I was looking at the latest Fixed Deposit Rates recently.

And they are frankly quite attractive with rates of up to 2.85%.

Remember, with fixed deposit there are no allocation limits (unlike Singapore Savings Bonds), so you can put in fairly large sums if you want.

And unlike T-Bills where the liquidity is a real problem, with Fixed Deposit if you really need the cash you can break the Fixed Deposit with a small penalty fee, which is a great option to have.

So with rapidly rising interest rates (3.5% – 3.75% by early 2023), it’s probably worth spending some time discussing Fixed Deposits.

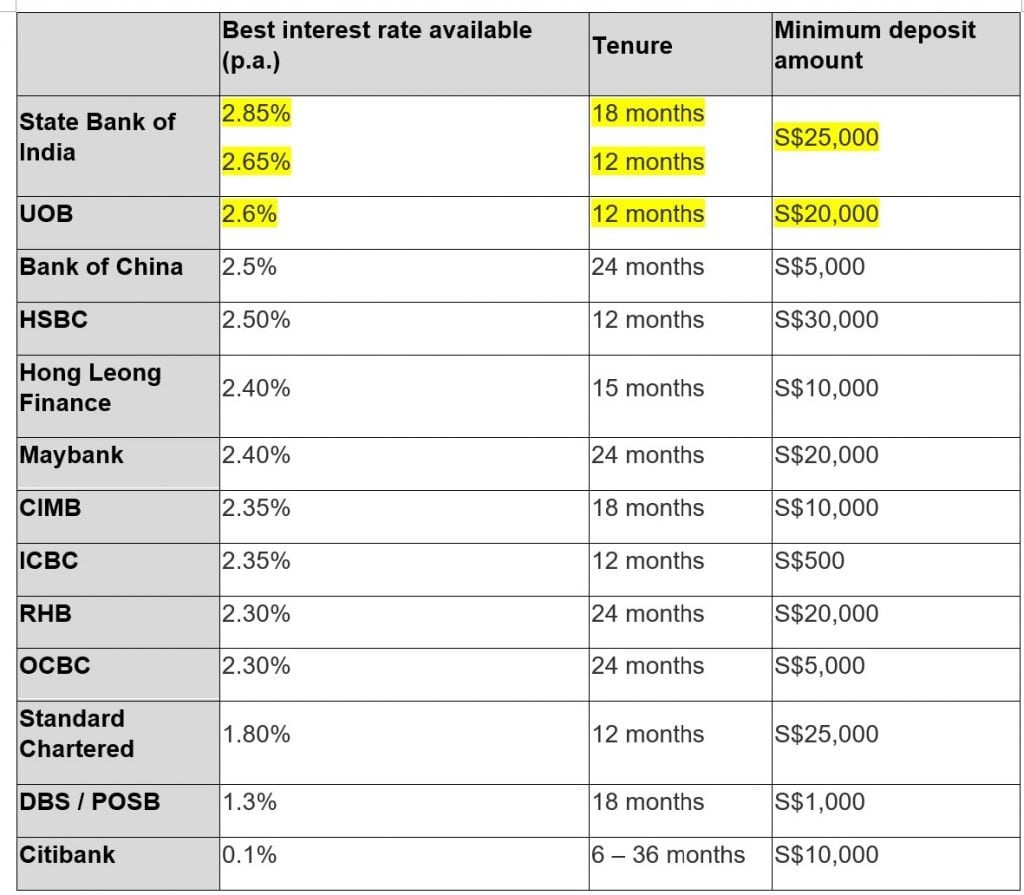

Best Fixed Deposit Rates in Singapore (September 2022)

I’ve set out the latest Fixed Deposit Rates in Singapore below.

The best rates you can get right now are highlighted in yellow:

- 2.85% for 18 months at State Bank of India

- 2.6% for 12 months at UOB

Fixed Deposit Rates are frankly very good – 2.6% for 12 months, 2.85% for 18 months

For the record, these Fixed Deposit Rates are very good.

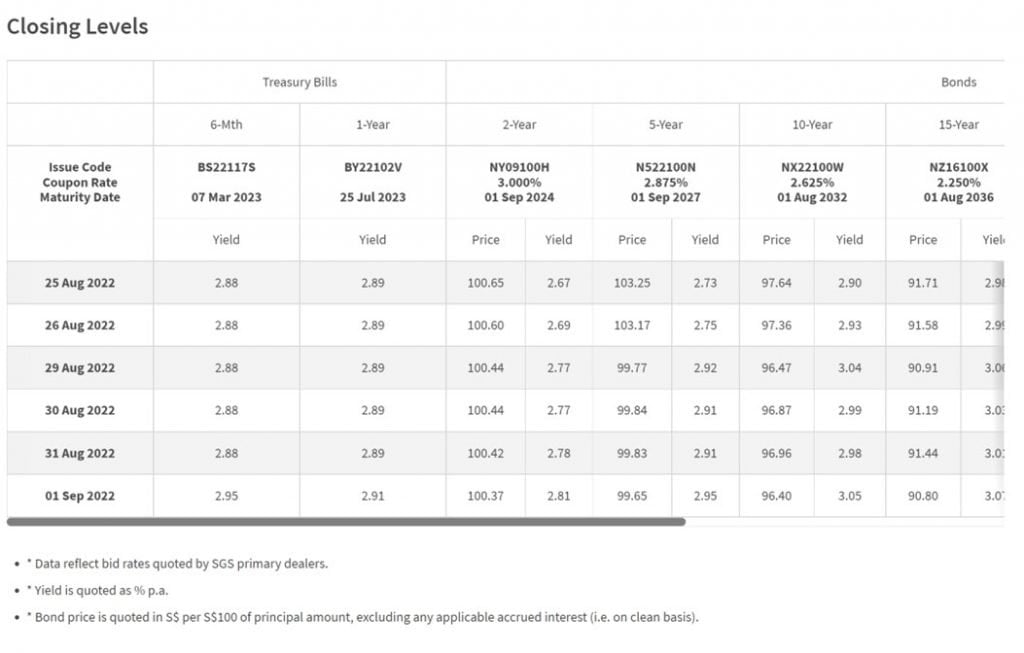

As reference, here’s the latest Singapore Government Securities (SGS) yields:

You’re looking at 2.91% on the 12 month yields, and about 2.8% on the 24 month yields.

With the latest Fixed Deposit, you can get 2.85% on an 18 month fixed deposit from State Bank of India:

Or 2.6% for 12 months from UOB:

Which is very close to the latest market pricing on Singapore Government Securities.

SDIC Insured (up to $75,000)

And because Fixed Deposits are classified as bank deposits, they are SDIC insured up to S$75,000.

Basically you can pick any bank that you want, and the amount you deposit is absolutely risk free up to S$75,000.

If you want to go beyond S$75,000, and you’re worried about the solvency of some of the smaller banks, then you could just stick with UOB.

The 2.6% for 12 months is very decent, especially coming from a local bank.

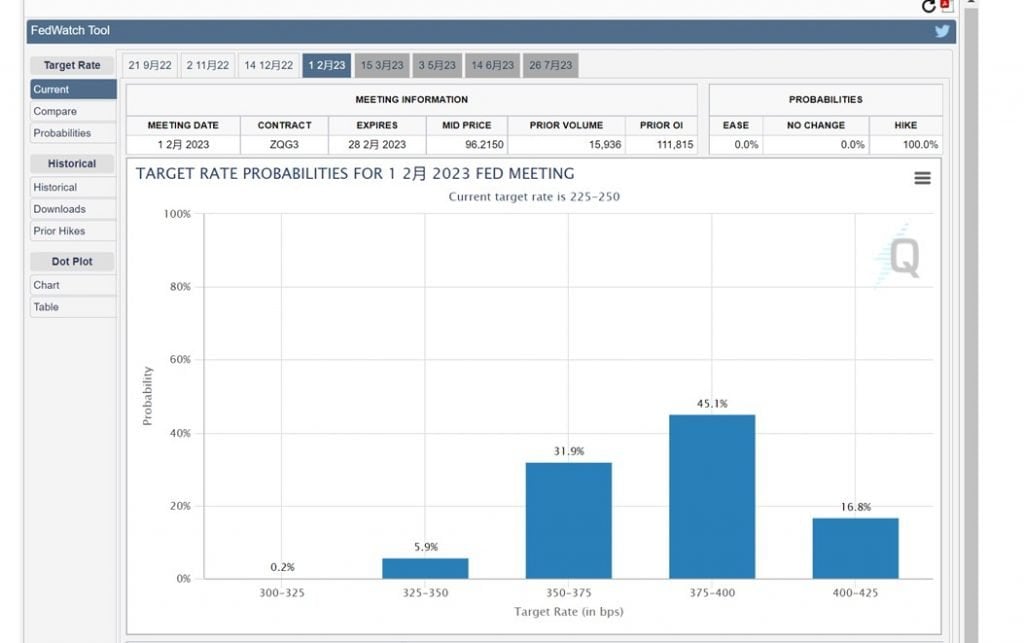

Will Interest Rates go up even further?

Now I know that many investors are waiting for interest rates to go up even higher before locking in their money.

For the record – I agree that interest rates are going up.

The market is pricing in a 45% chance of the Feds Funds Rate being at 3.75% – 4.0% by January 2023.

It’s going to be the highest interest rates we’ve seen in a decade.

Sidenote that this is why I’m not particularly excited to deploy my cash into financial markets just yet.

Even with a “soft landing” you’re going to see terminal interest rates at close to 4.0% for this cycle, which is going to cause havoc across the global economy.

So yes, for the record – I do think you’ll get better interest rates by end of 2022 or early 2023.

Don’t be penny wise pound foolish though.

Because if you’re going to chuck the cash in a savings account to earn 0% from now until the end of the year, you might be better off just deploying them somewhere first, even at a lower yield.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What happens if you need your money back early? (Ie. Is there liquidity?)

If you wanted your money back early, you can let the bank know to break the fixed deposit early for a small penalty fee.

The penalty usually takes the form of a lower interest rate.

Every bank has a slightly different policy on the penalty though, so it is best to check with the specific bank you are depositing with.

The legal T&Cs will also say that the bank has the right to not allow you to withdraw your monies early.

But in my experience this is very rarely exercised (outside of a financial crisis), and you *should* be able to get your money back with a small penalty fee.

Whatever the case, it’s not as bad as T-Bills though, where it’s almost impossible to get your money back before maturity.

Fixed Deposit vs Singapore Savings Bonds vs T-Bills / Singapore Government Securities – Which to pick?

To sum up the pros and cons of each instrument:

|

|

Singapore Savings Bonds |

T-Bills |

Fixed Deposit |

|

Interest Rates |

Average |

Good |

Average |

|

Risk Free |

Yes |

Yes |

Up to $75,000 SDIC insured |

|

Allocation Limit |

Poor |

Good |

Good |

|

Liquidity (ability to exit before maturity) |

Good |

Poor |

Average |

|

Ability to lock in interest rates long term |

Good |

Poor |

Average |

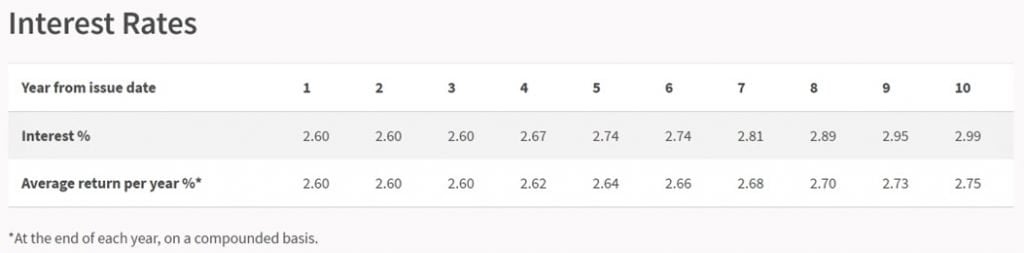

Singapore Savings Bonds (October 2022)

Latest Singapore Savings Bonds yields are set out below, you’re looking at 2.6% for the first 2 years.

That’s in line with the Fixed Deposit Rates, but not as good as T-Bills.

But Singapore Savings Bonds can be redeemed any time with no penalty, and give you the option of holding up to 10 years with interest rates that are already locked in.

The problem of course, is allocation, with each person only getting up to $13,500 the last month.

T-Bills

T-Bills yield 2.95% for 6 months, so if all you care about is getting the highest interest rates then t his is the place to be.

There is also no limit as to how much you can apply

With T-Bills you do sacrifice the liquidity, as they are close to impossible to sell / redeem prior to maturity.

And because the duration is only 6 months (or 12 months), if interest rates are lower on maturity there is a bit of a “refinancing risk”.

Fixed Deposit

Whereas with Fixed Deposit, there’s no limits on allocation.

Yields are decent too, as discussed in this article.

And you do have average liquidity, because you have the option to exit early with a small penalty fee.

What am I doing?

I think for me in this climate – liquidity is king.

With interest rates rapidly approaching 4.0% terminal by early 2023, I think at some point in the next 12 – 18 months something is going to break.

I need to be able to access my liquidity rapidly if so.

And I am probably fine to accept a slightly lower yield on my cash, as a cost of that liquidity.

So my favourite instrument for my cash remains Singapore Savings Bonds, for the ability to redeem any time with accrued interest (with up to 1 months delay).

And I keep some cash in a high yield savings account, as I do need the instant liquidity for daily needs.

T-Bills have real liquidity issues, so I would probably only use it if I don’t see myself needing the funds for 6 months or more.

Fixed Deposit could come in handy to plug the gap.

That being said, I do think if I am using a fixed deposit I would probably just wait a couple months until end 2022 or early 2023, and lock in the 3%+ interest rates.

But hey – that’s just me.

The exact mix and allocation will have to depend on each investor.

Love to hear what you think!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try here.

As always, this article is written on 3 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

1. Your yield% for TBills is based on discount rate (d)? Effectively, the equivalent interest rate (r) should be r=d/(1-d). Which means r is more than 3% p.a.

2. Last walkin to UOB on 1Sep placed 2.7% FD for 15mth.

No I didn’t use any discount rate when calculating the yield – so you are right the r would be higher.

Thanks for the heads up on the 2.7%! 🙂

I thot interest rate is going up, then why spore savings bond interest going down? Any idea?

It’s a short term trend vs the mid term trend.

Interest rates went down last month together with the stock market rally, but it has since gone up again. SSB yields the next few months *should* go back up.

BEA FD 12 month, 2.88%, min100k

Thanks! Didn’t want to include this originally because of the 100k minimum, but I probably should. 😉

Can please explain how t bill works? Say apply at atm $1000 and latest cut off yield is 2.99%. Is it 6 months later when it is due, i will get back $1000 + 2.99% interest? That is 1000+29.9=$1029.90?

Thank you.

T-Bills are issued at discount to face value. So you get the interest (2.99%) when you get the T-Bills, and the principal back 6 months later ($1000).

oh….