A lot of you may have seen the news about homebuyers protesting at Evergrande offices in China this week.

Evergrande’s debt issues have been well known for a long time, but things really started accelerating the past week – and a default looks virtually certain now.

But beneath the surface, this is a massive event for China credit, with a real risk of contagion.

I’ve seen a lot of hot takes out there on (1) this is China’s Lehman, or (2) Don’t worry the CCP will bail them out, that are getting it wrong.

The reality, is far more nuanced.

I’ll do my best to break down what is happening, and share my views on what’s coming next.

What is Evergrande (恒大)?

Now Evergrande isn’t some small SME, it’s China’s second-largest property firm by sales.

They own more than 1300 projects across 280 cities in China.

They have sold 1.7 million homes to Chinese homeowners, on which payment has been collected but construction is still in progress.

So this is potentially a too big to fail kind of property developer.

And this is Evergrande’s share price, down 81% the past year.

Evergrande (恒大) Timeline

I’ve set out a simplified timeline below.

If you’re pressed for time, feel free to skip straight into the TLDR version below.

Aug 2017

- Evergrande vows to cut its debt for the first time, aiming to slash net gearing ratio to 70% by June 2020 from 240% in June 2017.

Nov 2018

- The central bank names Evergrande in a report as one of the few financial holding conglomerates on its watch that it says could cause systemic risk.

Aug 2020

- Regulators meet with 12 major property developers, including Evergrande, in Beijing to introduce caps for three different debt ratios in a pilot scheme, dubbed “the three red lines”. These are:

- Liabilities / Assets < 70%

- Net Leverage < 100%

- Cash to Short Term Debt > 1

Nov 2020

- Evergrande Property Services Group’s (6666.HK)Hong Kong IPO raises $1.8 billion.

Jan 2021

- Electric vehicle unit China Evergrande New Energy Vehicle (0708.HK)raises $3.4 billion by bringing in six new investors.

July 2021

- A court orders a freeze on a 132 million yuan bank deposit held by Evergrande at the request of China Guangfa Bank Co

- Fitch downgrades Evergrande to “CCC+” from “B”.

Aug 2021

- Construction work halted on two Evergrande projects in Kunming, one of them for overdue payments and the other was scheduled to deliver to homebuyers in October.

- China’s central bank and banking watchdog summon Evergrande’s senior executives and issues a rare warning that the company needs to reduce its debt risks and prioritise stability.

- Evergrande issues an earnings warning, expecting as much as 39% drop in its first-half net profit.

September 2021

- Evergrande said on Aug. 31 that work has been suspendedon some real-estate projects after it delayed payments to its suppliers and contractors, and warned for the first time that it may default on its borrowings if it can’t resolve its liquidity problems.

- Both Moody’s Investors Service and Fitch Ratings cut their credit ratings on the company deeper into sub-investment grade.

TLDR: What happened with Evergrande?

Evergrande is a classic example of what happens when an overly indebted property developer borrows too much money, to grow too fast.

When things were good, they borrowed a lot of money, and they bid for land at prices significantly higher than market prices.

This didn’t matter to them, because the risk was transferred to home buyers, and the banks that financed the purchase.

This worked well for local governments, households, and banks because house prices went up in a straight line.

The problem though, was that this couldn’t keep up forever.

Over the past 15 years, house prices in major cities (and mortgage debt) soared. To the point that very few people can afford a house in a Tier 1 city in China today.

The problem of this is twofold. (1) The amount of real estate debt in the system is very high, creating leverage and repayment issues. (2) The real estate debt was crowding out more productive sectors like technology and manufacturing, preventing China from rebalancing towards a consumption driven economy.

If China didn’t solve the problem, there was a real risk they would have become Japan Part II, and Japan’s lost decade after their bubble burst in the 1990s.

So China started on the deleveraging move (the three red lines), and things started getting really hairy.

What happened this week with Evergrande?

Things really accelerated the past week:

- CCP tells Banks Evergrande won’t pay interest next week.

- Evergrande’s onshore bond trading suspended.

- Evergrande employees in China held hostage as worried investors demand payments

- Investor protests at Evergrande offices

- PBOC injects 90 billion RMB of liquidity, the most since February 2021

Next Week (20 Sept)

- Evergrande is scheduled to make interest payments due Sept. 23 of $83.5 million for a dollar note and 232 million yuan for a local note

Is Evergrande definitely going to default?

Once a property developer lacks the cash flow to pay their contractors (early Sept), things go bad really fast.

Once you stop paying your supplier / contractors, they stop work on your existing construction projects.

Once they stop work, you can’t complete your projects, and you cannot collect cash from your buyers.

Usually when a property developer enters this phase, there’s almost no way out – unless you get external help, or if the creditors come together to restructure their debts.

To put things in perspective, Evergrande owes about 1 trillion RMB to its suppliers, which is $155 billion USD. For a company that only has about $40 billion USD in assets now.

Long story short – Yes, a default is virtually certain at this stage.

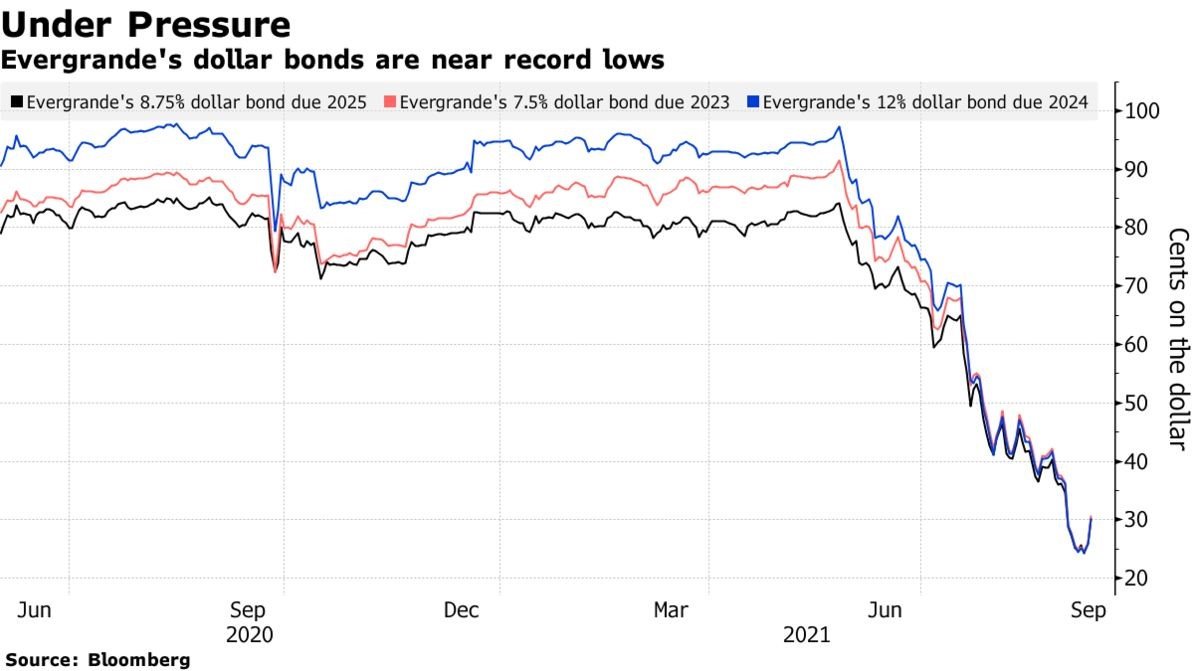

The market knows this too, so Evergrande’s dollar bonds have absolutely collapsed.

The dollar bonds from 2023 out to 2025 are all trading at about 30 cents on the dollar.

Is there any other way out for Evergrande?

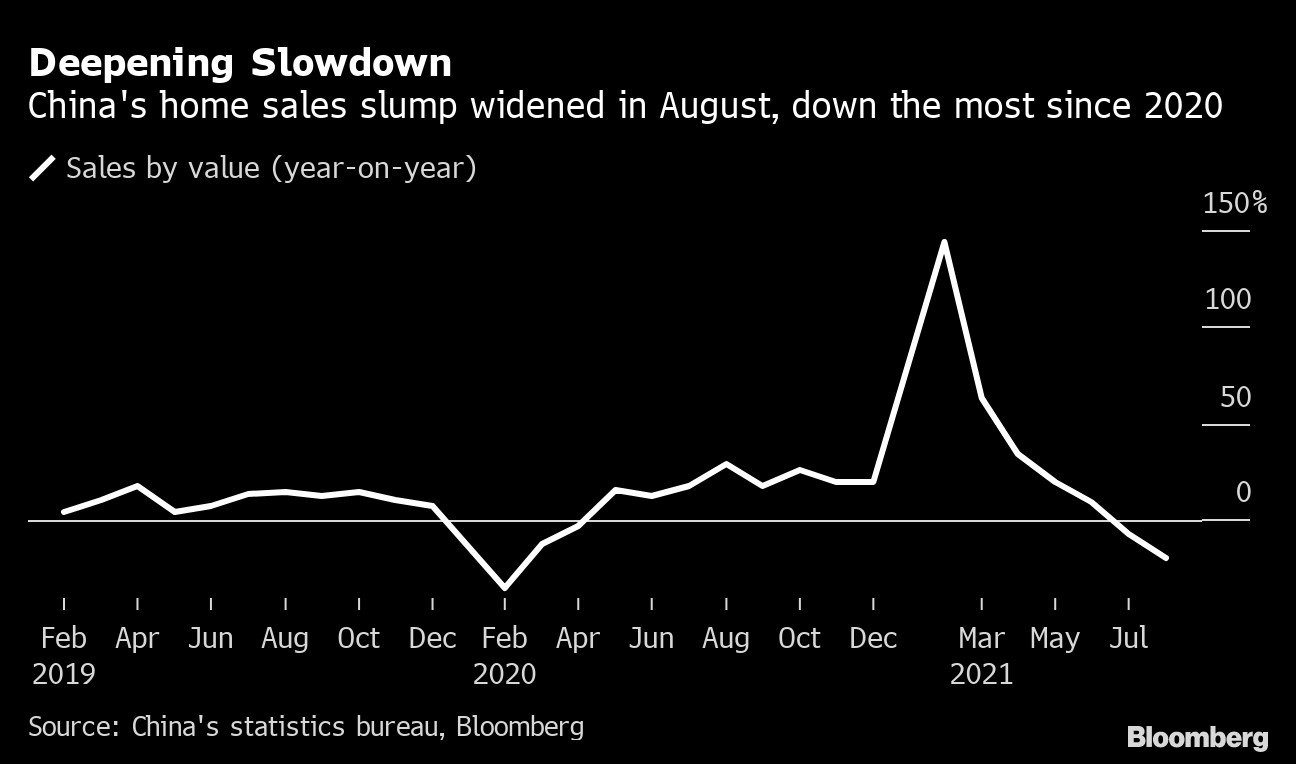

Evergrande can sell land or assets to raise liquidity, but when there’s blood in the water, everybody smells it.

So liquidity in the real estate market in China has dried up – land transactions down 76% year on year in August 2021.

What can be sold has already been sold – bottled water, and the two listed entities (EV and Property Services) have seen their share price collapse due to their links to Evergrande.

And don’t forget that all other property developers in this market are under the same leverage limits – which limits their ability to buy from Evergrande.

BTW – we share commentary on Singapore Investments every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

What happens next?

So that’s where we are today.

What happens next? How is this going to play out?

3 possible paths forward:

- Best Case (CCP Bailout)

- Base Case (Orderly restructuring)

- Worst Case (China’s Lehman)

Best Case (CCP Bailout)

This is the best case scenario – a complete or partial takeover by a State-owned Entity (SOE), presumably on Beijing’s orders.

Once a SoE comes in, it will be taken to be sanctioned by Beijing, and amount to an implicit bailout by the state.

Conditions across the board will stabilise for property developers and property prices.

As the market recovers and conditions stabilise, Evergrande can sell its assets at better prices.

In this scenario, bondholders can see recovery of 30 cents or more on the dollar. This is the best case.

Base Case (Orderly restructuring)

This is the base case – an orderly restructuring of Evergrande.

The company will be allowed to go “insolvent” and enter into an orderly winding up.

There will be some initial contagion in the market, especially among the closely linked suppliers/contracts and developers.

But over time, the banks/SOEs will likely step in to “bail out” the second order effects, by extending liquidity or supporting the next wave of impacted companies.

Business operations of Evergrande will be allowed to go on, and construction of existing projects will be completed.

In this scenario, bondholders will see more limited recovery. There is initial contagion, but over time the state will step in to prevent any further systemic risk. Homeowners should eventually get their completed houses.

Worst Case (China’s Lehman)

This is the worst case. This is basically China’s Lehman moment.

This scenario is disorderly default – Evergrande defaults, and the CCP does not step in to bail out second order effects.

There is widespread contagion across the property and banking sector.

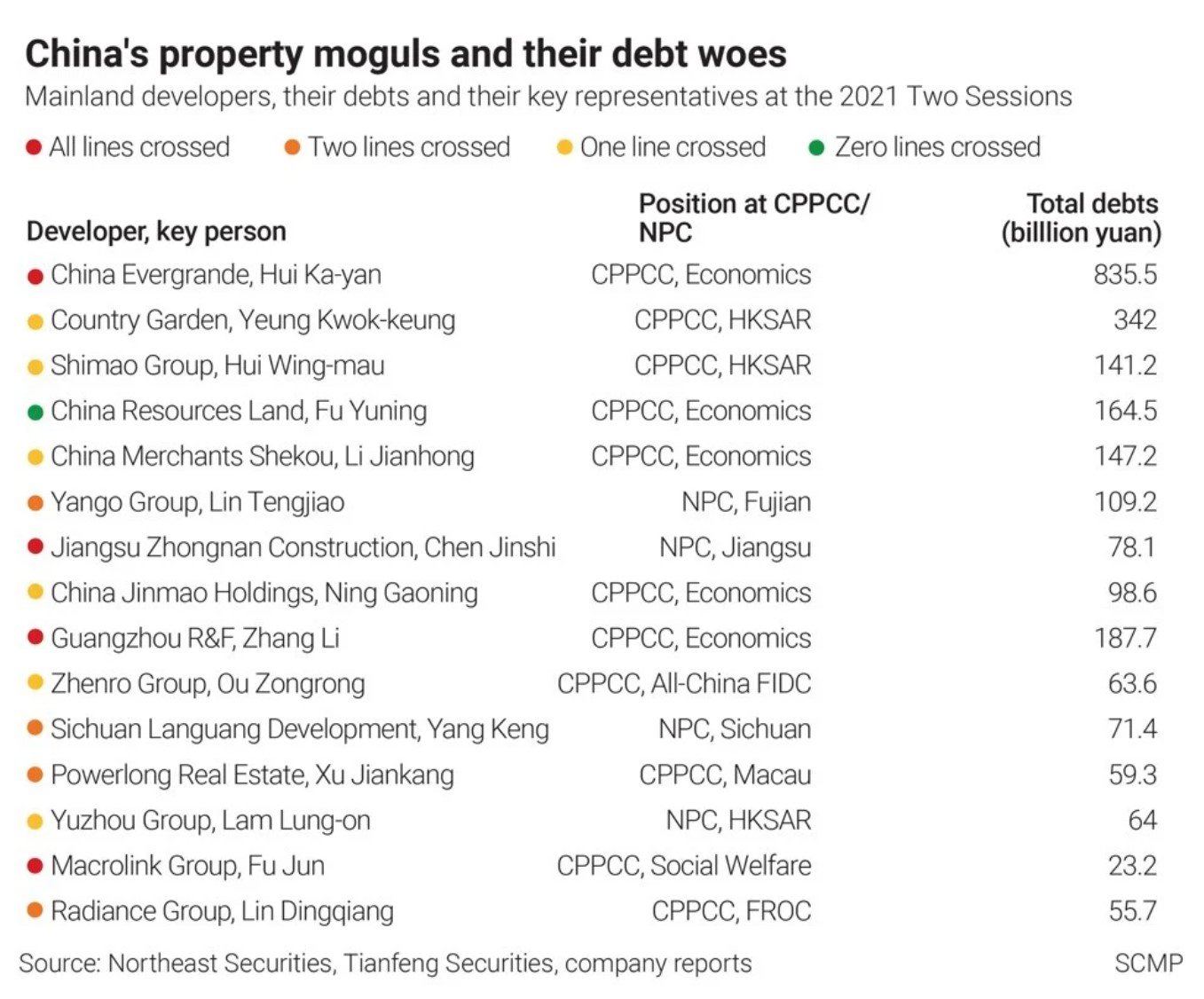

Real estate counts for 46% of all loans in China, and 18% of all China offshore bonds. If it blows up, it’s really going to blow up.

Liquidity will freeze up across the board, and we have a repeat of Lehman in China – a massively deflationary event across the board that can only be solved by massive state bailouts and money printing.

What starts with China will eventually spread to Asia and trigger a broader Asian crisis.

Is Chinese real estate going to collapse? Is there risk of contagion?

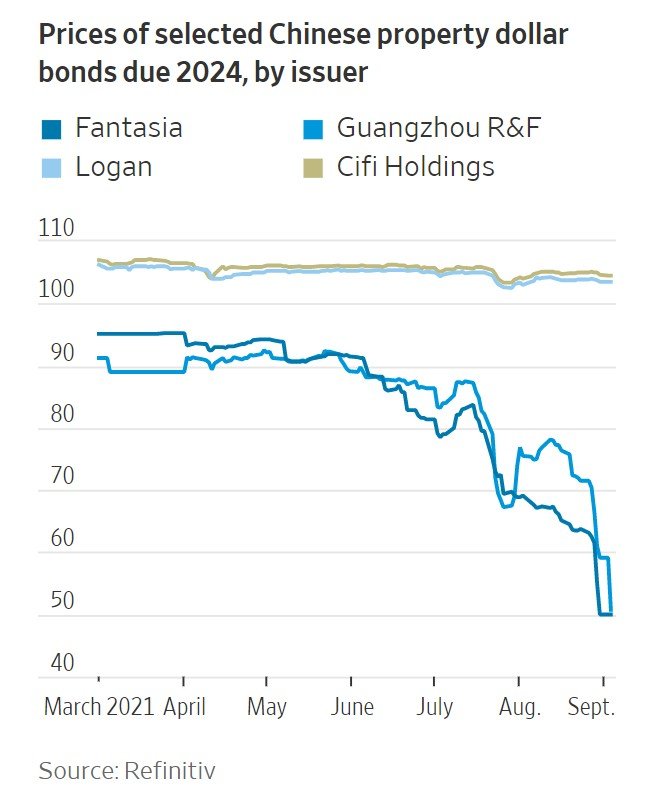

The market is already pricing in contagion risk for the weaker property developers, with both their share price and bonds collapsing:

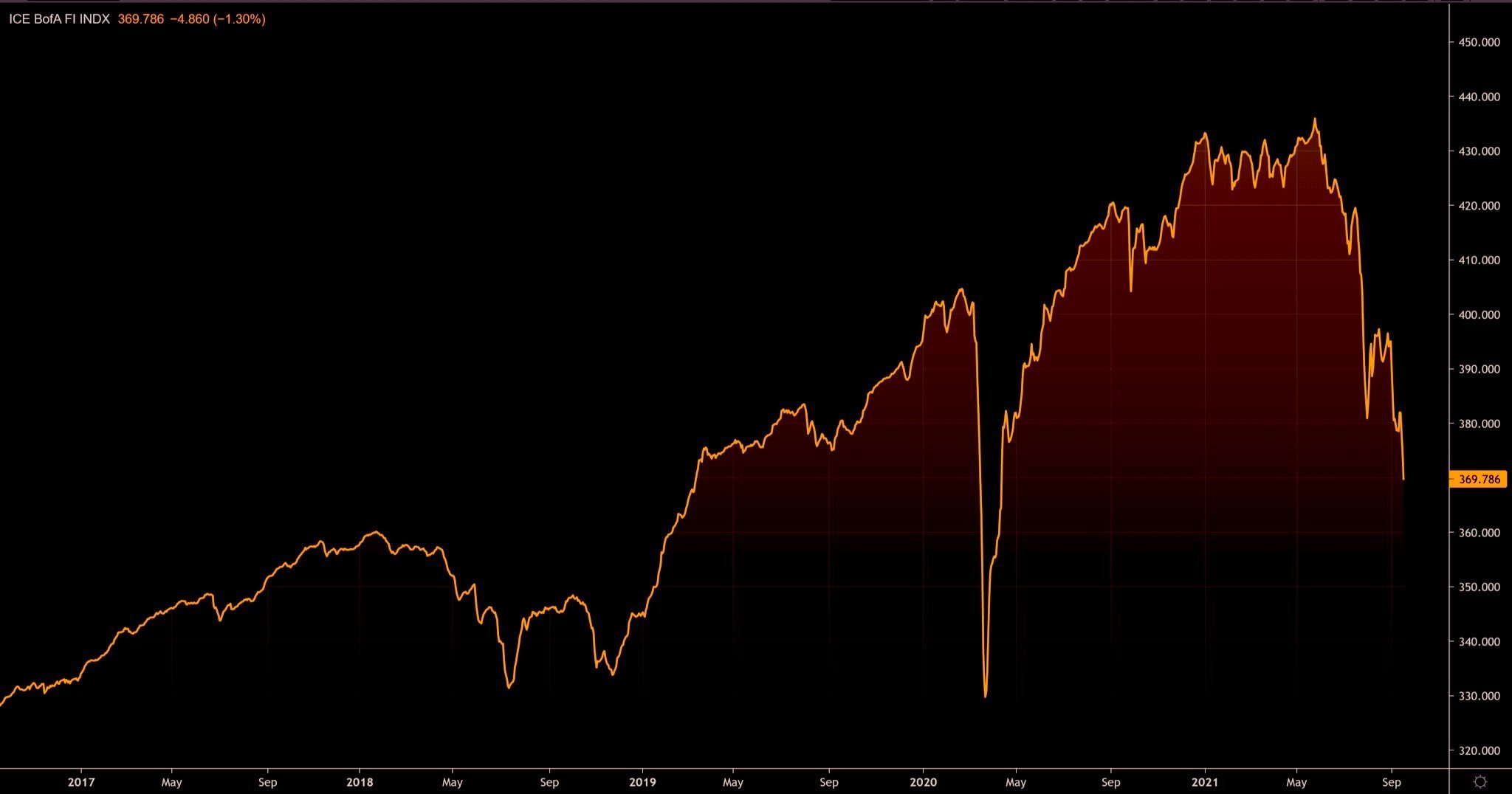

China’s High Yield debt too is collapsing, only 10% away from its March 2020 lows.

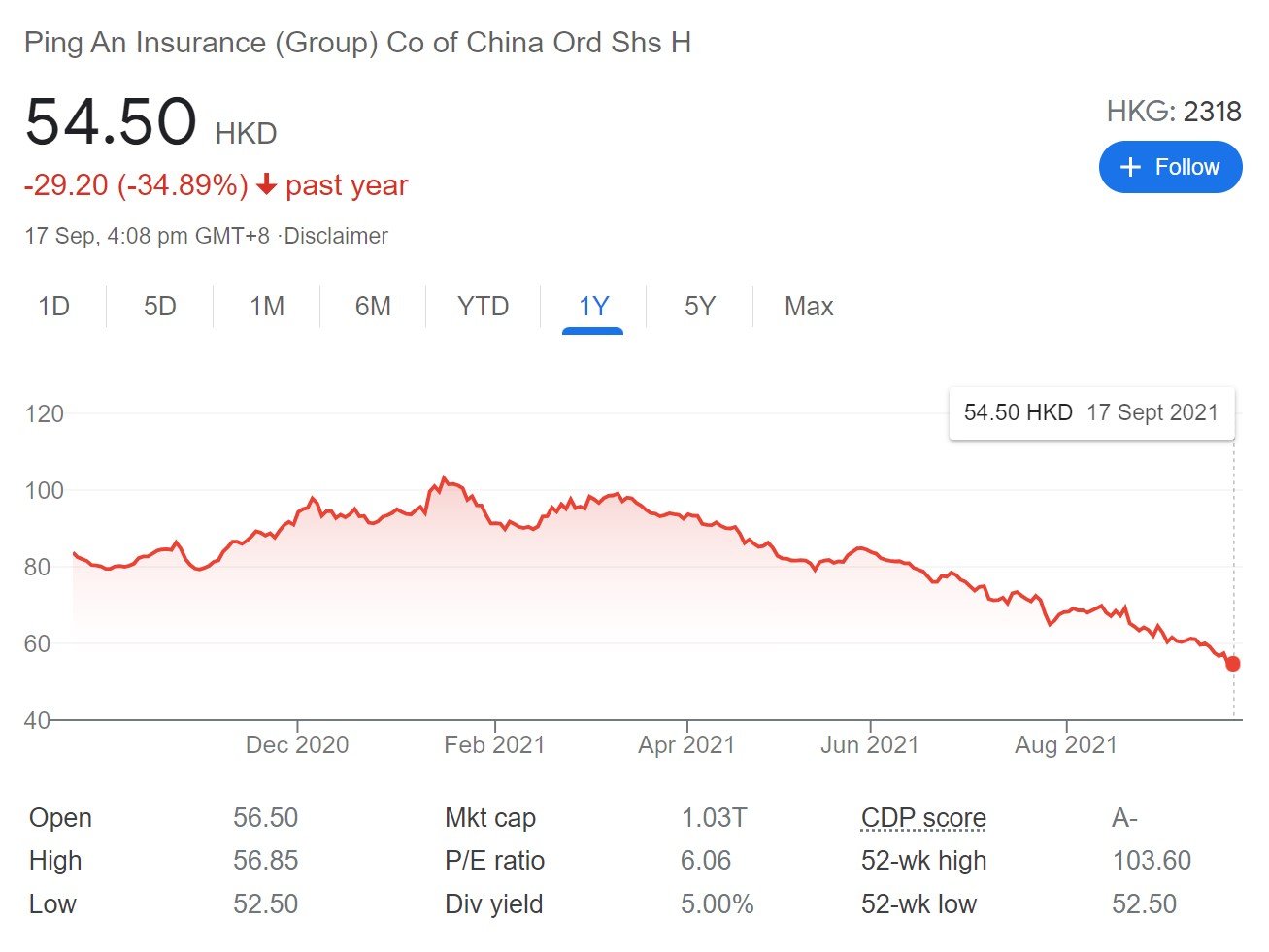

Even the banks / FIs are not spared. Here’s Ping An, the largest insurer in China:

So the market is already pricing in the tail risk. For now, it’s contained to China, but this can easily spread very fast.

Is this China’s Lehman moment?

I think the truth lies somewhere in between.

I don’t see the best case (CCP bailout) as likely.

CCP wants to send a signal to the market that excessive risk-taking and leverage will be punished. If they step in and bail out Evergrande, what signal does that send to the market?

Likewise, the worst case (Lehman) would also be a policy mistake.

Sure, you teach Evergrande a lesson, but then the whole market freezes up in a financial crisis, and you’re forced to do 10x more just to undo all the damage.

The base case seems the most probable here. Evergrande will be allowed to default, and a restructuring will take place. But the state will step in to prevent any broader contagion to the system.

But I can’t rule out a policy mistake. Lehman did happen in 2008 after all.

So it’s important to at least be aware of the tail risk here.

How long will this take to play out?

The underlying problem here is leverage.

There’s too much leverage in the system, concentrated in real estate.

And this will only end if leverage comes down across the board – Think asset sales from the weaker players to the stronger players. Bad players to be “restructured”. SOEs to pick up some assets to do their part.

And for those familiar with deleveraging – this takes time to play out.

You don’t deleverage an entire industry overnight.

Easily, 6 to 12 months or more.

Coincidentally, just in time for the 20th Party Congress, and Xi’s “relection” for a third term.

Long story short though – this will take some time. Expect more rot to come to light.

What are the second order effects?

A China slowdown is really bad news for commodities.

Iron Ore in particular, has collapsed since July:

Which in turn has impacted the miners. Here’s BHP Biliton, one of the largest Iron Ore miners in the world:

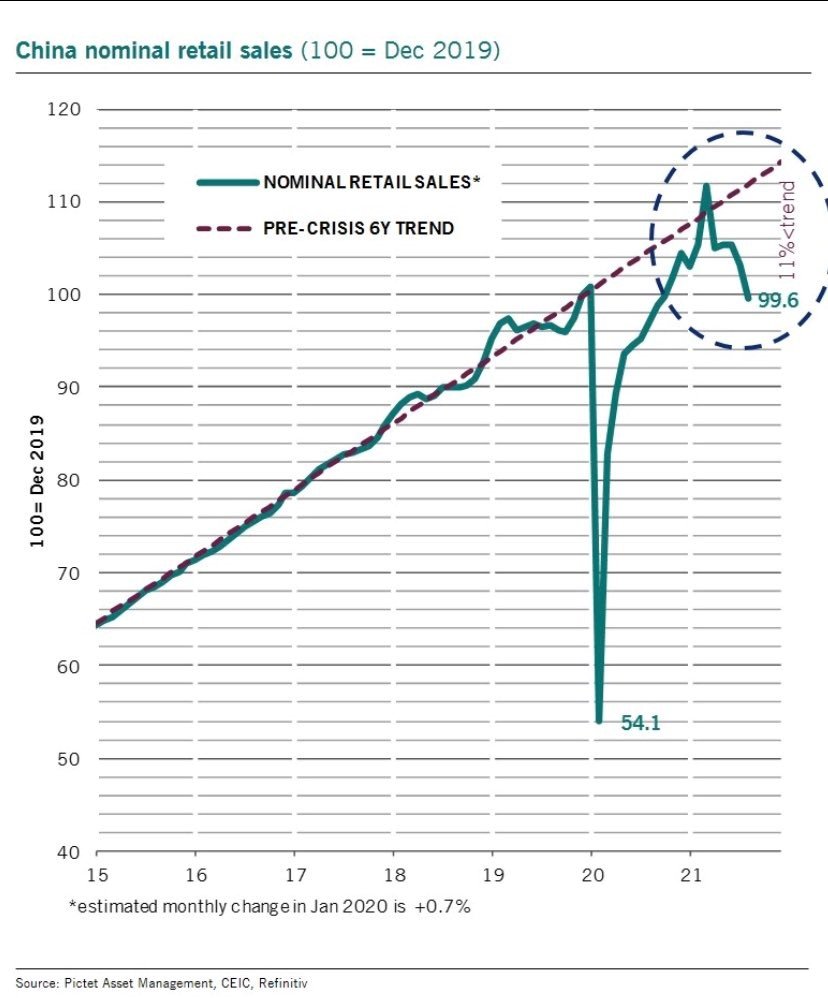

A lot of high frequency indicators in China are starting to roll over.

Still early days, but retail sales are pointing towards sluggish consumer spending.

Is the RMB going to depreciate massively?

Funnily enough, a Evergrande default would be a deflationary event. It will suck out liquidity from the system, which may actually strengthen the RMB.

The key here is the policy response. If there’s a flood of liquidity injected by CCP, then sure RMB will depreciate.

But remember how we talked about the key being deleveraging?

I don’t think we’ll see a Federal Reserve style money printing here. PBOC may keep monetary policy tight short term to finish up the deleveraging – which could keep RMB tight.

Is this Asian Financial Crisis Part II?

For now though, onshore funding stress is still very benign.

In China’s financial system – the state and the banks are basically the same thing.

So despite what is going on, I wouldn’t expect any of the big 4 banks (ICBC, CCB, ABC, BOC) to fail.

That’s not to say there wouldn’t be contagion. Just look above and it’s clear that the second order effects are already playing out, in the areas that are not state controlled.

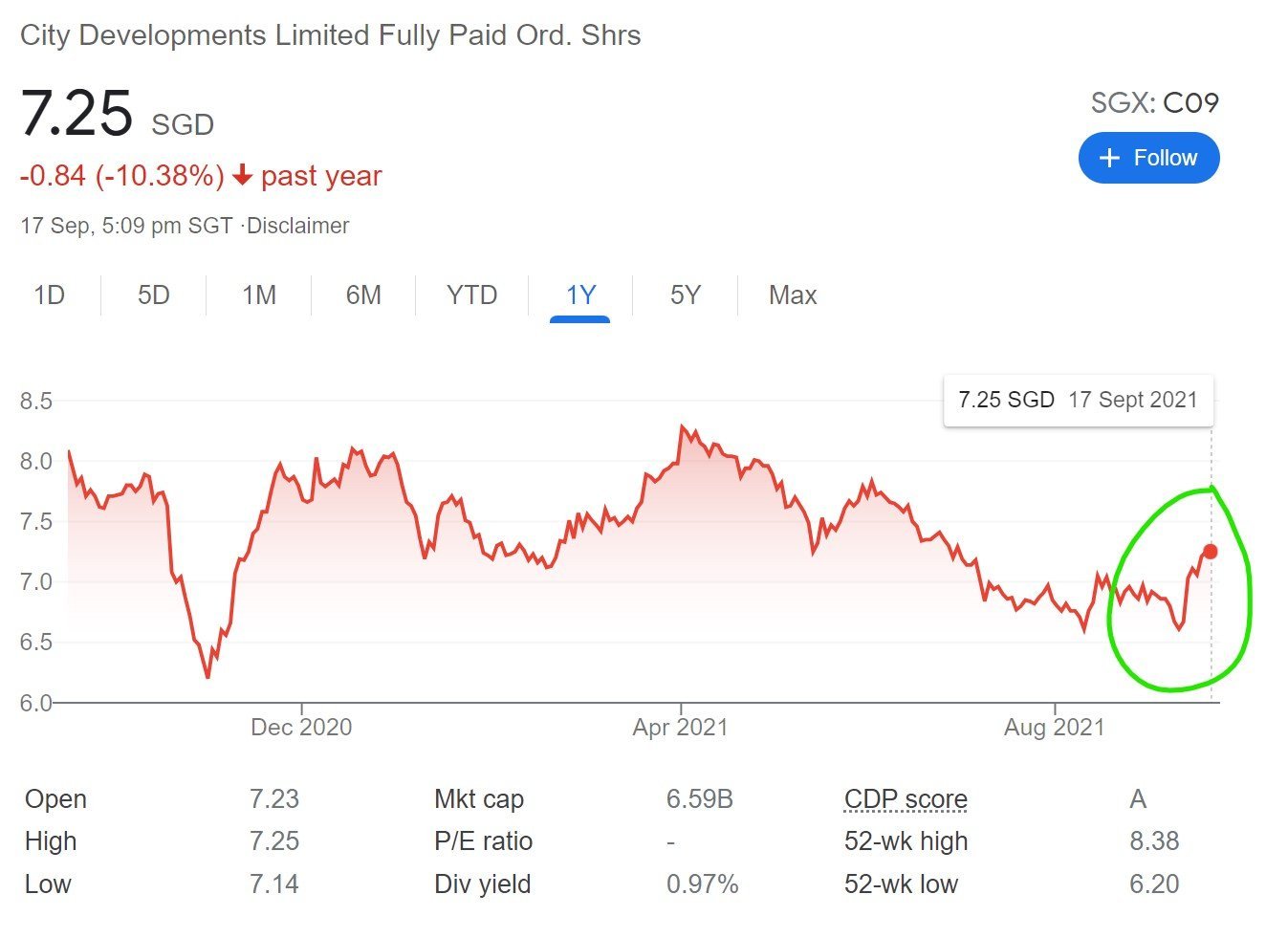

CDL sold Sincere for $1

The past week, CDL announced that they are selling off their China Sincere investment for $1.

We covered Sincere a while back – so check it out here for the full story.

Long story short, CDL bought overly indebted China Sincere (a real estate developer). A lot of directors disagreed and resigned – including the uncle of current CEO Sherman Kwek (son of Kwek Leng Beng). And now we find out why, because CDL effectively wrote off $1.78 billion in investments into Sincere this week, closing the chapter on that saga.

Anyway, given what a shitshow China real estate is in now, the market loved it, and CDL’s share price rallied nicely after it was announced.

Closing Thoughts: Timing of Evergrande a coincidence?

The fact that this is playing out together with a broader crackdown on Tech, Education, Personal data etc isn’t lost on me.

Xi needs to remain in power in the 20th Party Congress next year, and he needs to show that he can deliver.

By doing this, he’s trying to clean up the system and position for the next phase of growth, while also very conveniently weakening political opponents.

It’s a win-win right?

Short term though, I would expect uncertainty and volatility to stay high for a while. Construction activity and real estate price increases are going to stay muted for a while.

This isn’t as simple as CCP coming in to bail out the whole industry. Not happening.

But with every crisis comes opportunity. For investors prepared to take long term views on China, this could open up some amazing opportunities to accumulate at great prices. Probably as good as 2008, if not better.

For those who are keen – you can check out my China stock watch, together with my personal portfolio and how I am positioned on Patreon.

As always – love to hear what you think!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Check out our review on Tiger Brokers and MooMoo.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide on the best buying platforms here.

As always, this article is written on 18 Sep 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Join our Reddit community at r/SingaporeInvestments.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

any directly/indirectly linked SG stocks to look out for?

Almost any player with China real estate will experience second order effects. The key is how broad the contagion will be.

I think I know what the horse is thinking, so here’s one for you, have a good laugh and a great weekend:

https://www.youtube.com/watch?v=Bhf87Kn0ytE

Haha good one – had a nice laugh.

On a separate note, really ugly open for HSI today. 😉

Spot on again. Just wanted to add some thoughts as well. First being the overleveraged property sector weighing too heavily in the banking system. Per my understanding, this is because property is deemed by Chinese bankers to be the best collateral, hence the loan books tilting towards property. Now that China is bringing up property REITS, its a win-win situation. De-leverage the property sector from bank loanbook while allowing retail investors to invest and earn dividends while soaking up their excess liquidity. Second, the iron ore commodities rout sure is funny.. in the span of months, the hottest trends turns into the despised sector.. naturally the resulting effect of speculative activities overtaking the real use of the commodities, though the run up was partly due to the huge demand for steel now. Lastly, the CDL saga is really quite ridiculous.. the CEO, who has basically discredited himself and his father, had given his friend essentially free money (a gift?), lost 20+% of shareholder’s wealth accumulated over years and the share price rebounded based off this news. Surprised SGX hasn’t taken a look at this alarming governance lapse at CDL (basically multiple independent directors quit in protest but no one in the firm took a second thought and considered slowing down the process).. but my guess is there are connections behind the scenes and SGX can’t do much against our Singapore MNCs.

Very interesting comment. Some of my personal thoughts:

1. REITs is interesting. For now, China REITs are limited to infrastructure REITs, and the listing conditions are very tight. It will help in time, but for now it won’t come fast enough to help with the short term deleveraging.

2. Broadly similar views on CDL and destruction of shareholder value. Hindsight is 20/20, but this deal looked like a disaster last year, and it played out almost exactly as everyone predicted. Slow motion train wreck. But I guess the question is that now that the saga is over, is CDL a good pick up at this price?

Thanks. Agree, the ship is too big to steer for the moment. But the first step in the right direction is always commendable!

Yes.. agree. It was a train-wreck in the works even from the onset. I was thinking to myself why did CDL obtain such a terrific deal from Sincere last year, around the time when the acquisition deal terms was adjusted for CDL to acquire a bigger portion of Sincere for a lower price. Guess the only way for CDL to revitalize their share price is for their UK property REIT to work out..

Haha well they do have big exposure to Singapore resi which is really hot right now. Guess them overpaying for the en-blocs in 2018 turned out well after all. 😉