Life is funny sometimes.

We went 20 months without any IPOs on the SGX main board.

And then in the span of 1 week, we get 2 great IPOs.

We covered Temasek Retail Bonds yesterday, and a lot of you have asked for this – so today we’ll review Daiwa House Logistics Trust IPO.

Is this REIT IPO any good? Worth subscribing? Let’s find out!

Basics: What is Daiwa House Logistics Trust?

From the Prospectus (emphasis mine):

“DHLT is a Singapore real estate investment trust established with the investment strategy of principally investing in a portfolio of income-producing logistics and industrial real estate assets located across Asia.

The initial portfolio of DHLT will comprise 14 high quality modern logistics properties in Japan with an appraised value of approximately JPY 80,570.0 million or S$952.9 million and an aggregate net lettable area (“NLA”) of approximately 423,920 square metres.”

Highlights of Daiwa House Logistics Trust’s IPO Portfolio:

- Pure Japan Logistics play at IPO

- 3.7 years Portfolio Age is very, very new properties

- 7.2 years WALE is pretty long (which is good)

IPO Details for Daiwa House Logistics Trust:

- IPO Price of $0.80 per unit

- Indicative Market Cap of $540 million on listing

- Forecast Yield for FY 2022 is 5%

- Public Offer of $20 million

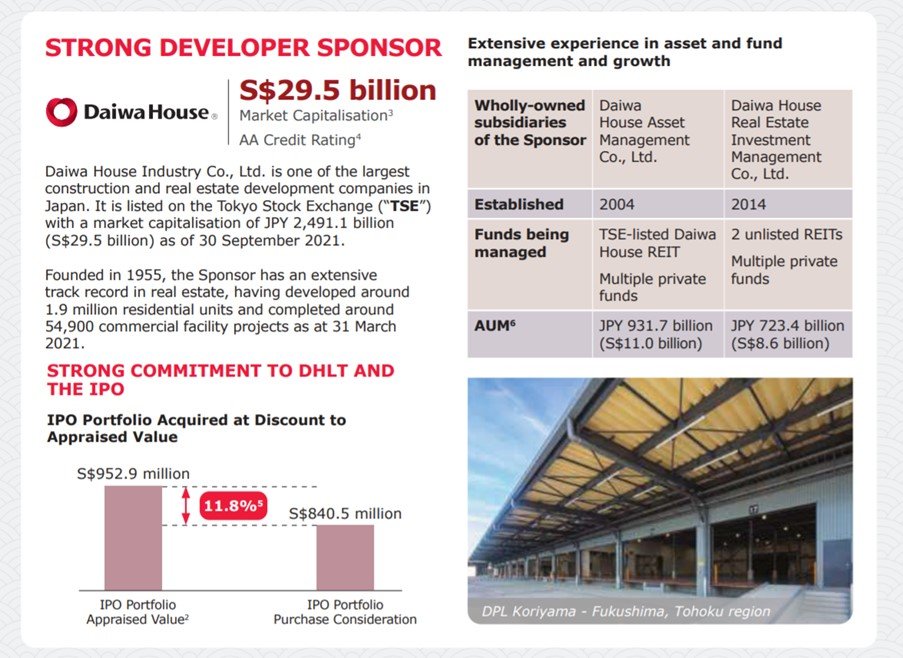

Sponsor of Daiwa House Logistics Trust – Daiwa House

The Sponsor, Daiwa House, is one of the largest construction and real estate development companies in Japan. It’s listed on the Tokyo Stock Exchange with a market cap of US$20 billion (S$27 billion).

The Sponsor has a real estate AUM of S$20 billion, which is not Blackrock or CapitaLand level, but still pretty decent.

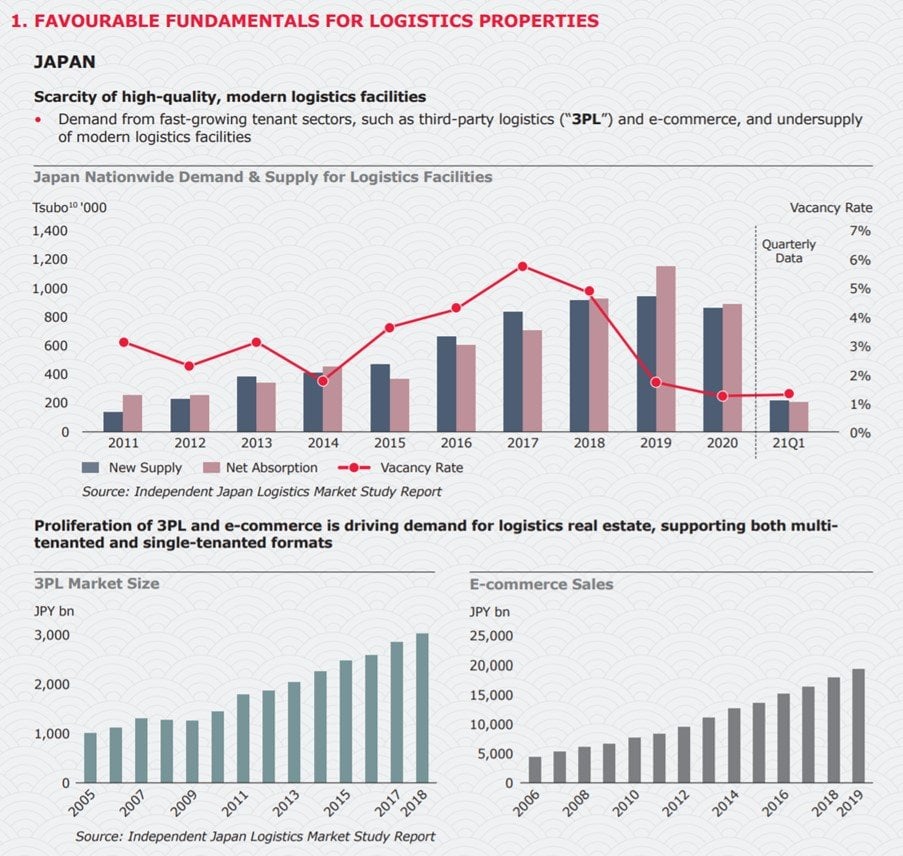

Logistics has tailwinds from e-Commerce

Because we’re living in the age of a global pandemic, logistics real estate is the hottest thing since sliced bread.

Just like the rest of the world, demand for e-Commerce (and logistics space) in Japan is very strong.

New supply of logistics properties is generally quite muted, translating into very low vacancy rates for logistics facilities in Japan (about 1%).

This is a very good sign.

How Good are the Properties for Daiwa House Logistics Trust?

The IPO portfolio for Daiwa House Logistics Trust is purely Japan, and you can see the locations above.

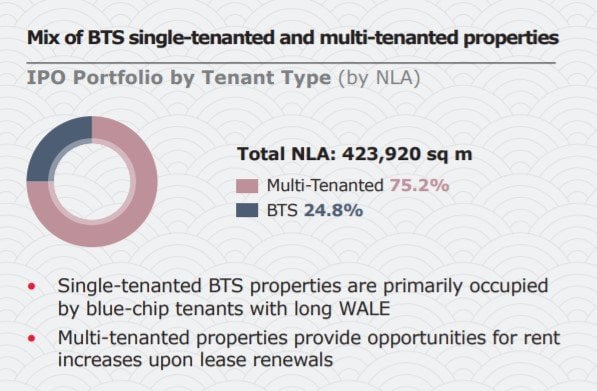

They’re a mix of Built to Suit (BTS) and Multi-Tenanted. BTS are locked into long term leases and give you bond-like stability, while Multi-Tenanted needs to be renewed over time and gives you upside (or downside) based on market rents.

Daiwa House Logistics Trust has a 24%-76% split between BTS and Multi-Tenanted, which is decent.

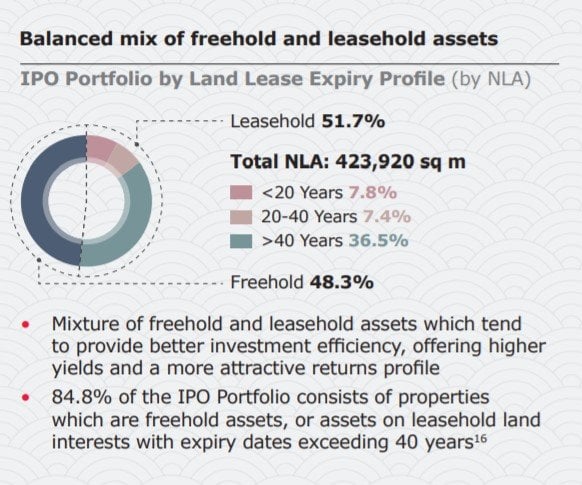

48% of the IPO portfolio is freehold, with another 36% with more than 40 years lease remaining.

There’s 7.8% with duration of less than 20 years though, which will be a problem in time to come. I don’t know how Japan real estate works – when the lease is up can you pay a nominal fee to the government to renew the lease?

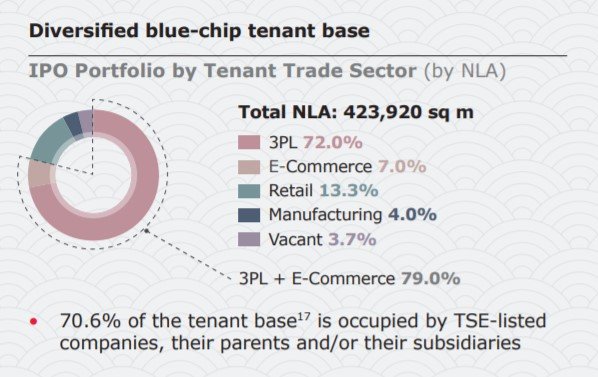

As you would expect with a logistics REIT, the bulk of it (79%) is leased to third party logistics or eCommerce.

70% of the tenant base is Japan listed companies, which is a very strong blue chip tenant portfolio.

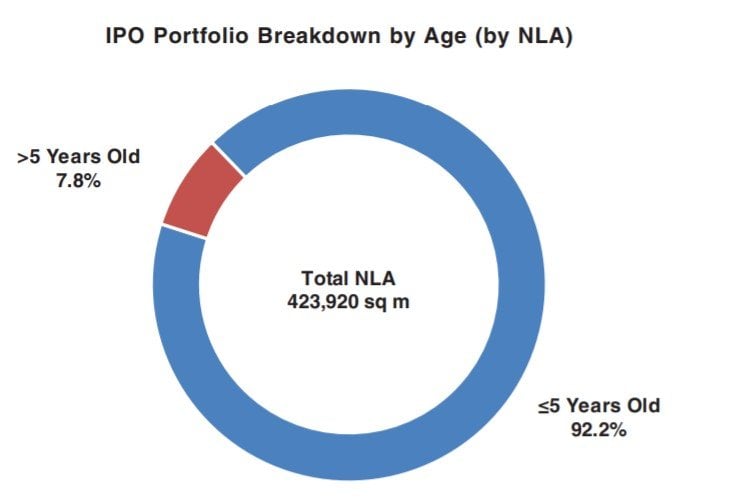

What is amazing about Daiwa House Logistics Trust is that the average age of the IPO Portfolio is only 3.7 years old.

That’s almost brand new.

There’s no income support, so the fact that they’re able to pull 6.5% natural yield with brand new properties is testament to how strong the demand for logistics space in Japan is (or how good the Sponsor is).

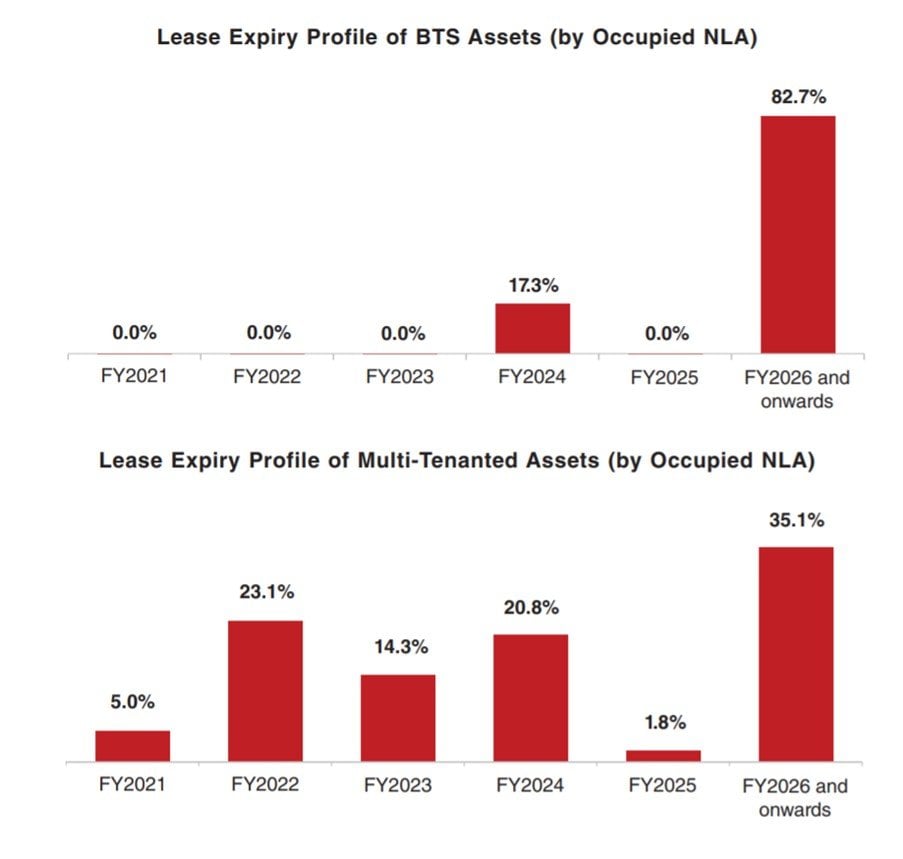

Lease Expiry profile is decent too.

For BTS most of the leases are expiring very far out, beyond 2026.

For Multi-Tenanted there is 23% of leases expiring in FY2022, but that’s not necessarily a bad thing as it could allow the REIT to lock in higher market prices.

Valuations of Daiwa House Logistics Trust

Daiwa House Logistics Trust is IPO-ing at 1.05x book value (NAV is $0.76 on listing date).

The valuer (Savills) used a cap rate of about 4%+ for the Daiwa House Logistics Trust Properties.

I checked this against the industry level cap rates for Tokyo (from CBRE), and they’re sitting at about low 4.0%.

I’m not that familiar with Japan real estate so I can’t comment further, but I would say the cap rates of 4.0% – 5.0% are not unreasonable.

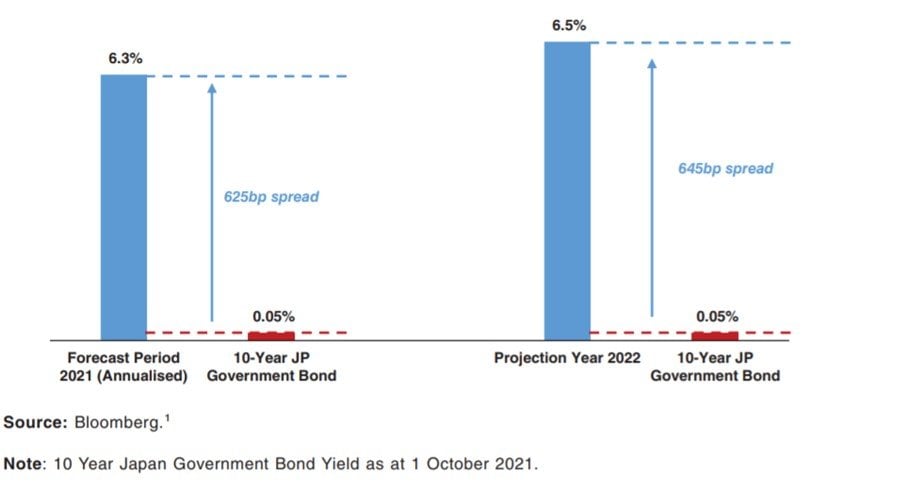

Distribution Yield of Daiwa House Logistics Trust – 6.5% for FY 2022

Projected yield for Daiwa House Logistics Trust is 6.5% for FY2022.

That’s a 6.45% spread against the 10 year JGB, which sits at a ridiculous 0.05%.

There’s a reason why everyone loves Japan real estate.

Comparative Valuations of other Logistics REITs

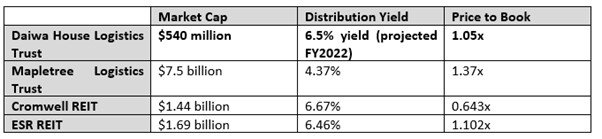

So Daiwa House Logistics Trust has an indicative $540 million market cap, 6.5% yield (projected FY2022), and 1.05x book value for a pure Japan logistics portfolio.

To put things in perspective, Mapletree Logistics Trust has a $7.5 billion market cap, 4.37% yield, 1.37x book value, for the geographical split below:

Cromwell REIT, which is pure European logistics, has a $1.44 billion market cap, 6.67% yield, 0.643x book value.

ESR REIT, which is pure Singapore industrial / logistics, has a $1.69 billion market cap, 6.46% yield, 1.102x book value.

It’s not an apples to apples comparison, but I would generally say that Daiwa House Logistics Trust’s valuations are generally in line with the market, and maybe slightly on the cheap side.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

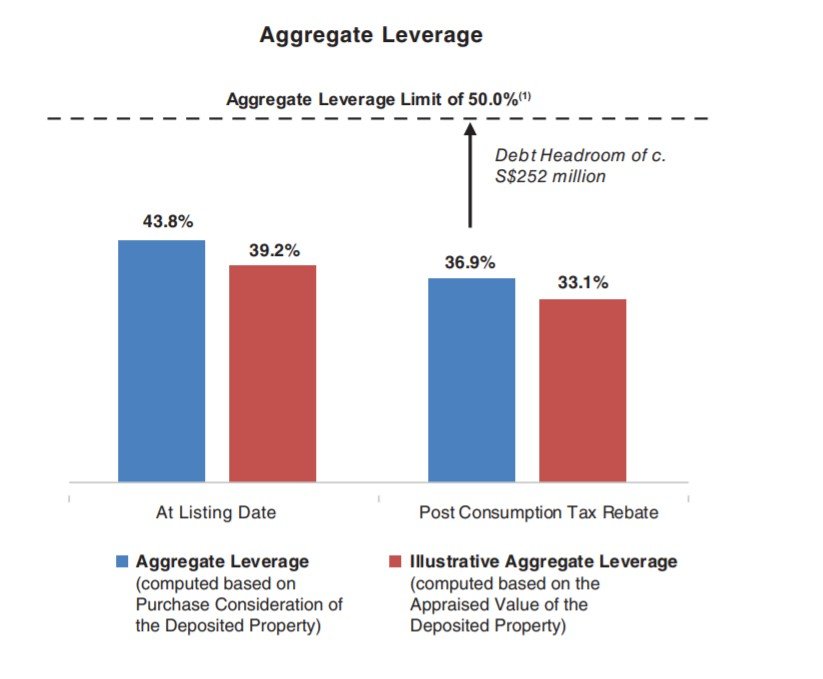

Leverage of Daiwa House Logistics Trust

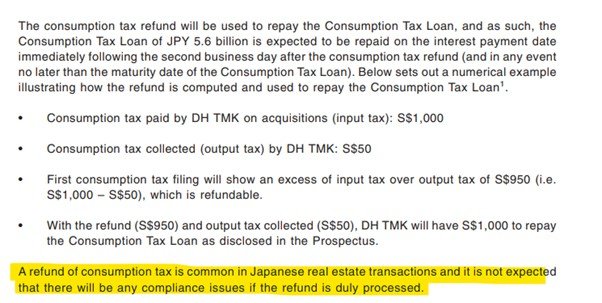

Leverage on listing is 43.8% which is actually really high for a new REIT.

According to Daiwa House Logistics Trust they will get a consumption tax rebate from the Japan Tax Agency by 2Q 2022 (this is rebate for the tax on the acquisition of the IPO portfolio), after which leverage will drop to 36.9%.

This is Japan not China so I’m generally less concerned about such things, and according to the Manager this is common in Japan real estate transactions:

Why did Daiwa House Logistics Trust IPO in Singapore instead of Japan?

A big question I had was why did Daiwa House Logistics Trust IPO in Singapore instead of Japan.

The Sponsor has a big brand name in Japan, surely they could have listed there and covered their books 10 times over?

Daiwa House REIT

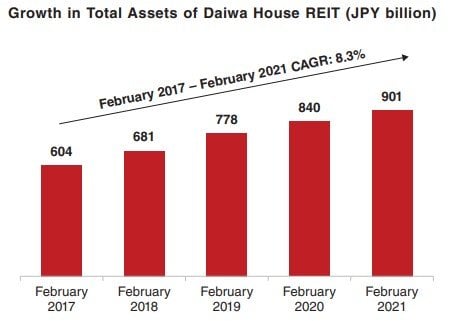

It turns out, they already have a REIT listed in Japan – TSE-listed Daiwa House REIT Investment Corporation.

Daiwa House REIT is a mega REIT, with a diversified portfolio of 227 properties, including 64 logistics facilities (50.0% of the total portfolio), all of which were developed by the Sponsor, in addition to residential and retail assets across Japan.

It has an AUM of JPY 846.5 billion (S$10.0 billion) and a market capitalisation of JPY 757.5 billion (S$9.0 billion).

Very decent growth in asset base over time too.

Looks like the CICT/Ascendas REIT of Japan, which is good as it shows the Sponsor has a good track record with their REITs.

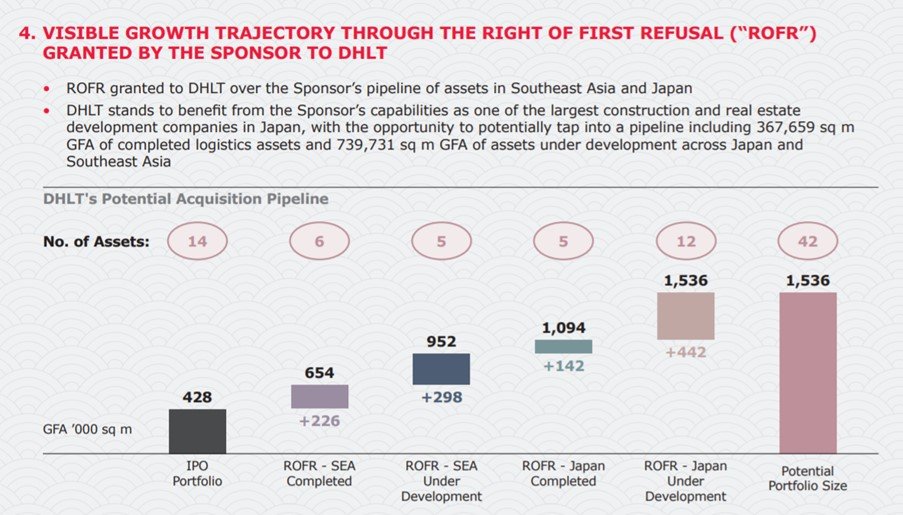

SEA ROFR Pipeline for Daiwa House Logistics Trust

It kind of makes sense then, that the Sponsor already has a mega REIT in Japan.

And they want to create a new Logistics REIT in South East Asia, that they can use to inject their South East Asia logistics assets over time.

Singapore is the largest REIT market in Asia ex Japan, with a very favourable tax regime, so it makes sense.

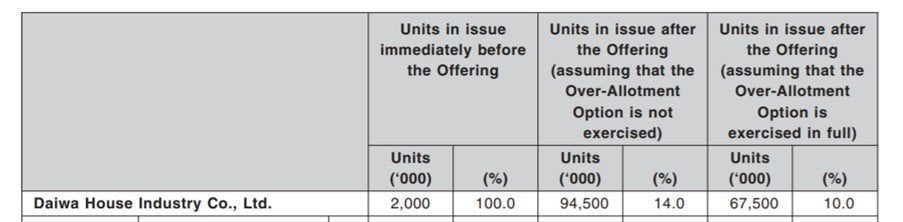

Sponsor holds 10% – 14% stake post IPO

The slightly worrying thing is that the Sponsor Daiwa only holds a 14% stake post listing, which drops to 10% if the over-allotment is exercised.

This is really low and looks a lot like the Sponsor cashing out.

I would have preferred to see them take a much bigger stake as a show of faith for investors, considering how tiny the market cap is on listing ($540 million).

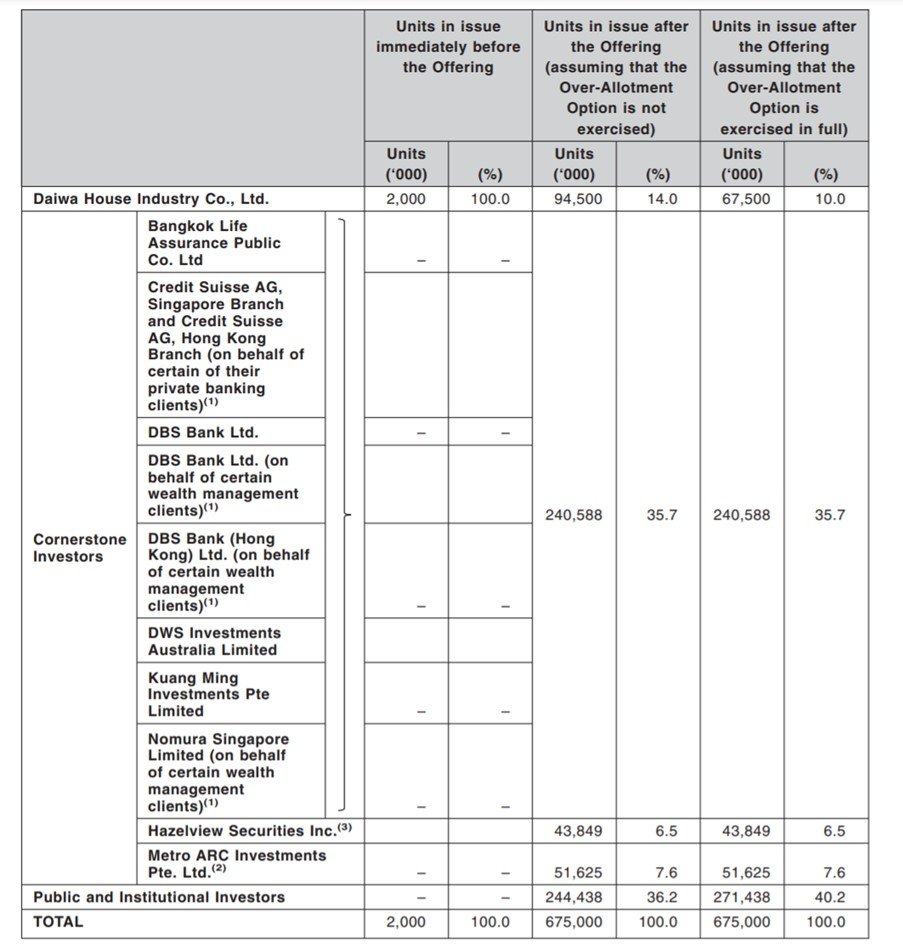

Cornerstone Investors – Daiwa House Logistics Trust

Cornerstone investors are set out below, and they’re mostly private wealth (high net worth individuals).

I suppose it’s a given considering the market cap for Daiwa House Logistics Trust is so small ($540 million).

Yen FX Risk

Because the rental income is in Yen, as Singapore based investors we need to be aware of Yen-SGD FX risk.

SGD has strengthened against the Yen by 15% in the past 18 months, which is a huge drag on earnings.

Yen is a risk off currency, which means that if the market melts down (like in March 2020) the Yen will strengthen significantly. This is because Japanese investors borrow a ton of Yen locally and use it to invest globally (to earn the carry), and in market stress events they sell foreign assets to move back to Japan – strengthening the Yen.

Viewed this way Daiwa House Logistics Trust, with its Japan properties and earnings in Yen could be quite an interesting portfolio diversifier.

You can see the impact on distribution yield if SGD strengthens against the Yen – a 5% SGD move will lead to a 0.3 – 0.4% change in yield.

Will I subscribe for Daiwa House Logistics Trust IPO?

I actually really like Daiwa House Logistics Trust.

Sure, there are some red flags like the Sponsor holding a 10% stake post IPO, cornerstones being primarily private wealth, the small market cap of $540 million etc.

But there’s also a lot to like about Daiwa House Logistics Trust, like the Sponsor injecting the assets at a 11.8% discount to appraised value (don’t forget we looked at the cap rates which are not unreasonable).

The IPO properties are also very new, with a very long WALE, and very decent 6.5% projected yield.

And logistics has a lot of tailwinds behind it with the explosion in eCommerce.

This is Japan too, so the market tends to be very stable. And don’t forget the rock bottom Japanese borrowing costs (10 year JGB at 0.05%) that can further juice yield.

Great REIT for Leverage?

I can actually see a lot of private wealth individuals using Daiwa House Logistics Trust with leverage.

Because these are Japan properties, they tend to be quite stable.

Throw in 30-40% additional leverage on top and you could be looking at 9% – 10% yields.

Public Offering is a puny $20 million

That said, the public offering is a puny $20 million, which looks like it was thrown in more as an afterthought.

Even if you apply, the chances of getting a meaningful allocation are not high.

Might be better to just wait till it starts trading and buy this REIT off the open market.

How to Subscribe for Daiwa House Logistics Trust IPO?

Public Offer closes at 12pm on Wednesday, 24 November.

Sign up is via the usual Internet Banking or ATM or DBS, POSB, OCBC and UOB.

Closing Thoughts: Daiwa House Logistics Trust IPO Review – Worth subscribing for this 6.5% yielding REIT IPO?

I like Daiwa House Logistics Trust.

The 6.5% yield is decent for Japanese properties, the Sponsor is a big name, logistics has a lot of tailwinds right now, and the pipeline is strong. I also like the fact that the Sponsor injected the assets at an 11.8% discount, it shows commitment to the REIT long term.

I don’t like the low Sponsor stake post-IPO, and I don’t like that the cornerstones are dominated by private wealth.

But this is a Japanese Sponsor, and Japanese culture is slightly different, so I’m willing to give them the benefit of doubt.

It’s a 4.5 Horse Rating for me.

That said – I haven’t decided whether I want to subscribe for the IPO.

I like the REIT, but public offer is so small that I suspect I’ll either get a tiny allocation or none at all.

So it may make more sense to just wait until Daiwa House Logistics Trust starts trading and then buying on the open market. This gives me the opportunity to watch how the share price trades on the open market too.

I think 2022 is going to be a massive year for investing, and I do want to keep some powder dry too.

If you’re keen, you can view my full portfolio and stock watch on Patreon, to see how I’m positioned.

But what do I know – I have until Wed to decide.

As always – love to hear what you think!

Daiwa House Logistics Trust IPO – FH Rating

![]()

FH Rating Scale

As always, this article is written on 21 Nov 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Questions

1. Jap properties are mostly freehold but this IPO is not. Did the sponsor change some tenure to leasehold when sold to the reit?

2. You mentioned the age of the properties are 3 years +. Why are half of the properties having short remaining lease if the buildings are so new?

I may have missed something or some info were not shared by the seller?

P/s I didn’t read the prospectus

Yah good points. Maybe it was an existing lease, and then they built a new property on top of it? Don’t know enough about Japan real estate regulations to comment intelligently unfortunately.