DBS Bank needs no introduction.

Every true-blue Singaporean will recognize the DBS and POSB logo instantly.

I’ve had a lot of requests to do an analysis on DBS Bank, so here goes!

What is DBS Bank?

DBS Bank was originally known as the Development Bank of Singapore. It was created by the Singapore government in 1968 to finance industrial activities in Singapore.

But that was a long time ago.

Along the way DBS acquired POSB bank, and today it’s the largest bank in South East Asia by assets.

DBS’s 5-year chart is set out below, and it’s down about 30% from its cycle highs of $30.

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance. You can learn more in my review on ShareInvestor Webpro here.

Short term outlook for DBS

Short term, there are 2 main problems that worry me about DBS (or an investment in banks):

1. Falling net interest income (NII)

The core business model of a bank, is to borrow money at x%, and lend it out at y%. The difference between x and y, is the profit for the bank.

A bank like DBS is able to access money very cheaply because all the mom and pop in Singapore put their savings at DBS or POSB.

So when interest rates are high, DBS makes a lot of money because they borrow cheap, and lend it out at expensive rates.

Well, interest rates are rock bottom now, and likely to stay that way for a while.

This is bad for DBS, because the rates they lend out at have dropped. So less profits for DBS.

2. Rising Non-Performing loans (NPL)

Basically, bad loans. COVID19 causes companies to go bankrupt, the company cannot repay DBS, and DBS loses money.

It’s as simple as that.

Earnings

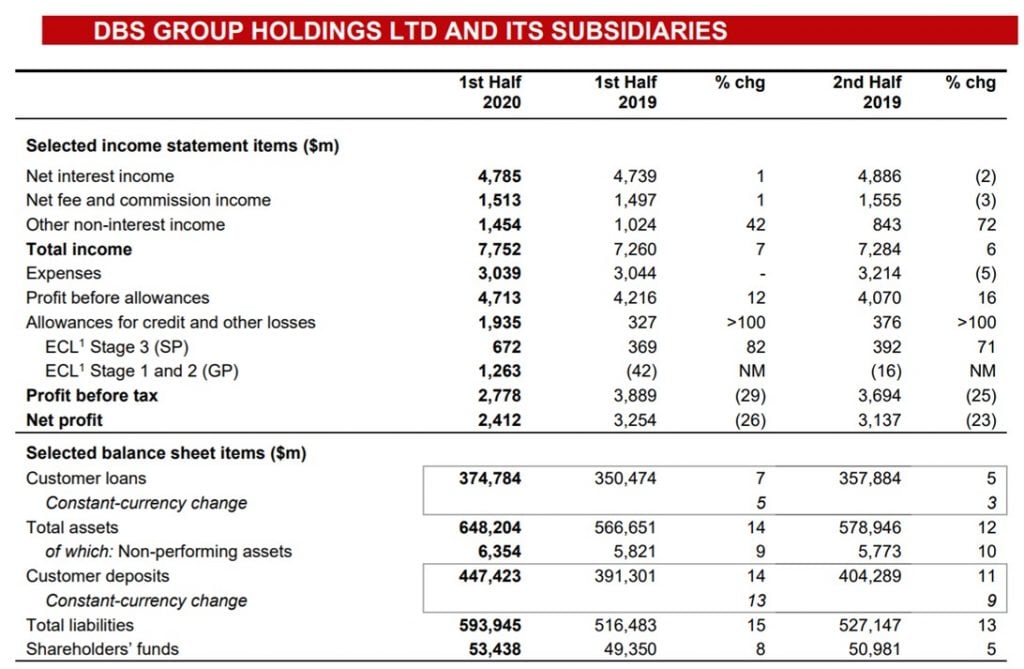

Let’s dive straight into DBS’s Q2 earnings. It’s a lot to digest, so I’m just going to break it down into 3 big points:

- Net interest income is flat

- Fee income is flat

- Bad loan provisions are up massively

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

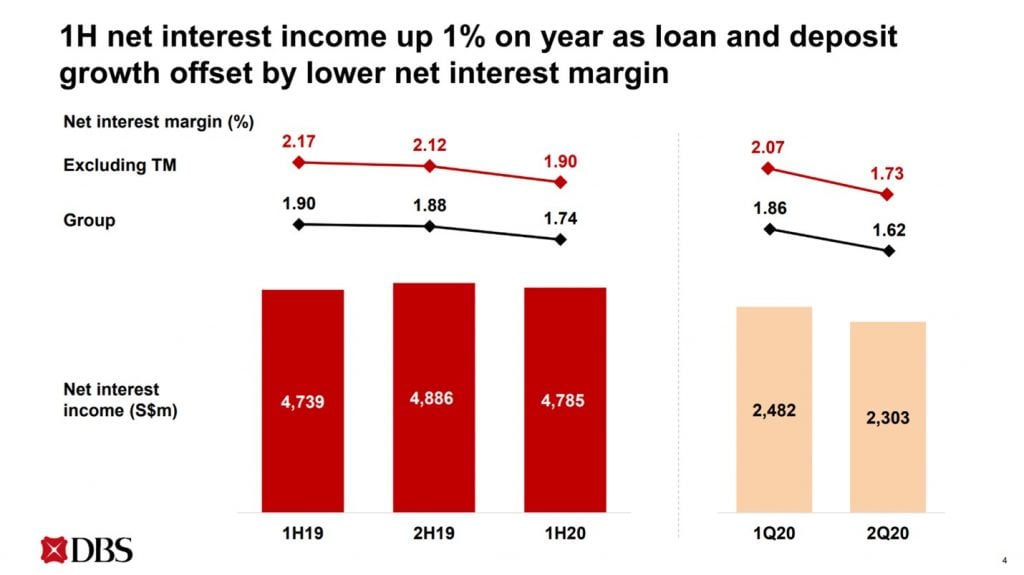

1. Net interest income is flat

Why is DBS still able to have a 1% rise in net interest income compared to 2019, when interest rates have dropped so much?

The simple answer – is that while interest rates have gone down, loan volume has gone up. The bank makes less per loan, but there are more loans than 2019, so the overall earnings are flattish.

This is a good thing.

That said, as this crisis wears on, more and more borrowers are going to refinance their loans, and they’ll start enjoying lower interest rates – so less earnings for DBS.

But at the same time, DBS has already dropped the interest rates they pay on their savings accounts like DBS Multiplier, so they can borrow more cheaply.

That should help, but it probably won’t make up for the fall in interest rates.

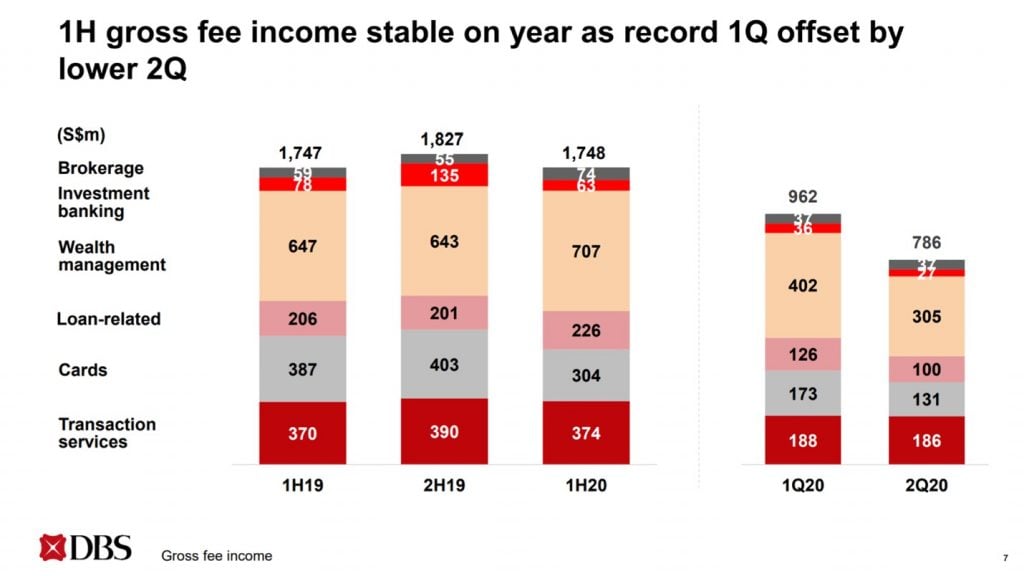

2. Fee income is flat

Fee income is holding up really well. Credit card spending is down by quite a bit because of reduced spending, but wealth management is holding up well. Lots of clients are investing it seems.

3. Bad loan provisions are up massively

Remember the bad loans we talked about?

So DBS recognizes as such, and they’ve set aside $1.26 billion to cover for loan loss provisions.

But – This is where it gets a bit tricky.

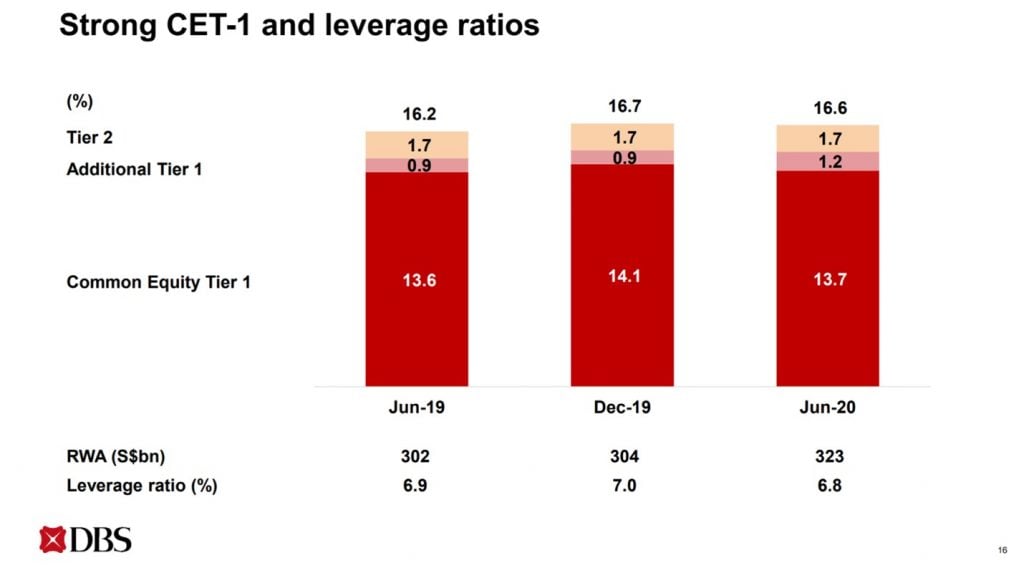

Balance sheet is really strong

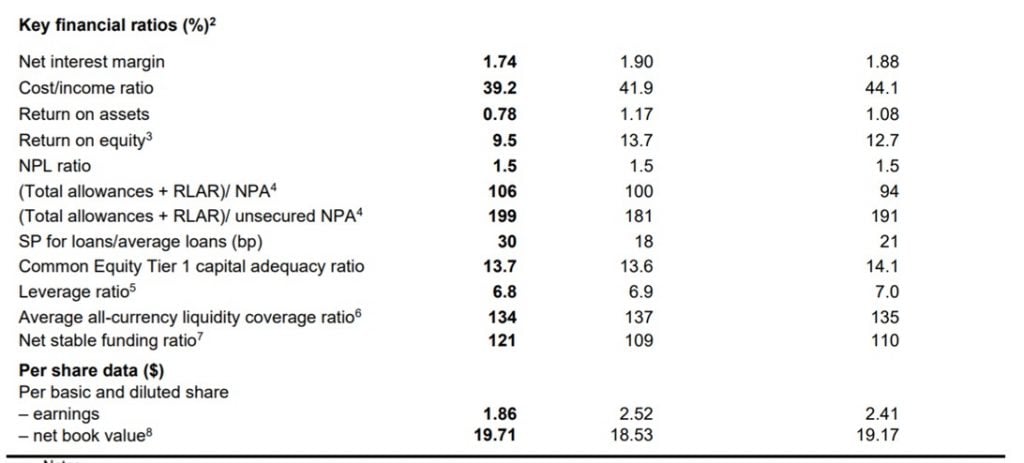

Common Equity Tier 1 (CET1) basically measures the amount of safe, Tier 1 capital the bank has. The minimum required CET1 ratio by 2019 is 4.5%.

DBS has 13.7%.

So balance sheet wise, DBS looks rock solid, a complete opposite of the 2008 crisis.

“But FH, the government has been keeping the zombie companies afloat”

The difference with this COVID crisis, is that the amount of fiscal stimulus has been unprecedented, this early into the crisis.

In 2008 and in 1997, the government let the market crash, and people started going bankrupt and losing houses, before the bailouts came.

This time around, the moment the crisis hit, the fiscal stimulus and bailouts came. So the government paid salaries, they gave businesses free rent, they allowed loans to be deferred until 2021.

And the impact was massive.

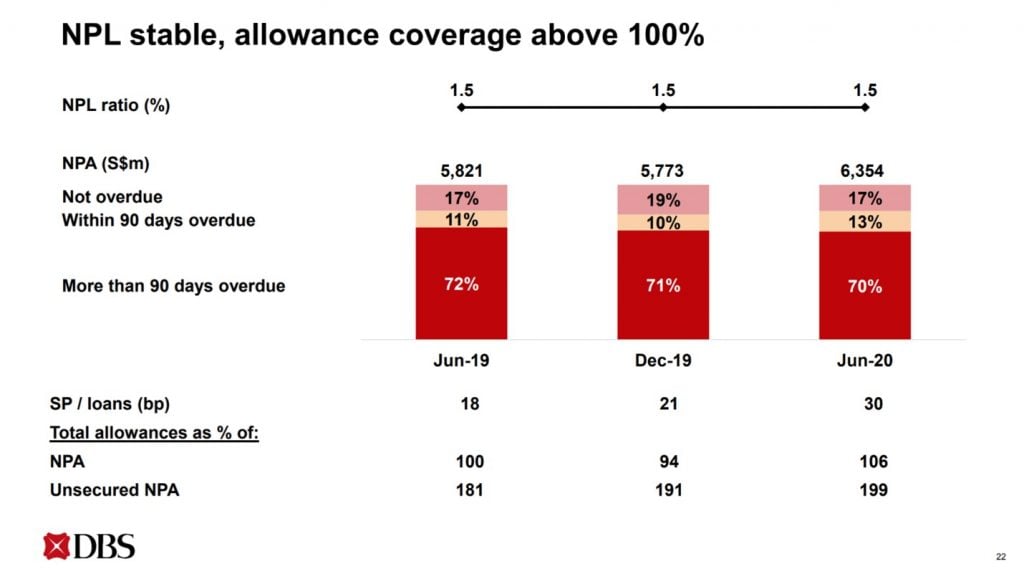

We’re in the worst recession since WWII, and DBS’s non-performing loan rate is flat at 1.5%, exactly where it was a year ago.

Looking at the chart below, you’ll never know COVID-19 never even happened.

What happens next for banks?

So if you are in trouble because of COVID, back in April you could apply to the bank to have your loans deferred until 2021. So you didn’t have to pay a single cent on the loan until 2021. Crazy stuff.

But we’re nearing 2021 soon, so the million dollar question is – what happens when all these loan moratoriums fall off?

Do these borrowers have the money to pay, or do they default?

Some numbers

5% of DBS’s loan book is under moratorium. OCBC and UOB have 10% and 16% respectively.

And of this 5%, about 70% is SME loans, and 30% is consumer loans. And within SME loans, about 90% is secured mostly against property and LTV is generally below 70%.

Long story short – even if the SME loans go bad, DBS can still take the property as collateral, and Singapore property tends to be pretty stable.

So DBS seems pretty safe, and at first glance, the loan allowances look overly aggressive.

Too good to be true?

So we’re in the worst recession since WWII, but DBS’s income and balance sheet are rock solid, and bad loan allowances looks overly aggressive.

What’s the catch? If this were true, DBS’s share price would be 20% higher already.

I think the catch here, is that no one knows how long this crisis is going to last.

It’s the exact same thing with the Great Depression, that lasted from 1929 to 1933.

At the start of the crisis in 1929, banks, just like right now, had fortress balance sheets. They looked like fantastic investments.

But as the crisis wore on, business got worse and worse, and more companies started defaulting. And by 1932, banks were failing one after another.

The key here is going to be: (1) how long COVID will last, and (2) how much fiscal support do we get from the government.

So if you can tell me that COVID19 will go away in 2021 and governments pump in a ton of stimulus, I think DBS is an unbelievable buy now.

But if COVID drags on longer, and we don’t get big fiscal stimulus, then all bets are off.

What do I think?

Personally, I’m not super optimistic in the short to mid term. I think this recession will last longer than expected, and I think there’s a real possibility of a double dip recession.

I think the real effects of this recession haven’t been felt yet because of all the temporary stimulus measures.

The only saving grace would be fiscal stimulus, but I’m concerned that politics will get in the way. I’m also concerned that countries will start to run out of firepower soon, because of all the record measures passed early this year.

There’s only one country in the world that can do unlimited stimulus, and that’s the US because of their reserve currency.

Long Term Outlook for DBS

But that’s the short term.

Longer term though, I’m pretty bullish on banks.

I’ve mentioned many times that I think the only realistic way out of this crisis is via inflation.

And inflationary conditions are usually good for banks.

The closest analogy will be the 1940s period, where US interest rates stayed at zero for almost ten years.

As inflation started to go up, more and more people wanted to take up loans to start a business or buy houses. With inflation, the amount you owe the bank stays the same, but the amount you make every year from your business or your property goes up. Borrowing from the bank becomes a no brainer.

So longer term, I think economic activity will eventually pick up when COVID goes away, and I think Singapore will bounce back. And banks will play a key part in that eventual recovery.

Rise of the Digital Banks

A potential wildcard, is the rise of digital banks.

MAS has delayed the licensing, but at some point it will happen.

And the potential players includes really big names like Grab, Singtel, SEA, Bytedance, Ping An etc.

Longer term, how would this impact DBS?

Personally I think it’s too early to say for certain. We don’t even know the strategies that these new digital banks will employ.

But I don’t expect the banks to be decimated as badly as they were in China, with the rise of WeChat and Alipay.

I think in Singapore, the banks have far more resources to defend against such an attack, and they also have the case study of China to learn what happens to a bank when you let digital players get between you and your client.

Jamie Dimon had a good quote on this. He told a story of how 5 years ago Fintech CEOs were telling him how they would kill JP Morgan and disrupt the whole industry. But 5 years later, all of them were keen to discuss partnerships with JP Morgan instead.

As it turns out, the finance sector, with all its regulations and entrenched players, is not as easily disrupted as it would appear.

So while I think Digital Banks will steal some clients, I suspect it will eventually settle into an equilibrium where digital banks have their own niche, while banks like DBS continue to remain relevant.

We’ll see though. Big wildcard here.

Valuations of DBS Bank

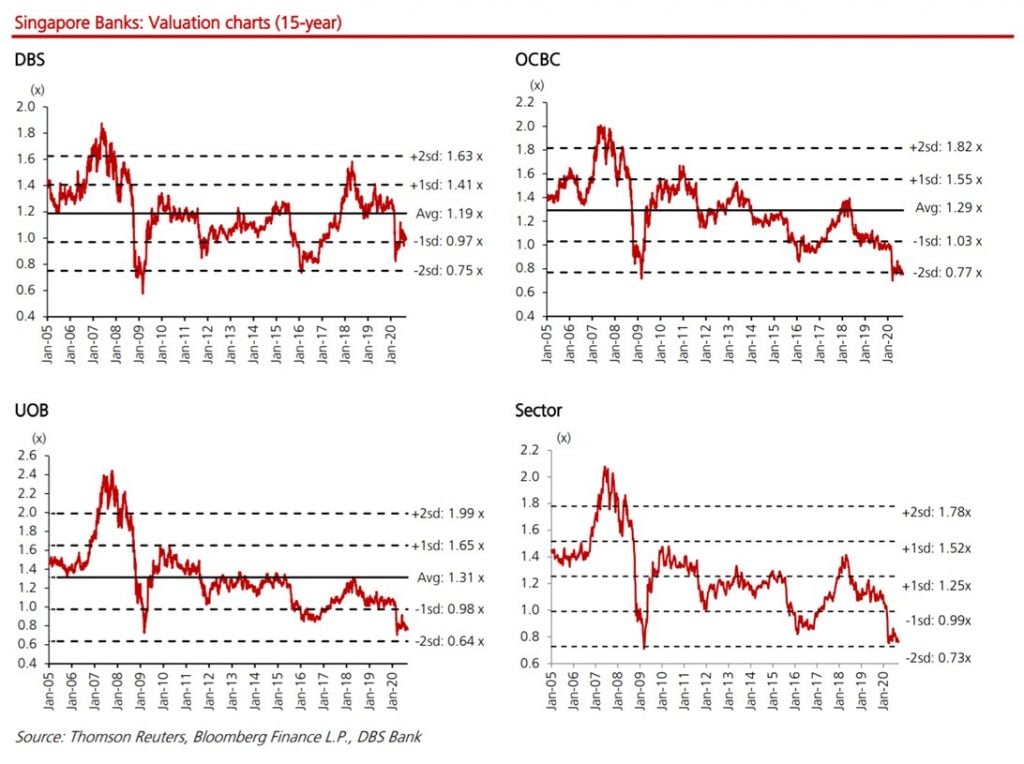

At $20.34 today, DBS trades at about 1.03x book value.

I’ve set out the long term valuations for all 3 banks below.

DBS’s book value of about 1.0x today is 1 standard deviation below its average. So it’s cheap, but not as cheap at it was in 2008 (which was a financial crisis). But pretty close to 2012 and 2016 lows.

OCBC and UOB are significantly cheaper on a valuations basis because they are higher risk. OCBC has bigger exposure to Hong Kong (we all know how that turned out), while UOB has bigger exposure to Singapore corporates (the non-GLC ones).

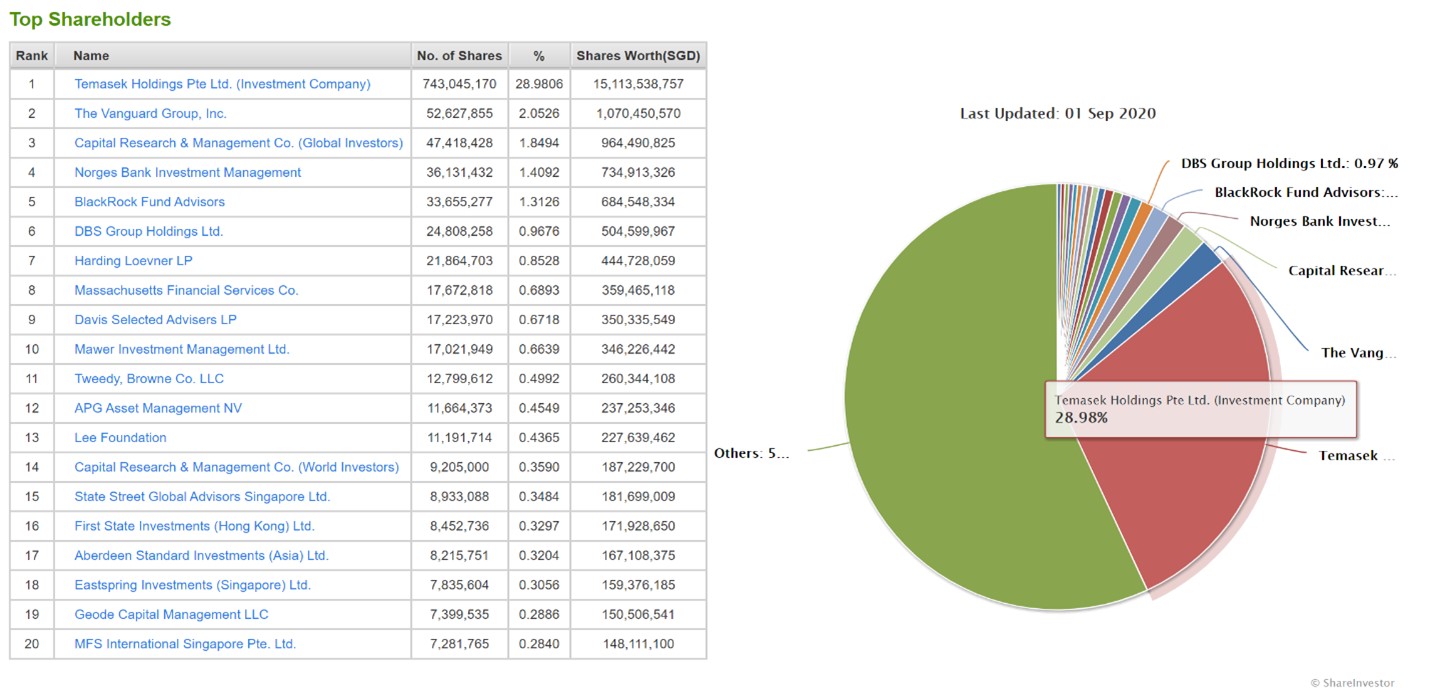

Shareholders

Temasek holds 29% of DBS Bank.

I think that’s pretty self-explanatory, this is another GLC just like CapitaLand and SIA.

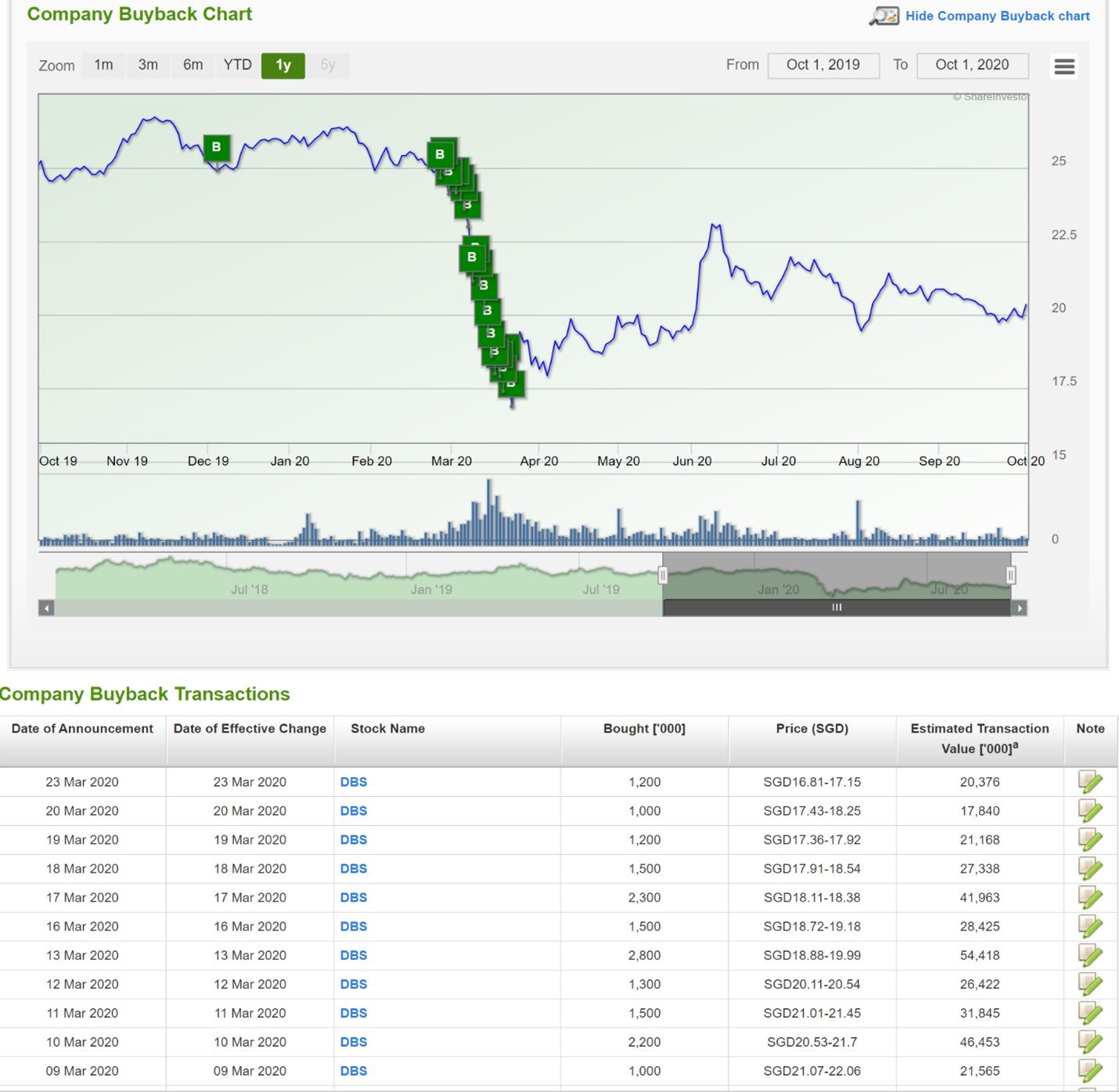

Share Buybacks

Share buybacks is really interesting.

Basically, DBS was buying their own shares all the way down during the March crash.

I won’t try to second guess why they did it, but with the kind of earnings they’re pulling in, and the kind of balance sheet they have, I can see why they would want to buy every single share they can at this price.

After the caps from MAS, dividends and buybacks are going to be limited for the near future though.

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one. If you do such analysis regularly, well worth checking it out. Our review on WebPro (and Promo Code) here.

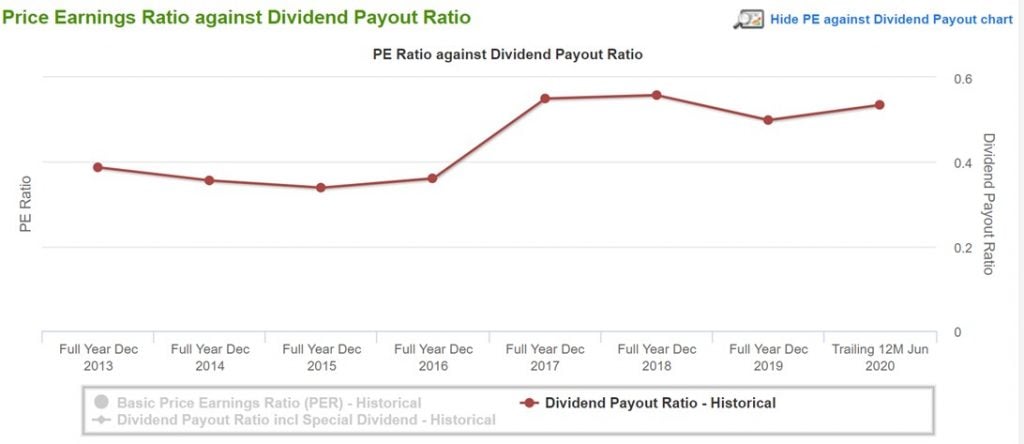

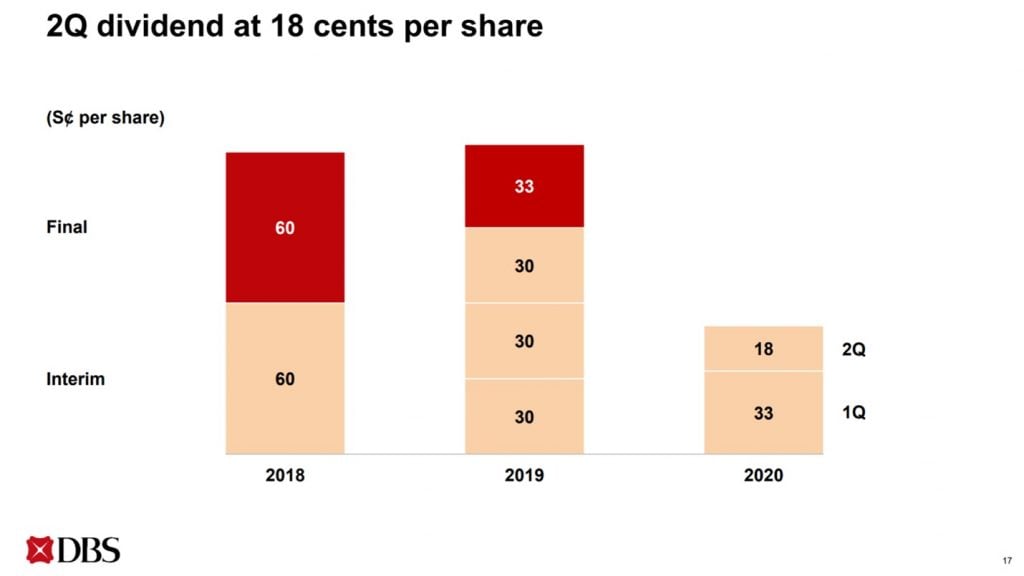

Dividend

Dividend payout ratio is also a very healthy 50%.

However, MAS has announced that it will cap the amount of dividends banks can pay out at 60% of FY2019 dividends.

This would drop payout ratio to a very sustainable 33% on a trailing twelve-month basis.

At today’s price of $20.34, that dividend works out to a 3.5% yield.

Decent, but not the 6% it was pre-MAS cap.

Technically this cap on dividends will fall away in 2021, but I think there’s a decent chance that MAS will extend it because of how COVID is playing out.

DBS Research seems to agree:

The Monetary Authority of Singapore’s call to cap FY20 dividends at 60% of FY19’s was predicated on shoring up capital amid the uncertain economic climate. As of 2Q20, CET1 ratios for DBS/OCBC/UOB stood at 13.7%/14.2%/14.0%, which are strong. In our opinion, lower net interest income, coupled with relatively soft credit demand and asset quality uncertainty, opens the possibility of extension of dividend cap into FY21F from a prudent standpoint, given continued uncertainty amidst the pandemic and uneven recovery paths across countries, regions and industries.

What is DBS Bank’s competitive advantage?

I was talking to a famous Asian investor recently, and he offered me this bit of advice: Before investing, always yourself – what is the company’s competitive advantage?

So what is DBS’s competitive advantage?

The way I see it, it is the cheap cost of financing. This comes from being the retail bank where most Singaporeans save their money, and from the Temasek backing. A cheap cost of funds allows them to lend cheaply and still make money, and the Temasek backing means they never need to fear running out of cash.

One could also argue that it is having a banking license in a highly regulated and profitable market like Singapore. I don’t disagree.

The entry of digital banks will encroach on this somewhat, but the lesson from the US and Europe seems to be that when you already have established banks, it’s very hard for fintech players to disrupt because of all the regulation. We’ll see though, I’m happy to be proven wrong on this one.

Closing Thoughts: Would I buy DBS at $20?

We’ve done a number of reviews on GLCs like SATS, SIA, Keppel and Singtel recently.

And I must say DBS has been an absolute breath of fresh air.

For once, we get to look at a player with a real competitive advantage, which is dominant in its industry, and with sound economic moats.

Valuations wise, it’s also very cheap on a historical basis.

The biggest wildcard here is COVID. If COVID drags on longer than expected, we absolutely need to see continued fiscal support or the insolvencies will start going up. If so, things can get hairy real quick.

I like DBS a lot, but at the end of the day, there still is some tail risk here, and DBS isn’t a slam dunk investment. I still think averaging in makes sense from a risk management perspective, simply because we don’t know how COVID and how the fiscal stimulus plays out. This crisis may last 6 months, or it may last 2 years. Nobody knows.

Because of that, I’ll give DBS a 3.75 horse rating.

At $18 or $19 it’s probably a 4 horse, but at $20 it’s slightly below a 4 horse for me.

Full disclosure – I have a decently sized position in DBS, and I’ve been averaging in consistently since late March.

As always, this article is written on 2 Oct 2020 and will not be updated going foward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

I would love to hear what you think though. Would you buy DBS at $20?

Share your comments below!

DBS Bank – FH Rating

![]()

FH Rating Scale

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hello,

Great article as usual. Great if you can consider adding in a small section to compare DBS against UOB and OCBC listing briefly each pros and cons and give your horse rating on these 2 bank as well.

Thank you

Ok, I might do a separate article for UOB / OCBC. 🙂

Probably need to factor in that DBS has a competent CEO.

True, that’s a good point. Just like Jamie Dimon at JPM.