DBS Group Holdings Ltd (D05.SI), is South East Asia’s largest bank, and one that needs no introduction to any Singaporean. This is the bank we grew up with, one that we all have an account with. I grew up with a POSB savers account (using my thumbprint), so this bank holds a special place in my heart.

As at 29 March 2018, DBS’s share is trading at S$27.50, implying a forward yield of 4.36%, higher than its ever been outside of recessionary conditions.

Does this make DBS Bank Ltd a buy? Is DBS a good investment at this price? Is DBS a better buy than its peers, Oversea-Chinese Banking Corporation Limited (OCBC, O39.SI) or United Overseas Bank Limited (UOB, U11.SI)? Why is its forward dividend yield so high when compared to OCBC and UOB?

Given the ubiquity of DBS, I expected a plethora of articles discussing the above questions, but was taken aback to find that there are none. I am going to attempt to answer these questions, and I hope that fellow financial bloggers will join the discussion on this quintessential Singapore stock.

I will split this article into 2 parts, a macro-view focusing on the global macroeconomic conditions and a micro-view focusing specifically on DBS.

Basics: DBS Bank Ltd

Wikipedia summarises DBS quite aptly: “The bank was set up by the Government of Singapore in July 1968 to take over the industrial financing activities from the Economic Development Board. Today, its branches numbering more than 100 can be found island-wide. DBS Bank is the largest bank in South East Asia by assets and among the larger banks in Asia, with total assets of S$482 billion as at 31 Dec 2016. It has market-dominant positions in consumer banking, treasury and markets, asset management, securities brokerage, equity and debt fund-raising in Singapore and Hong Kong.”

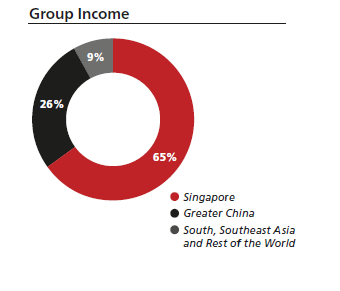

DBS’s group income is primarily derived from Singapore, with Greater China the next largest market.

Source: DBS FY2017 Annual Report

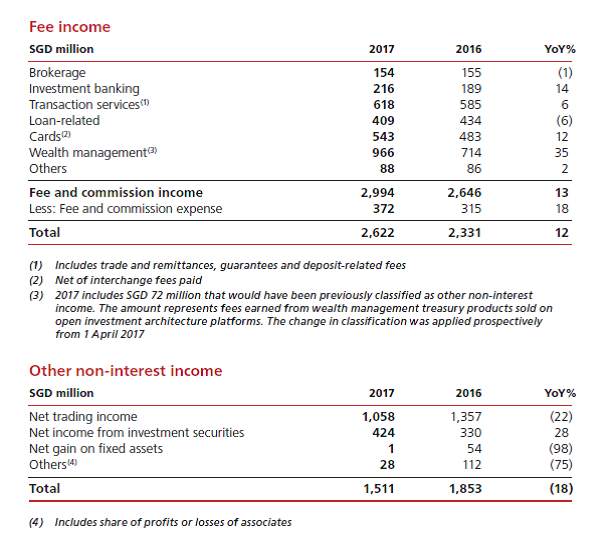

DBS’s income is primarily derived from interest income, with secondary sources being fee income (Eg. brokerage, investment banking, wealth management, card services), other non-interest income (Eg. trading income, investments)

Source: DBS FY2017 Annual Report

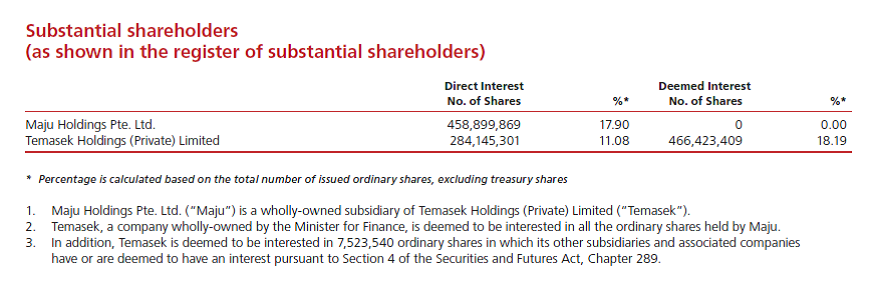

Temasek Holdings (Private) Limited, holds 18.19% of DBS. Given the systematic importance of DBS Bank to the Singapore economy, I find it unlikely that DBS will ever be allowed to go under.

Source: DBS FY2017 Annual Report

Macro View

- Economic Cycle

Bank stocks, including DBS, are highly cyclical in nature. As evident from the 20 year DBS chart, the stock trades in boom and bust cycles, in line with the global economy. It plunged in 2001 following the Dot-Com boom, in 2008 after the Great Financial Crisis, in 2012 with the Euro Sovereign Debt Crisis, and in 2015 with the China devaluation of the RMB.

This will not change going forward. If anything, the 5 year chart of DBS looks really scary to me, as it has had an astounding run-up from about 18 dollars in 2017 to 27 dollars currently, which may imply a turn in the economic cycle.

Source: Yahoo Finance

Given how closely DBS is tied to the financial cycle, we need to understand which stage of the economic cycle we are in. There is little point looking at the Singapore market in isolation, as Singapore is an open market that is huge affected by the global financial conditions.

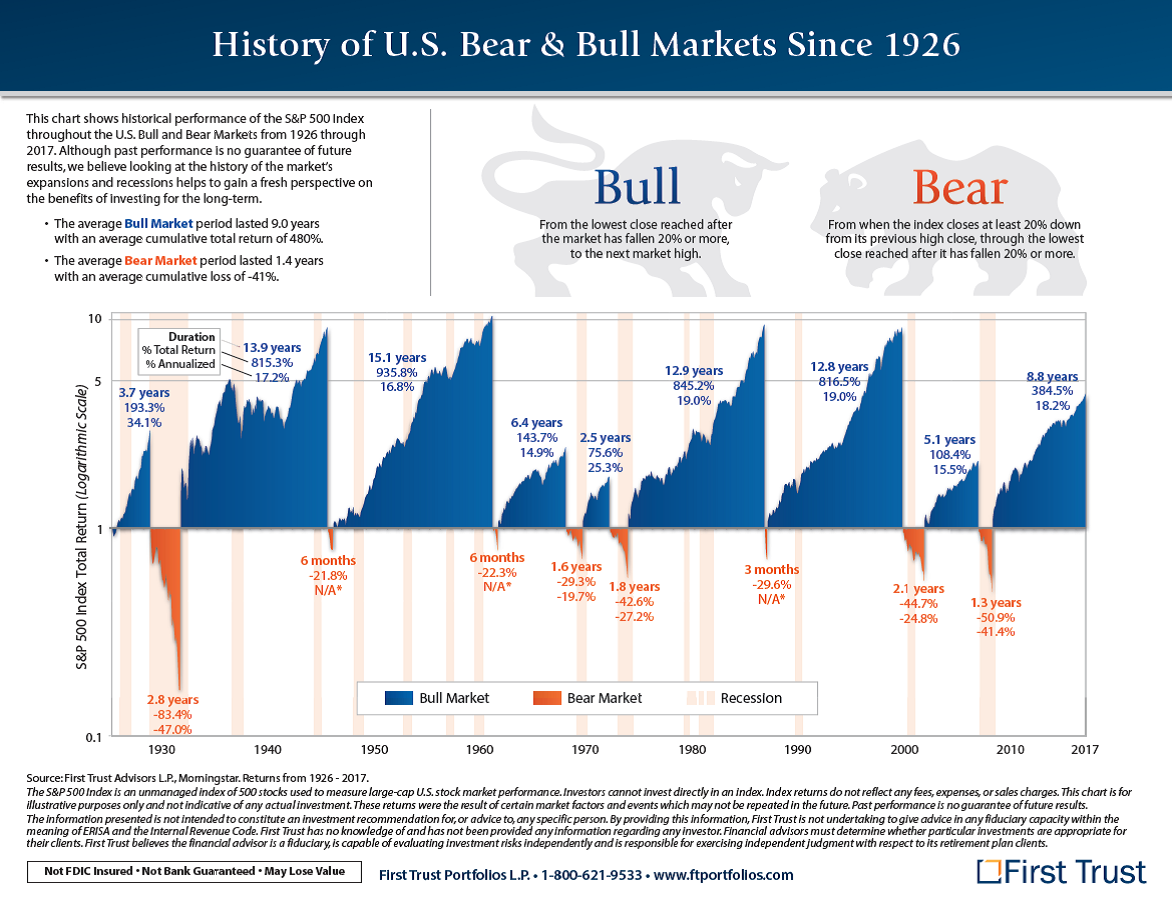

Let’s look at the US market first. Given that 2008 was the last recorded recession or bear market, we’ve basically had a 10 year bull run. The average bull market lasts 9.0 years, so we are beyond the average length at this stage, but we are by no means the longest bull market in history (15.1 years).

Source: First Trust

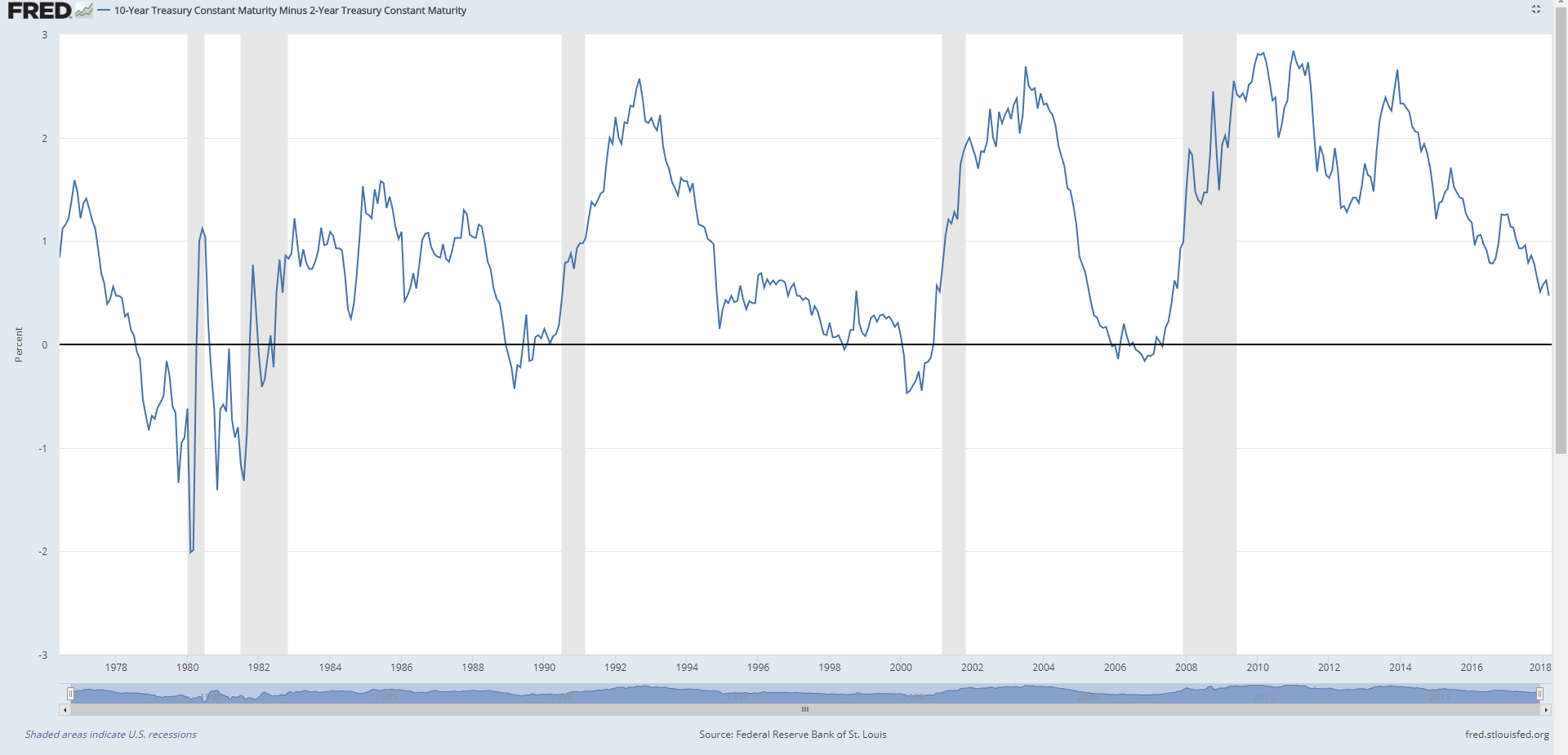

The USD Treasury 10 year minus 2 year yield curve is used as a leading indicator for US recessions, as it has inverted before every single recession in recent history. The yield curve has not inverted yet (inverts when it goes below zero), although it looks like it is getting there, especially with Jerome Powell’s Fed on a path towards higher interest rates. However, given that the yield curve provides approximately 9 to 12 months indicator of a recession, there is no need to forecast the forecast, or attempt to predict when the yield curve inverts. When it inverts, I will need to reevaluate my equity positions.

Source: St Louis Fed

The next market we need to consider is China. China has had an astounding growth since 2008, and it is now the second largest economy in the world. Most of us in Singapore now deal with China clients and China companies on a day to day basis, and there is no getting around the fact that the health of Singapore’s economy is deeply intertwined with China. The greatest tail risk with China, as it has been for the past 20 years, is their bad debt situation. The recent issues with Anbang Insurance, HNA, Dalian Wanda, indicate that Mr. Xi Jinping is serious about clamping down on bad debt. What this bodes for the Chinese economy though, is anyone’s guess. Pundits have been forecasting a China crash from their bad debts every since the 1990s, and every single one of them have been proven incorrect thus far.

My personal take is that Xi Jinping’s consolidation of power is good for China, as it allows him to more effectively tackle the bad debt situation. I will continue to observe the situation with much interest, but I remain optimistic about their ability to address bad debt while maintaining a balance with corporate growth.

The global economy may therefore be more robust than what pundits would say.

Micro view

- Dividend Yield – 4.36% forward yield

On the Q4 2017 financial results call, Mr Piyush Gupta (DBS CEO) announced that DBS will be paying a S$1.20 dividend going forward. His justification is important enough to be reproduced in verbatim below (emphasis mine):

“Next, just a quick comment on capital and dividends – Sok Hui talked about the overall Basel rule finalisation and impact on us. I had [thought] we might have an impact of maybe up to 10% on RWA. As the way the rules have come out, the impact [on us] is only 5%. This is much lower than the European banks. My estimate is most European banks would see an impact of 30-50% on RWA. We will see some impact from the standardised approach to calculating counterparty credit risk and from the fundamental review of the trading book – those are the two areas we will see some impact. The standardised floors have no impact on us at all.

We had a 14.3% transitional CET-1 at the end of the year and 13.9% fully phased-in. I’ve guided before that we’re comfortable at around the 13% range – it could be plus minus 0.5% points – which means we have surplus capital. As I had said before, as soon as we get clarity on the Basel reforms we can be more efficient with our capital usage.

So we did three things. One, we bumped up the annual dividend to $1.20 per share. That gives you a pay-out ratio north of 50%. [While] we’re not committed to a pay-out ratio, that’s a good starting base. On top of that, we decided to do a one-time 50 cent dividend. And that’s really to do a one-time return of the surplus that we’d built up in preparation for the Basel reforms kicking in. [In addition,] we decided to terminate the scrip dividend. As you know, we never gave a discount on scrip dividend for several years, so it [minimised dilution]. Nevertheless, we kept issuing more capital every year and we decided to stop that. So in sum, the impact of these is a dividend yield as of today’s share price of about 4.5- 4.6% – we’re a fairly high-yield stock at this point in time.

We’re not changing our dividend policy. Our policy has always been to increase dividends over the longer term in line with earnings growth. We’re going to maintain that stance. We don’t have a specific pay-out ratio in mind but we will continue to be steady and stable in terms of how we think about dividends, in line with earnings growth.”

Essentially, the finalisation of the impact of Basel III on their risk weighted assets has afforded DBS sufficient clarity to optimise their capital usage. This is interesting because as Piyush Gupta himself pointed out, this makes DBS a high-yield stock, something you would expect more from a utility such as a telco rather than a bank. There are a couple of possible explanations, based on observations of other high yielding dividend stocks:

- Slower Growth – Their business model has matured to a point where high growth is no longer realistic, and new investment of capital yields diminishing returns. The company therefore pays a higher dividend to shareholders as a reward for holding the stock. Given what I understand about DBS and its aspirations, this doesn’t seem a plausible explanation.

- Rerating of the stock – An interesting theory floated recently was that DBS may be looking to rerate the stock in anticipation for a large corporate transaction (eg. M&A) down the road. By raising the dividend significantly above its peers OCBC and UOB, the market may afford DBS a P/E expansion, sending this stock to new heights. This would facilitate the acquisition of a lower P/E bank, which would boost DBS’s asset pool and make it a truly global bank. An interesting point of view indeed, and only time will tell if this is true.

- Occam’s Razor – Sometimes, the simplest explanation may be the correct explanation. It might really be that the finalisation of the impact of Basel III rules have allows DBS to free up existing capital, to be released to shareholders in the form of a dividend.

Whatever the explanation, there is no getting around the fact that DBS is now a high yield dividend stock. It is interesting to watch how UOB and OCBC respond to this. Do they raise their dividend in response, when they themselves have not finalised the impact of Basel III? Or do they watch as the DBS stock rerates with its higher dividend?

- Focus on Return on Equity (ROE)

Like many other Temasek linked companies, DBS is showing a renewed focus on Return on Equity. In the 2017 Annual Report, Piyush Gupta spoke at length about DBS’s focus on ROE, which again, is important enough to be reproduced in verbatim (emphasis mine, I love this guy’s quotes). Take note also on how they plan to achieve this 13% ROE, essentially a three pronged method of (1) rising interest rates, (2) clarity on Basel III implementation freeing up capital for other uses and (3) digitisation.

Q1: You recently spoke about a return on equity (ROE) target of 13%. It is a level that DBS has barely achieved in the past; at the same time, banks are finding it difficult to maintain their historical returns because of more stringent capital requirements. Why would it be different for DBS?

A: Our ROE since 2010 has been around 11%, similar to the preceding decade.

Normalising for allowances, our 2017 ROE would also have been at that level. However, the underlying returns of our business have been rising since 2010. Wealth management income has quadrupled during the period to SGD 2.11 billion and now accounts for 18% of group income, while cash management income crossed SGD 1 billion this year from almost nothing. Both are low-capital-usage and high-returns businesses. The proportion of capital-intensive trading income has halved to one-tenth of group income. These improvements have been masked by the low interest rate environment and a build-up of our capital, both of which are now being reversed.

Interest rates have been low over the past decade. Three-month Singapore-dollar interbank rates, the benchmark for pricing domestic loans, last peaked in 2006 at 3.5%, declined during the global financial crisis and then stayed below 1% until 2015. Since then they have been hovering around 1%. With reflation in the global economy well under way, the general view is that interest rates around the world are on a cyclical upturn. Given our balance sheet structure, a one-percentage-point increase in domestic interest rates roughly translates into a one percentage-point improvement in ROE.

With the publication of Basel regulatory requirements in December, we finally have clarity on capital requirements. The impact on us is not significant – risk-weighted assets rise by only 5% on a pro forma basis when the rules are fully implemented in 2022. The capital we have been building up because of the uncertainty can now be returned. The special dividend of 50 cents per share is the initial step to recalibrate our Common Equity Tier 1 (CET1) ratio closer to our long-term target of 13% compared to the 14% we have been operating on. Barring unforeseen circumstances, we are also raising the annual payout to SGD 1.20 per share. The reduction in CET1 will be another driver for improving ROE.

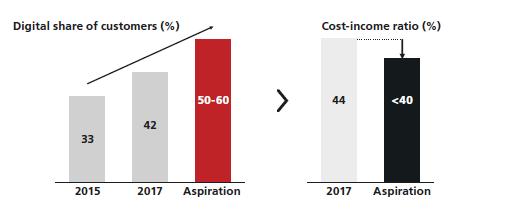

A third ROE driver is the improvement to the cost-income ratio that digitalisation brings. Digitalisation enables us to increase wallet share at lower marginal costs in developed markets and scale profi tably into the granular SME and mass consumer segments in emerging markets. These gains should reduce the cost-income ratio by at least half a percentage point annually in the near term. Over the intermediate term, the rate of cost-income ratio improvements will pick up if our digital strategy enables emerging markets to contribute more meaningfully to DBS. A five-percentage-point improvement in the cost-income ratio translates into a one percentage-point improvement in ROE.

These three drivers will contribute to DBS’ ROE at their own pace and cycles, but their combined effect should result in a discernible improvement in our returns over the next few years. We believe a ROE of 13% is readily achievable.

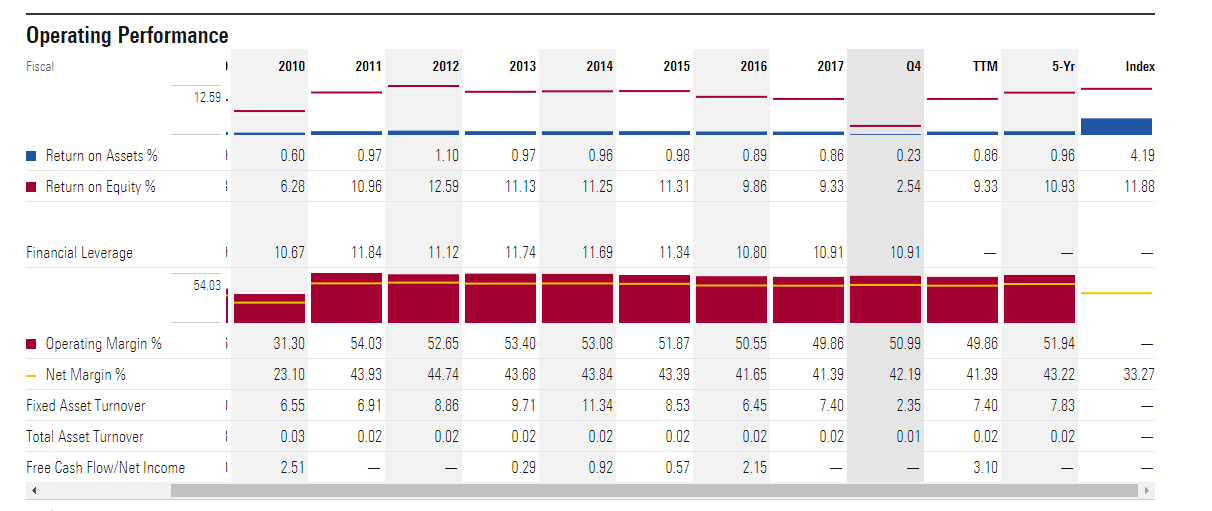

Whether they can execute remains to be seen, but Mr Gupta has a fantastic track record at DBS thus far, and I remain optimistic on execution. If this 13% ROE can be achieved (the TTM ROE is 9.33%, and the typical ROE for banks is 11%), there may be significant upside for DBS’s share price.

Source: MorningStar

- Digitisation

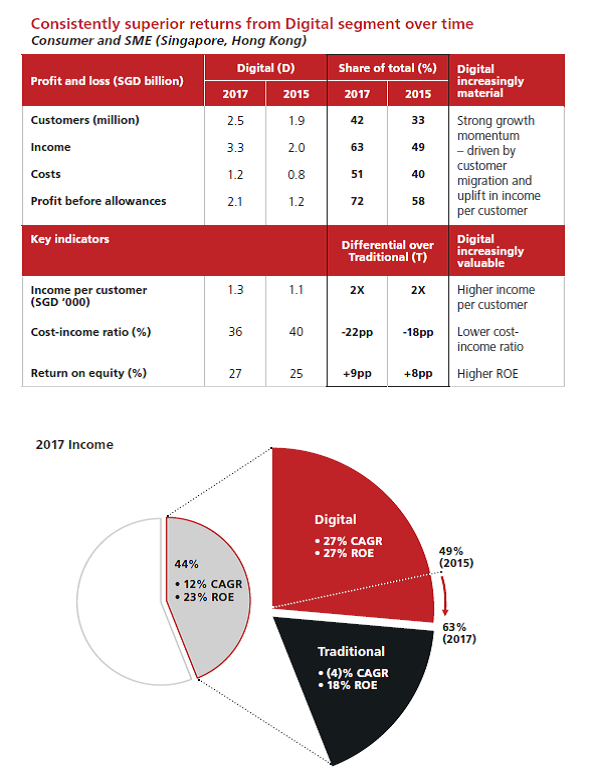

In the DBS 2017 annual report, DBS branded themselves the Digital Bank of Singapore, which underlines their focus on digitisation.

Source: DBS FY2017 Annual Report

I opened a DBS multiplier account recently, and was blown away by the impact of a full digitisation of a bank’s backend. As I have existing accounts with DBS, all I had to do was to consent to use my existing personal details and signature, and a few clicks later, my new account was ready. There was no need to upload identification documents, or to wait 5 working days for a backroom monkey to process the account.

This, to me, is the future. Today’s millennials are used to transactions being executed instantly, and legacy banking, where one waits 3 working days for the bank to process a transaction, is simply untenable. The ominous rise of cryptocurrencies, Alipay, Wechat Pay, shows that there is massive pent up demand for a more efficient form of global banking and monetary transfer, and if it is not met by legacy banks, it will be met by some startup funded by Alibaba. The fact that DBS is relentlessly focused on digitisation is not only a good to have, it is a must in today’s society.

DBS has gone through 2 years of hard work and costs in digitising their entire back end, and I think that they will really start to reap the benefits going forward. There are many charts showing how digital customers are more engaged and perform more transactions (translates to higher stickiness), and are cheaper from cost perspective, given that most of the transactions are processed by the computer instead of a human.

Having moved a significant portion of my assets over to DBS recently, I testify to this. DBS’s internet banking interface and mobile app are by far the most intuitive and convenient of the 3 local banks. Given a choice, I would use DBS’s interface over the other 3 any day (UOB is the worst, please up your game UOB…).

Source: DBS FY2017 Annual Report

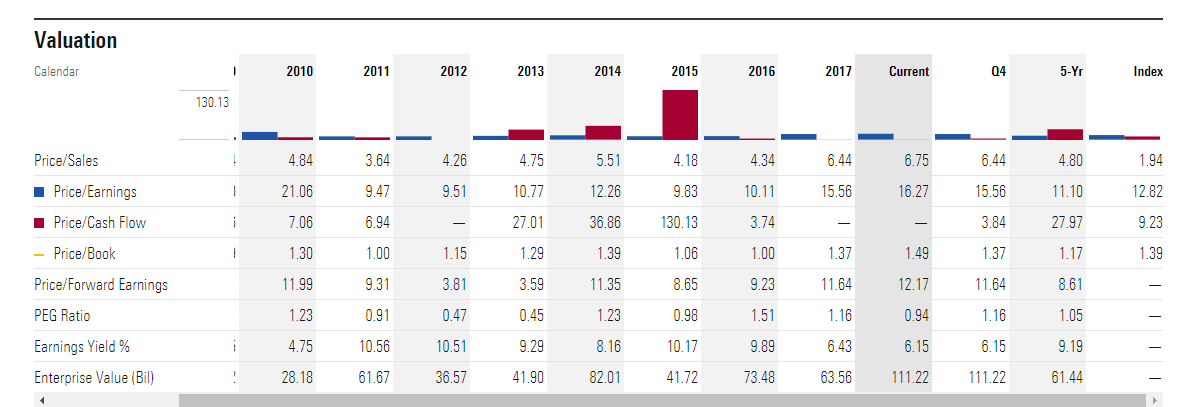

- Valuation

The key valuation metrics of DBS vs UOB and OCBC are set out below. It is clear that DBS is trading at a premium to the other 2 local banks, in terms of TTM P/E and P/B. I think that this is justified given DBS’s focus on ROE and digitisation, especially since they had to incur significant costs the past 2 years to focus on digitisation. Their TTM ROE is the lowest of the three banks, and once they start to reap the benefits of digitisation, their valuation metrics may catch up and possibly surpass the other banks.

With their strong forward dividend, it becomes a lot harder to compare DBS with the other 2 banks, simply because you are getting paid to hold onto the stock.

| DBS | UOB | OCBC | |

| P/E | 16.32 | 13.16 | 13.89 |

| Forward P/E | 10.91 | 10.42 | 10.66 |

| P/B | 1.48 | 1.38 | 1.24 |

| ROE | 9.31% | 10.84% | 9.72% |

| Forward yield | 4.36% | 2.9% | 3.15% |

Source: MorningStar

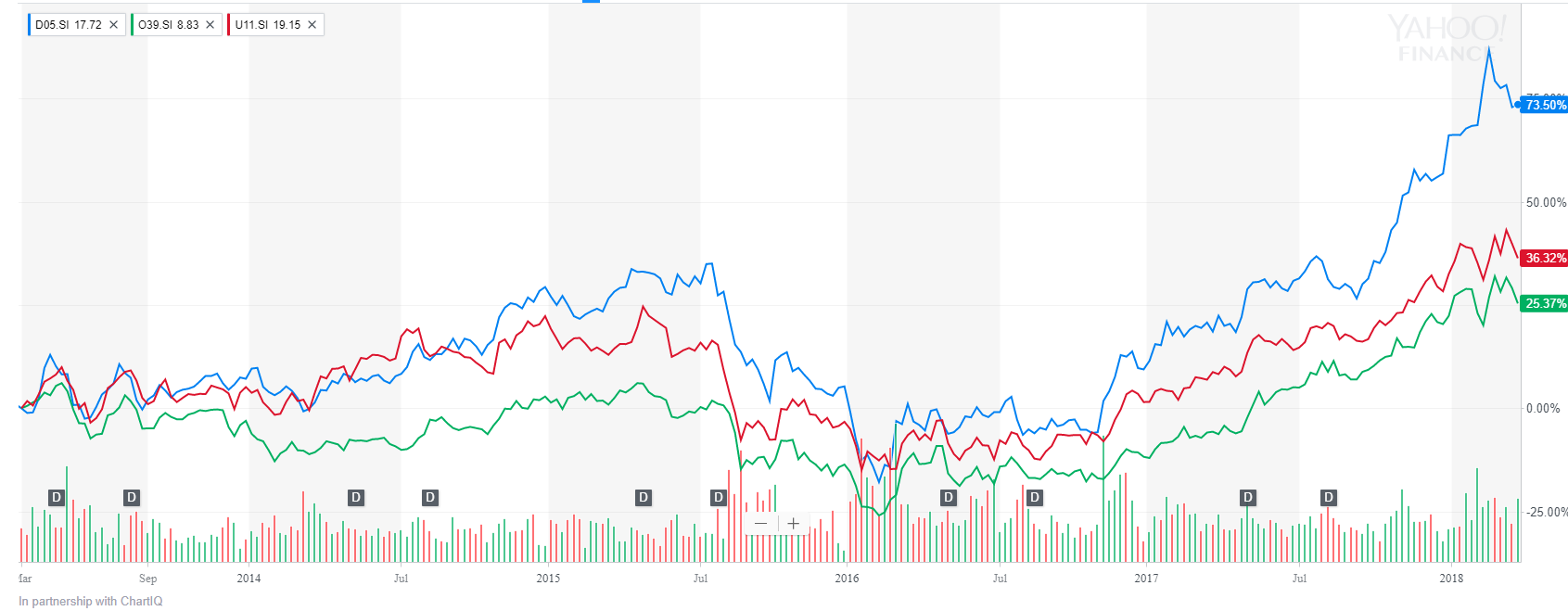

DBS has had a much stronger run than UOB and OCBC (76% vs 36% and 25% respectively), but I think this is justified for the reasons above, and given OCBC’s troubles in integrating Wing Hang bank into its fold.

Source: Yahoo Finance (Blue is DBS, Red is UOB, Green is OCBC)

Tail Risks

There are 3 main tail risks that I am afraid of.

Economic recession / Trade War

There is no industry more in tune with the health of the economy than the financial industry. An economic recession should be at the forefront of every investor’s mind when investing in banks. I am keeping a firm eye on the economic indicators such as the yield curve, but none of these are predicting an imminent recession.

The risk of a trade-war from President Trump looks a bit overplayed to me. Admittedly, a full blown trade war would be disastrous for the global economy, but I have my doubts whether it will ever come to that. President Trump has proven himself adept at resorting to sweeping populist plays to garner public support, only to leave the matter hanging (eg. North Korea, ban on guns, Mexico Border wall). The actual implementation of tariffs would take months to implement, if at all, and the current tariffs being proposed (including reciprocal tariffs from China) look very targeted, and unlikely to cause sweeping damage to global trade.

Rise of Fintech

The rise of fintech is a threat for any global bank. However, fintech has been around since 2011, and predictions about the demise of traditional banks have not come to fruition. The financial industry is highly regulated, and my belief is that as these non-traditional fintech players grow in size, they will find their growth increasingly hindered by stringent regulatory requirements. Traditional banks have been around for decades, and are familiar in navigating the regulatory landscape. I am confident that there will be a place for a bank that keeps abreast of technological changes.

Of the 3 local banks, my bet is on DBS. Having had numerous opportunities to work with DBS staff on a professional level, I am always impressed by how progressive the bank is, and their willingness to adapt to accommodate new financial and technological innovations. For example, PayLah is the most successful mobile transfer app so far, and DBS Ideal has been widely adopted by many Singapore corporations.

Growth

Closely related to this is the question of growth. The Singapore banking industry is an oligopoly, and it is incredibly hard to steal market share from competitors. To grow its assets, DBS has to either acquire a competitor (Eg. the acquisition of ANZ), or expand into neighbouring economies. The emphasis thus far seems to be on improving ROE and digitisation first, to give DBS a platform on which it can grow. However, not much clarity has been provided on its plans to grow the bank going forward.

Recent initiatives such as digibank India and digibank Indonesia are useful in gaining a foothold in neighbouring markets, but whether these can grow to become a significant revenue contributor, remains to be seen.

I will continue to watch this space with optimism, and with the 4.3% forward dividend, it gets a lot easier to be paid to wait (perhaps a large M&A to shortcut growth?).

Closing Thoughts

With its 4.3% forward yield, DBS now looks like a dividend play. It trades at a premium to UOB and OCBC, but this is justified given that they have been spending heavily on digitisation. Having spent significantly on digitisation to reduce operational costs and increase efficiency, I am confident that DBS is better placed than UOB and OCBC to reap the benefits going forward.

Ultimately though, there is no getting away from the fact that DBS is a bank stock, and like all bank stocks, it is deeply intertwined with the global economy. No amount of digitisation will save the share price when the next recession comes, which it will. Accordingly, an investment in DBS is inherently risky.

My personal take is that none of the major economic indicators are pointing towards an imminent recession. The current correction in share prices may simply be just that, a pause in bull market run. If so, there may be 2 to 3 years left on this bull market, and some money to be made on DBS.

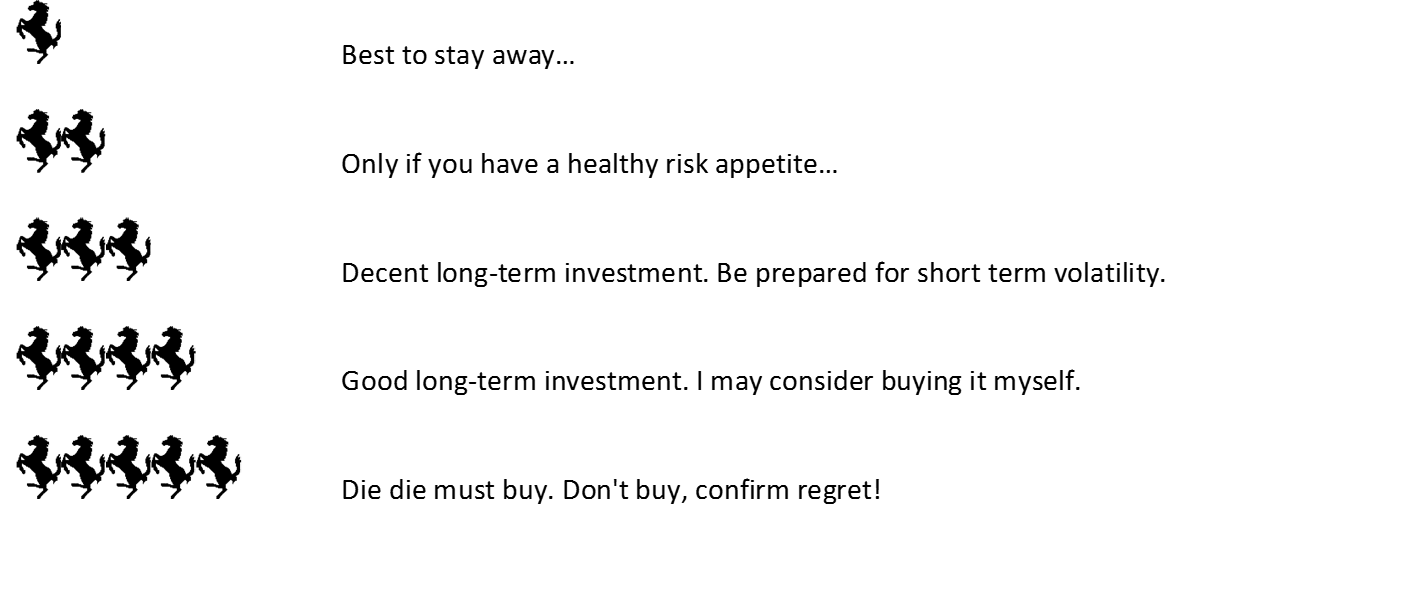

I have an existing position in DBS, and may consider adding to my position in the weeks ahead. I will give DBS a 3 horse rating, because I like the mid-term prospects of the stock, with its high yield, its focus on ROE, and its digitisation efforts paying off. Short term is tricky because the market is in correction, but I believe the 4.3% forward yield will serve as a floor on the share price. Long term I am wary of the end of this economic cycle. Invest with care.

Thinking about investing in S-REITs for income yield? Check out what you should look out for in a S-REIT here.

DBS Bank Ltd – Financial Horse Rating:

Financial Horse Rating Scale:

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

I remember reading this nearly a year back. What are your thoughts about DBS now post correction? Any regrets holding in 2018? Thanks

No regrets. After including dividends, an investor who bought at this price is probably sitting on a small gain. I also think that there is still some upside left in this stock, simply because this economic cycle isn’t over yet.

That said, I’m a lot more bearish on the global macro outlook over the next 12 – 24 months than I was this time last year, so I’m growing a lot more cautious on stocks like DBS going forward.

Cheers.

While dividend gains are nice to obtain, I feel it should not be at the expense of eroding capital gains.

Anyhow, thank you very much for bothering to reply such an old post. Will definitely keep reading FH.

Well there was a nice rally in share prices today that brought it close to 25. ;).

No problem at all, and thanks for your support. If you’re looking to exit, my gut feel is that there will be at least 1 more good opportunity to do so, before the next recession hits. 🙂

Thanks for the article! Very insightful for a newbie investor like me! What do you think of DBS as of now? Is it too late now to get some DBS (& other banking) stocks? Thank you!

Well it always depends on your investing horizon. As a long term investor, I still really like DBS. 🙂

Short term though, there’s just a lot of volatility.

hey financialhorse. If i have a long term investment horizon is starting to Dollar Cost Average monthly savings into DBS stocks a good idea for the dividend growth and compounding effect( especially with starting in a time like this where there is room for capital gains considering the low prices currently)

Well it really depends on your risk appetite and investment objectives. If you’re prepared to lock up the money for 3 years or more, I think prices now are interesting on a historical basis. That said, if you’re able to active invest, there are probably better places to park the money. So it really depends on the kind of investor you are. 🙂