I’ve been accused of talking too much about “Ah Gong” stocks on Financial Horse.

So I figured for this week, let’s jump back into the 21st century.

Let’s talk about the Best 5 Growth Stocks to Buy for Singapore Investors in 2022.

Whether it’s a Cloud play, SaaS, SASE, data analytics – all fair game.

Because who said you can’t teach an old horse new tricks. ????

Rules for Best 5 Growth Stocks to Buy for Singapore Investors 2022

A couple of ground rules to frame this discussion:

- No China stocks

- Less than $50 billion market cap

- 3 to 5 year holding period

No China stocks

I know a lot of you think China is uninvestible.

I have my own views on that, but for the sake of today’s article, we’ll leave all that out. No China stocks on this list.

If you want my full China stock watch you can check out Patreon.

Less than $50 billion market cap

I get that $50 billion is a bit of an arbitrary cut-off.

But the point of this list is not to list the usual boring SEA, Airbnb, FAANG.

A stock below 50b market cap can easily 3-5x if they execute well.

Whereas when you buy Apple at $2.48 trillion, do you really think the stock is going to 3x from there.

3 to 5 year holding period

The short term is notoriously hard to predict, especially as we move into the tightening phase of this cycle.

3 to 5 years is long enough to allow the short term factors to fade away, and the true earnings potential of the company to show itself.

Best 5 Growth Stocks to Buy for Singapore Investors in 2022

Digital Ocean

Market Cap: $11.3b

Price/Sales: 29

There are 2 ways of looking at Digital Ocean.

If you love it, you’ll call it the Shopify of Cloud Computing.

If you hate it, you’ll call it the poor man’s AWS (Amazon Web Services).

For me personally, I lean a bit more towards the former camp, which is why I aped into the stock in the 50s range.

I’m up 100% since, but I think that over a 3 to 5 year horizon, this growth stock may still have room to run.

The goal of Digital Ocean is to simplify cloud computing, for small and medium businesses.

The analogy is that using AWS (Amazon Web Services) today is like flying a jumbo jet.

There are a ton of controls and optionality, everything you can possibly need as a Fortune 500 CTO.

But as an SME you don’t need all that. You just need something that is simple, cheap and works.

Digital Ocean wants to be the “Shopify” of cloud computing.

To make it so easy to use cloud computing, that the army of future developers and creators can spend their time building the business, instead of worrying about the cloud.

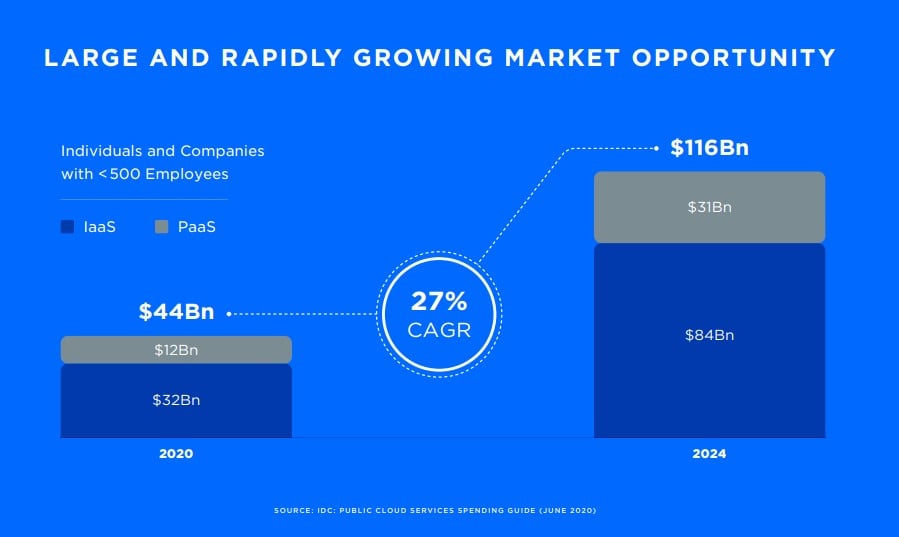

If they can pull off this vision, the upside is massive, because the total addressable market (TAM) for cloud computing is going to explode in the coming years. Literally every SME is going to be built on the cloud going forward.

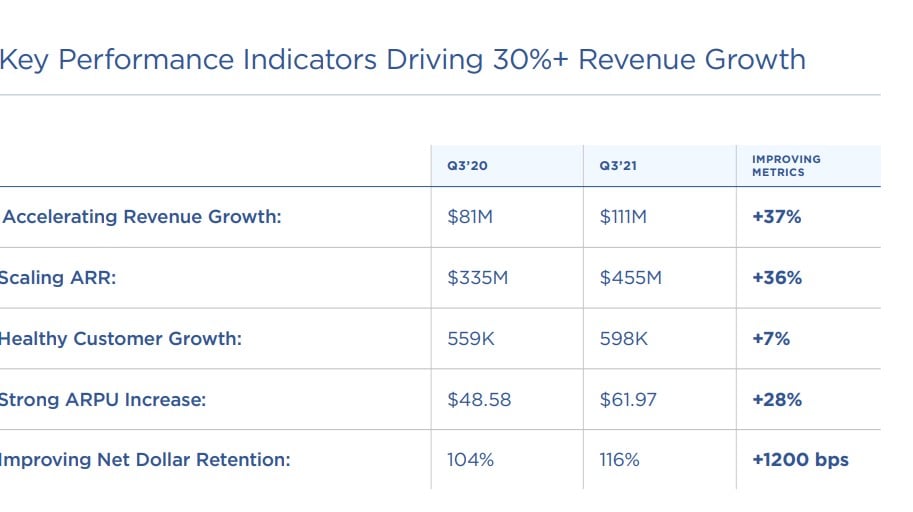

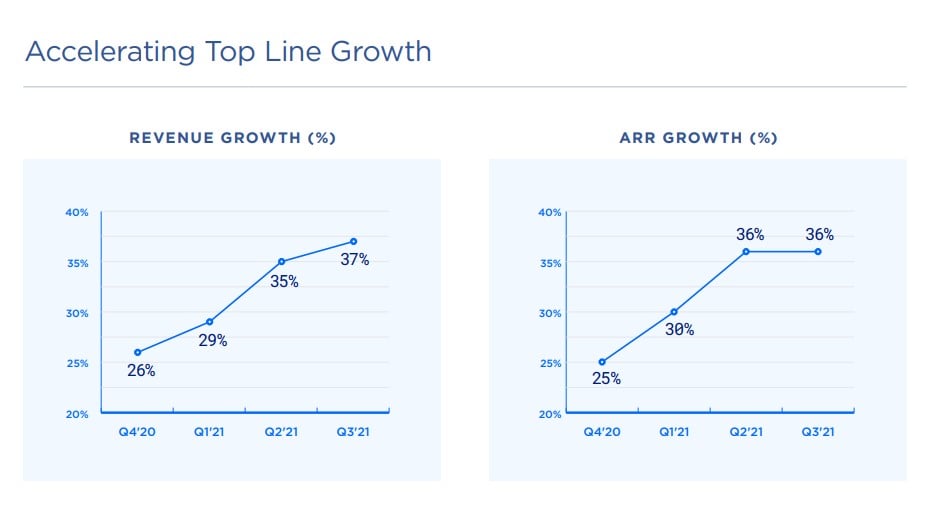

So far at least, the performance has been keeping up:

- 37% year on year revenue growth,

- 36% growth in annual recurring revenue (ARR),

- 28% growth in average revenue per user (ARPU),

- Rock solid growth in net dollar retention (NDR) to 116%.

Citron Research, the former short seller turned long only, recently issued a great report on Digital Ocean that is worth checking out if you’re keen on this growth stock.

For now, Digital Ocean’s 37% revenue growth is powered by a marketing spend that is just 10% of their revenue.

When you compare that with other SaaS players who spend 50% of revenue on Sales & Marketing, you start to appreciate the kind of revenue upside potential here when they decide to up the marketing budget.

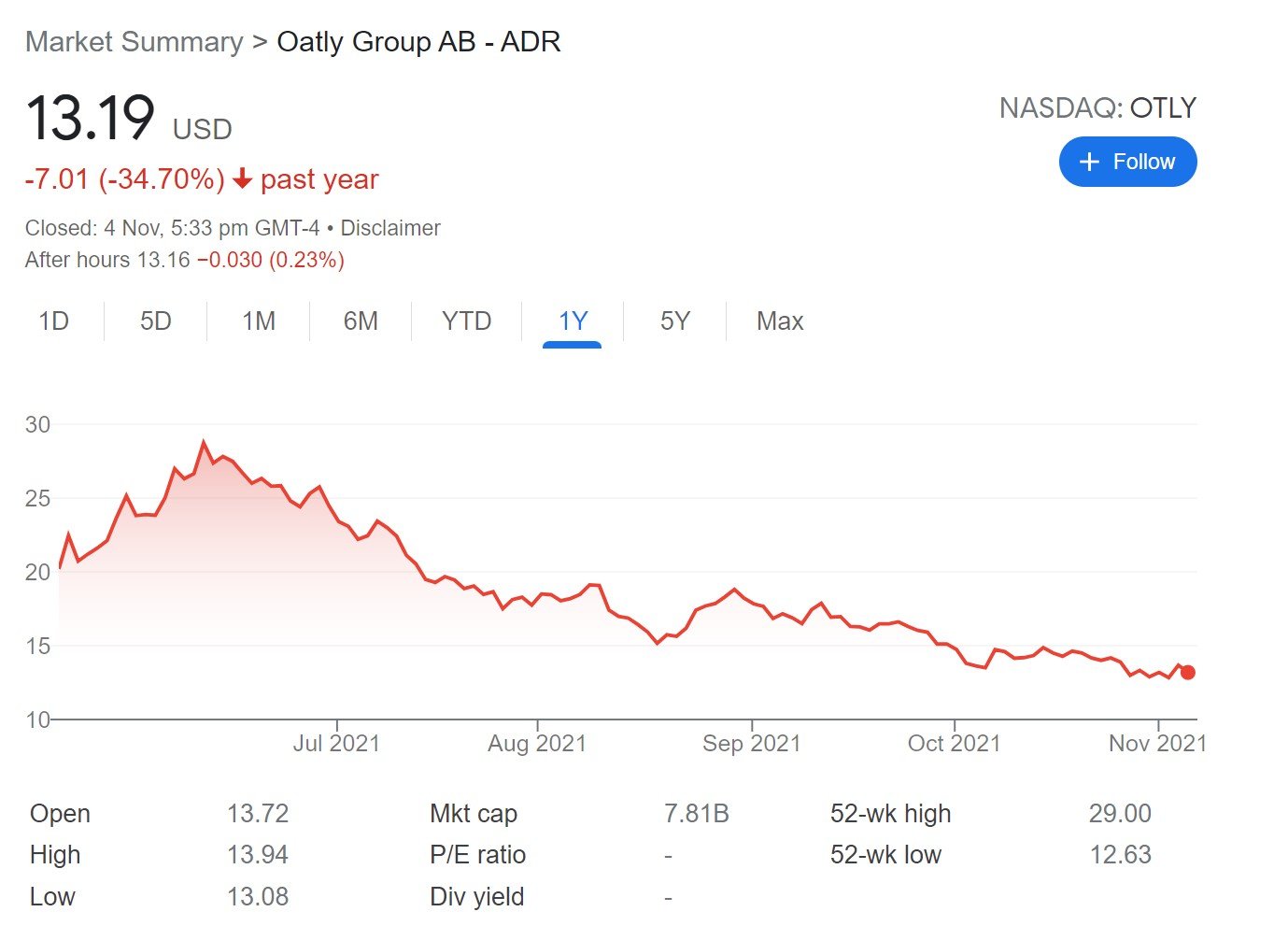

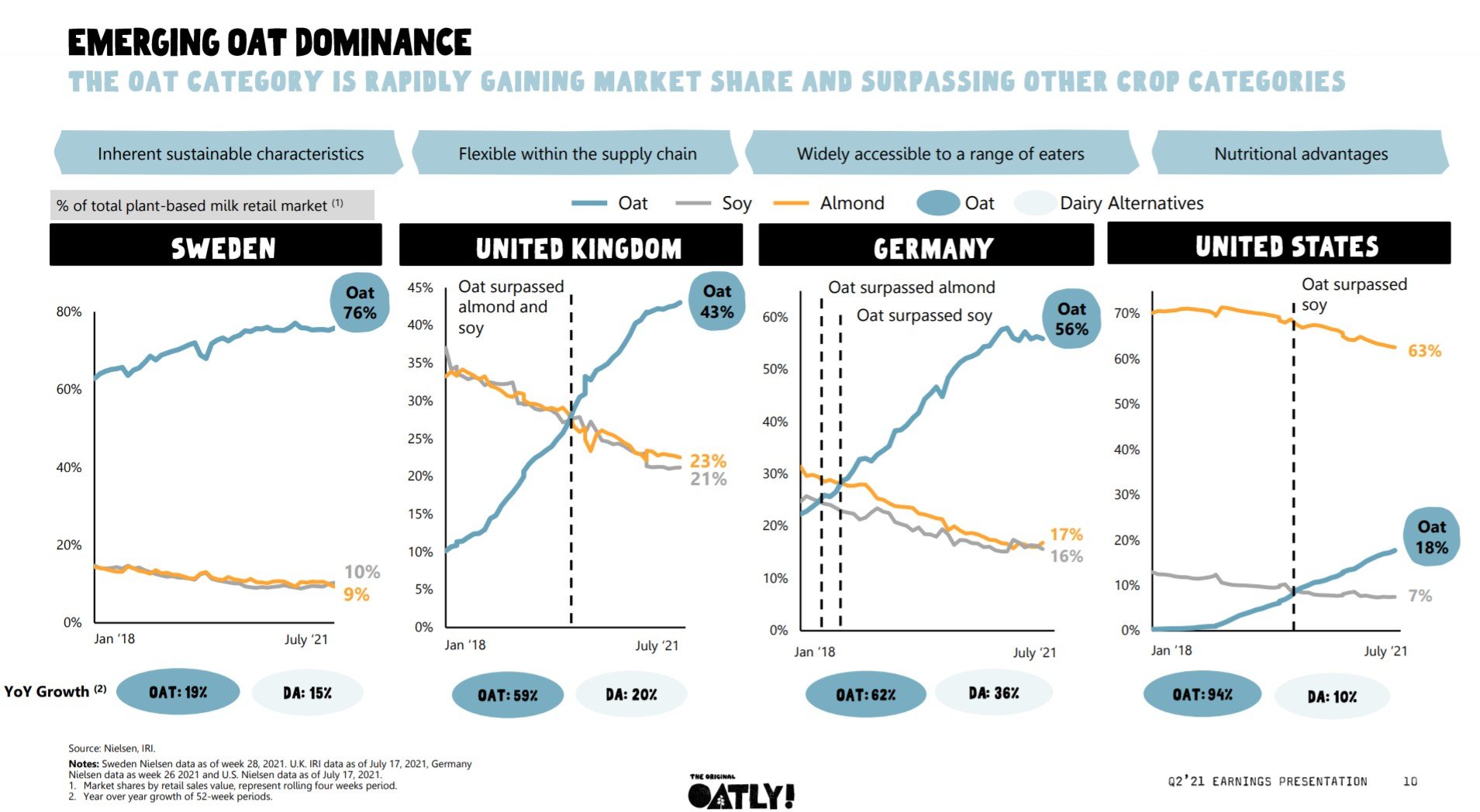

Oatly

Market Cap: $8 b

Price/Sales: 19

I know I know.

The people who hate it think it’s just oat milk.

The people who love it? They tell you that it’s Oat Milk.

Oatly is a very controversial stock, and I recently penned a full in depth analysis for Patreons on this growth stock. So do check that out if you’re keen.

To summarise, I think Oat Milk is different from Fake Meat like Beyond Meat.

I don’t think fake meat works because the taste is nowhere close to real meat, and the price is too high. True meat lovers like me would never buy it (after the initial try). And true vegetarians won’t buy it because it tastes too much like meat.

Whereas when you put Oat Milk in a beverage, the taste is very close to cow’s milk. And there’s a billion or so people in Asia who are lactose intolerant (okay maybe I exaggerate, but the point is that it’s big). That’s real market demand there.

As a Swedish company, Europe is their core market, with Asia and America the growth markets.

Oatly recently entered into a partnership with Starbucks to roll out Oat Milk to consumers, and apparently the demand was through the roof.

To the point where their production literally cannot keep up with demand.

Short seller Spruce Point Capital recently released a short attack on Oatly that contributed to the recent drop in short price.

The full report is here, and practically a must read if you’re keen to invest.

I extract the key arguments below, which point towards:

- Oatly not being environmentally friendly

- Potential financial accounting issues

At 19 times Price to Sales, this growth stock doesn’t come cheap too.

Especially when you think about the mega players like Nestle coming up with their Oat Milk competitors.

Like I said, Oatly is a controversial one.

If you like it, you like it. If you don’t like it, there are a million reasons why this growth stock is tricky.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

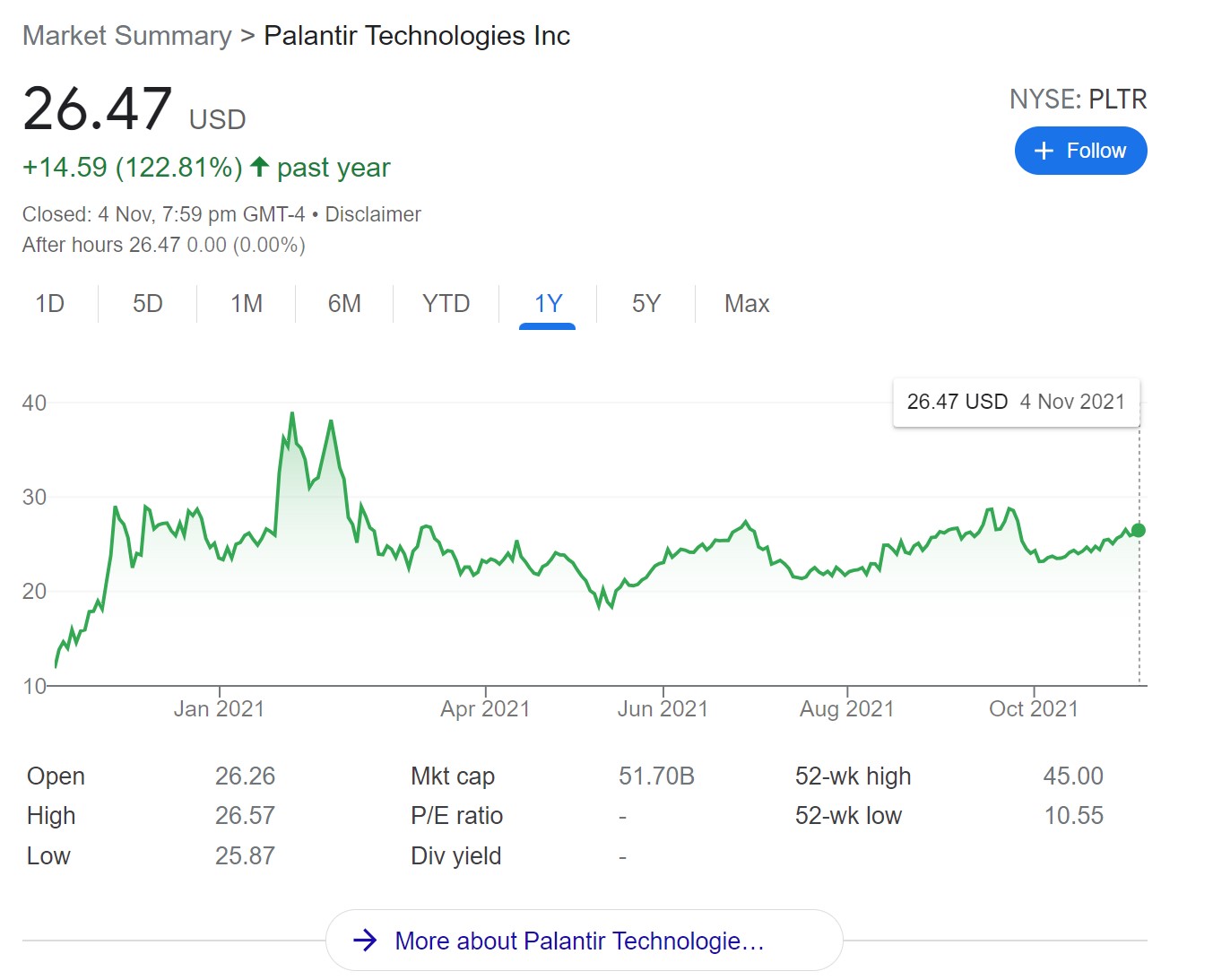

Palantir

Market Cap: $43 b

Price/Sales: 42

I don’t really know how to describe Palantir, because this company is so secretive.

There are 2 main products: Gotham, and Foundry.

Gotham is the data operating system used by defence and intelligence agencies. It collects real time data from sensors around the world (cars, drones, jets, phones etc), and combines that into 1 operating system. And it applies AI / Machine Learning to generate actionable insights. It’s used by the US Air Force, Navy and Army.

In other words, this is software straight out of a James Bond movie.

Whereas Foundry is the commercial version of Gotham. It does the same thing, but for private customers. Supposedly to “allow management to make data-based decisions to optimize the business”.

Because this software is used by intelligence forces, it’s very, very hard to get information on it, including to understand just how good it is.

Revenue growth is very solid though, coming in at 49% year on year growth, at a 31% operating margin.

Solid growth in ARPU and customer growth as well.

The share price has gone nowhere for a whole year though, so depending on how you see it, could mean a great buying opportunity or a complete dud.

My personal view is that Palantir is a stock that requires some patience. Enterprise SaaS is a slow and steady business. Think Salesforce, not Netflix.

You won’t get big flashy numbers each quarter, but each contract you lock in will stay with you for the next 10 years. Enterprise customers are sticky like that.

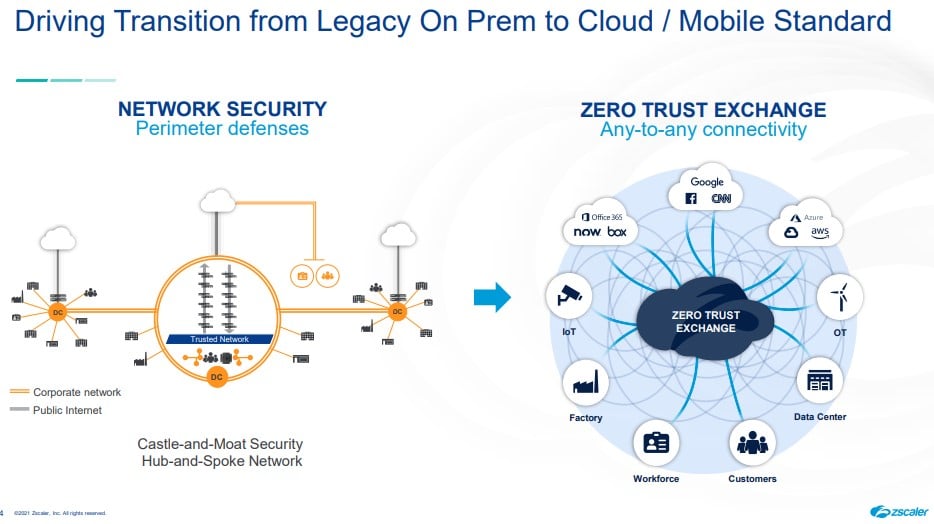

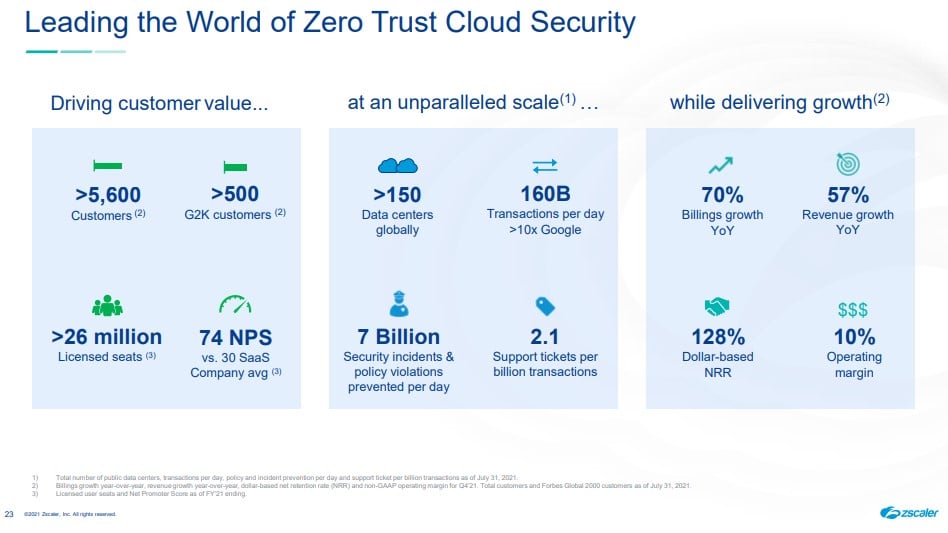

Zscaler

Market Cap: $46 billion

Price/Sales: 66

If not for the $50 billion rule, Crowdstrike probably would have made this list.

But instead Zscaler makes the list with its $46 billion market cap.

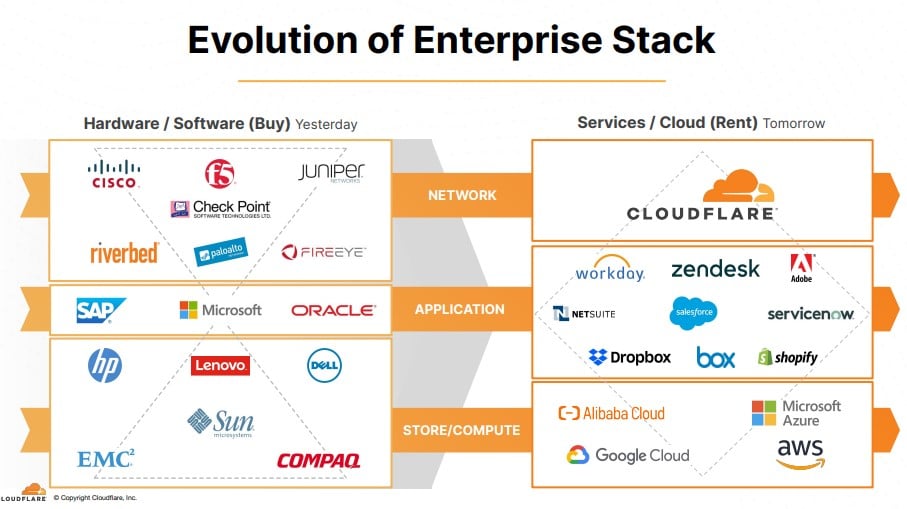

You’ll notice that a lot of names on this list are cloud players.

And that’s by design. I’m just hyper bullish on this whole sector right now.

In 2021, computing power is becoming a utility.

Think of it like electricity. When electricity was first invented, each company had their own generator.

Over time, electricity was centralised, and today you get electricity from the grid.

Exact same evolution for computing power.

At the start every company had their own inhouse server farm.

But increasingly, computing power is becoming centralised. Companies just “rent” computing power from the cloud, from players like AWS, Azure, or Digital Ocean.

In the future, every company will be a cloud company. Computing power will be something you pay per use, like electricity.

COVID and work from home has accelerate this trend by an order of magnitude. With everyone working from home, traditional centralised networks (hub and spoke) just don’t cut it.

You need a whole new wave of systems designed from the group up for cloud. A whole infrastructure on security, analytics, identity verification, just to support this transition.

Things like zero trust security, and SASE (Secure access service edge).

Zscaler is one of the leading names in this space, alongside names like Cloudflare and Crowdstrike.

This growth stock doesn’t come cheap at 66 times Price/Sales, but almost no player in the cloud space is cheap today.

What you do get, is 57% revenue growth, 128% net dollar retention, and a net promoter score of 74. That’s some ridiculous numbers there.

Cloud growth will slow down one day, but it doesn’t look like we’re there yet.

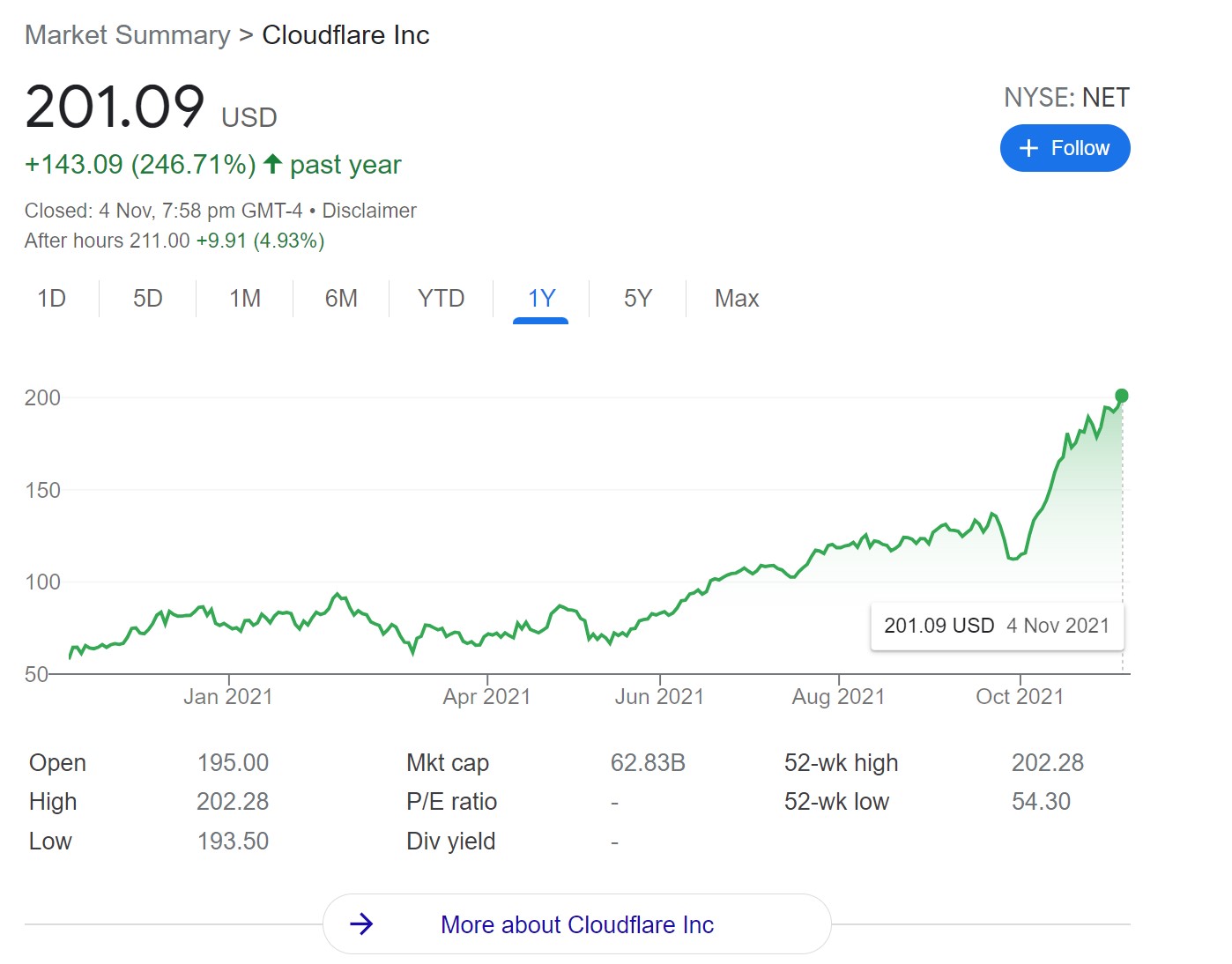

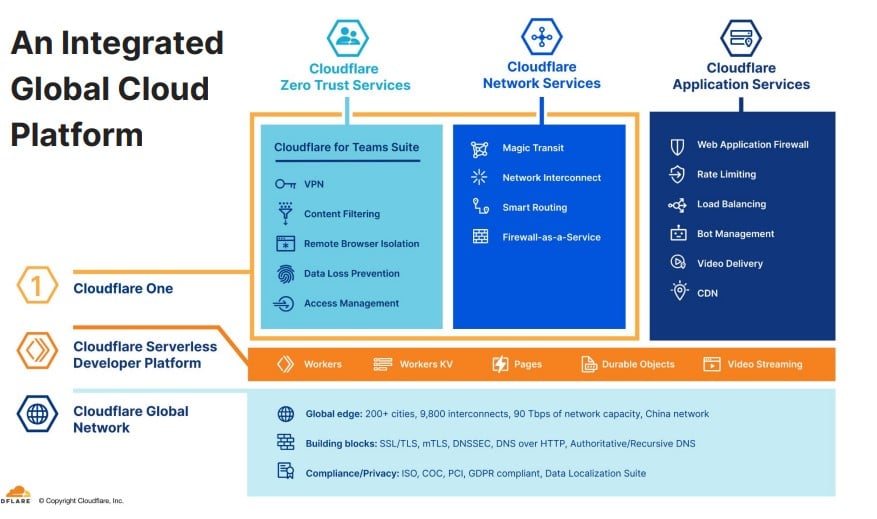

Cloudflare

Market Cap: $60b

Price/Sales: 135

For the final stock, I decided that be dammed with the arbitrary $50 billion market cap rule.

I’ve been talking about Cloudflare since it was in the $20 range, and it’s one of my biggest positions today.

While players like Crowdstrike focus on security, Okta on identity verification, Cloudflare’s focus is on… building a better internet.

I look at Cloudflare and I’m just mindblown by the number of ways this company can evolve.

They are trying to build themselves into the backbone of the internet, and find ways to monetise that later.

Now that’s a business model I can live with. Heck, even Financial Horse is run on Cloudflare.

Despite all that, the financials are still very solid, for a company that isn’t even all that focussed on monetisation.

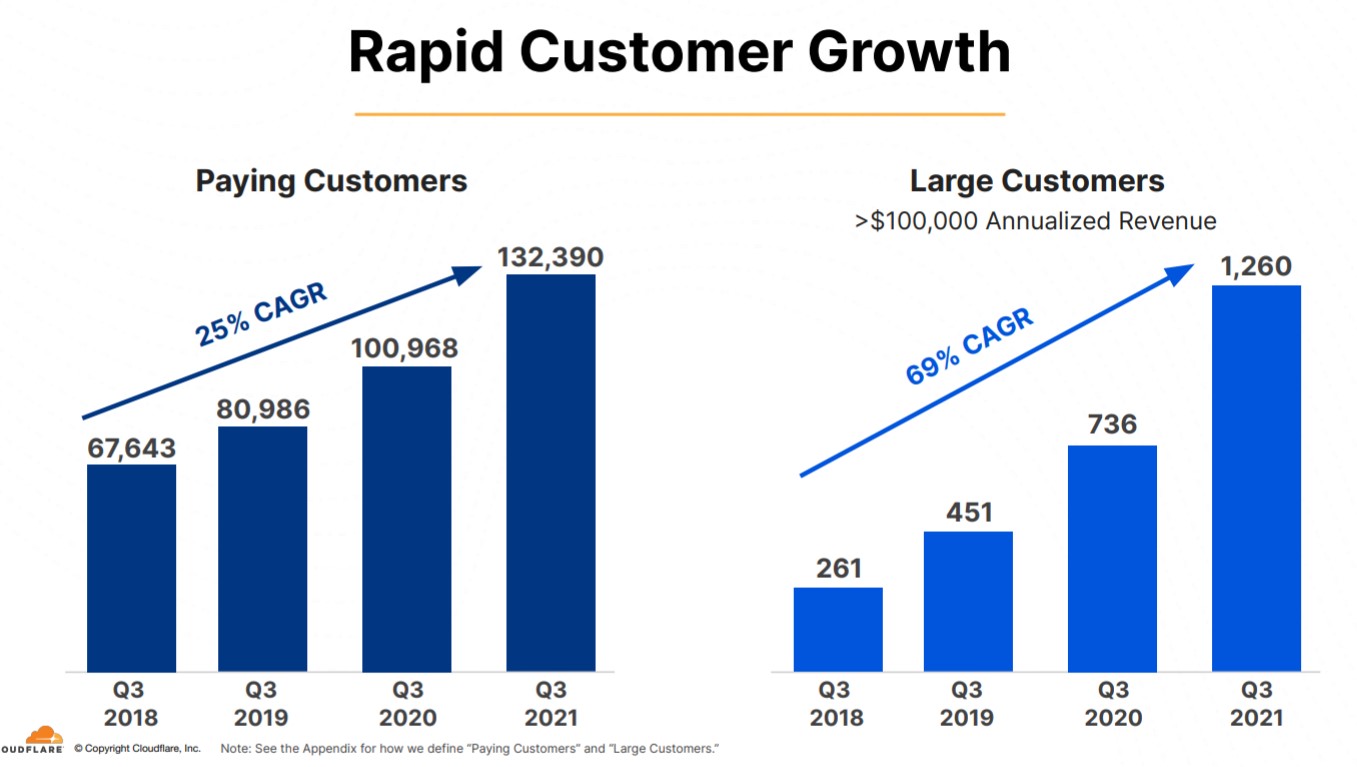

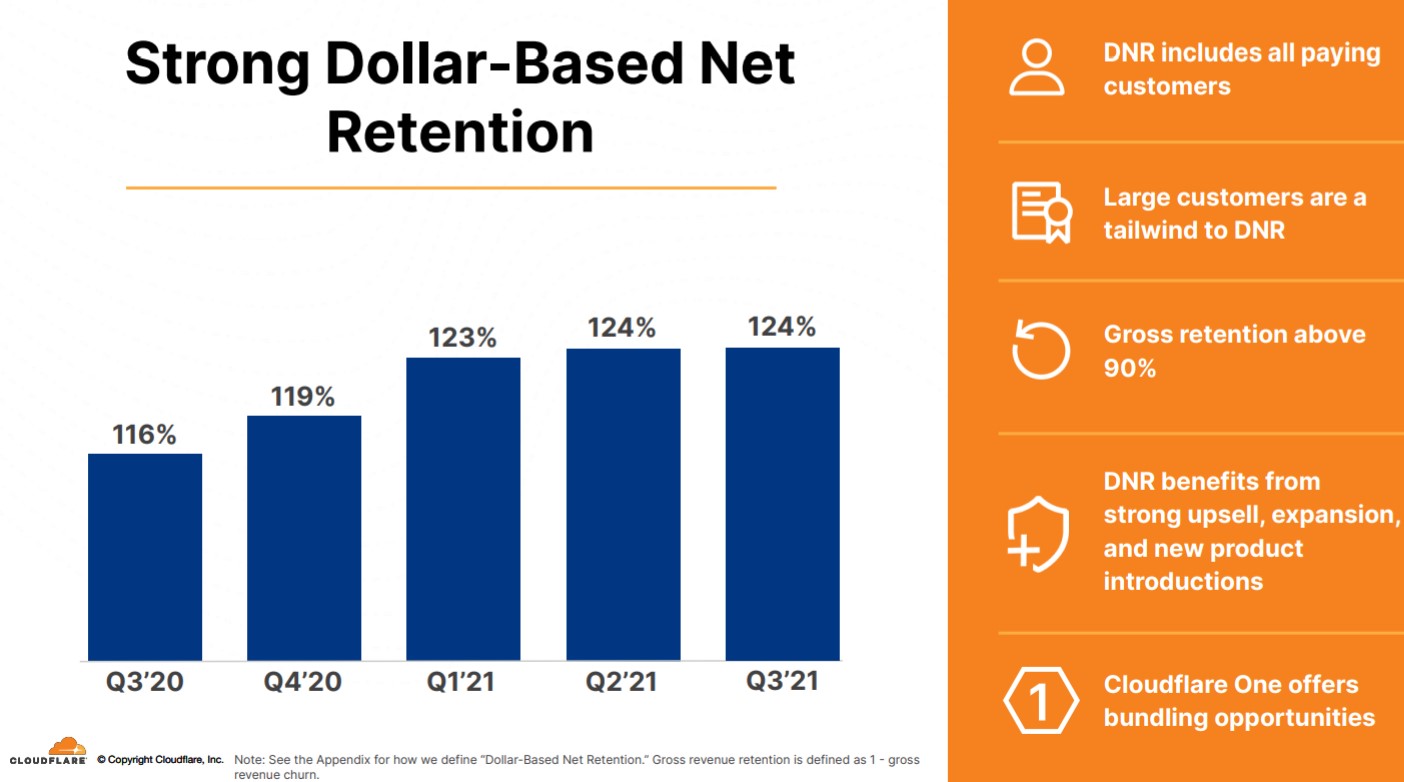

51% year on year revenue growth, 124% net dollar retention, and 69% CAGR in large customers growth.

The valuations are mind boggling though.

135 times price to sales.

That said, if I could just buy 1 player in the cloud space and hold for 10 years, it’s probably going to be Cloudflare. That’s the amount of conviction I have in this stock.

Sure, it may sell-off short term because of rising interest rates, but that would just be a buying opportunity to me.

Honourable Mention – Other Growth Stocks to Buy in 2022 for Singapore investors

There are a lot of other fantastic growth that failed to make this list for some reason or other, so big honourable mention to them.

Cloud Players – Crowdstrike, Service Now, Workday, Datadog

In the cloud space there is Crowdstrike (Security Cloud), Service Now (Service Cloud), Workday (HR Cloud), Datadog (Data Analytics).

The future is going to be cloud centric, and every company will build their IT around the cloud.

That’s just going to power massive growth for the sector in the coming years.

It’s a rising tide lifts all boats scenario.

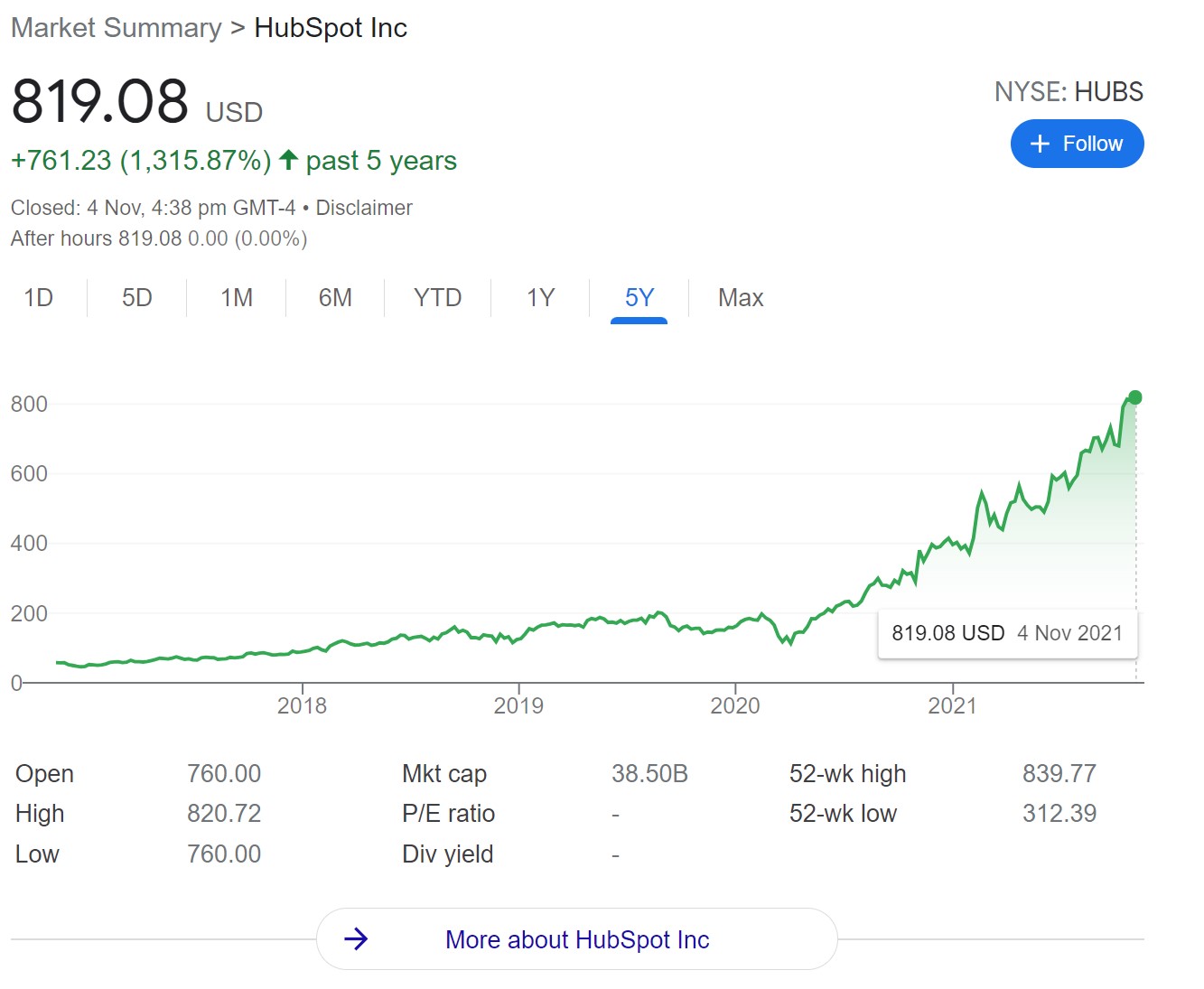

Hubspot

Hubspot is a stock I would rather not talk about because it reminds me of what could have been.

I noticed this stock at the $200 range, but I never pulled the trigger because I thought it was overvalued. ☹

Hubspot is the poor man’s version of Salesforce, which is a cloud based Customer Relationship Management (CRM) platform.

In simple English, it helps you manage your relationship with your customers and sales leads. Things like their previous history with you, status or orders, contact information and so on.

iFast

It’s sad that I’m doing a whole list of growth stocks and there’s only 1 stock from Singapore. If there’s any great growth stock in Singapore that I missed please, please let me know in the comments.

Even then I’m necessarily sure I’m that bullish on iFast.

There’s a lot of potential competition in the sidelines from players like Endowus, StashAway and Syfe. All of which are very well funded from VC money.

The share price has gone sideways for the past 6 months too.

Why no Biotech Growth Stocks?

A notable absence from this list is Biotech.

I get that Biotech is on the cusp of breakthroughs that will revolutionise humanity.

Unfortunately, I just don’t have the technical expertise to evaluate Biotech.

I understand a bit of cloud and Web3.0, but Biotech is just a step too far for this horse.

If any of you have good names, just let me know in the comments below!

Closing Thoughts: Tightening Monetary Policy a headwind for Growth stocks?

Full disclosure that I hold positions in many of the names above. You can check out my full portfolio and asset allocation (together with the full stock watch) on Patreon.

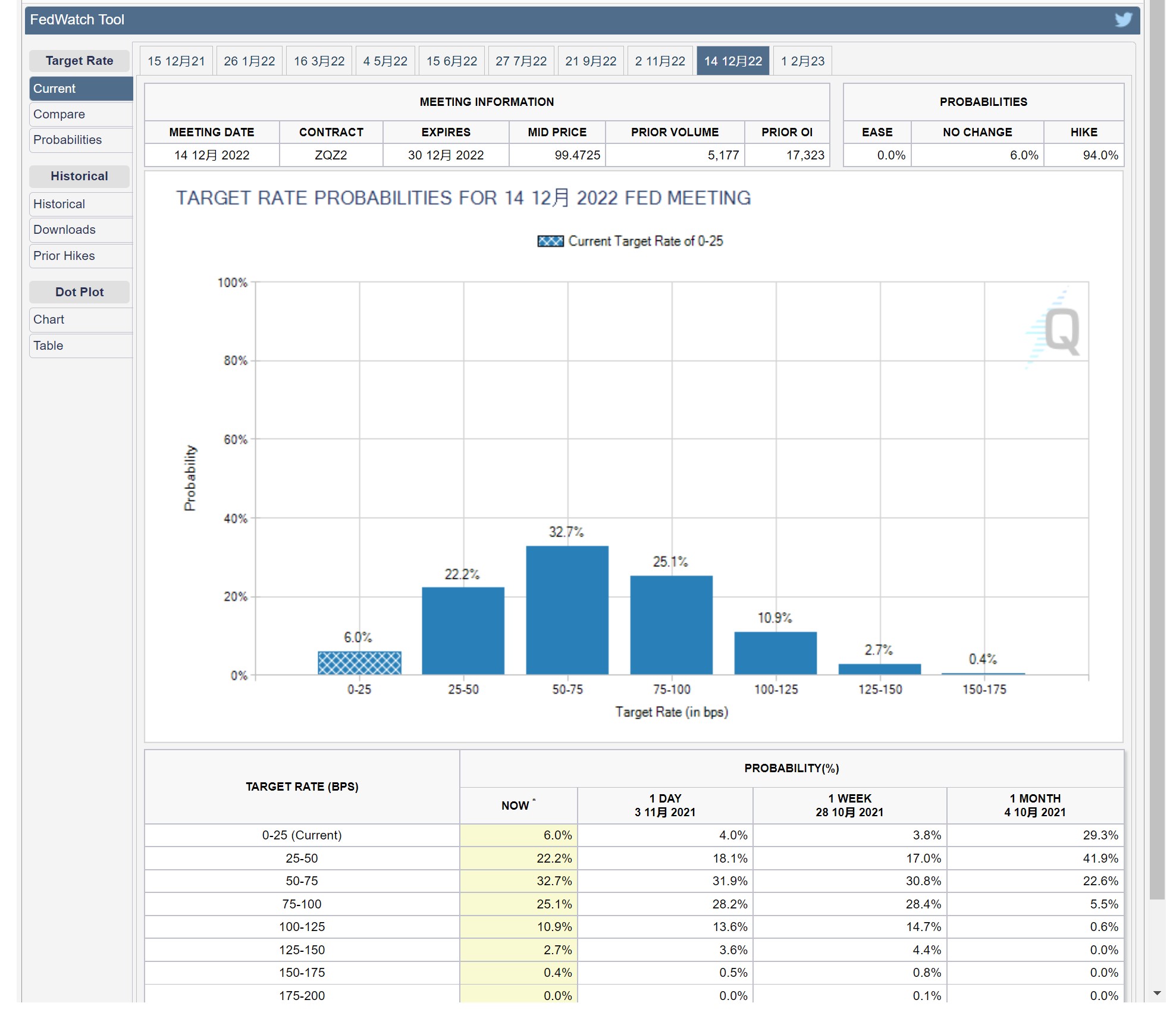

Just this week, the Feds announced the tapering of QE, to end completely by June 2022.

And markets are pricing in anywhere from 2 – 3 rate hikes by Dec 2022:

If so, that’s going to be a massive headwind for growth stocks, and some caution is warranted.

That said, most of these growth stocks are secular plays, with the potential to grow their core business for years to come.

As investors, we can’t control the macro, we can only control what we buy, and when we buy.

For solid companies with secular growth and >50% year on year revenue growth, I’m happy to buy and keep buying on declines.

As always, this article is written on 5 Nov 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi,

the valuations are quite insane for the above stocks and most of them don’t even make any profits yet (still burning lots of cash). The next stock downturn may cause a crash in these stocks. But having said that, they may run up even more before crashing. And whether they will return to previous highs, not so sure. So I’m having a dilemma whether to join in the party or not.

I’d prefer to buy safer classics like Nvidia/AMD/ASML and other green energy related since we will see secular demand for chips even though their growth rates are not as high.

Cloudflare — I just don’t understand what’s the appeal of their services, even with my software background. They have a huge overlap with cloud platforms like AWS/Azure, no? What’s stopping Amzn and Msft from copying them wholesale?

They are a commodity product with little switching cost.

Oatly — another low-tech commodity product with *very* intense competition. Their only moat is their brand. There are other better products with organic + enriched vitamins.

Digital ocean — also don’t get it why they’re so popular. I used before, it’s just a clone/subset of AWS and cheaper for sure. That’s about it. Nothing amazing other than the cheapness. What’s stopping other cloud players from cutting their prices to compete?

For tech, it’s better to invest in those with strong moat, stickiness and high switching costs. Nowadays, any tech startup can come along, raise capital, burn cash and lure customers away. I.e. burn cash to disrupt. I only believe in those with patented/hard tech/AI which provide strong moats. SaaS like ServiceNow/Salesforce has some moats but may not be the strongest. The entire SaaS sector is very matured, that’s why we can only see younger startups using the burn cash method to gain market share, but what’s stopping new entrants from doing the same to those startups? Thats why BioTech/AI/chips would be better for longer term investments.

I feel like these stocks only good for short-term trading, good for making quick profits . Like Tesla, their ‘growth’ may eventually slow down once competitors catch up, and then we will see a ‘pop’ in their stock prices (like PINS/SNAP). I think the pandemic and huge money printing has driven up the valuations of growth stocks.

I have a long-term portfolio which is ‘get rich slow with strong moats’ and another portfolio which is ‘get rich quick but with higher risks’ (aka growth stocks with little moat).

I think you should do research into AI/hard tech /quantum/space/biotech/green energy — that’s where the future is. I’d very much be interested in that.

Man after my own heart! I too have a long term portfolio filled with all the boring slow burn stocks, and another portfolio with the high risk high return stocks (kinda like those on this list). 😉

Any good names to recommend in AI/Quantum? Most of the best ones are still private?

When there are no clear winners, one good strategy is to buy the related ETFs until some companies emerge. Big Tech like Google is also working on quantum.

I used to avoid ETFs as I thought their returns are low. But I have since discovered that some ETFs e.g. related to green energy have been multi-baggers since 2020. Eg. LIT, TAN, ICLN. Imagine if you had went all-in, you’d have tripled or quadrupled your portfolio in a relatively lower-risk manner (vs all-in on a few growth stocks). I’m looking at opportunities to enter these ETFs. Sometimes boring stocks may provide very decent returns on a good risk/reward basis.

That’s interesting, appreciate the sharing.

I own names like NVIDIA, AMD, Salesforce etc too, but at these prices can they really do a 5x? Once you’re at 200b, how much higher can you go from there?

The point of keeping the names on this list below 50b is that there is the potential for a 3-5x if they execute well.

I actually agree with most of your comments above. Those are very legitimate concerns. But we do need to recognise that if the companies above have found a way to solve the problems you raised, their valuation would be 5x higher than where they are now. We’re betting on the future here, and the future carries uncertainty.

It’s like buying Amazon in 2005 before they became world beating juggernaut. Sure, there were a ton of problems with the business model, and no guarantees they would solve them.

Which is why it all goes back to risk-reward, and proper position sizing. As long as you limit growth stocks to an acceptable size of your risk portfolio, they could be a great way to juice returns if you get the picks right. 🙂

But problem is we don’t know when the music stops/growth stops for some of these stocks. Look at Moderna/BioTech, their stocks have popped. Can we as retailers get out in time? I think it’s about setting a target for your portfolio e.g. 20% per annum, and then look at safer bets that can /likely to produce such returns. There are quite a number of small/mid-cap high growth stocks outside of SaaS that are profitable and have some moat e.g. patents. These have potential to be multi-baggers. Also pick growth stocks that burn cash to build moats (e.g Amzn building logistics) rather than to blindly capture market share without moat.

But why would you intentionally set a target performance for your portfolio? Isn’t the better approach to determine how much risk you are prepared to take on, and for that level of risk devise the portfolio that can achieve maximum gains?

So if risk appetite is low, then maybe allocate 10% of the portfolio to high risk stuff, and the rest to large cap dividend / moat style stocks. But if risk appetite is high, there are certain market conditions (perhaps like now) where the potential upside can be very high.

All these growth stocks have become a race for “who can burn the most cash to capture the most market share” lol — looks to me somewhat like a ponzi scheme/Greater’s fool theory. What will happen when they stop burning?

To be fair this question has been asked for the past 10 years, and tech companies are still burning cash for market share. 😉

Think about it, if the product is truly good and must-have, why do you need to burn so much cash? Apple, Msft and Oracle were profitable at the start.

The way I look at this is:

From iPhone 3 => iPhone 8 is huge improvement

From iPhone 8 => iPhone 13 is incremental improvement

From Windows 3.1 => Windows XP is huge improvement

from Win XP => Win 10 is incremental

Every next iteration yields less and less innovation and benefit for the customer => marginal returns. You;d be surprised why many companies are using legacy software and refuse to change or they don’t update very often — simply because they don’t see much benefits and they dont want the operational risks that come with it. That’s why many of these SaaS startups have to provide the incentives for companies to switch — this already tells you how little moat or benefits they provide for their customers. Also once these starrtups become profitable, their profit margins become opportunities for Big Tech.

Hm interesting. But at the start, some of the big tech like Amazon / Facebook were burning cash for market share too? With many of these SaaS players, doesn’t the moat come from their network effects, which itself requires the market share?

Many of the saas have no moat. Like cloudflare, cdn and ddos services low cost of switching. The tech is matured. There usually no network effect. They need to burn cash to defend their moat. Even tiktok can capture market share so quickly, you think FB has a strong moat? Gen z are avoiding fb. Fortune 500 companies life cycle are only a few decades. If you have worked at a corp before, you would know how often they change tools, although it comes with op risks. Those with strong moat are like amzn, strong logistics, which shopify and walmart dont even dare to compete with. Who would burn billions to fight? Deep tech also strong moat as you cannot possibly catch up with years of R&D overnight. Only those saas with strong ecosystem that are always innovating provide strong moat and even so, new comers can always catch up

Hm so what would you propose investing in instead?

Repeat of 2000.

I worked in semicon all my life but I don’t invest in them. The memory of 2000 still haunts me. And probably, as an insider, I see more business risks than outsiders.

A wise man once said if I work there and use my salary to buy their shares, I am doubling my risks. Recently a friend who worked in that infamous bankrupt water treatment company lost a job + the 6 digits money he poured into the company shares, perps, bonds. So the wise man did have wisdom. Lol.

That is a great way of seeing it. Very wise indeed.

To take it one step further, I suppose for those of us who earn in SGD, own a home in SG, using money to buy SG stocks is trippling down on Singapore!

You may interpret that way. So important to diversify especially into totally uncorrelated assets, just in case. And don’t be over confident. Think risk first, not reward first.

Agree with this. My only concern is that in today’s market, almost every asset class is correlated with each other. We saw this in March 2020 when even traditional hedges like Treasuries and Gold were selling off due to liquidity – only stopped when the Feds stepped in. The whole world has become a single leveraged long trade.

Agree with this. My only concern is that in today’s market, almost every asset class is correlated with each other. We saw this in March 2020 when even traditional hedges like Treasuries and Gold were selling off due to liquidity – only stopped when the Feds stepped in. The whole world has become a single leveraged long trade.

Everytime ppl say this time is different, but actually everytime it’s always the same! All valuation will be eventually dragged down by gravity, this is a “supreme rule” above any fancy theory to support the high valuation. Maybe someone will say, I know it’s going to hit the iceburg, but it’s huge! I can see it from distance, so will jump off way bf we hit it. Guess what? literally nobody escaped.

True, quite a few readers have pointed this out.

I suppose the question then is going back to 2013 and looking at Amazon at 300 times PE, how do we differentiate the Amazons from Nikolas? The true Amazons will continue growing even with macro headwinds, but the Nikolas will die horribly. The challenge is picking the right ones.