Unless you’ve been living under a rock the past month, you’ve probably heard about the whole CPF saga. Long story short, CPF made some changes to CPF Retirement Sum withdrawals and a lot of people started getting really upset. I’ve always wanted to do an article to share my thoughts on the use of CPF as an investment tool, so I felt this was an opportune time.

What is CPF?

The basics of CPF should be relatively familiar to everyone. Seedly has a short guide that was quite well done, and I’ve extracted the key portions below.

Basically,

- An employee will contribute 20% of each month’s wage to their own CPF account.

- Employer will contribute an addition 17% of whatever their wage will be to their CPF account accordingly.

So: 20% from you + 17% from boss = 37% of total wage goes into CPF

- The CPF account will then be allocated to 3 different accounts.

- Ordinary Account (OA)

- Special Account (SA)

- Medisave Account (MA)

| Accounts | Usage | Interest Guaranteed | Allocation |

| Ordinary Account (OA) | Housing, Investments, Education, Approved Insurance | 2.5% | Age < 35: 23% Age 34-45: 21% Age 45-50: 19% Age 50-55: 15% |

| Special Account (SA) | Old Age/ Retirement-related financial products | 4% | Age < 35: 6% Age 34-45: 7% Age 45-50: 8% Age 50-55: 11.5% |

| Medisave Account (MA) | Hospitalisation expenses, Approved medical insurance | 4% | Age < 35: 8% Age 34-45: 9% Age 45-50: 10% Age 50-55: 10.5% |

Before you are 55, you can use:

- CPF OA – To purchase a house, to pay mortgage or to invest (35% of investible assets)

- CPF SA – You can’t use this

- Medisave – For hospitalisation bills

CPF Retirement Account

When you are 55, everything in your Ordinary Account (OA) and the Special Account (SA) will combine to form your Retirement Account (RA)

You will then be able to withdraw anything in your CPF Retirement Account, provided that you keep a minimum sum inside. There are 3 types of minimum sums, let’s go through them individually.

| CPF Payout Scheme (3 Tiers) | CPF Minimum Sum To Have (in 2017) | Remarks | |

| Basic Retirement Sum | $83,000 | If you own a property, you can withdraw the difference (CPF minus $83,000) | |

| Full Retirement Sum | $166,000 | If you have no property or Choose not to withdraw | |

| Enhanced Retirement Sum | $249,000 | Top-up into CPF Life |

Basic Retirement Sum – If you want to withdraw most of your CPF moneys, your best bet is the Basic Retirement Sum. This only applies if you have a property to secure a CPF property charge against. The way it works is that CPF will place a property change on your property, and if / when you sell your property, you have to use the proceeds from the sale to top up the CPF Retirement Account to the FRS amount + interest accrued.

If you do this property charge, you only need to keep the Basic Retirement Sum (BRS) in your CPF Retirement account, and you can withdraw everything else in cash. The BRS changes every year to keep up with inflation:

Basic Retirement Sum |

|

| Age 55 in 2016 | $80,500 |

| Age 55 in 2017 | $83,000 |

| Age 55 in 2018 | $85,500 |

| Age 55 in 2019 | $88,000 |

| Age 55 in 2020 | $90,500 |

Full Retirement Sum – If you don’t have a property to secure again, or just don’t want to do a property charge, you’ll need to keep your Full Retirement Sum (FRS) in the CPF Retirement Account, and everything in excess can be withdrawn in cash. The FRS numbers are set out below.

| 55th birthday on or after | Full Retirement Sum |

| 1 January 2017 | $166,000 |

| 1 January 2018 | $171,000 |

| 1 January 2019 | $176,000 |

| 1 January 2020 | $181,000 |

Enhanced Retirement Sum –Alternatively if you want to keep more money in the CPF Retirement Account to buy a better CPF LIFE plan, you’re free to do so.

Note that even if you are unable to meet the BRS or FRS, you’ll still be able to withdraw up to S$5000. Government is good that way.

CPF Life

CPF Life is a bit more complicated, and I spent a fair bit of time trying to understand it myself. I found that the easiest way to conceptualise this, is to imagine that you are buying an annuity plan with your CPF moneys at age 55. I googled annuity, and this is the definition they gave me:

- “a fixed sum of money paid to someone each year, typically for the rest of their life.

“he left her an annuity of £1,000 in his will”

-

a form of insurance or investment entitling the investor to a series of annual sums.“loans secured on an older person’s home which are used to purchase a life annuity:

Let’s go into the details of CPF Life:

Pick a plan – Depending on how much you chose to retain in your CPF Retirement accounts, you get to pick between 3 different CPF Life plans:

- Standard plan is the default plan,

- Basic plan gives you less monthly payouts but a higher residual sum that you can leave to your children,

- Escalating plan has monthly payouts that start low but increase gradually over time.

| | Standard Plan

(default plan) |

Basic Plan |

Escalating Plan |

| Basic Retirement Sum

(BRS) |

$730 – $790 | $690 – $720 | $570 – $620 (initial amount) Payouts increase by 2% every year |

| Full Retirement Sum (FRS) $176,000 |

$1,350 – $1,450 | $1,280 – $1,320 | $1,040 – $1,140 (initial amount) Payouts increase by 2% every year |

| Enhanced Retirement Sum (ERS) $264,000 |

$1,960 – $2,110 | $1,860 – $1,920 | $1,510 – $1,660 (initial amount) Payouts increase by 2% every year |

Note: These monthly payouts are estimates and computed as of 2019. Payouts may also be adjusted to account for long-term changes in interest rates or life expectancy. Such adjustments (if any) are expected to be small and gradual.

The CPF LIFE Estimator can help you to estimate your monthly LIFE payout and the bequest for the different plans depending on your Retirement Account savings.

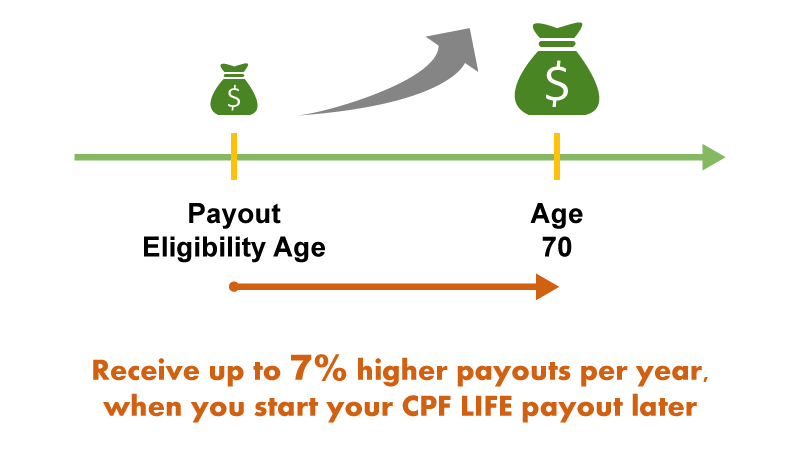

Pick when to start payout – The earliest you can start CPF payouts is when you’re 65. You can delay receiving payouts up to age 70, and for each year you delay receiving a payout, the monthly payout goes up by 7%.

Determining your monthly payout – How much you get in your monthly payout, depends on 2 main factors:

- Which plan you bought, and how much you spent to buy it (this part is within your control)

- Your gender, age, CPF interest rates and mortality rates (this part is beyond your control, and is used by an independent actuarial consultant to generate the payout numbers)

Because of this, the actual monthly payout will vary from individual to individual, and depends on the year you start the plan, and also depends on your personal circumstances. CPF has a calculator on their website that can be used to give you some indication of the numbers.

But the fact remains that if you are 30 years old now, it’s going to be hard to predict what the payouts will look like when you are 65.

What happens when you die – CPF Life works like any other annuity. The payouts will continue for as long as you live. So the longer you live, the more you “make” from this annuity. The shorter you live, the less you “make”.

It is important to note that the amount you get back from CPF Life, will NEVER be lower than the initial principal (but not including interest) you put in at age 55 when you chose which plan to buy.

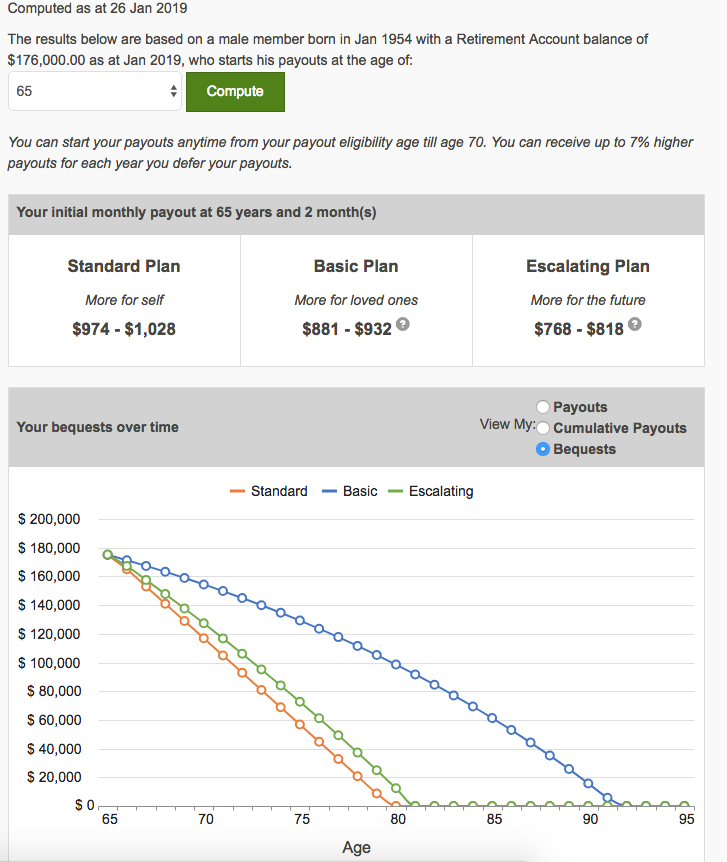

Let’s use a simple example here. Imagine Xiao Ming picked the Standard Plan on a Full Retirement Sum when he was 55. He put in S$176,000 at 55, and this generated interest at a nice 4 – 5% a year. At 65, he starts receiving about $974 – $1,028 a month. Unfortunately, he passes away 10 months after his 65 birthday, so the total amount he withdrew from CPF Life was only about S$10,280.

The amount that will be left to his loved ones, will be the original amount at 55, less the payouts he received: S$176,000 – S$10,280.

Of course, the next question here is: what happens to the rest of the interest generated on the S$176,000 from 55 until the day he passed away? As it turns out, because the money was used to purchase an annuity (CPF Life), the interest generated went back into the annuity pot, and is being used to fund the annuity scheme. You can think of it as an insurance product. With health insurance, when you’re healthy, you don’t claim under the policy, and all your premiums are paid into a pot, and the insurer uses the money in the pot to pay to those who fall sick. With CPF Life, everybody pays into a pot, and CPF uses the money in the pot to make payouts to members. The longer you live, the more payouts you get.

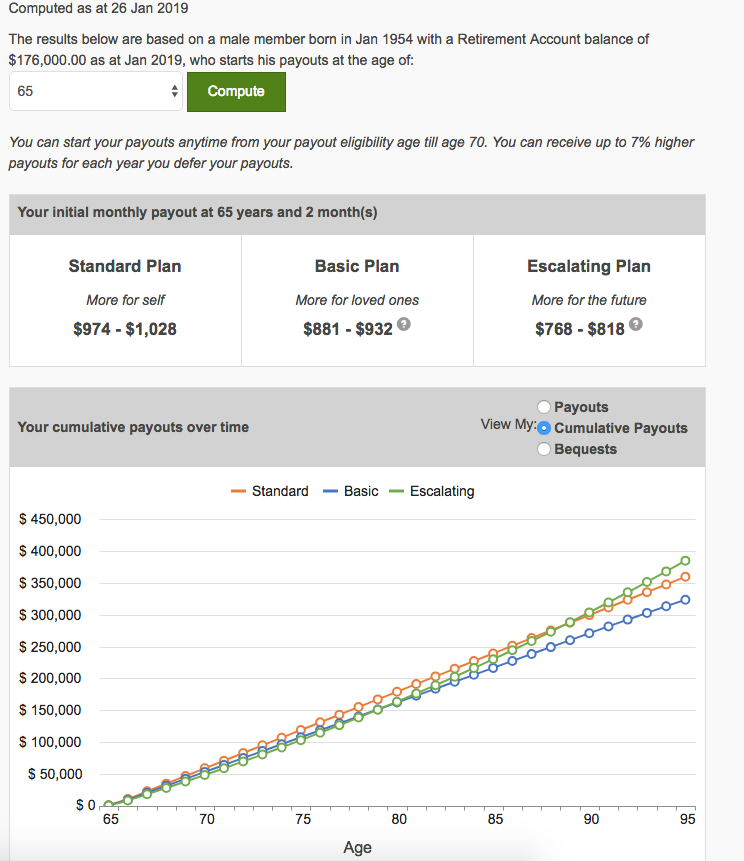

There are some charts below to illustrate this point. Do note that because the residual amount that will be left to your loved ones is pegged to your principal amount and doesn’t include the interest, after a certain age, the initial principal is fully depleted by the monthly payouts. To go back to the Xiao Ming example, after about 15 years of S$1028 monthly payments (when he is 80 years old, assuming he starts payments at 65), he would have fully “used up” his original S$176,000, so there would not be any bequest left to his loved ones when he passes away. Of course, the monthly payments will still continue at that stage, because that’s the whole point of the annuity.

If you took nothing away from the discussion above, you just need to know that the longer you live, the better CPF Life is. So eat healthily and exercise guys… government is right when they ask us to cut down on sugar.

What is the misunderstanding?

Frankly speaking, the entire mixup with CPF recently was quite silly. It arose in relation to the CPF Retirement Sum Scheme (which is the earlier version of CPF Life), but the position will apply equally to CPF Life. I’ve summarised the before and after positions below:

- Before: If you didn’t notify CPF, the CPF Life (or CPF Retirement Sum Scheme) payouts would never start. You had to notify CPF (via a form or a website) of the age you want payouts to start, before it would start. As you can see, that was a pretty silly plan.

- After: The change that CPF made, was to set the default payout for CPF Life at 70, so even if you did absolutely nothing, the payouts would start at 70. If you want it to start earlier, you just need to notify them.

In the grand scheme of things, this change was actually a good one, although I have to admit, the way it was communicated could have been improved.

CPF Investment Strategies

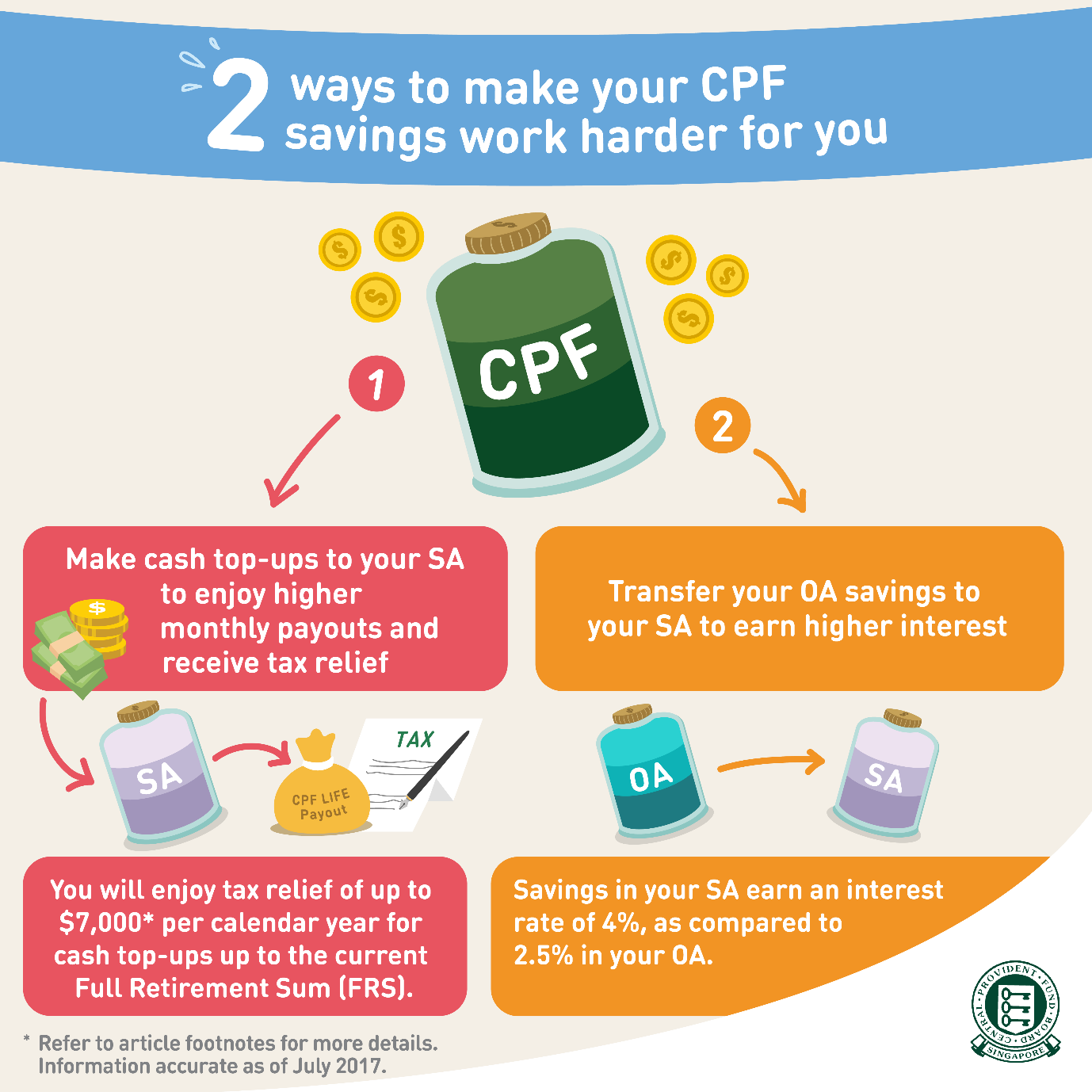

There are 2 strategies to maximise CPF:

- Top up your CPF SA in cash, and

- Transfer your CPF OA into your CPF SA

Topping up CPF-SA with Cash

A lot of financial bloggers out there recommend topping up your CPF-SA with cash early on in your life to enjoy the higher returns. There’s no doubt that this is a viable strategy, but I don’t agree that this is the be all and end all investment strategy that these guys are touting. There are a couple of downside risks that we should be aware of:

Downsides

- Liquidity – I talk a lot about liquidity on this site. Liquidity to me, is the ability to cash out on an investment any time I want to. Liquidity is important to me as an investor because life is unpredictable. One day you’re at the top of the world in your financial career, the next day you’re unemployed in the midst of a financial crisis, and your loved ones contract a serious illness. It’s an extreme example, but it just goes to illustrate the fact that you never really know when you may need to access your funds.A topup into CPF-SA is irreversible. Before you do a cash topup, you really need to be absolutely sure that you will not need the cash in the short term, because the next time you can access that cash, is when you’re 55.

- Changes to CPF Life or Full Retirement Sum – I’ve set out the long term Full Retirement Sums below. As you can see, it’s increased from S$80,000 in 2003 to S$171,000 in 2018 (to be fair, I can totally understand why it’s gone up so much, because the cost of living in Singapore has gone up tremendously in that time).But the fact remains, if you’re a 30 year old Singaporean topping up your CPF SA, you’ll only be able to withdraw it in 25 years, which is 2044. What the FRS sum will be in 2044, is anyone’s guess.To put things in perspective here, CPF Life was first introduced in 2009. If we take a longer term perspective of 20 to 30 years, there remains the possibility that a successor to CPF Life, or a CPF Life version 2, could come into play.

| 55th birthday on or after | Full Retirement Sum |

| 1 July 2003 | $80,000 |

| 1 July 2004 | $84,500 |

| 1 July 2005 | $90,000 |

| 1 July 2006 | $94,600 |

| 1 July 2007 | $99,600 |

| 1 July 2008 | $106,000 |

| 1 July 2009 | $117,000 |

| 1 July 2010 | $123,000 |

| 1 July 2011 | $131,000 |

| 1 July 2012 | $139,000 |

| 1 July 2013 | $148,000 |

| 1 July 2014 | $155,000 |

| 1 July 2015 | $161,000 |

| 1 January 2017 | $166,000 |

| 1 January 2018 | $171,000 |

| 1 January 2019 | $176,000 |

| 1 January 2020 | $181,000 |

- Changes to the Interest Rate – I think this risk is incredibly small, but I’ll just include it for discussion’s sake. The risk here is that if there is a prolonged slowdown in the global economy that negatively impacts returns on risk assets (ie. something similar to the 1930s or the 1970s), the interest rates paid on CPF-SA may be reduced accordingly from the current 4% floor. In such a situation, there may not be a way to withdraw the CPF-SA moneys even if the returns decrease.That said, I do think the chances of this happening are slim.

Benefits

- Higher interest rates – A lot of financial bloggers advocate topping up CPF-SA early on in your life, because of the higher returns of 4% on the CPF-SA. Unfortunately the situation is a lot more nuanced than that, because of the liquidity point mentioned above.Let’s put it this way. If you’re 30 years old, you’re basically locking up cash for 25 years, for a 4% return a year. With a 25 year investing timeframe, you could probably just invest that money in the S&P500 or a global stock index and you’ll probably get 6-7% returns, which is the long term average return of global equities.If you’re in your mid 40s, it’s basically a 10 year lockup period, in which case CPF-SA topup may become quite attractive, because a 4% annual compounded returns, completely risk free may potentially trump equity returns over the next 10 years, given where we are in the debt cycle, and the current stock market valuations. Don’t forget we’re nearing the end of a 10 year short term debt cycle, so equity returns over the next 5 to 10 years may be low from this point. Long story short, how attractive the 4% returns is, depends a lot on your age, and on the stage of the current debt cycle.

- Risk and fuss Free – What is good about CPF-SA though, is that it is risk free and fuss free. If you don’t know anything about investing, and have no plans on ever learning anything, you probably shouldn’t be DIY investing your retirement funds. What CPF-SA does, it guarantee you 4% returns every year, with minimal input required. That’s peace of mind, and it frees up a lot of time to focus on the more important things in life, like your career, your family or your interests. If you want a place to just park your money risk free and achieve moderate returns, CPF-SA is a very good choice.

- Tax Savings – Any cash topups into CPF-SA will enjoy tax exemption, up to S$14,000 per year. If your income is high, CPF-SA topup is a great way to reduce your tax bill, and don’t forget that a 20% savings on tax, is equivalent to about 3 years’ worth of investments at a 6% return. Don’t forget that you can also utilise the Supplementary Retirement Scheme for tax savings. I wrote on this previously so do check it out for more information, but long story short, use SRS for tax savings if you’re young, use CPF topups for tax savings if you’re older (near 55), and use both SRS and CPF topups if your income is very high. Of course, it does get a bit tricky because you can only top up CPF-SA up to your FRS amount, so if you were a high income earner when you were young you could easily have hit this at an early age, so you do really need to think about your personal situation and how best to make CPF work for you.

Just to very clear, I’m not saying that topping up CPF-SA in cash is a bad thing. I think it’s a great idea for many types of investors. For example, if you don’t know the difference between a stock and a bond and you’re picking between CPF-SA topups or a professionally managed ILP with high fees, I think the CPF-SA is a better choice. Or if you’re in your mid 40s and haven’t hit FRS, CPF top ups are great because it’s completely risk free, and you get 4% returns without the volatility that comes with equity markets. If fact, even if you’re a great investor who’s going to become the next Stan Drunkenmiller, there’s still a lot of merit in CPF-SA functioning as a portfolio diversification, just in case one of your plays on the stock market goes completely wrong.

But of course, just like any other investments, it does come with certain downsides, and I do think its important to take note of the liquidity issues, the risk of changes to the scheme, the moderate returns etc, before making any decisions.

Topping up CPF-SA with CPF OA

The considerations to transfer funds from CPF-OA to CPF-SA are pretty much the same as the above, only without the tax savings point, so I won’t touch too much on this.

How do I use CPF?

This post got a lot longer than I expected. But I’ll just round off with some thoughts on how I use CPF for myself personally. It may or may not work for you, but at least this gives you an alternative to consider.

- CPF OA – I treat my CPF OA as a medium term bond. It yields a very nice 2.5% risk free return, and I can withdraw it any time to buy a house, or to pay the mortgage or to invest in a downturn (35% of investible assets can be used to buy stocks). I deliberately left moneys in CPF-OA when purchasing a property because it’s 2.5% risk free which is higher than anything I can get outside, and I can always use it to make mortgage repayments anytime I want. Otherwise, when the next financial crisis comes around, I can just max out my CPFIS picking up bank stocks on the cheap.

- CPF SA – I ignore my CPF SA. To me, it’s money I can’t touch until I’m 55 anyway, so I don’t see much point factoring it into my personal planning now. When I’m in my 40s and I have more clarity on what the FRS sum will be when I hit 55, perhaps I’ll start taking it into account.

- SRS – I top up SRS to the maximum each year, to enjoy the tax savings. I use SRS for my retirement planning, because I enjoy making my own investment decisions, and I like that SRS give me the option to withdraw the moneys anytime, subject to payment of a 5% penalty + prevailing income tax. SRS is my preferred tax planning method because I am young. Of course, when I am in my mid 40s or 50s, CPF topups may prove superior, assuming nothing changes between now and then.

Closing Thoughts

Whether you like it or hate it, CPF is part and parcel of every Singaporean’s life, no different from NS.

And like NS, complaining about it is great fun, but it doesn’t really change anything. To me, CPF is just an investment tool. And like any other investment tool, it has its own rules. Once you take the time to understand the rules and how it works, you can figure out how to make the tool work for you, rather than the other way around.

And just for the avoidance of doubt, I am a huge supporter of CPF. I think the fact that any Singaporean working in Singapore automatically has a 17% boost to his income, and is automatically enrolled on a well thought out retirement plan that generates decent returns, puts us well ahead of many other developed nations in this regard. Sure, it isn’t perfect, but nothing in this world is.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy!

[mc4wp_form id=”173″]

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

You can actually use your CPF SA to invest if its more than 40k

That’s a good point. Thanks for raising it. I guess this does negate the “low returns” point somewhat, since CPF SA funds can be used to invest in shares. Although just to get the CPF SA up to 40k will take at least a few years of work, so the op cost there will remain.

Cheers.

Hi,

1. The January 2019 saga was about CPF members under the Retirement Sum Scheme, it wasn’t about CPF Life.

2. When we are 55, SA monies and then OA monies are transferred to the RA, to make up the Full Retirement Sum. So there are people who have monies remaining in SA and OA even after 55. They are the ones with high CPF balances. There’s a nice table that summarises how much we can take out at 55 in a lumpsum at this url https://www.cpf.gov.sg/Members/Schemes/schemes/retirement/withdrawals-of-cpf-savings-from-55

3. The misunderstanding is –

• Before, prior to 2018: If you didn’t notify CPF, the Retirement Sum Scheme payouts would never start. You had to notify CPF (via a form or a website) that you wish payouts to start. There were CPF members who didn’t start their payouts even when they were 70 and older.

• From Jan 2019: The change that CPF made, was to set the latest start date for Retirement Sum Scheme payout as 70, so even if you did absolutely nothing, the payouts would start at 70. If you want it to start earlier, you just need to notify them. It can be at any age, eg when you are 67 years 7 months old.

For CPF LIFE, we select our plan only when we wish to start the annuity payout.

Thanks for the clarifications, appreciated. I’ve updated the post accordingly.

Cheers.

i hope CPF next change was to include optional choice for us to en-roll back to Retirement Sum Scheme.

Yes, that would be a very nice touch, and give members a lot more flexibility.

Hi FH,

This 65-to-70 payout start also applies to CPF Life. If someone ignores it, he/she will eventually be placed on the Standard Plan by default with payout from 70.

This means that between 55 to the selection & start of a CPF Life plan, we get to “keep” the RA interest generated, and it forms part of the principal sum for buying the CPF Life annuity plan.

Hence the marketing spiel that every year of delay will result in up to 7% higher payouts.

Only the interests generated when the CPF Life plan is activated will be transferred to the pooled fund.

PS: CPF merely wanted to normalise the payout start of the Retirement Sum Scheme to be the same as that for CPF Life scheme.

PPS: CPF is a good example of behavioural finance implementation & the “Nudge” tactic talked about by Richard Thaler.

Ahh so my original understanding was correct. Thanks Sinkie. 🙂

Haha, to be honest, I fully understand what CPFB was trying to do, but as you rightly pointed out, it was quite a good example of behavioural psychology at work here.

Hi,

This is mentioned in the writeup:

“Of course, the next question here is: what happens to the rest of the interest generated on the S$176,000 from 55 until the day he passed away? As it turns out, because the money was used to purchase an annuity (CPF Life), the interest generated went back into the annuity pot, and is being used to fund the annuity scheme.”

If the above is true, it will be pointless for one to go for FRS or ERS, since not many can live beyond 80.

Opting in for BRS, to withdraw the rest of the amount to do our own investment will be a wiser choice.

Hi there!

Yes that’s one way to look at it. The other way is that if you for some reason live to 100 plus, the FRS/ERS option would turn out to be a fantastic one.

It’s a bit of a glass half full / half empty kind of analysis. 🙂

Cheers.

“Basic Retirement Sum – If you want to withdraw most of your CPF moneys, your best bet is the Basic Retirement Sum. This only applies if you have a property to secure a CPF property charge against. The way it works is that CPF will place a property change on your property, and if / when you sell your property, you have to use the proceeds from the sale to top up the CPF Retirement Account to the FRS amount + interest accrued.”

dont fully understand this yet. so if you dont sell the ptty? you still get to keep the initial withdrawal? in this case, most people should pledge in order to get a bigger sum at the initial. highly unlikely anyone would be selling their ptty around the 70-80 age?

Yes that’s right, if you don’t sell your property you get to keep the withdrawal. It’s sort of a way to ensure that you don’t sell your house and spend all your money, only to have nothing left for your retirement. 🙂

I used to think the 17% employer contribution was great too until I worked in the US, Europe and China. Turns out because of the cap of employers contributions on $6K salary, for higher earners, this max contribution of $1020/month is actually very low compared to schemes in other countries. Contributions by companies there are typically a lower percentage of say 12% but with no cap or a very high cap. So if one earns above S$8500 a month, employers contribution will be higher, in some cases, much higher. Over decades of working life, the difference is very great and this is one big reason why we have a problem with retirement adequacy in Singapore. The cap hasn’t been raised in eons to keep up with inflation unlike the Minimum Sum. This problem is compounded by allowing and indeed, perhaps even encouraging overuse of CPF for housing instead of for retirement.

That’s a really interesting point. I just googled the average salary in Singapore, and turns out it is S$67,152. For someone on the average salary, the problem you just mentioned would not really be an issue. I guess in a way, CPF helps the lower – average income, and for the higher income, the carrot would be the lower personal tax rate.

Hi FH, I got interested in this article because I personally did a great deal of research (and calculations) on CPF SA. I think this was one question your article didn’t really address, but could be of interest:

[[Should you top up your SA with OA?]]

Benefit:

– Enjoy higher interest rate, compounded

Downsides:

– Lose the flexibility for OA usage, and possibly a good property opportunity (whether or not you should, is a separate discussion)

– Now, another downside that is not so apparent (ST did an article on this but the calculations were too simplistic), is the opportunity cost it has on the potential top-up via cash. More specifically, because of an OA top-up, one would have reduced the “space” for potential cash top-up (7k per year), limited by SRS. This reduces the potential tax savings for a certain number of years, as well as the potential higher interest rate the cash can enjoy (assuming one does not have a better way to invest that cash).

Personally, the interest rate factor was not a huge concern as I invest my cash. However, the tax savings point (and its attendant TVM, because one would also invest tax savings) was significant.

Thus, I did up a spreadsheet to determine which is more “worth it”, with these parameters (1) age, (2) tax rate (to determine tax savings), (3) expected returns rate on the cash if not used for top-up, (4) amount of OA topup to SA, and (5) an assumption that FRS will continue to rise at approx 4k per year.

Without going into specific details, would like to share some insights:

(1) OA top-up to SA always earns more. Just gotta get this out of the way, but it is quite intuitive because larger sum + TVM. However, the bigger question is whether it’s worth the loss of flexibility OA has.

(2) For people older than 40, should do cash top-up to SA compared to OA top-ups. Potential loss of more tax savings due to higher pay. Interesting because it is aligned with your recommendation, implying that it is indeed a good move.

(3) OA top-up to SA is most worth it for younger people (<30), with a low tax rate. But the problem with this is the group of people who needs to use their CPF OA the most.

Hence, OA top-up to SA exists in a rather awkward position as a policy and investment tool. On one hand, objectively it always create better returns than cash top-up, but by design it is really optimal only for young people, who have a low tax rate, are cash rich, and have a substantial OA for top-up…who hardly exists. So because of its inherent inefficiencies, I chose not to do OA top-up to SA, but rather leave OA where it is and efficiently purposed.

Hi Alaric,

My apologies, I may have missed this comment previously. Anyway I reread your entire comment again, and I must thank you for your sharing. It’s a point that I had not considered previously, but I do agree with most of your observations.

Most young people will (at most) think of cash topups to CPF, I highly doubt any young person would consider using OA to topup SA.

Just recently, CPF Life and RSS did something horrific. The calculation for monthly payouts beside the usual age, sex, assumed medical is based on the quantum transferred from RA account to CPF Life and the payout period( from 65 to 70 to 85, our estimated lifespan, which I guess, it could be the national average lifespan of a Singaporean). So, the period pegged to national lifespan average was increased to 92-97 years old. Please play with the CPF calculators.This means that instead of a payout period of 20 years(65to 85), it is now about 30 years( 65 to 95). This formula has depressed the payout sum. Yet, it is hidden under ‘actuarial’ rubbish, a non-transparent way of doing things! This is my anecdotal research of my peers, recently receiving their monthly payouts, a much lower sum to their surprises. Almost a third. It has upset and surprise many recipients.

Hmm… that’s definitely one problem with CPF Life…

Well, actually, the first 40k of CPF SA attracts extra interest, which means that it pays 5% in total. 5% is pretty darn good, so the opportunity cost is not as high as we think.

Yeah, fair point. Although for someone who has worked for a few years (or has high income), he might already have hit the 40k ceiling, so he only gets 4%. But yeah, absolutely get where you’re coming from.

I think you need to rewrite the whole paragraph again. There is already change since I believe from 2015 onwards. Your article have since consider misleading to many. Go to CPF life estimator again and key the figure of age 55 FRS 171K and bequest amount at 65 , he would receive $267K of bequest.

Your article is in 2019 but it seem that you misread certain conditon mainly

1) Issue of policy – Deduction of Premium will be done just before PEA or age 65 (not like in 2015, it is at 55 and hence your calculation). This affect your calculation above

Wow you are right, I just did this on CPF Life and it seems they have updated the calculations since the time I wrote this article. Do you happen to know when this change came about? I’ll try to do an update article on it.

I just trying to find out more on CPF basic Withdrawal plan and how do you “lose” your premium interest. For CPF life std/esc plan, your losses is always on the bequest loss if you pass on early meaning to say if you passes on early say age 67 – age 89 , you stand to lose bequest amount around $40,000 to $140,000 as compare to Basic Withdrawal. You should do a write up on that as CPF have smartly avoided mention that in their website

Secondly, for basic withdrawal , the premium is 10-20 percent of RA amount which I believe the interest earned go to the LIF pool. This interest I believe can be withdraw when you are age 90(only for basic) which range around 54K to 108K (based on FRS of $181,000.00)

So for basic plan, if you passes on before 89 or worst at 89, your losses is around (1K – 108K)

premium is refundable for this case but not the interest

Hi FH.

I understand that at 55yo, SA + OA will go into RA.

The balance above minimum sum CAN be withdrawn.

What are the options for this balance.

Can we leave it in OA to yield the 2.5% interest?

Can we decide in the future to withdraw any portion we wish?

Or is the case, MUST withdraw the complete balance at 55yo?

I hope you can enlighten.

As I recall, you can leave it in CPF to earn the 2.5%. 🙂

Can we leave any balance after hitting FRS in the RA to earn the 4-5% int?

I recall the answer to be yes, but there are some contraints as to when and how the money can be withdrawn.

Hi

Thank you for a very informative article.

Can you confirm if the passage below is correct? Because I would assume that all interest earned between age 55 to 65/70 would belong to the CPF member personally and not go into the annuity pool.

“Let’s use a simple example here. Imagine Xiao Ming picked the Standard Plan on a Full Retirement Sum when he was 55. He put in S$176,000 at 55, and this generated interest at a nice 4 – 5% a year. At 65, he starts receiving about $974 – $1,028 a month. Unfortunately, he passes away 10 months after his 65 birthday, so the total amount he withdrew from CPF Life was only about S$10,280.

The amount that will be left to his loved ones, will be the original amount at 55, less the payouts he received: S$176,000 – S$10,280.”

If I am correct about CPF member keeping the interest earned on their RA before the annuity starts, Xiao Ming would therefore leave to his loved ones the S$176,000 plus 10/15 years of interest minus S$10,280. Since Xiao Ming opted for the Standard Plan (100% of his RA balance goes into the annuity).

If Xiao Ming had opted for the Basic Plan (10% of RA balance goes into the annuity), he would leave behind for his loved ones the following:

S$176,000 plus 10/15 years of interest minus S$10,280 plus 10 months’ interest on S$158,400 (which is 90% of S$176,000)

That’s a really good question. I recall this was the case when I wrote the article, but perhaps I made a mistake when running the numbers, or things have changed since.

If you input the same numbers into the CPF Life calculator, you will be able to get the answer. Do let me know if my understanding above is incorrect!