After my previous article on SBS Transit, I’ve been meaning to do a follow up on Comfort Delgro.

With the stock touching a low of $1.39 this week, I figured this would be a good time.

Lots to cover today, so let’s get right into it.

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

Basics: What does Comfort Delgro Do?

Comfort Delgro is an international transport conglomerate.

The main markets (and the services they provide) are:

- Singapore – 75% ownership of SBS Transit (Bus, MRT, LRT), 67% ownership of VICOM, Taxi, driving school

- Australia – Bus, Taxi, Patient Transport

- UK – Bus, Coach, Taxi, Private hire

- China – Taxi, Bus, Car rental, driving school

- Ireland – Coach

- Vietnam and Malaysia – Car leasing, Taxi

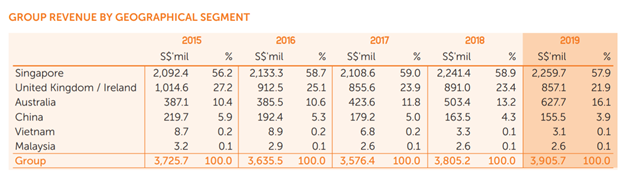

The revenue breakdown pre-COVID is set out above.

Essentially, Singapore, UK and Australia are the 3 main markets. The others – China, Vietnam and Malaysia are small to negligible.

Of course, the problem with looking at historical numbers for a stock like Comfort Delgro, is that COVID19 has been an absolute game changer for the industry.

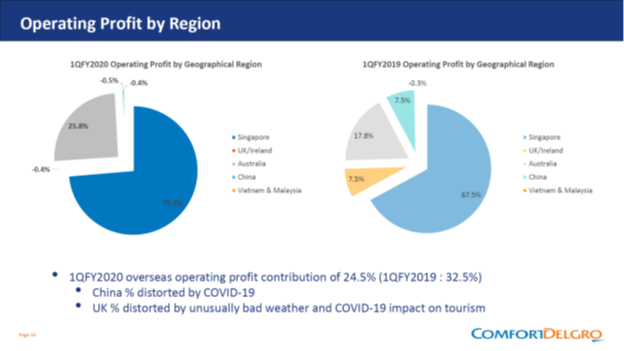

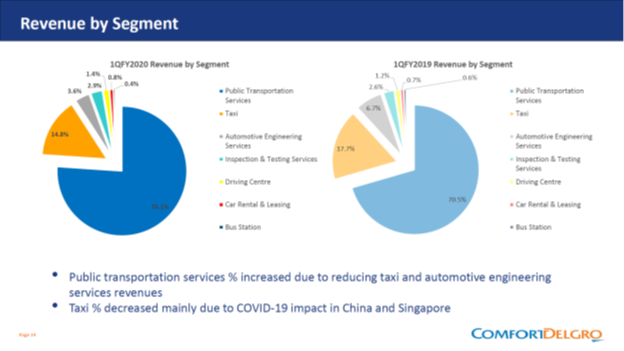

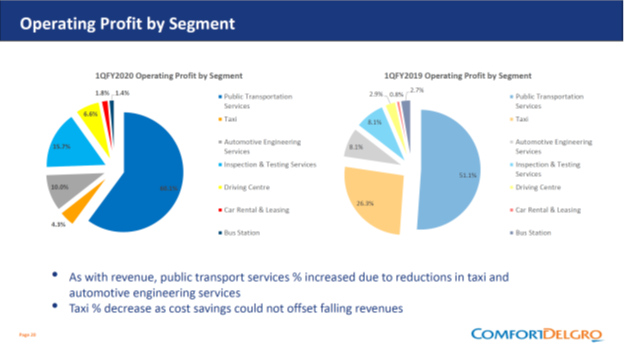

I’ve extracted some of the latest Q1 2020 breakdowns above, which you give you an idea of how things have changed post COVID.

The problem though, is that these are Q1 numbers, back when China was the worst hit country, and Singapore, UK and Australia were still looking good (yeah… remember then?).

The point here is – Q1 numbers are not going to be meaningful because the COVID19 situation has changed materially since. Likewise the Q2 numbers are not going to be of much use because Singapore was in lockdown then, so obviously things look bad.

What we really want to know, is what earnings will look like in 2021. And that’s really what the rest of this article will look at.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security.

Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

What do earnings look like?

Source: ShareInvestor WebPro

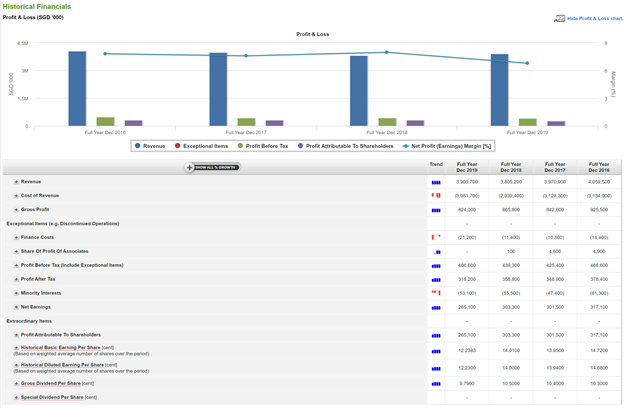

But first – historical earnings for the past 4 years are set out above, and they are remarkably stable.

This was pretty surprising because despite the stable earnings, the share price has only gone one way the past 5 years.

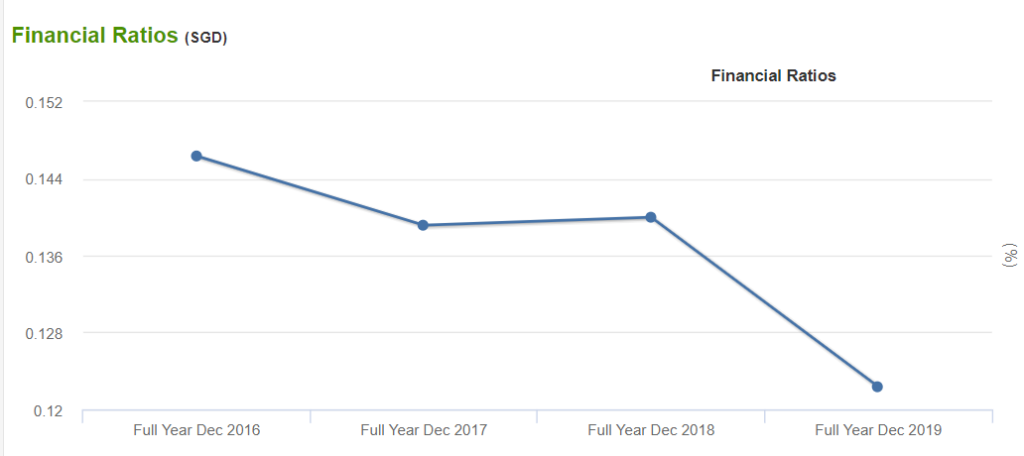

Source: ShareInvestor WebPro

Taking a look at Earnings Per Share (EPS) though, tells a different story as it’s on a cosistent decline.

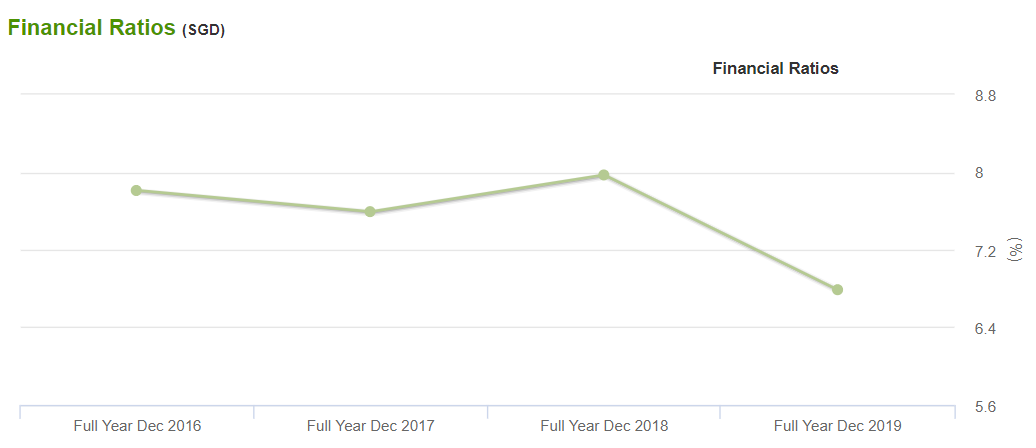

Margins don’t look good too, and they’ve been going down even pre-COVID. As it turns out, this is a pretty low margin business generally, well below 10%. Guess the manpower and fuel and equipment costs really add up, which is something the ride hailers like Uber and Grab have learnt.

Profit Warning

Comfort Delgro recently issued a profit warning for the 1H2020. I’ve extracted the details below, but all you need to know is that Comfort Delgro will be in a net loss for 1H2020 due to COVID19, but their liquidity position still looks very good with over $600 million cash on hand, and $700 million in loans they can draw down on.

So the earnings will be bad, but there is little insolvency risk here, at least short term.

The Board of Directors (the “Board”) of ComfortDelGro Corporation Limited (the “Company”) wishes to announce that based on the preliminary review of the draft financial results for the first half ending 30 June 2020 (“1HFY2020”), the Company is expected to report a net loss for 1HFY2020.

The expected net loss for 1HFY2020 is mainly attributable to: (a) the significant impact of COVID-19 on the Company’s operating regions as highlighted in the Company’s COVID-19 Business Update published on SGXNet on 22 May 2020; and (b) the possibility of impairment of the Company’s investments in certain local and overseas subsidiaries.

Notwithstanding the above, the overall financial position of the Company remains healthy.

As indicated in the Company’s COVID-19 Business Update of 22 May 2020, the unaudited cash and cash equivalents as at 31 March 2020 was $632.8 million and the available facilities in various currencies were approximately $704.7 million.

Impact of COVID19

Now the elephant in the room is COVID19. How will COVID19 impact Comfort Delgro’s business?

The saving grace for Comfort, is that they provide domestic transportation.

They provide buses, MRTs, taxi, coaches, basically stuff you use to get around your country. Contrast that to someone like SIA or SATS which relies on international travel.

Between the two, I think domestic transportation will recover first. Once countries can get COVID19 under control, domestic transportation can recover to a decent proportion of their pre-COVID levels.

International travel though, probably isn’t going to recover meaningfully until we have a vaccine or when most countries have cleared up COVID19.

Pre-COVID, the 2 big earnings drivers for Comfort Delgro were the Public Transportation and Taxi business. Taxi was hit very hard because of all the rental waivers granted during the lockdown, but most of these will be gradually phased out going forward. Likewise, public transport has taken a dive because of the circuit breakers, and most people are working from home these days.

So the short term impact is definitely bad. But remember how no one buys a stock for the earnings the next 3 months? And it’s the earnings in 18 months that matters?

So we all know 2020 is going to be a bad year, and what we want to know is about 2021. And in 2021, whether the Public Transport and Taxi earnings recover will largely depend on whether COVID19 comes under control.

If yes, and domestic travel recovers, earnings will pick up. If not, earnings are going to stay down.

Personally, I think that in 2021, domestic travel will start to recover meaningfully. Sure, it may not be at 100% of pre-COVID levels, but perhaps we may get up to 70% to 80% of pre-COVID levels.

At that kind of levels, it could be sufficient to sustain a meaningful recovery in Comfort Delgro’s earnings and share price.

Don’t forget that it’s fallen about 40% since COVID, and a recovery of even half that loss is a 30% gain from here.

Impact of Grab and Ride Hailing on the Taxi Business

The rise of Grab was bad news for Comfort Delgro’s taxi business, which we have seen in Comfort’s share price the past 5 years.

The interesting thing though, is that COVID19 has hit Grab very hard too. Sure, GrabFood has grown, and they’re trying to expand aggressively into the Fintech space, but there’s no denying Grab’s core revenue still comes from ride hailing, and the COVID shutdowns has hurt Grab badly.

They’ve been forced into layoffs and cost cutting exercises as a result.

What about post-COVID?

Do we see Grab aggressively slash pricing to compete with Comfort? I actually suspect not.

The difference between Ride Hailing and International Air Travel is that the latter is a lot more price elastic.

For airlines to get customers to fly again after this, they will likely need to slash pricing – which is what makes the entire airline business such a horrible investment (the price inelastic and lucrative business travel is largely gone – left with price conscious lesiure travellers).

With Ride Hailing, there’s actually increased demand now because people are reluctant to take MRT/Buses, and not everyone can afford their own car.

And with Grab being hit so badly, I don’t think Softbank is going to take too kindly to them embarking on another round of big customer acquisition via artificially subsidizing fares.

So in some ways, we may actually see Ridehailing and Taxis settle into an equilibrium after this, with no aggressive price cutting. This will be great for profits, but bad news for consumers.

But hey, we’re looking at this as investors right?

Valuations – Sum of Parts Analysis

It’s really tough to predict earnings for Comfort Delgro, so we’re just not going to bother.

Instead, we’re going to do a sum of parts analysis for Comfort Delgro.

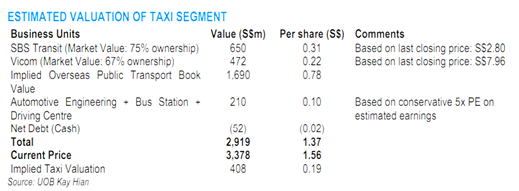

The 5 main business units are set out above (taken from a UOB report).

SBS and VICOM

SBS Transit and VICOM are public companies, so it’s easy to work out the value based on current share price.

The 75% and 67% ownership works out to $699m and $506m respectively.

Don’t forget that these are majority stakes, so we already leaving out the majority premium in these numbers.

Overseas Business

The overseas investments into Australia, UK and China are tough to value because again, we don’t know what future earnings look like. We’ll use a more simplistic analysis of investment cost.

Comfort Delgro made those investments at $1879.5m cost, so let’s assume a 20% impairment to that investment, and we get a valuation of $1503.6m.

Automotive + Bus Station + Driving Centre

For automotive + Bus Station + Driving Centre, we’ll use UOB’s conservative 5x historical PE, to get $210 million.

Net Debt

And finally, net debt position of $52 million.

Taxi Business

We’ve been fairly conservative with the numbers above.

But add that all together, and we get $2866, versus the current 3.06b market cap

What this means, is that based on the numbers above, the taxi business is valued at $196m.

Comfort Delgro is a taxi operator with 60% market share in Singapore, and a fleet of over 10,000 taxis.

At a valuation of $196m, you’re basically buying each taxi at about $19,600, which given car prices in Singapore, is below or close to replacement cost.

That looks like a bargain to me.

Problems with this analysis

The greatest risk with the analysis above, is the value of the overseas business. I just have no clarity on what the earnings are going to look like going forward.

If things take a turn for the worse, the 20% impairment we used above can easily look way too aggressive.

My gut feel, is that they should bounce back, because both UK and Australia have managed to get the COVID situation under control. Once that happens, domestic travel can start to resume, and the coach / bus businesses should bounce back.

As we’ve seen, once the domestic situation has been controlled, people are pretty willing to go out there and move around the country, so demand can bounce back pretty quick – as long as COVID is under control.

Of course, I would be careful about wishful thinking though. Second wave concerns in the fall are very real.

Dividend

Couple more points to run through to finish up the analysis, and then I’ll share my holistic view.

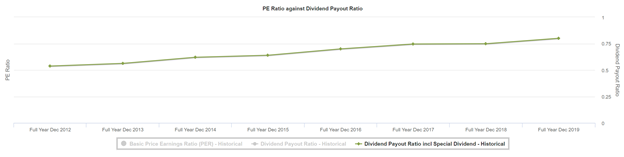

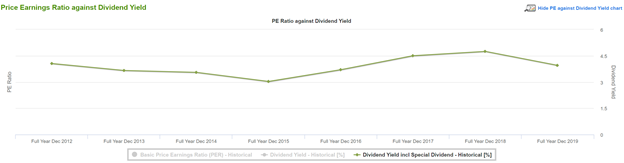

Source: ShareInvestor WebPro

Source: ShareInvestor WebPro

Historical dividend sits at about the 3.5% to 4.5% range. Payout ratio has been steadily increasing though, from the original 50% payout ratio in 2012 to about 75%.

This is not good, because a 75% payout ratio is way too high.

With the earnings impact from COVID19, there is little doubt the dividend will be cut going forward. So don’t buy this for the dividend.

Shareholders

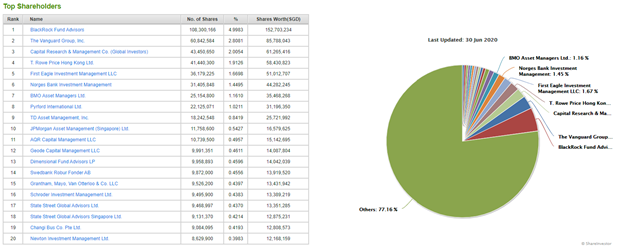

Source: ShareInvestor WebPro

The list of shareholders looks really strong, with big names like BlackRock, Vangaurd, T Rowe, JPAM, Norges Bank etc featuring on the list.

I really like this.

Buyback

Very little buyback activity to take note of.

The bulk of it was done during the March decline, which is just another reason why I’m not a fan of share buybacks – companies always end up buying their shares at too high a price.

Is Comfort Delgro a good investment?

And finally, the million dollar question: Is Comfort Delgro a good investment?

You can analyse stocks all you want, but if you don’t pull the trigger, you will never make any money.

So don’t make that mistake. Analyse, and then conclude.

Whether you are right or wrong – the market will provide the answer in time. If you are right, learn why you were right. If you were wrong, learn why you were wrong.

Margin of Safety

The simple answer here, is that I think there is a fairly decent margin of safety in Comfort Delgro right now.

At a price of 1.4, you’re basically buying:

- Majority stakes in VICOM and SBS Transit at market price

- The entire Overseas business at 80% of investment cost

- The automotive engineering, bus station and driving school at 5x historical earnings

- The Singapore taxi business with 60% market share at under $200 million, or slightly over $19,000 per taxi.

That looks pretty decent in my opinion.

BUT – Many risks remain

But there are many risks to this view.

The biggest one of course, is a second wave of COVID19.

If COVID19 comes back in the fall (and I actually suspect it will), then all bets are off. Earnings impact will depend on how severe the second wave is, and how drastic the measures taken by government to combat them are.

The other possibility is that COVID stays with us for a while, so that we never go back to pre-COVID levels of domestic activity, at least for a year or two. The longer this lasts, the greater the earnings impact.

Another possibility is that there is a price war, or government mandated levels of pricing. With this, even if demand recovers, profits may not recover.

All of these are possibilities that can make the current price look expensive.

The saving grace, is that Comfort Delgro has a strong liquidity position. If one of these scenarios play out, hopefully the weaker players will go bust, resulting in industry consolidation and stronger profits when everything eventually clears up.

Closing Thoughts: 3 Horse Rating

I do believe that eventually, COVID19 will come under control.

When it does, domestic travel will be the first to recover, way before international travel. And I see Comfort Delgro as a good way to bet on domestic travel.

It’s well diversified across all forms of transport – buses, coach, taxi, MRT etc. It’s diversified internationally, and it also has a strong liquidity position to get through to the other side.

Ultimately though, investing is about risk-reward.

Comfort Delgro is not without its risks.

I do think that short term, the share price can continue to slide.

But the more it slides, the bigger the margin of safety baked into the stock, and the bigger the returns in an eventual recovery.

And because no one knows where the bottom lies, nor how long COVID19 will persist in the short term, I think some averaging in makes sense here.

So I’ll give Comfort DelGro a 3 Horse rating. I like the stock, and I like the margin of safety. But short term, anything can happen really. There’s just too much uncertainty over COVID.

Do note that this article is written as at 24 July 2020, and will not be updated going forward. My latest thoughts, Stock Watch, and investment portfolio can be accessed on Patron.

Share your comments below!

Comfort DelGro – Financial Horse Rating

Financial Horse Rating Scale

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

This one should be safe, Govt will definitely wont allow it to fail. I will buy slowly, Thank for the well research article, God bless all of us safe and healthy.

Well, to be honest I dont think the government care that much about CDG as long as they don’t raise prices too much. 😉

hi where do u get the data of comfortdelgo taxi fleet size in singapore. Are you sure it have a fleet size or 18K a lot more than the data i have which i get it from AR.

Oh yes you are right – number should be closer to 10,000. I will update the article accordingly.

Hi, which one would you consider as better value? Comfort delgro or SBS transit?

Perhaps CDG. But I think the bigger issue here is how COVID plays out, and how to manage risk properly. If COVID never goes away for good, neither is going to perform well.

Hi FH,

With the recent announcement of losses, did you foresee a mass sell off, causing the price to drop significantly?

Thanks

Why though? They didn’t announce anything that came as a shock – everyone expected 1H2020 to be bad because of lockdowns. The key is what happens next. What is the govt stimulus, and how quick does COVID19 come under control.