I’ve been getting quite a few questions about Credit Suisse, and the potential implications on markets.

There are a lot of bad takes out there, split between:

- Credit Suisse will default and become Lehman 2.0

- Credit Suisse is nothing to be worried about

Now the truth rarely lends itself to such simplistic takes.

So for the record – No, Credit Suisse is unlikely to default short term, and no Credit Suisse is unlikely to become Lehman 2.0.

But no, Credit Suisse is not something to be ignored as well.

This article is a premium Patreon article, written on 4 October 2022. If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates (like this) have moved there.

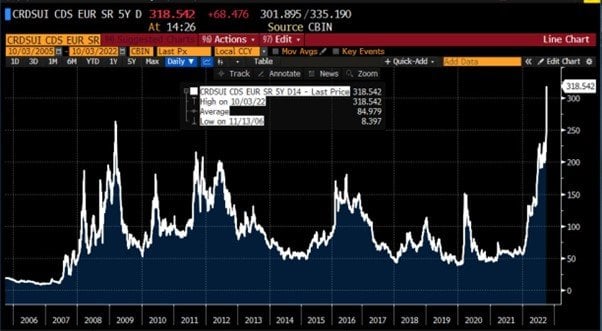

Credit Suisse CDS blowing up

Here’s the 5 year credit default swap (CDS) for Credit Suisse.

This is the cost to hedge against a default of Credit Suisse over the next 5 years.

As you can see, this week Credit Suisse’s CDS blew out to 300 bps, which was higher than what was reached in 2008.

Now remember, this is a free market, and CDS are typically only traded by big institutional investors (not retail investors).

Which means there are sophisticated players out there who are wiling to pay higher than 2008 prices to insure against the probability of default by Credit Suisse in the next 5 years.

Which is why those saying that this is nothing are not correct, something is indeed happening to Credit Suisse here.

This is NOT Lehman in 2008

BUT – for the record, the short term risk of default for Credit Suisse, is very low.

Breaking it down, Credit Suisse has a:

- CET1 ratio of 13.5%

- Liquidity Coverage Ratio is 191%

What does each mean:

“Common Equity Tier 1 (CET1) ratio compares a bank’s capital against its assets and covers liquid bank holdings such as cash and stock, as well as helping measure the ability of a given bank to withstand stress.

The liquidity coverage ratio (LCR) refers to the proportion of highly liquid assets held by financial institutions, to ensure their ongoing ability to meet short-term obligations. This ratio is essentially a generic stress test that aims to anticipate market-wide shocks and make sure that financial institutions possess suitable capital preservation, to ride out any short-term liquidity disruptions, that may plague the market.”

CET1 Ratio – 13.5%

Basically, for every $100 Credit Suisse lends, it is backed by $13.5 of liquidity.

This is very strong, and among best in class.

Back in 2008 it was about $3 per $100 lent out, but all that has changed post GFC.

DBS’s CET1 ratio, for the record, is 14.2%, only slightly better than Credit Suisse.

Liquidity Coverage Ratio – 191%

And for every $1 in short term obligations, Credit Suisse has $1.91 in liquid assets.

Again, this is among best in class.

So for what it’s worth, the risk of short term default by Credit Suisse here is very low.

BUT – This is not something to be ignored

BUT – if you think this is nothing, that is not right too.

Credit Suisse is a systematically important bank, and people are willing to buy 5 year CDS protection at 300bps, which is up 4-5x this year.

This isn’t something to be ignored.

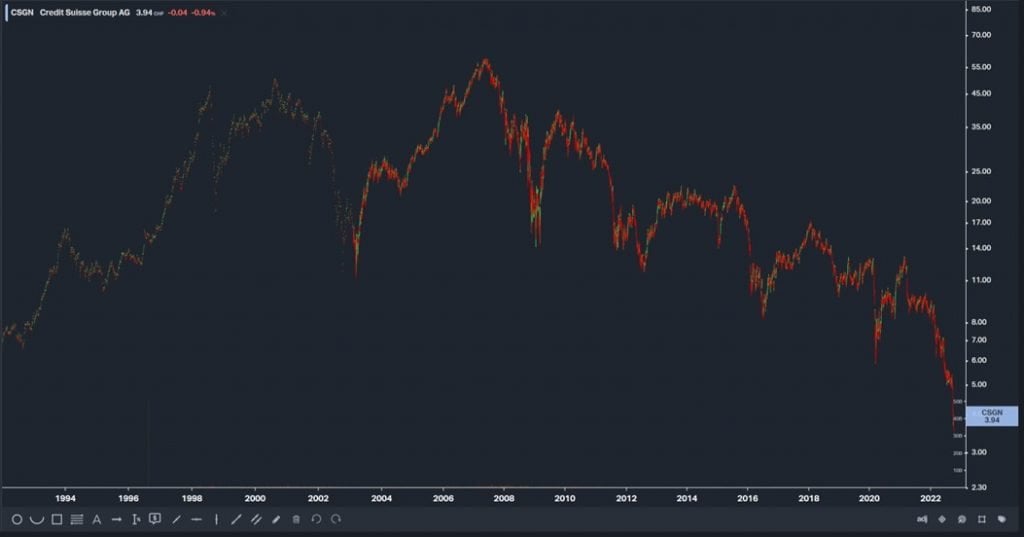

Meanwhile, the share price has plunged 60% this year alone.

And the long term chart is absolutely horrendous.

A decade of mismanagement and rock bottom Euro interest rates has done this to what was formerly a very illustrious and respected European bank:

The real problem for Credit Suisse…

Which brings us to the real problem.

A crisis of confidence, into feedback loops.

The doom loop works like this:

- Negative news in the media makes investors worried about Credit Suisse

- The CEO sending a memo to employees reassuring of solid “liquidity and capital strength” only creates more uncertainty

- Investors start to get worried. They:

- Start dumping products issued by Credit Suisse (to avoid counterparty risk), even at a loss.

- Move short term cash balances out of Credit Suisse

- Nobody wants to lend to Credit Suisse, borrowing costs go up

- Because of the plunge in share price, any capital raise would be incredibly dilutive

- As things worsen, any further downgrade by clearing houses could increase margin requirements, which exacerbate the issue

And so on.

You can see what started out as a crisis of confidence, can easily grow into some bigger.

Options for Credit Suisse are limited

Perhaps the bigger problem – is that options for Credit Suisse are quite limited.

With 5 year CDS at 300 bps, it becomes very hard to operate in investment banking.

Realistically, they are likely to have to exit their investment banking business, and transition mainly into private banking.

To pull off this restructure, they will need to raise about 4 – 6 billion Swiss Francs (by latest estimates).

With their market cap at 10 billion Swiss Francs, that’s an equity raise of almost half their market cap.

And you saw recently with SATS what happens when you try to do a big and dilutive equity fundraise in this market. And that was with a stable company generating good cash flow.

The same cannot be said of Credit Suisse.

They could try debt, but financing costs are likely to be prohibitive.

They could try asset sales, but when you’re bleeding the whole market smells it. So Credit Suisse is unlikely to get a good price on any of their asset sales in this market.

What does this all mean?

So I tried to explain the above as simply as I could, but it might still come across as a bit technical.

So to sum it up very simply:

There is no immediate default risk for Credit Suisse.

Talks of Credit Suisse imploding this week and triggering Lehman 2.0 are alarmist.

But frankly, the options going forward for Credit Suisse are limited, and not pretty.

Instead of a liquidity crisis, this may become one of solvency.

Credit Suisse will need to come up with a credible restructuring plan (backed up by capital raise and asset disposal), and they will need to avoid any further rating downgrades and/or crisis of confidence.

And even then, there is significant execution risk.

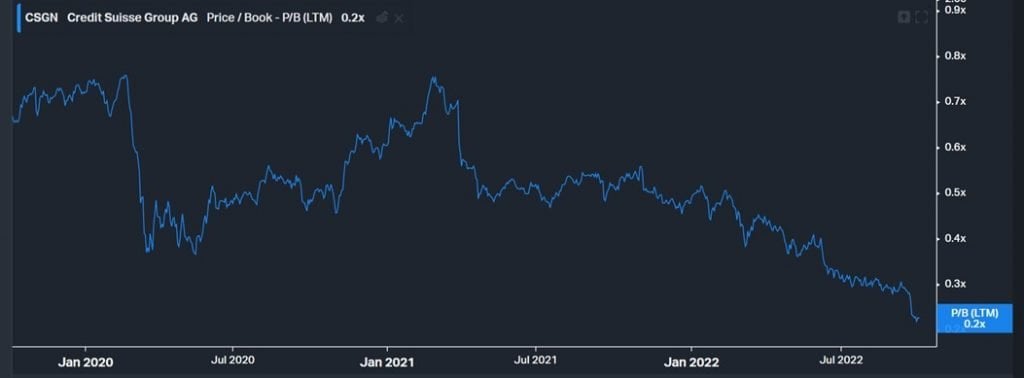

Is Credit Suisse stock a good buy?

Credit Suisse trades at 0.2x Price to Book:

That may look cheap, but frankly it is in line with other low-quality euro banks (Deutsche Bank for example).

It’s really a falling knife at the moment.

And in the absence of a catalyst, it’s hard to see what can arrest the slide in share price.

Don’t forget, there is also significant execution risk in any turnaround plan.

Many CEOs have tried over the past decade, to very little success.

Implications for the market generally

A decade of interest rates stuck at rock bottom is gone.

The era of cheap and unlimited liquidity is over.

Players like Credit Suisse couldn’t turn around their business in an era of cheap liquidity and rock bottom interest rates, and now they need to try again with higher interest rates, and tighter liquidity.

And that to me – is the key takeaway.

Credit Suisse might have been the first domino this cycle, but I highly doubt it will be the last.

As interest rates continue their march up, as liquidity gets tighter, we will start to see more and more “Credit Suisse” start to emerge from the woodwork.

For a decade you were able to paper over poor businesses because of favourable liquidity and financing.

All that is about to change.

If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates have moved there.

At S$15 a month you get the premium weekly market updates like this one.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get my full personal portfolio.

Don’t be penny wise pound foolish.

Think about how much you may have lost this year.

And how much you will lose in the next 12 months if you start buying too early.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Disclaimer: The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH,

It is very relaxing to read your blog on the weekends, when financial markets are closed. Your blog is enjoyable, prob the most enjoyable markets read in Singapore.

However, to pay for your portfolio, you need to do 2 things. 1. Track your portfolio performance and share it, to show you are in line or outperforming. Many credible bloggers do it, such as Breaking the Market. I can put your portfolio up on my Bloomberg to track it, for eg. 2. You need to go beyond blue chip stocks. Its easy to buy Mapletree or Capitaland Reits. No research required as these have state sponsors.

Having said that, I do empathise with your effort to build a side hustle that is fun. Your interviewee Jason Cai tried that, and I think received lots of hate mail for his option trade recommends that went wrong. So it is tough as Singaporean public is largely whiny and unforgiving. Perhaps you want to avoid that by not tracking your performance. But tracking it forces rigour, honesty and expertise on your own investing part.

My favourite markets blog is EarlyRetirementNow. It is completely free, Karsten has a PhD, works as a quant, and best of all he carries on thought provoking economic discussions with me on email. He loves numbers, as do I.

Thanks, truly appreciate the feedback and sharing! 🙂

Hi FH,

Nice article.

Usually, i don’t bother to read the comments but somehow end up reading it today.

Another “know-it-alls” teaching FH what to do.

Really don’t understand why these ppl are so free to attack you.

Pls ignore them and continue the good work, wish you a pleasant weekend.

Thanks, really appreciate the kind words. Means a lot.

Actually my wife and I read FH not only for the blog for many years but the entertaining comments. I like to see what other investors are doing.

In fact I think it is not wise to put all your money into stocks just because one guy on the Internet tells you to.

Haha, thanks for the support! 🙂

For what it’s worth, I mainly just share my views at the time the article was written. I don’t profess to be right, and I do change my mind when the facts change. This is how investing works.

I disagree. I think you are able to explain complicated situations in simple terms. A clear voice in this crowded space. Keep doing what you’re doing.

Thanks, appreciate the kind words. Means a lot. I try my best to contribute to the investing community in SG, hope it helps.

Actually, why don’t u show us the performance of your past portfolio ideas? How else I confirm whether good or not?

Hm alright, let me see how best to implement this going forward if there is demand. Might be a performance tracking for my current personal portfolio. Is that something that would help.

Hi FH,

Got baa baa sheep who would blindly go where you say. But i am from HK n dont trust any old how. I dont have 1m to invest or 800k a year but it is still my hard earned. I won’t just put money in any unit trusts my banker said is good. I still need to see results first.

Yup understand the point, will add this in as a new feature for Patreon moving forward.

Hmm, have worked in investment houses for 20 years, and daily morning meetings go like this:

A: We should buy XYZ stock.

B: Really? What about UVW stock?

C: What, how dare you B disagree with A! Get on your knees to beg forgiveness!

Fair to say C would not get hired by anyone to invest. Reminds me of a Rice Media interview with a teacher. She said Normal academic stream parents were nicer than Express stream parents, as they agreed with everything. Express stream parents questioned her more and debated her positions.

What do you think makes a good investor mindset, FH? What sort of investment discussion would you like to see in fund managers managing people’s money?

Yup understand the point, will add this in as a new feature for Patreon moving forward.

Maybe u can talk about defensive stocks to buy for next 5-10 years. With capital preservation as much as possible. Now this decade is high inflation , war, geopolitics all at the highest point!! Highest risk ever globally. Europe will drag the world in recession. Developing nations may default due to strong dollar. Sri Lanka already did. Many countries have yet to fully recover from Covid crisis and now we have more global problems. I think this decade requires more defensive positioning, Saudi Arabia which is US ally has turned on Us by selling them oil at higher prices. Really full geopolitics in play. The only thing I can agree with u is we cannot invest like the past 10 years.

The path forward is highly uncertain. I foresee s&p will go sideways since fed has to raise and reverse rates and maybe print money along the way to fight recession and inflation. Probably yet another lost decade for s&p. The war likely will drag on as Russia doesn’t seem to give up and is training more troops

Man, where did these trolls come out from

I always enjoy your sharing FH, thanks for doing what you do

Thanks, appreciate the kind words. 🙂

There will always be people who would offer differing opinions, but as long as they come from a constructive point of view, we should welcome them. You can learn from others’ suggestions and make your own decision, and probably most importantly, learn more about yourself too.

I personally feel FH is very humble. I have learnt a lot from you, please keep up the good work. I do hope to become your patreon in future.

Thanks for the kind words! I try my best 🙂

Hi FH,

I was debating with myself for a while whether to write this comment and in the end thought I would do it in the hope that it would be helpful. As pretty much no one reads comments on old articles, you will probably be one of a few, if not the only one, to read it. I believe it is most helpful when one is direct in providing feedback so I hope you don’t mind the bluntness.

1. It is important to balance sowing vs reaping

– You spend a lot of time to research and write good articles so it is fair and right that you are compensated for them.

– There has been a clear shift towards monetizing the site in the past couple of months with the more interesting posts being moved to Patreon only.

– While this is certainly your prerogative, I would be cautious about killing the golden goose by going too far in this direction.

– Interesting articles bring new readers to your site, a reduction of interesting articles would reduce the number of new readers. While you would be monetizing existing readers more effectively, over time, the number of new readers would fall, hence reducing the overall potential readership.

– Over the last couple months or so, there have been 18 articles on SSB/T-bills/FDs, a very straightforward and simple topic. These outnumber the more original articles that initially sparked interest in the site.

– The impact of this on the site will not be seen immediately but it will certainly have an impact over the longer term.

– Fundamentally, one would have to consider what the motivation was in setting up the site and if one wanted to move to a subscription based model.

– One way to balance this without being overly binary could be to release the Patreon only articles 3 months after they were written. That way, it provides interesting articles for new readers while still providing an advantage for Patreons who can act on the analysis in a timely fashion.

2. It is easy to be right for a couple of years, it is hard to be right over the long-term

– You have made some great calls over the last couple of years, especially calling out the market turning point during the pandemic.

– Yet, it is hard to be consistently right over the long-term. Cathie Woods is a good example and more locally, we have seen Forever Financial Freedom and Probutterfly who did well for a few years but are struggling somewhat now. There are very few Warren Buffetts in this world.

– The ingredients of how the market works have changed. With high inflation, clear indicators like a Fed pivot are no longer possible.

– My belief is that better answers come about with robust discussion across different viewpoints and this leads to better answers over the long-term.

– By having the more interesting articles being Patreon only, you lose the wisdom of the community and you do have some thoughtful readers making insightful comments and adding to the discussion in a meaningful way.

– Perhaps one way around this is to invite thoughtful readers to become “Honorary Patreons”. They may not contribute in a monetary fashion but their time and effort in commenting is worth a lot more than the $25 or $100 a month.

– BTW, as an aside, I am somewhat uncomfortable reading about “Don’t be penny wise pound foolish. Think about how much you may have lost this year. And how much you will lose in the next 12 months if you start buying too early.” as a reason for joining Patreon. Is this something that you or really anyone can credibly promise?

Anyway, just my two cents. I write this as a way to be helpful so pls take my comments in this spirit.

Hi CMC,

Thanks for the comment, and appreciate the feedback as a long time reader.

Just to share the thinking behind focussing more on T-Bills or SSBs of late – for some reason the demand for such content has been very high (in terms of readership).

And I myself have been getting a lot of queries on T-Bills/SSBs, many of which cannot be answered so simply. And given the macro climate, I do believe for long only investors, T-Bills or SSBs are probably the best place to be to ride out the storm in the near term, given elevated macro uncertainty.

So that’s the rationale behind focussing more on T-Bills or SSBs of late. For some reason it’s what the readership seems to want (as reflected by viewcount).

But in any case, I have been thinking about the exact same point, even before you raised it.

So rest assured that I will try to include more macro based content going forward. Have one planned for this weekend in fact!

Hopefully that would keep the general readers updated on my latest macro views. 🙂