So… CapitaLand called for a trading halt this morning…. for CapitaLand, all the CapitaLand REITs, Ascendas REIT, and Ascott REIT.

That’s when you know something big is coming.

And boy, they didn’t disappoint.

Because the deal that they announced was a mega deal.

I’ve had a lot of requests to break down CapitaLand’s restructuring, and I’m more than happy to do so.

It’s quite a complex deal, and the implications for shareholders are not that easy to decipher.

Anyway, lot’s to cover, so let’s dive right into it.

What is going on with CapitaLand?

To sum it up in one sentence:

CapitaLand is privatizing their development business.

That’s it.

The details are a lot more complex, but if you take away one thing from this article, let it be this.

CapitaLand is splitting their business into 2:

- CapitaLand Development – Which is the property development business (builds new properties, and holds the developing assets)

- CapitaLand Investment Management (CLIM) – Which holds the mature assets (after property income has stabilized), the REITs, the private funds, the property managers, and the hospitality business.

CapitaLand Development, which holds the developing and younger assets, will be privatized.

CapitaLand Investment Management, which holds the mature assets, will remain listed.

How is CapitaLand doing this?

So now we get into the details.

The current structure of CapitaLand is set out below.

The box circled in red, is what will remain listed after this restructuring. The development business will be privatized.

After the restructuring, this is what the new CapitaLand will look like.

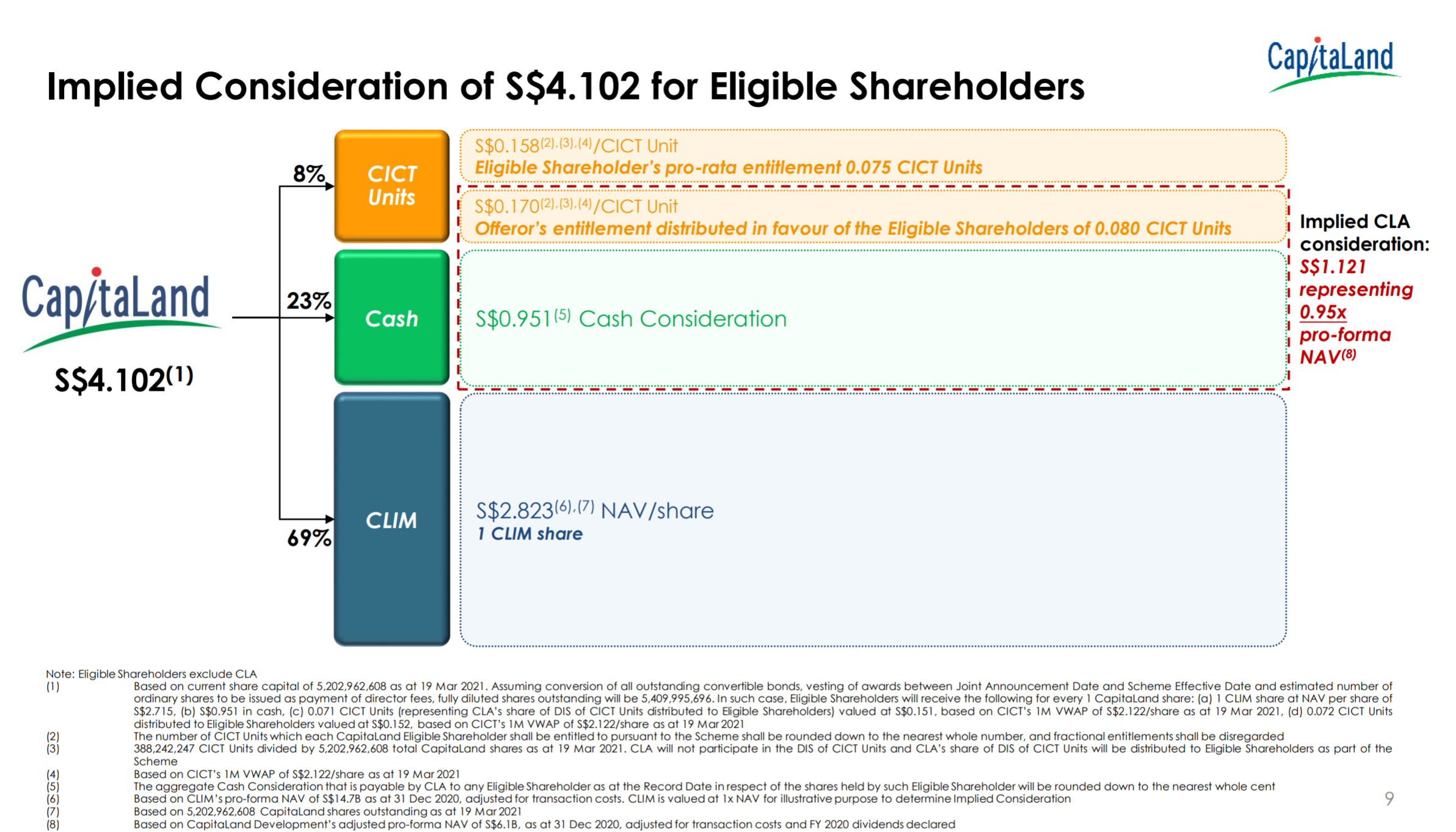

And the way this transaction will be effected, is that all CapitaLand shareholders will receive:

- 1 share in the new CapitaLand Investment Management (CLIM)

- $0.951 in cash

- 0.080 units in CapitaLand Integrated Commercial Trust (CICT)

- 0.075 units in CICT

So the way to think about it is this.

Originally there was the CapitaLand Investment Management Business + CapitaLand Development Business.

The former will stay listed, and you get shares in CLIM.

The latter will be privatized, and CapitaLand is paying you $0.951 cash and 0.080 units in CICT per share in CapitaLand.

And they’ll throw in another 0.075 unit in CICT as a bonus.

Not that complex right?

Don’t forget to join our Telegram Channel and Instagram(or YouTube) !

[mc4wp_form id=”173″]

So CapitaLand is worth $4.102 per share now?

Yes, and no.

The $4.102 per share assumes the new shares in CapitaLand Investment Management (CLIM) trades at 1 times NAV on the open market after this restructuring.

Markets being markets – they may refuse to cooperate, and we may see CLIM trade above or below NAV.

For reference, CapitaLand’s share price has traded below NAV over the past few years, so it remains to be seen if the same thing will happen with the new CapitaLand Investment Management.

Why is CapitaLand restructuring?

According to the CEO (emphasis mine):

This restructuring is about sharpening our focus and positioning ourselves to be an asset-light and capital-efficient business. We have made good progress to pivot ourselves to the new economy sectors, expanding our global footprint and growing our fee-income business. We are now taking the next step to create a leading global real estate investment manager with dominance in Asia, especially through our track record in the public REITs space. As listed REIMs generally trade at a premium to their NAVs in the capital markets, we are confident that CLIM will be able to drive returns for our shareholders given its scale, capabilities and a strong ecosystem.

The real estate development business is subject to longer gestation periods and not adequately appreciated by the public markets. With a privately held development business, we will be able to better ride property development cycles to optimise returns across asset classes and geographies. We can make more appropriate risk-return decisions to undertake attractive but longer gestation projects, and optimally build our pipeline and incubate projects. With the privatised development arm as a key source of pipeline for CLIM, the well-established CapitaLand ecosystem remains intact. This symbiotic relationship within the Group will be a major advantage for CLIM and differentiate it from other real estate investment managers.”

Basically, it is to unlock shareholder value.

The development business is a risky business.

You take on development risk (eg. risk of delays or contractors going bankrupt), you wait years for the property to complete, and when all that is done you may get a market crash like COVID which affects real estate prices.

So the public market doesn’t like the development business, and rightly so.

This is why the listed REITs tend to trade at a premium to property developers like CapitaLand, Frasers and CDL.

So the thinking here, is that if you take the development business out of CapitaLand, and you leave the mature assets + stakes in the REITs + the fund management business, the market may give the share a higher multiple.

In other words – unlocking shareholder value.

What will remain in the listed CapitaLand?

What will remain, is:

- Stakes in the CapitaLand REITs that used to be held by CapitaLand:

- CapitaLand China Trust

- CapitaLand Integrated Commercial Trust

- CapitaLand Malaysia Mall Trust

- Ascott REIT

- Ascendas REIT

- Ascendas India Trust

- Stakes in the unlisted Funds (eg. the Raffles City Funds)

- Stakes in the mature properties (eg. Ion Orchard, Galaxis)

- The hospitality business (Ascott)

- The operating platforms (property managers)

How will CapitaLand’s share price trade tomorrow?

I would say the share price goes up – but how much it goes up by is tough to say.

It all depends on how the market would value CapitaLand Investment Management, which is not that easy to figure out.

It’s still a very big company with very diverse asset classes, and a very large global footprint.

It’s not like a REIT where the valuation is more straightforward.

With this many properties over this many countries, and so many diverse businesses, really tough to call how the market would value it.

Gut feel is that 1x NAV is a tad optimistic, but let’s see.

Do I like this CapitaLand restructuring?

Full disclosure – I am a CapitaLand shareholder, and I hold a stake in CapitaLand.

My initial instinct is that I like this restructuring.

The way I see it – doing something is better than doing nothing at all.

CapitaLand’s share price has been languishing below NAV for the longest time, and perhaps this could be the catalyst that changes things.

But truth be told, it’s not that straightforward to value the new CapitaLand Investment Management Business.

All that’s changed really, is to remove the development business from the listco.

Will the market give CapitaLand a good valuation after this restructuring?

I’m not so sure as well.

The trading over the next few weeks would be very interesting.

What am I doing with my shares in CapitaLand?

I haven’t decided yet.

My initial reaction to this restructuring is positive, but I’m not sure if I’m missing anything here.

I really want to see how the market reacts over the next few days.

And give myself more time to mull over the deal.

So I might do a fuller article this weekend if there’s interest. Let me know in the comments below!

Would love to hear your thoughts on the CapitaLand restructuring as well!

As always, this article is written on 22 March and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Nice summary of what’s happening!

Since CICT shares will be given to Capitaland shareholders based on certain valuation, any thoughts on how this may impact CICT’s price?

Will share more thoughts on the REITs this weekend. Initial view is that the new CLIM has the potential to become a cheaper way to get exposure to the underlying REITs (many of which are trading above NAV). Might explain why the REITs sold off slightly today.

Hi FH

I’m not a expert in analysis, but I do feel that alot of investors tend to avoid property development business sectors which is cyclical like oil & gas , offshore Marine… Etc. Divesting property development business does on paper seems be able to give investors a second look on Capitaland as an viable investment. On top of the fact that Sg investors liked dividend stocks like Reits, and this might have an positive effect on the new CLIM stock.

I might be wrong though. Would love to read your indept analysis again.

Regards

Boon

Great comment Boon, and yes I agree with that. Removing the development business is indeed a good move for the stock.

I will share more views this weekend, esp on the impact for the REITs. CLIM is quite an interesting vehicle the more I think about it, holds the same REITs + Funds, but trades at a discount to NAV when the REITs trade above book value.

Great article and good analysis.

Glad you like it! 🙂

You’re spot on regarding moving the development to CLA and leave the CLIM as an investment company. I believe investors will end up valuating this new entity higher that the NAV. That said, this is not the only point. It leaves CLIM a free reign to transform from a totally fixed income management company to risk/fund/ mutual management. It all depends how aggressive is the new entity. Many companies has made similar transformation, potential singapore companies should also follow suit for higher growth potential.

Really good comment Chas, and the more I think about it the more I agree. CLIM may have the potential to trade quite strongly going forward. Holds the underlying REITs which all trade above NAV, while CLIM trades below NAV? Quite an interesting situation.

What happened to the dividend of 0.09 cents. What is the XD and why is the CD disappear from ticker. So can we still get the dividend if we buy or sell now ?

Best to check with your broker for this one. 🙂

Hi Financial Horse, firstly, really enjoyed your comments and articles, please keep up the good work! My gut feel is that Capitaland had recycled their capital by monetizing their Reit assets at the peak of the latter’s cycle. This is maybe evident that shareholders of CICT, etc are all trading with weakness now…the Reits’ holders may realise that capital appreciation for these assets maybe a thing of the past (the current steepening yield curve probably set off Capitaland’s decision to do this deal…). Hence, it really depends what is an investor’s objective of holding the Reit assets going forward. Definitely good for current Capitaland holders more than the new entities… what do you think?

That’s interesting. I will share more views on the REITs this weekend. Prelim thoughts are that the new CLIM has the potential to become a cheaper way to get exposure to the underlying REITs (many of which are trading above NAV). Might explain why the REITs sold off slightly today.

I’m also of the view it’s a good move by Capitaland, both for existing Capitaland shareholders and prospective CLIM shareholders. Given the attractive deal they’re offering, it’s more likely than not that the price of Capitaland will continue to appreciate in the coming months before reaching an equilibrium at around $4.

Yeah understand your point. I’m starting to warm up to this idea as well. Esp when all the REITs are trading above NAV right now.

Hi FH, always enjoy reading your articles! Would it be correct to say they are paying $0.95 cash for the development business? Why did they have to top up with the CICT shares and even offer up their own entitlement? Indeed why CICT in particular?

Yes that’s correct. Good question – only management will know the answer. You’re right in that they could have paid in units in any of the other REITs instead, even Ascendas.

Hi FH, always enjoy reading your articles! Would it be correct to say they are paying $0.95 cash to existing shareholders for the development business? Why did they have to top up with the CICT shares and even offer up their own entitlement? Indeed why CICT in particular?

Yes that’s correct. Good question – only management will know the answer. You’re right in that they could have paid in units in any of the other REITs instead, even Ascendas.