In my previous article on CPF, I made the argument that one should think carefully before making CPF topups because (1) CPF-SA money is locked away until 55, (2) changes to CPF retirement sum or CPF Life can affect your ability to withdraw CPF moneys, and (3) the 4% interest rate on CPF-SA may not match up to equity market returns over a 20 – 30 year investment timeframe. I also argued that CPF topups are best suited for older Singaporeans who are nearer to 55, while younger Singaporeans should consider SRS instead.

Since then, there’s been some really great information and commentary that came to light, that really enriched this debate. So I wanted to revisit the issue, and examine if my original arguments still made sense.

The first piece of information, is a commentary written by someone’s former GP teacher. It was shared on his Facebook Page, and was eventually picked up by Seedly.

I’ve extracted the Seedly version below because it has some nice charts:

Tldr; A recipe for boiled frogs

A Minimum Sum with no Maximum

It’s not that easy to find information on the changes to the CPF over the last 40 years. You would think that the CPF Board would have made a simple, easy to read article or poster charting those changes, but no. (I wonder why…)

So I looked through the Hansard, (the record of what is discussed in Parliament) to find out when the changes took place and the reasons for those changes and the promises each Minister made, and whether they stuck to those promises or not…

So here is what I’ve got so far. Apologies for the long post.

In 1984, the PAP govt proposed raising the CPF withdrawal age from 55 to 60. There was widespread opposition to this plan, with objections from NTUC and even PAP MPs like Lim Boon Heng and Toh Chin Chye opposing the plan in Parliament. It didn’t go through.

In the 1984 General Election, the PAP’s share of the vote dropped from 77.7% (1980 GE) to 64.8% (1984 GE). And for the first time since 1965, the opposition won seats in a General Election, capturing not just one but two seats (Chiam See Tong and JB Jeyaretnam).

So the PAP went and licked its wounds, and then came up with the Minimum Sum Scheme. The idea was that age 55, you could still withdraw all of your CPF, but…

… the govt was worried that people might squander their retirement savings or they might lose it to conmen or bad investments. So the govt proposed the setting up of this thing called the Minimum Sum Scheme.

A sum of money from your CPF withdrawal at age 55 would have to be placed in a retirement account. A fixed minimum amount, set at $30,000. Money from this account would be paid to you from age 60 onwards, about $230 every month, for the next twenty years.

And if you had property worth more than $30,000, you could pledge your property, so you could still withdraw all of your CPF savings. Lee Yoke Suan, the minister proposing the scheme said that most Singaporeans would be able to pledge their property and so they would be able to withdraw all of their savings. And they would also enjoy a monthly sum of money from age 60 onwards, from their retirement account. Seems wonderful right?

But then the Minimum was adjusted in 1989 because of worries about inflation.

Then it was hiked by 5K each year from 1995 because of worries of longer lifespan and higher expectations of living, with the promise that after it hit 80k, adjustments would go back to being pegged to inflation.

This promise was abandoned (or forgotten?) in 2004 when it was hiked by annual amounts ranging from $4,500 to $11,000 from 2004 to presently 2019. I guess the only way is up…

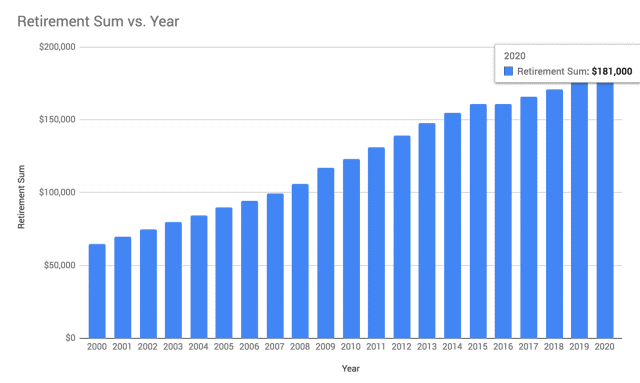

Minimum sum through the years:

| Year | Retirement Sum |

| 1986 | Minimum sum scheme announced by Lee Yoke Suan. |

| 1987 | $30,000 – could be fully covered by a property pledge. |

| 1989 | $30,900 – minimum sum starts to be adjusted yearly for inflation (Minister Lee Yoke Suan, in reply to MP Charles Chong) |

| 1994 | Minister Lee Boon Yang announces changes to CPF, Minimum Sum to be raised to $40,000 in 1995 and by $5000 each year up to $80,000 in 2003. After 2003, increase will be pegged to inflation). |

| 1995 | $40,000 – Now only 50% can be covered by property pledge (announced in 1994, Lee Boon Yang) |

| 1996 | $45,000 |

| 1997 | $50,000 |

| 1998 | $55,000 |

| 1999 | $60,000 |

| 2000 | $65,000 |

| 2001 | $70,000 |

| 2002 | $75,000 (Minister Lee Hsien Loong announces that Minimum Sum will be raised beyond 80k in 2004, by an amount yet to be decided. ) |

| 2003 | $80,000 |

| 2004 | $84,500 (+4.5k) |

| 2005 | $90,000 (+5.5k) |

| 2006 | $94,600 (+4.6k) |

| 2007 | $99,600 (+5k) |

| 2008 | $106,000 (+6.4k) |

| 2009 | $117,000 (+11k) |

| 2010 | $123,000 (+6k) |

| 2011 | $131,000 (+8k) |

| 2012 | $139,000 (+8k) |

| 2013 | $148,000 (+9k) |

| 2014 | $155,000 (+7k) |

| 2015 | $161,000 (+6k) |

| 2016 | $161,000 (no change because date of change of minimum sum changed from July to January) |

| 2017 | $166,000 (+5k) |

| 2018 | $171,000 (+5k) |

| 2019 | $176,000 (+5k) |

| 2020 | $181,000 (+5k) |

$181,000 – the minimum sum today (now called “Full Retirement Sum), of which only 50% can be covered by a property pledge – so you will still have to set aside $90,500 in your CPF.

Reference Link: https://www.cpf.gov.sg/Members/Schemes/schemes/retirement/retirement-sum-scheme

Visual chart from 2000 to 2020

Age where you start receiving payouts from the Minimum Sum:

| 1987 | Monthly payouts can start from 60 |

| 1999 | raised to 62 |

| 2012 | raised to 63 |

| 2015 | raised to 64 |

| 2018 | raised to 65 (to be raised to 67, when re-employment law matches 67.) |

| 2019 | supposed controversy over CPF letter reminding people that they have to apply for their payouts to start from 65. |

What a difference 35 years makes, doesn’t it.

In 1985

At 55, you get access to all your CPF money and can use it how you see fit.

In 2020

At 55, you can get $5,000 of your CPF money plus the rest except for the first $181,000 (or first $90,500 if you pledge your HDB) which you will get in a monthly payment from age 65 onwards.

A Simple Formula to Predict How much you will need at your age

If you want to guesstimate what the Minimum Sum (Full Retirement Sum) will be when you turn 55, use this formula:

$5000 × (55 – your age this year) + $176000 = __________

Mine is $251,000

In other words, CPF Minimum Sum amounts go up over time, and the withdrawal age (and rules) evolve over time. And if you use the data since 2000, it usually goes up by about S$5000 a year on average.

Of course, sharp readers will point out that one problem with the analysis above is that it takes past dollar values and extrapolates it into the future based on simple dollar values, without taking into account the effect of compounding.

Another way to analyse the data, would be to use compound interest. If you take CPF Minimum Sum to be S$30,000 as at 1987, and if it will be S$181,000 in 2020, that works out to a 5.6% compounded annual growth rate (CAGR). Interestingly enough, this 33 year CAGR of the CPF Minimum Sum, being 5.6%, is higher than the rate of return on CPF-SA at 4% (excluding the first S$5,000). And for discussion’s sake, if you extrapolate this compounded growth into the future, after another 30 year period, the CPF Minimum sum in 2050, based purely on this simplistic analysis, will be about S$928,000.

Of course, I am not saying that the CPF Minimum Sum will be S$928,000 in 2050. Where it will actually be in 2050 depends on many factors beyond our control, such as life expectancy, Singapore inflation rates, economic growth etc. However, if you accept the argument advanced by the Singaporean above, then you will appreciate that there is some uncertainty over where CPF Minimum Sums will be in future. And that to me, is the key point here.

Of course uncertainty works both ways, so there could also be the possibility that the CPF Minimum Sum is completely abolished some time in the future, rendering this entire discussion pointless.

The next interesting comment was shared by a fellow reader on Financial Horse’s comments section:

Just recently, CPF Life and RSS did something horrific. The calculation for monthly payouts beside the usual age, sex, assumed medical is based on the quantum transferred from RA account to CPF Life and the payout period (from 65 to 70 to 85, our estimated lifespan, which I guess, it could be the national average lifespan of a Singaporean). So, the period pegged to national lifespan average was increased to 92-97 years old. Please play with the CPF calculators. This means that instead of a payout period of 20 years (65to 85), it is now about 30 years (65 to 95). This formula has depressed the payout sum. Yet, it is hidden under ‘actuarial’ rubbish, a non-transparent way of doing things! This is my anecdotal research of my peers, recently receiving their monthly payouts, a much lower sum to their surprises. Almost a third. It has upset and surprise many recipients.

Now this is a real life example of a reader who was receiving CPF Life payouts, only to find that his (and his peers) monthly payout sum decreased drastically due to the way CPF Life is calculated. Which really helps to put things in perspective

The last interesting comment I wanted to share, was another comment by a reader:

Hi FH, I got interested in this article because I personally did a great deal of research (and calculations) on CPF SA. I think this was one question your article didn’t really address, but could be of interest:

[[Should you top up your SA with OA?]]

Benefit:

– Enjoy higher interest rate, compounded

Downsides:

– Lose the flexibility for OA usage, and possibly a good property opportunity (whether or not you should, is a separate discussion)

– Now, another downside that is not so apparent (ST did an article on this but the calculations were too simplistic), is the opportunity cost it has on the potential top-up via cash. More specifically, because of an OA top-up, one would have reduced the “space” for potential cash top-up (7k per year), limited by SRS. This reduces the potential tax savings for a certain number of years, as well as the potential higher interest rate the cash can enjoy (assuming one does not have a better way to invest that cash).

Personally, the interest rate factor was not a huge concern as I invest my cash. However, the tax savings point (and its attendant TVM, because one would also invest tax savings) was significant.

Thus, I did up a spreadsheet to determine which is more “worth it”, with these parameters (1) age, (2) tax rate (to determine tax savings), (3) expected returns rate on the cash if not used for top-up, (4) amount of OA topup to SA, and (5) an assumption that FRS will continue to rise at approx 4k per year.

Without going into specific details, would like to share some insights:

(1) OA top-up to SA always earns more. Just gotta get this out of the way, but it is quite intuitive because larger sum + TVM. However, the bigger question is whether it’s worth the loss of flexibility OA has.

(2) For people older than 40, should do cash top-up to SA compared to OA top-ups. Potential loss of more tax savings due to higher pay. Interesting because it is aligned with your recommendation, implying that it is indeed a good move.

(3) OA top-up to SA is most worth it for younger people (<30), with a low tax rate. But the problem with this is the group of people who needs to use their CPF OA the most.

Hence, OA top-up to SA exists in a rather awkward position as a policy and investment tool. On one hand, objectively it always create better returns than cash top-up, but by design it is really optimal only for young people, who have a low tax rate, are cash rich, and have a substantial OA for top-up…who hardly exists. So because of its inherent inefficiencies, I chose not to do OA top-up to SA, but rather leave OA where it is and efficiently purposed.

Really interesting discussion right? After reading all these comments, what I figured was that my original analysis on CPF top-ups was way too simplistic. There were just so many other factors in play that would determine whether you should perform a CPF topup:

Ability / Confidence with investing – With CPF-SA, you are essentially locking up the money from your current age until 55, in exchange for a 4% interest rate (excluding the first S$60,000 in CPF). By contrast, the long term returns from equity markets over 100 years is around 6%. This means that if you are a good investor, there is a decent chance that you could probably earn more on the money if you invest it yourself, than if you place it in CPF-SA.

That said, similar studies also show that the long term average returns of retail investors is around 2.5%, simply because they buy high, and sell low, and try to market time. So be honest with yourself on your investing prowess. If you don’t think you are a good investor, CPF topups may be a good choice.

Age – 55 minus your age, is basically the lock up period for the amount of your CPF money that is greater than the CPF Minimum Sum amount at 55. And the longer the lockup period, the greater the chances that a similar investment in a broad equity index will outperform the 4% benchmark rate paid by CPF-SA. And the longer the lockup period, the greater the uncertainty over the CPF Minimum Sum when you hit 55.

The way I see it is this. The closer you are to 55, the more CPF topup makes sense (assuming you cross the CPF Minimum Sum), because 4% guaranteed returns is great over the short term. The closer you are to 55, the less uncertainty over CPF Minimum Sum and withdrawal policies as well.

Income Tax bracket – Your income tax bracket matters because cash topups into CPF-SA are tax exempt, to the tune of S$7000 a year. So if you are in a high tax bracket (I would say anything above 10% is worth it), you should seriously consider using CPF cash topups or SRS as a way to avoid tax. By contrast, if you are in a low tax bracket (below 10%), you should favour topups from CPF-OA into CPF-SA, because the tax savings for you are less important.

I wrote on article on SRS as a method of tax avoidance previously, so do check it out if you are keen (CPF also has a great article on CPF topups vs SRS ).

Life Goals / Cash on hand – This is a tricky one. If you have a lot of cash on hand, and you don’t need to use it anytime soon, a cash topup into CPF-SA makes sense. If you have no cash on hand, but you have a large CPF-OA that you don’t need to access anytime soon, a CPF-OA topup into CPF-SA makes sense. If you are young and saving up for your first house purchase, neither CPF-OA or cash topups make sense, because you will need to save it to buy a house and get married. So it’s important to understand your life goals here.

Rate of CPF Minimum Sum increase – Based on the reader commentary set out above, what is clear is that it is incredibly hard to know for certain what the CPF Minimum Sum will be when you are 55. A lot of comments I received on the previous article were that you should top up your CPF earlier, to give it more time to compound, so that it can outpace the rate of increase of CPF Minimum Sum. I definitely get the merits of that argument, but without clarity on the exact formula used to determine CPF Minimum Sum, I think it’s hard to say conclusively that the 4% return outpaces CPF Minimum Sum increases.

Rounding it up

To round it up, CPF cash topups are best for older investors, who have high income, and lots of cash on hand. Of course, such investors should do both CPF cash topups, and SRS.

CPF OA topups into CPF-SA are best for younger investors who have lots of cash on hand and no need to access the liquidity anytime soon. And, as the reader mentioned above, such people simply do not exist, so CPF OA topups into CPF-SA are indeed in a pretty strange place.

Closing Thoughts

So after all that discussion, where does this leave us? At least for me personally, the answer is clear. I am in a medium income tax bracket, but I personally use SRS for tax avoidance. I think I am an average investor, so the 4% returns on CPF-SA is only decent. I am young, so the lockup on CPF-SA moneys is long, and less attractive. I do have quite a lot of cash on hand, but also a lot of spending coming up, so that would discourage me from CPF topups. And personally I do also have some reservations on how CPF Minimum Sum will evolve in the coming years, so I prefer to adopt a wait and see approach.

For me at least, it’s pretty clear to me that I wouldn’t be doing a CPF cash topup anytime soon.

Would love to hear your thoughts on the above!

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

How long will these Golden Numbers hold ?

4% Interest Rate

CPF Withdrawal Age 55

CPF Life Payout Age 65

CPF Life Payout Duration

Yes, I do agree that there is uncertainty over changes to CPF policy going forward, especially for those who are looking at a 20 to 30 year horizon.

I think a bit differently or take another approach to CPF-SA account. I take it as a protective put per se at 4% return guaranteed. Which means no risk. In investment world this is like a sharp ratio of 4, which does not exist anywhere else.

So if one is above average tax bracket and has spare cash allocated for retirement, CPF SA top ups are a must. Because this is your guaranteed paycheck received without much risk taken.

With SA account guaranteed returns, an average investor can afford to take more risk in equity markets and can afford to take the volatility long term. Without a decent stash in SA, taking long term equity risks is more scary.

I guess the main concern expressed in this article is the uncertainty over the ability to withdraw the money in the CPF-SA account. Doesn’t matter how much is inside if the withdrawal rules are tweaked when you are nearing retirement. Any thoughts on that concern?

Let’s vote the PAP government out of office. Then we can have a straightforward CPF policy or a simple retirement plan, when all the CPF can be withdrawn when a member reaches 55 years old. The government just used too much gimmicks in order to delay the return of our CPF. Thank you.

Well… that’s one way to see it. Thanks for sharing your thoughts. 🙂

This whole CPF is a bloody scam, so what if they gave you 5% or 10% return if end of the day they lock it up n can only see but cannot touch. We d Medeka Generation has been con for the last 40 years so just take my advice….VTO is d only solution if u don’t want to collect cardboard or clean tables .

Thanks for sharing your thoughts. 🙂

I think majority of Singaporeans are being too unfair to its government. As a foreigner here I see government policy is quite sound and fair and logical. It’s actually good that CPF does not allow to take all the money and requires some standard minimum to be kept. Government rightly assumes that majority of retail investors will be better off this way than taking out their entire life savings at one point and squandering them all. Retail investors tend to underestimate investment risks and attribute their portfolio performance to their skill than to the market, that’s why based on some US statistics, retail on average earns 350-400 basis points lower than what market gives.

I see it all the time in my practice: starting from people not reading what they sign to genuinely misunderstanding what they read or misplacing their risk appetite. So, overall I think its a good development for CPF not to give back all the money.

And about uncertainty – the only two certain things in life are death and taxes like someone famous said. Markets performance is uncertain too. So don’t think CPF policy is more volatile than the market. With 4% risk free return, I am ready to take the volatility and uncertainty.

Hi Elena, thanks for sharing your thoughts, really insightful stuff. I guess when you have a national, mandatory savings plan for all citizens, and you make unilateral changes to the withdrawal policy, there is bound to be people that are upset. That said, I definitely agree that CPF is better than many other national pension plans out there, but as Singaporeans, it is our goal to ensure that we do not rest on our laurels, and continually improve CPF to ensure that it remains the market leader and the best pension plan available in the world. Discourse like this, and promoting greater understanding on the benefits and limitations of CPF, is definitely a great start!

Try Russian government pension….you will be running back to Singapore and praising you were born here…guys, you do live in paradise by most places standards…

How is it a scam? Have you checked annual GIC returns for past 10 years? Do you know GIC invests all over the world and started doing a lot of innovation in the world of investment waaay before hedge funds did? Please, give some credit to your government and what they do. They work your CPF quite well for returns. Russian government is just sitting on a pile of cash or buying gold – not much to achieve even 1% return. Does not re-invest oil and gas income either. So, really, read up a bit before making such statements. I am not a Singaporean, but I am offended.

Elena, please do not be offended by the vocal minority that does not represent the informed majority. With only emotive words and no viable alternatives, this is an exact reflection of their lives and why they are in such predicament in the first place.

The 1st issue with financial investments is that modern corporate finance involves alot of financial engineering. Some of the methods used are pretty dodgy. Variables and valuations can be easily goal-seeked. The 2nd issue is that there is an increasing increase (!) in the monetary base (if I may extrapolate this to refer to the world’s MB based on the fed’s) and the debt (the other side of MB) in the system. Therefore when the tide rises, all boats rise. Therefore, one can slowly begin to appreciate that it is only know in our “modern” era that the value of financial assets seem to be moving up rather quickly while the real world income stagnates and payday loans are now even offered in Singapore! :O When the entire structure of debt based fiat collapses, Goalseeked values will no longer hold any meaning because $ will be toilet paper (and without the need for a financial alchemist at that!). Working within the confines of the current “modern monetary system”, it does appear to any sane person at first glance that the GIC is doing a pretty great job (I am sure the analysts there are elites / mandarins). However when collapse happens and correlation risk across assets is, horrors of horrors, realised, I am sure the one having the last laugh is definitely neither the good folks at GIC nor the Singapore government, it would probably be the countries which have placed their trust in that “barbarous relic”. If one believes otherwise, than one need look no further than the fact that the chinese government decided to advise its citizens to “invest” in that relic since the early 2ks, which incidentally might just explain the ramp up in its fiat “value”. Your government knows how the game is being played because it has been bitten once before.

Haha fair enough. Thanks for sharing your thoughts!