So I was reading this article in the Business Times.

It talked about how UOB reported record net interest income this week – and yet share price fell 4.5%.

It then went on to say that analysts continued to hold a “buy recommendation” on UOB stock.

This got me thinking.

Everybody seems to think the banks are a good buy these days.

I mean, interest rates are going up, so banks make more money on their lending. Therefore banks are a good buy right?

When everyone thinks a stock is a good buy…

But if there’s anything I’ve learned from my time in investing – it is that when everyone thinks something is a “good” and “safe” buy, it usually is anything but.

Most of my best investments were made when few thought it was a good idea.

When it made me nervous to the pit of my stomach to pull the buy trigger.

Think oil in April 2020 as prices were going negative, REITs in 2008 and so on.

In fact some of my worst investments are buying what was generally accepted as a “safe” stock.

So I figured – let’s relook the Singapore banks.

Are they still a good investment in this climate? Or is it time to sell?

For discussion’s sake I’ll run the analysis using DBS, but the analysis can be applied to UOB and OCBC as well.

DBS tops out 4 – 8 months before peak interest rates

About a year ago, I wrote an article discussing how to trade DBS bank stock from a business cycle perspective.

This was what I wrote:

“If you look at the 20 year history of DBS, you’ll find that DBS usually tends to top out about 4 – 8 months before the peak in US interest rates.

Red arrow is the cycle top for DBS, and blue arrow is the top in US interest rates.

So if you want to trade DBS stock, you need to watch out very closely for the turning point in US interest rates.”

In plain English – over the past 20 years, DBS bank stock usually peaks about 4 – 8 months before US interest rate cuts.

DBS Stock Price has gone nowhere the past 12 months

If you zoom out a bit more, you’ll find that when I wrote the article last year, DBS share price was at $36.5.

Today it trades at about $34.6 ish, down 5%.

Which means that had you bought DBS last year, you’ll be down 5% capital gains wise.

Throw in the 5% dividend and you’re just about flat on your DBS investment.

In a climate when you can get 4% risk free on a T-Bill.

Man… really makes you think why you’re taking on all the equity risk premium for (instead of just cashing out and putting the money into T-Bills).

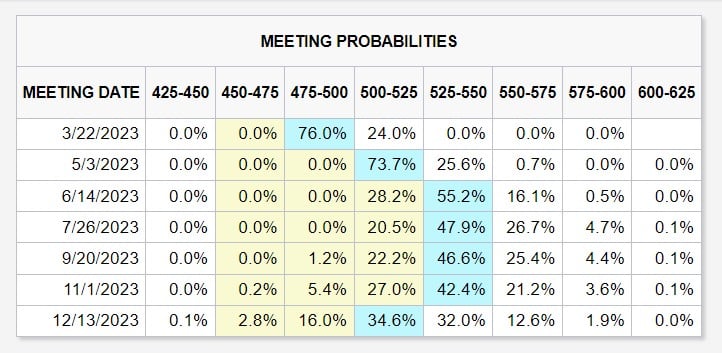

When does the market expect interest rate cuts?

Coming back to the topic at hand.

A couple of weeks ago the market was expecting interest rate cuts in the second half of 2023.

I said then that this was completely unrealistic, and the market seems to have woken up to this reality.

The market now doesn’t expect meaningful rate cuts until early 2024:

If you go by this logic, it would mean that DBS share price would peak around Q2 – Q3 this year (4 – 8 months before US interest rate cuts).

Does that mean you want to sell DBS Bank stock by middle of 2023?

3 key arguments to continue holding DBS Bank Stock

There are 3 key counterarguments I can think of on why you’ll want to hold onto DBS (or bank stocks generally) for longer this cycle:

- Banks earnings are at a record high

- Banks are much stronger this cycle (than 08)

- Inflation means higher rates for longer

But FH… DBS earnings are at a record high

Okay for the record, I absolutely get that DBS earnings are at an all time high.

Likewise for UOB and OCBC.

But c’mon, in a stock as widely followed as DBS – do you really think you can outperform by looking at the financial results?

The financials are fundamentally backward looking in nature.

With a red hot economy and rapidly rising interest rates, nobody is questioning that bank earnings are going to soar to record highs.

If you want to market time with a stock like DBS, it’s all about trying to anticipate the turn in the business cycle.

You’ll want to make a call on whether, in the next 6 – 12 months:

- The Feds are going to be cutting interest rates

- Loan defaults will go up due to a recession

That’s what the game is about if you want to trade DBS stock.

Can the US market serve as an early warning on when to sell Singapore Bank stocks?

For the record, I also pulled up the 2008 charts (brown is US Financial Sector (XLF), candles is DBS).

Takeaway seems that once XLF starts to fall, DBS starts to follow almost immediately.

Likewise for the 2015 and 2018 cycles:

So it seems like you can’t really use the US market as an early warning signal on when to sell Singapore Bank stocks.

No shortcuts here it seems, we need to reason from first principles.

Singapore Banks are much stronger this cycle?

The other argument in favour of holding onto the banks, that I like a lot more.

Is that this is no longer 2008.

After the 2008 fiasco, the banks went through a decade where they cleaned up their balance sheets.

The banks today are rock solid, and won’t crumple like a house of cards in the next recession.

Fair enough.

Let’s run with this argument.

Where is the upside for DBS at this price?

DBS’s book value is $21.4.

At $34.6, it trades at about 1.6x book value.

That’s very richly priced.

JP Morgan in the US is priced at a 1.55x book value for reference, and that’s a world class bank led by Jamie Dimon.

How high can DBS go, if everything plays out perfectly?

The highest that DBS ever went (since listing) was listed was 1.9x book value, which was the 2007 high right before Lehman.

Let’s say DBS goes back there, which is quite an optimistic scenario.

That’s $40, which is about a 20% upside from here (capital gains).

Dividend of DBS (4.85% annualised)

Throw in the annualised dividend of about 4.85% (5.7% if you count the special dividend).

And you’re probably looking at a 25% upside for DBS – if everything goes perfectly, and we go back to 2007’s valuations.

What is the downside for DBS bank stock (if we get a mild recession)?

What about the downside though?

How much are you risking for that potential 25% upside?

In 2008 DBS stock price crashed to 0.6x book value.

In 2020 and 2015 it went to 0.9x book.

Now for the record I absolutely agree that banks are much stronger this cycle (than 2008).

I also don’t think we will see a deep recession like 2008.

Let’s say we have a mild recession, and DBS goes to 1.1x book value

That’s $23.5, about a 30% downside from here.

Throw in the dividend and you’re looking at maybe 25% downside.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Inflation means higher rates for longer

Which brings us to the third point.

Which is more likely in the next 12 months:

- DBS going to 1.9x book value, or

- A mild recession

Where are we in the cycle?

Because of the Fed soft pivot in Jan, it has created a reacceleration in economic growth, which has pushed out the length of this business cycle.

So while this may result in higher interest rates for longer down the road, it also means that interest rate cuts are not imminent here.

Just look at how strong the jobs market and consumer spending are.

Which means you could probably hold onto the banks for a little while more, if you really wanted to time it to perfection.

But as to whether you’ll see DBS go to 1.9x book value ($40).

Frankly that’s quite an aggressive price target.

You could argue that if we have strong economic growth DBS can continue to grow its loan book, so the share price growth can come from organic growth rather than multiple expansion.

This is possible too, and worth discussing.

Does Inflation change the analysis above?

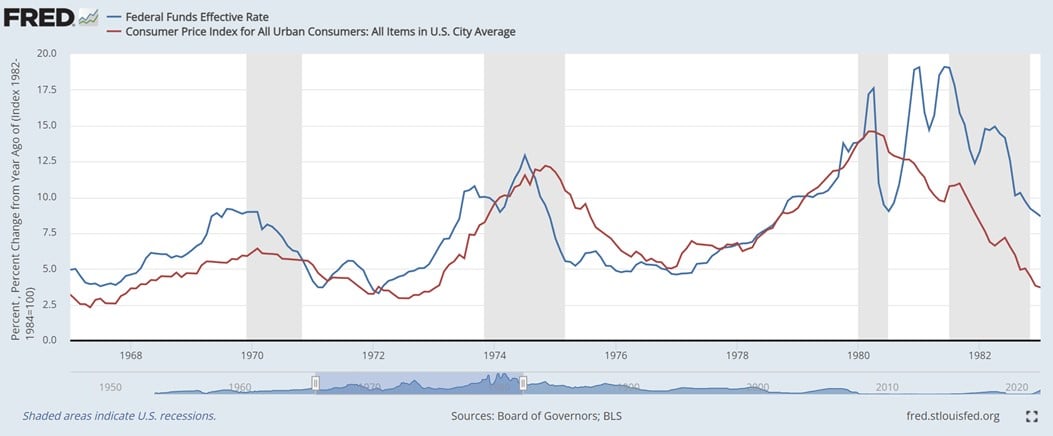

This cycle is unlike every other business cycle the past 40 years.

The main reason – inflation is a key limiting constraint.

Inflation was not a problem the past 40 years, so the solution to every recession was to cut interest rates.

This time around, inflation is a very real problem.

So the ability of the Feds to cut interest rates in a recession is affected.

Which means that you can’t analyse this like a “normal” business cycle from the past 40 years any more.

More reasoning from first principles is required.

How will inflation affect bank’s stock prices in the next recession?

The last time inflation was a problem was the 1970s in the US.

That’s really far back.

We can also take guidance from the Emerging Market banking sectors, which are used to central banks raising interest rates to combat inflation.

The key lesson, seems to be that:

- High inflation means higher interest rates (to combat inflation)

- Higher interest rates are good for banks… up to a certain point (when it triggers a big recession)

There is a sweet spot for interest rates for the banks.

High enough that they make good money on their lending.

Not high enough that it sends the economy into a tailspin, where you get a recession and loan defaults.

So the lesson in the 1970s, is that inflation was good for the banks at first, as the higher interest rates boosted their net interest income.

But as inflation refused to go away, the Feds kept raising interest rates higher and higher in successive cycles.

Until at some point borrowers started to fail across the board, leading to widespread bank failures.

So again, it comes back to timing.

Banks can do well with high inflation, but you want to be very careful on timing, and not hold on for too long.

You want to sell before the rate cuts or the cycle turns.

Will I sell DBS Bank stock (or buy more)?

Full disclosure that I hold positions in both DBS Bank and UOB Bank.

I have taken profit in some of my DBS Bank and UOB positions late last year, but I do still hold quite significant positions in both.

Timing wise it looks like we won’t see a recession or rate cuts in 2023.

So if you really wanted to min-max timing, you could probably still hold for now.

But looking at the discussion above, I just find it hard to see myself pulling the trigger and buying a lot more bank stocks at these prices.

Best case you’re looking at maybe 25% upside at these levels.

But no denying that we are approaching the later stages of the rate hike cycle / business cycle.

If we get a mild recession you’re looking at maybe 25% downside.

If we get a bad recession maybe even bigger downside.

So FH… what are you going to do?

I’ll probably hold onto my bank positions for now.

But as 2023 plays out, I may trim my positions further depending on how the business and rate hike cycle plays out.

Patreons will get updated macro views from me as and when I do, so do sign up if you are keen. I share premium macro updates just like this one on a weekly basis to share my latest positioning.

Like I said, the best investments make me uncomfortable.

They make me sick to the stomach when I think about buying.

DBS today, just seems like a “safe” play.

You’re risking 25% downside, for 25% upside.

That’s not the kind of asymmetric bets I like to make, where you risk 25% downside for 100% upside.

Buying DBS today, isn’t like buying DBS in March 2020 anymore.

The upside seems very much limited, while the downside can very easily materialise.

And at 1.6x book value, I’m not sure whether the risk-reward makes sense, as we approach the later stages of this Fed hiking cycle.

But let’s see.

Closing Thoughts: Really goes back to individual investment strategy

That said I know many out there who use DBS as a portfolio hedge, or as a long term buy and hold.

Just to be clear, this article is not meant for those investors.

If you’re buying DBS to hedge your tech / REITs against a rapid move higher in interest rates, as part of a broader portfolio strategy.

Or if you’re one of those whose average price in DBS is $13 and you plan to DCA for the next 20 years.

Please don’t let me stop you.

This article is written more from an active timing approach.

An intellectual exercise if you like, for me to think out loud on whether I want to continue holding my Singapore bank positions, or to lock in a profit.

As always, this article is written on 24 Feb 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

That’s true, when everyone starts thinking this is a sure win thing… indeed, the story changes but the tune does rhyme

I bought during March 2020, thanks for the intellectual exercise, will ponder if I should and when to sell this

Pretty much the point of this article!

Not saying to sell it now, but to get readers thinking about whether it still makes sense to hold, or at what price (or point in this hiking cycle) would it make sense to start locking in profits.

Certain investors may just decide to hold long term through the next business cycle, which is perfectly fine too!

Dear FH

Very good analysis and fully agree.

For a SG-focused long term investor with dividends as a key point, it is a no-brainer. Hold and add progressively with each market correction/individual pullback. There are no better alternatives with selling even at 40$! Where can they deploy the proceeds without re-investment risk (in case they for fixed income) or re-entry risk, if they stay in cash?

Theoretically, you can sell at 36-40$ and redeploy in good quality REITS. But this will involve not only taking a big risk as you are betting that rates will fall and REITS will go higher but also only for an additional circa 2% higher yield. I would not go down that route and rather prefer to hold and create a natural hedge buying select REITS as I have posted before.

Unless there is a bad deep recession with stagflation, if banks fall due to rates going down, REITS will save the day and vice versa.

One of them and rather both will bring the bacon home!

I bought UOB after the drop last week post-results and will be buying both DBS and OCBC progressively at 34$ and 12.50$ respectively gradually- Nibble first and buy more if they fall

This needs a disciplined plan and conviction to stick to the plan.

As regards trading, IMHO the SG market is not great. Still can do it and I have done minimal buying selling of the banks in the past for Kopi money! For big whales who can afford to buy say 1000 shares or more at one go, they can do this better. Sadly most of us here responding, I presume, are not in that category! I may be off the mark here but would like to stand corrected though

Regards

Garudadri

Hi Garudadri,

Great comment and agree with you.

Not sure if we will see a deep recession at this point, and even if we do, how long before governments start whipping out the fiscal stimulus playbook again (very hard to put the genie back into the bottle now that they have discovered the power of handouts)!

I’m inclined to think that we may see some variant of the 1970s, where inflation picks up, Feds tighten, inflation drops, Feds loosen playing out to some extent in the mid term.

Whether that is tradeable using the Singapore banks is actually a good point that you raise, the SG market does tend to be less volatile with more buy and hold investors. So even if one is inclined to trade this, there may be better instruments out there!

I can see the appeal of the portfolio you are running, with a mix of high quality REITs and banks. 😉

Last year, 20 Feb, you did a write up in which you also talked about selling within the quarter. I responded saying my own plan was quite similar to yours. And I did sell some. I also said that DBS may caress the $10billion dollar profit mark. The CEO recently said it may in FY23. In the months following my selling, and especially last week, I added to my holdings and now actually has more shares than this time last year! A very short term attraction to me is that within the next 2.5 months, the 4QFY 22 and 1QFY23 dividends will total at least $1.28 a share. And in the last few days, the case for more hikes in rate this year in the US has strengthened. I am therefore not planning to reduce yet.

Thanks, very much appreciate the sharing, good to follow up a year on.

Just to share what I did – I didn’t sell that quarter in the end, because it looked like the rate hike cycle would continue to play out. I did eventually sell a bit by end of 2022 though.

Position wise, I am definitely holding less DBS/UOB today than I did last year (still retaining well over half of my bank positions)!

Agree that dividend looks good if you count the special dividend (almost 5.7% yield).

What does concern me slightly is that with the cyclicals they always look the best right before the cycle turns.

Again, not saying to sell now, but at some point this cycle the Feds will start to slow the pace of hikes, and the risk-reward may shift towards rate cuts instead of hikes. Agree that we’re probably not there yet given how hot the economy is running, but if the Feds are serious about combating inflation, we will get there eventually.

I just love your analysis. I am a silent follower. My one liner the bank’s wealth management business is not doing well, you can’t reward stock price depending on the interest rate margin. The bank pays nothing much on deposits, I put out as much as I can on OCBC 8 months 4.18% pa (THANKS OCBC). I would wait for that 30% crash!

Thank you, truly appreciate the kind words and support! 🙂

DBS (and POSB) have so much funds at their disposal that I suppose they don’t see a need to attract new funds via FD!