As long time readers may recall, I bought a position in Digital Core REIT at IPO.

I then sold it for a 20-30% profit post IPO.

Since then, the share price has collapsed 65%.

At latest price of $0.415, that works out to a 9.5% trailing dividend yield.

50% discount to book.

And this is a data centre REIT – remember when DC REITs used to trade at 3% yields?

Boy… how fast fortunes change.

In any case, I was quite keen to take an updated look at Digital Core REIT, to see if value has emerged at these prices.

Digital Core REIT trades at a 9.5% Dividend Yield (latest Unit Price of $0.415)

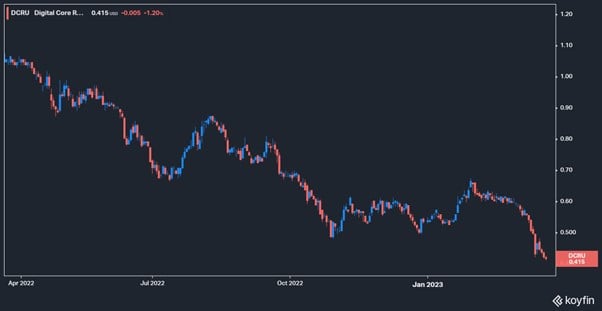

You can see the performance since IPO below.

Digital Core REIT IPO-ed at $0.88 and went as high as $1.25.

It then collapsed 65% from highs.

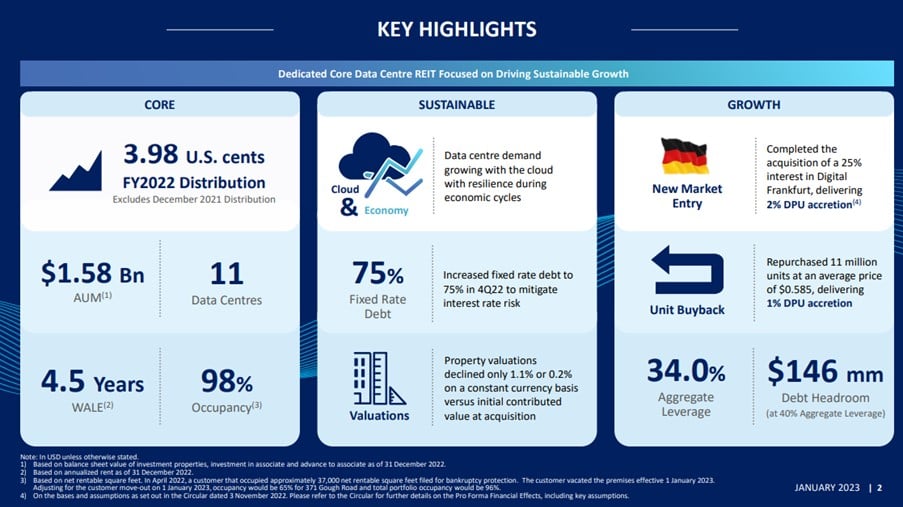

FY2022 dividend is 3.98 cents.

At current price of $0.415, that works out to a whopping 9.47% dividend yield.

And a 50% discount to book value.

3 things that concern me about Digital Core REIT

Look after the risks, and the upside will take care of itself.

As investors, you always want to manage risk first, and think of upside second.

There are 3 points that concern me about Digital Core REIT:

- Top Tenants are running into difficulties

- Conflict of Interests with Sponsor

- Valuations of the properties

Top Tenants are running into difficulties

Long story short – some of the top tenants are running into difficulties.

Don’t know about you, but reading some of these reports gives me a déjà vu of the post 2000 Dot Com bubble, when funding dried up and tech companies failed by the dozen.

Second Largest Tenant (Cyxtera Technologies) downgraded

Here’s the reporting from the Edge (emphasis mine):

According to DBS Group Research, Cyxtera Technologies is one of DC REIT’s top 10 tenants accounting for 22.6% of gross rental income. Cyxtera Technologies is a data centre owner and operator in the US, and Asia-Pacific.

Last month, Bloomberg reported that Cyxtera is attempting to refinance a revolving credit facility that matures in November this year. “Fresh concerns on Cyxtera’s ability to service their debt obligations have surfaced, and most recently, Moody’s downgraded the company’s corporate family rating from B3 to Caa2. Moody’s cited that although they believed in Cyxtera’s underlying business fundamentals, they are concerned with the firm’s ability to service debt obligations in the medium term,” the DBS report says.

“We understand that although energy prices have came off the peak and have stabilised, the high interest rate environment calls into question Cyxtera’s ability to continue expanding and growing, which has been once of the key drivers of its business strategy,” DBS says.

Digital Core REIT even issued a response to the article.

Here’s their reply (announced on SGX, emphasis mine):

The Manager wishes to announce that:

On 17 February 2023, Moody’s Investors Service downgraded to Caa2 from B3 the corporate credit rating of Digital Core REIT’s second-largest customer (Digital Core REIT does not disclose the identity of its customers, as the lease agreements with these customers contain confidentiality provisions that restrict Digital Core REIT from disclosing their identities or the terms of their agreements.) , a publicly traded global colocation and interconnection provider that occupies three buildings in Silicon Valley, two in Los Angeles and less than 5% of a facility in Frankfurt, and represents approximately $16 million of annualized rent or 22.6% of Digital Core REIT’s total annualized rent.

(ii) On 16 March 2023, the customer announced that it entered into an agreement with its lenders to extend the maturity date of its only 2023 debt maturity to April 2024.

(iii) The customer remains current on its rental obligations and has not requested any rent deferments, rental reductions, or contraction of the space it occupies.

To sum up.

The second largest tenant has been downgraded and may be facing cash flow issues.

But as of now, it hasn’t defaulted yet, and is still paying rent.

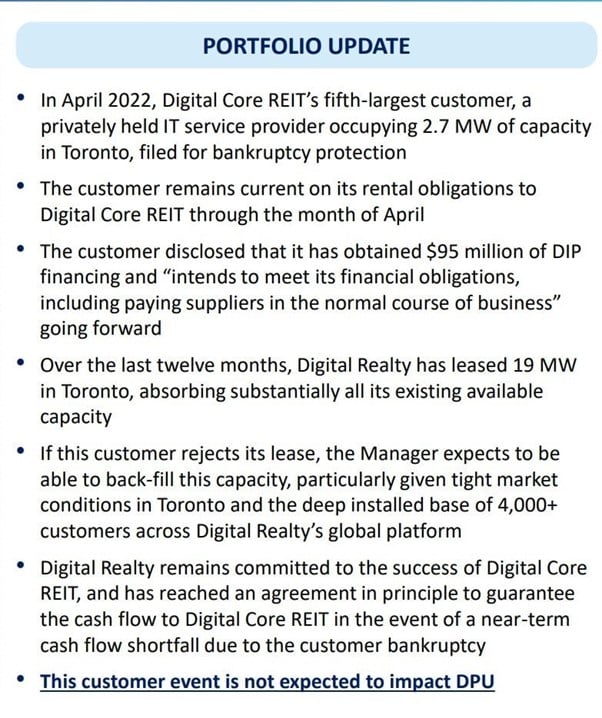

Bankruptcy of 5th Largest Tenant last year

This is particularly troubling when you look at it in light of what happened in 2022.

With the bankruptcy of Digital Core REIT’s 5th largest customer (which makes up 7% of revenue).

So in the span of 12 months, the fifth largest tenant has filed for bankruptcy.

While the second largest tenant has a rating downgrade and may be facing financial difficulty.

That’s… concerning.

Sponsor provides “rental guarantee”

In the case of the 5th largest tenant bankruptcy though, the Sponsor (Digital Realty Trust which owns a 30%+ stake), provided a guarantee of the rental income stream to Digital Core REIT in the event of a near-term cash flow shortfall due to the customer bankruptcy.

In plain English – if Digital Core REIT runs into cash flow issues because of this bankruptcy, the Sponsor will provide a backup rental income stream.

Will they do the same if the second largest tenant goes bankrupt?

DBS had this to say:

“Based on our estimates, Cyxtera is DC REIT’s second largest tenant, accounting for 22.6% of DCREIT’s revenues. Although this may seem like a concern for DCREIT, we take comfort from its Sponsor’s commitment to the REIT. Similar to what we saw with SunGard previously, DCREIT’s Sponsor was quick to step in and provide support for the REIT.”

Is this cause for concern?

The million dollar question is whether these are isolated incidents.

Or whether they are in the canary in the coal mine for more tenant bankruptcies down the road.

Data Center REITs are prized for their stability.

They are locked into long term leases with built in rental escalation, which provides very stable underlying cash flow.

That’s the whole appeal of Data Center REITs.

This is not a retail mall where you’re finding new tenants every 2 – 3 years for each lot.

Financial difficulties in 2 of the Top 10 tenants in less than 12 months, is concerning.

My personal thoughts?

I do have concerns on how tech companies hold up going forward.

COVID was a one-off explosion in demand for tech services.

This was compounded by easy money from the Feds, allowing all kind of startups to get funding.

Now that the COVID boom is over, and easy money is over, I’m not so sure how well they hold up.

I shared previously that I see Silicon Valley Bank’s failure not as a sign of banking weakness, but as a sign of funding stress in the startup space.

I do think it will get worse before it gets better, for the tenants of Digital Core REIT.

Throw in overinvestment into data centres during the height of the COVID boom, and the mid term picture is also troubling.

Conflict of Interests with Sponsor

In my article on Digital Core REIT at IPO, I said my biggest concern was potential conflicts of interests with the sponsor.

Digital Core REIT is unique in that the sponsor is a REIT itself – Digital Realty Trust (listed in the US).

Digital Realty Trust is a $29 billion market cap behemoth, so the relationship between Digital Realty Trust and Digital Core REIT is vitally important for the long term success of the REIT.

We now have some better idea on this from the first acquisition announced by Digital Core REIT.

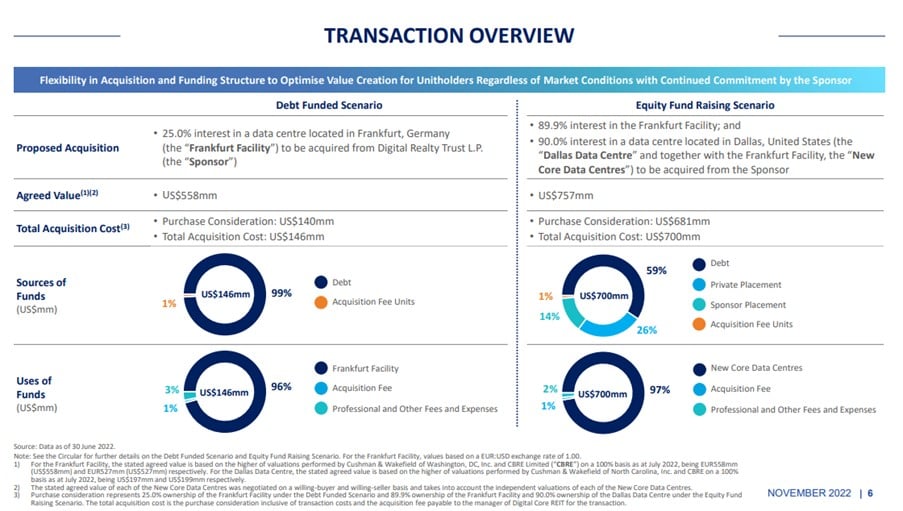

Basically – the Sponsor was planning to sell 2 data centres to Digital Core REIT.

How much Digital Core REIT would buy would depend on how much financing they could raise.

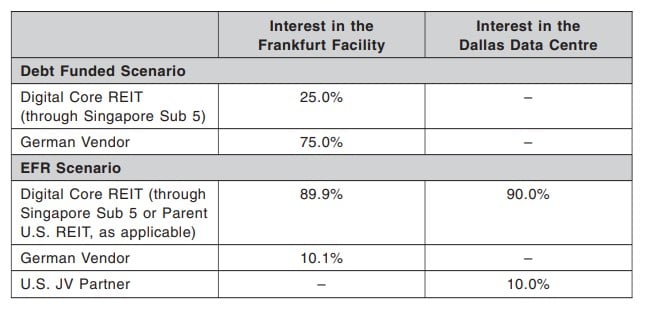

So 2 options were created:

Debt funded scenario – where Digital Core REIT would only buy a 25% stake in the Frankfurt property

Equity funded scenario – where Digital Core REIT would buy both the Frankfurt and Dallas property

As you know by now, nobody in their right mind would try to raise equity in the second half of 2022 – the market would have murdered you if you tried.

So Digital Core REIT (rightly I must say) went with the debt funded scenario.

This is good, shows that the Sponsor wouldn’t force a bad transaction on the REIT just to benefit itself.

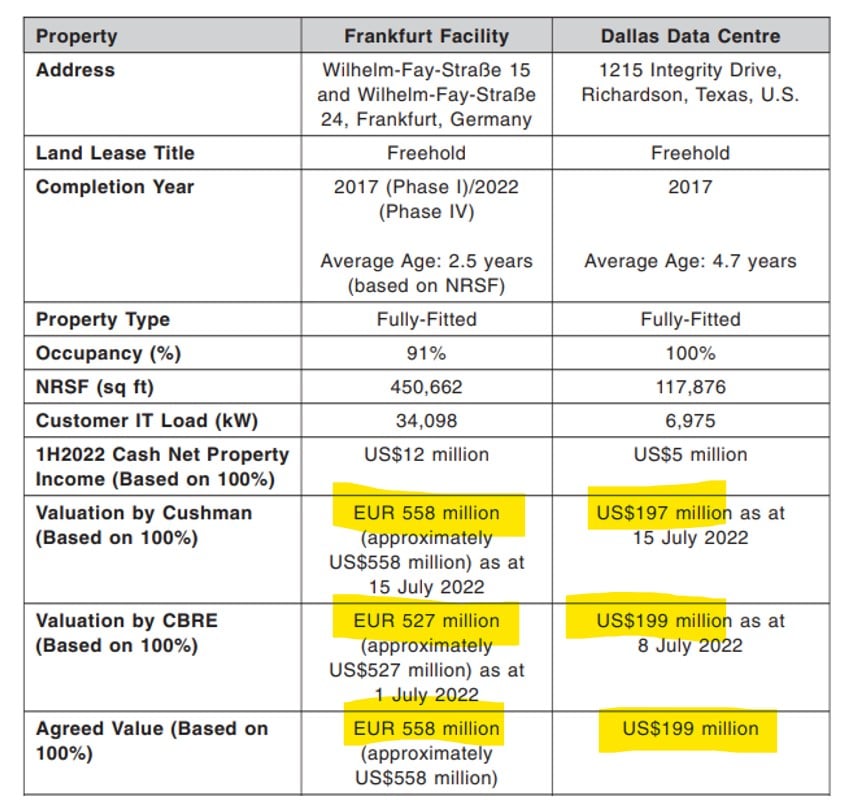

What about pricing of the Data Centres?

The pricing though, is more interesting.

2 valuations were done for regulatory reasons, and you can see that in both cases the final agreed price was the higher of the 2 valuations done.

This is interesting, in some other deals where the REIT is buying from the sponsor you would see price fixed at the lower of the 2 valuations, or the average of the 2 valuations.

If you dive deeper into the numbers, this works out to a 4% cap rate for Frankfurt, and a 5% cap rate for Dallas.

Are the valuations reasonable?

In 2021 / early 2022 without a doubt, that pricing would be considered a steal.

But in late 2022 with rapidly rising interest rates, the answer gets more tricky.

Sponsor – Digital Realty Trust

Let’s talk a bit more about the Sponsor.

Digital Realty Trust hasn’t been doing too well itself.

It’s down 43% from highs, and trades at a 5% dividend yield now.

With a $29 billion market cap (vs $500m for Digital Core REIT)

The sponsor does hold a convincing 30%+ stake in the REIT though.

I really like this.

But of course the question remains when push comes to shove – would the Sponsor still prioritize the interests of Digital Core REIT over itself?

Especially when the Sponsor is a listed REIT with its own shareholders to answer to?

My views on the Sponsor situation for Digital Core REIT?

The rental guarantee from the Sponsor when the 5th largest tenant went into bankruptcy is a nice touch.

The fact that they didn’t insist on the equity offering is good too.

The pricing of the Data Centers is probably on the high side, but to be really fair I don’t think you can fault them as they have their own shareholders to answer to as well.

At 4% and 5% cap rates, I wouldn’t say they are completely out of this world for the second half of 2022.

So I suppose there’s no real big red flags from the Sponsor so far, although we will need more time to make the call.

This isn’t a CapitaLand or Mapletree or Frasers where we have more than a decade of transactions to draw on to understand how the Sponsor would act.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

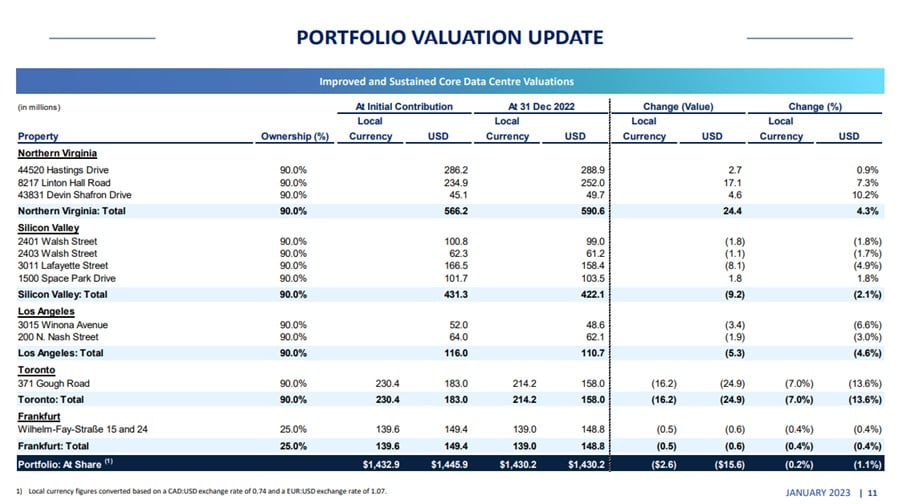

Valuation of Data Centres of Digital Core REIT

The last point is on valuations.

Digital Core REIT reported $68 million FY22 Revenue with a $1.423b Property Value.

That works out to a blended 4.875% cap rate for the entire property portfolio.

NAV is $0.83, so at current price of $0.415 you are buying at a 50% discount to book.

Works out to around 9.6% cap rates for the entire Data Center portfolio.

That’s definitely on the high side here, and suggests the market is pricing in distress.

Insolvency Risk of Digital Core REIT?

Tenant Default risk we already discussed above.

The next one to discuss is insolvency risk of Digital Core REIT.

Because if you are going to buy a REIT holding data centre assets at distressed pricing, you want to make sure you can hold on and emerge on the other side of this cycle.

Without any insolvency, or any big dilutive equity fundraise.

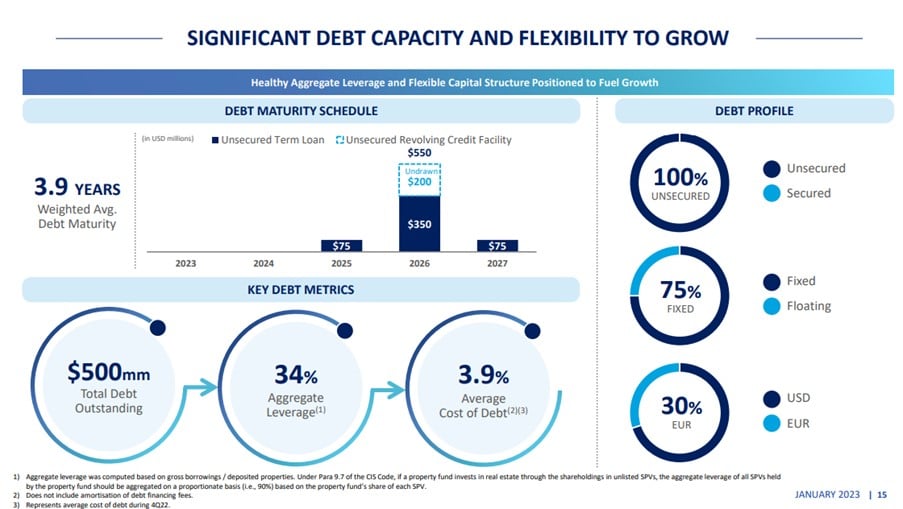

Financial Situation of Digital Core REIT

Debt maturity profile looks good.

No loans coming due until 2025.

All the debt is unsecured as well, and are fixed rate loans.

They also have a $200 million unsecured revolving credit facility they can draw down on.

So the financing side looks good.

And you would hope there’s no big equity fundraise at this price.

Looking at how Digital Core REIT rightly went with the debt transaction instead of equity transaction, here’s hoping this remains the case going forward.

Will I buy Digital Core REIT at 9.5% Dividend Yield? Is the risk-reward worth it?

At the end of the day though, investing is about risk-reward.

I’ve set out the key risks above, which everyone in the market knows.

The million dollar question then – is this appropriately priced in?

At a 9.5% dividend yield and 50% discount to book.

Does Digital Core REIT offer good risk-reward?

You’re basically buying at a 50% discount from 2021/2022 peak valuations, is that a good enough price to entice buyers?

What I am worried about

What concerns me, is that it is very clear the credit cycle has not bottomed yet.

With the failure of Silicon Valley Bank and Credit Suisse, I think we have only just entered the phase of the credit cycle where stuff starts to break.

I see Silicon Valley Bank and Credit Suisse as the weakest dominos this cycle, and therefore the first to fall.

I doubt if they are the last.

And the concern here – I just don’t know what I don’t know.

I don’t know what is going to break in the broader economy over the next 12 months (or not).

We’re kind of in a catch-22 here.

You see if nothing breaks, then the Feds just keep interest rates at these levels, and at some point highly levered instruments like REITs are going to suffer even more.

If something breaks, then well what is it that is big enough for the Feds to panic and start slashing interest rates?

And do I necessarily want to buy a small cap REIT like Digital Core REIT before an event like that?

This worries me.

The past few weeks feel like Bear Stearns in 2008.

Sure, market had a big relief rally after Bear Sterns was bought out, but the bigger fireworks lay ahead.

I would expect more opportunities to emerge in the equities / REITs space as this year plays out, so I do want to keep my options open as well. I’ll be updating my Stock / REIT watchlist this weekend for Patrons on where I see value right now – Do sign up if you are keen.

Will I buy Digital Core REIT at 9.5% Dividend Yield?

So to answer the question simply.

I don’t know.

I haven’t decided whether I will buy Digital Core REIT at this point in time.

I’ve shared some of my key considerations above, and hopefully they may help you in your decision making.

I’m tempted to pick up a position with a tight stop loss and careful risk management.

At 50% discount to book, market is pricing in real distress here.

At 50% discount to book, you have a fairly decent margin of safety.

Is it enough – ultimately for each investor to decide.

But hey, let’s see.

I’ll wait to see how things play out and decide accordingly. And I may use technical analysis to guide my exact buying decisions (and stop loss).

As always, Patrons will get updates if / when I make changes to my personal portfolio. I’ll be updating my REIT and Stock Watchlist this weekend as well. Do sign up as a Patreon if you are keen.

Digital Core REIT Unit Buyback

One final nugget of information, is that Digital Core REIT bought back 11 million units at an average price of $0.585 in December.

Even after this, the REIT can still buy back another 100 million shares under its unit buy back mandate.

That will bring gearing up to high 30%.

Looking at the SGX Announcements – most of the buybacks were done in December 2022.

With no new buybacks done in 2023.

With share price languishing in the low 40s, almost 30% below their previous average buy price.

I wonder if management will start activating the buybacks soon.

If exercised though, it could provide a real floor on the unit price.

This article is written on 24 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (extended to 31 March)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares (extended to 31 March).

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!