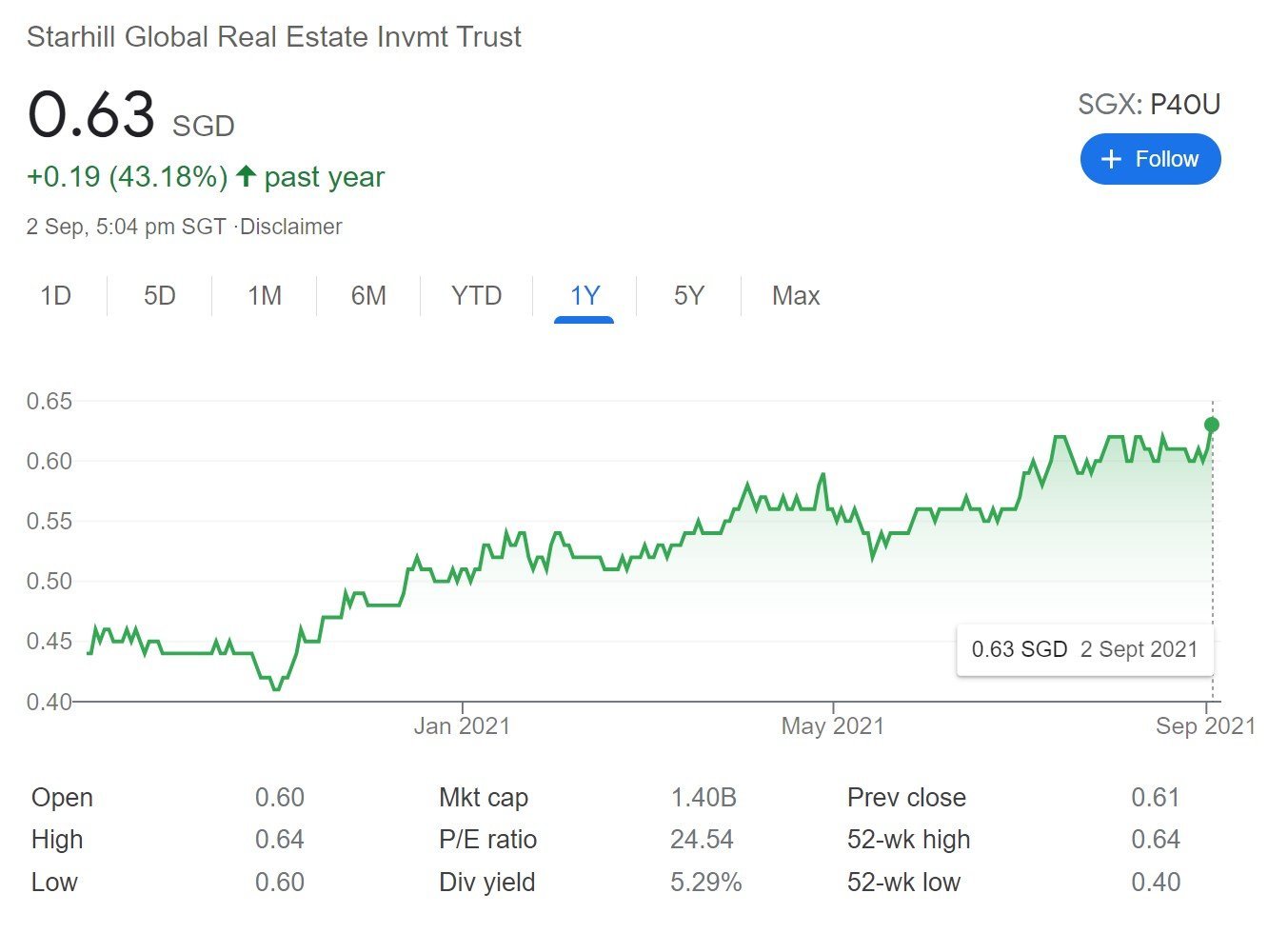

At the $0.40s range, I thought the risk reward looked amazing, and I was loading up (see our 2020 article).

But at today’s $0.63, it looks much more fairly priced to me – at a 6.5% yield and 25% discount to book.

The Malaysia assets, and Wisma may also prove to be a drag going forward.

At today’s price, I would probably go with Mapletree North Asia Commercial Trust, which is why Starhill REIT fell out of the list.

Full Disclaimer: I hold positions in MNACT and Starhill Global REIT. Full portfolio available on Patreon.

Closing Thoughts: Rising Interest Rates – Impact on Singapore REITs?

And of course, the elephant in the room – are interest rates going up?

REITs are basically levered investments into real estate. So your biggest fear as a REIT investor is when interest rates go up.

So far at least, interest rates have been remarkably stable since their March peak at 1.7%.

Personally, I don’t think this will last. I still think the path forward is for tightening monetary policy, and rising interest rates.

That could potentially spell a lot of trouble for risk assets across the board.

Overweighting any one asset class in this climate is probably not healthy, and I’m quite widely diversified at this point to REITs, dividend stocks, growth stocks, commodities, gold, real estate etc. You can check out my full asset allocation and Stock Watch on Patreon if you’re keen.

But we’ll see.

Love to hear your thoughts! Any great REITs that I missed out from this list?

Running a giveaway for Mankiw Principles of Economics (Graphic Edition) – Full set (worth $137)! 5 sets to giveaway – Details here!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Check out our review on Tiger Brokers and MooMoo.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide on the best buying platforms here.

As always, this article is written on 3 Sep 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Join our Reddit community at r/SingaporeInvestments.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Did iReit Global make the shortlist?

No not a big fan of the sponsor.

I sold off my position after I saw how the REIT was treated with the acquisition of the Spanish? assets.

Can comment why the sponsor no good? Thought CDL had a stake in the reit manager?

It was the way they handled the acquisition of the Spanish offices – where they pulled the deal because of lukewarm investor interest, then 1 year later did the same deal post-COVID, at the exact same price.

Maybe it’s just me, but I didn’t like how they handled it, so I sold my entire position (at a profit) shortly after.

Hi FH

Keep it up. I do own 4 of them.

Still no FLCT. Lol.

I think the price we paid really matters. Ah kong reit can also lose money if we bought at all time high especially those with miserable yield.

Haha FLCT didn’t make the list because of the 5% yield rule. And also I took out all Frasers REITs because they are too boring like Mapletree/Capitaland.

Interestingly enough I was looking at the blue chips like CICT and Ascendas the past week, and they look very fairly priced today actually. Have a good mind to add if we get a small dip from here.

Didn’t realised FLCT has doubled since I bought. Too lazy to monitor.

CICT holding big + more to come from CapLand distribution. Agree current price still ok to buy. May round up or down the odd lots. Ascendas is too expensive. MIT, KDC worst. Just my opinion only.

Starhill not bad for those who bought at 40s.

Just relax and KLKK first. Lol.

Haha I bought Starhill at 40s. Yield is nice, but if it hits high 60s I may just take profit and rotate to another REIT.

Agree that Industrial REITs are too expensive. But they havent had a meaningful correction since 2018, and just building a portfolio with Retail + Office is not ideal too.

I bought SH at 40 and 38 hehehe.

Don’t worry Industrial will drop eventually if you believe in wave theory. The ah kongs just had the first down leg only.

Haha good pick up at 40/38. I think I bought in around 42 if I rmb right.

No plans to sell and lock in the gains? Once it goes to high 60s the upside is probably quite limited and it’s just to collect yield already.

May consider to sell some if it reaches high 70s or if it goes bad. Can you imagine the profit when borders really open?

I don’t like to monitor prices closely. It’s just too tiring after 32 years.

Will only sell if prices reach ridiculous level. Recent examples were MLT and DBS. Will need decades to collect so much dividend if I continue to hold. Ridiculous profit is very hard to resist. I am human afterall. LOL.

What’s your view on CLI now? Hands itchy now. Lol.

Haven’t looked at CLI too closely. Market seems to really like it though, there looks to be a rerating in the valuations.

I have exposure as I was a CL stockholder even before this, so what I have is from the restructuring.

CLI has big exposure to China though, so as Evergrande plays out there may be share price weakness. But frankly haven’t done a deep dive into the valuations.

What about Manulife Reits?

Any views?

Never looked into them closely, so can’t really comment.