Note: Given that the final prospectus has been registered, do also check out my updated thoughts in a more comprehensive article here!

As many of you probably know by now, I absolutely love REITs. So I was terribly excited when I heard that the first mainboard IPO of the Year of the Rat was going to be a REIT IPO – Elite Commercial REIT initial public offer (IPO).

The preliminary prospectus was just lodged on MAS Opera (link here), so the final details are not out yet, but I just wanted to share some quick thoughts on this hot new IPO of Elite Commercial REIT.

Basics: Elite Commercial REIT IPO

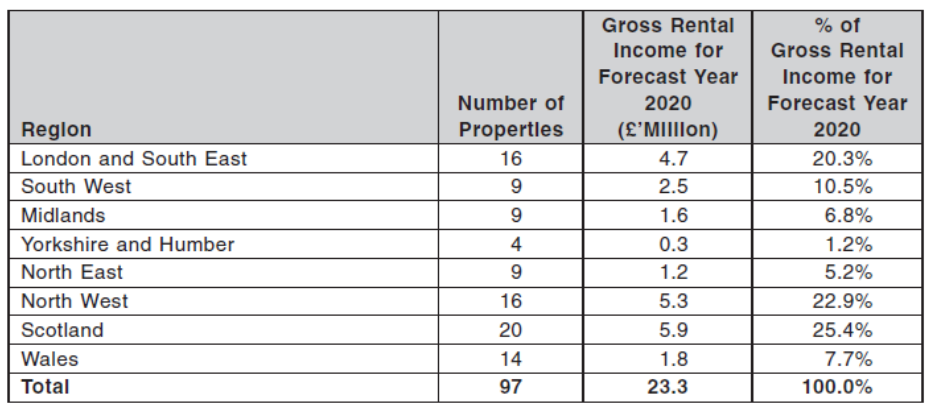

Elite Commercial REIT holds a portfolio of 97 commercial buildings (offices) across the UK. The initial portfolio has a valuation of about GBP319 million, which indicates this is going to be a small to mid-cap offering (leaning towards small).

Properties are scattered across the UK, with large concentrations in London and South East, North West, and Scotland. So not exactly big city stuff here.

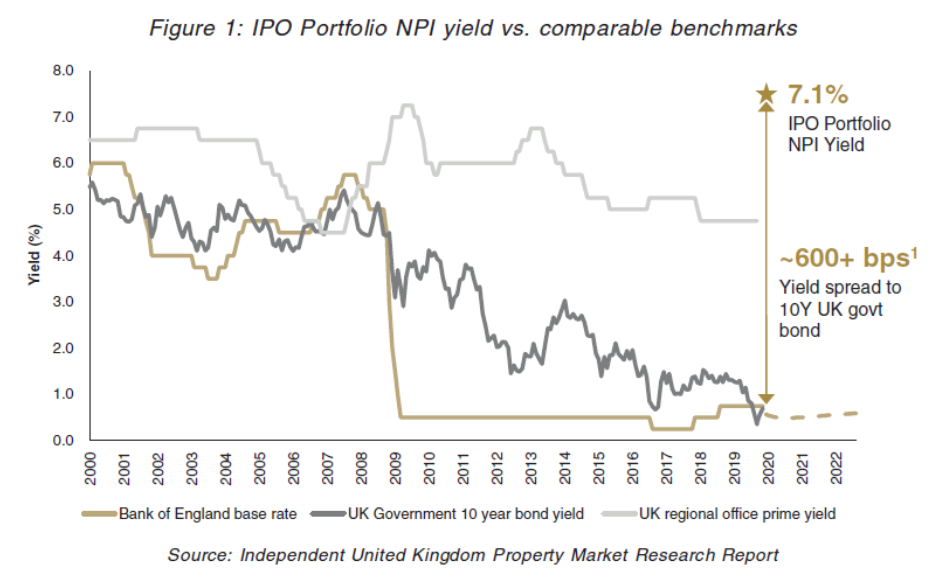

Indicative yield is 7.1%, which is not too shabby indeed.

Public offer of Elite Commercial REIT is targetted at 27 Jan 2020, or the third day of Chinese New Year. This likely means that the final prospectus will come out right before Chinese New Year.

3 Quick Thoughts on the Elite Commercial REIT IPO

-

DBS not on board?

One of the first things that struck me was the absence of DBS as one of the underwriting banks. It’s probably the first REIT IPO I’ve seen in a while where local juggernaut DBS isn’t on board. I wonder if there’s some juicy backstory here.

The presence of UBS as a Joint Issue Manager makes sense because this REIT is UK focussed, but OCBC replacing DBS is a very interesting one.

Disclosures in the prospectus point towards UBS and Bank of Singapore (OCBC’s private wealth arm) being the cornerstone investors. This does indicate that the issuer is using Bank of Singapore (instead of DBS) to place to private wealth in Singapore. So I suppose at the end of the day they’ll still get access to the same high net worth individuals, just via different banks.

It’s really interesting though, and the more I look at the list of underwriters, the more it leads me to think that this IPO may be heavily targeted at private wealth rather than institutional investors.

-

Yield of 7.1% looks really good

The indicative yield of 7.1% for forecast year 2020 looks really juicy.

Don’t forget that a couple of months ago, Lendlease REIT IPO went ahead with a 6.0% yield (Singapore and Italian properties) and was massively oversubscribed.

By that logic a 7.1% here looks pretty attractive, no?

There is a fair bit of forex risk and location risk (not all the properties are located in a mega-city London), so the big question is whether the higher yield is sufficient to compensate for the risk.

I have an early view on this, but I really want to wait until the final prospectus is out to see if there’s anything else I missed.

-

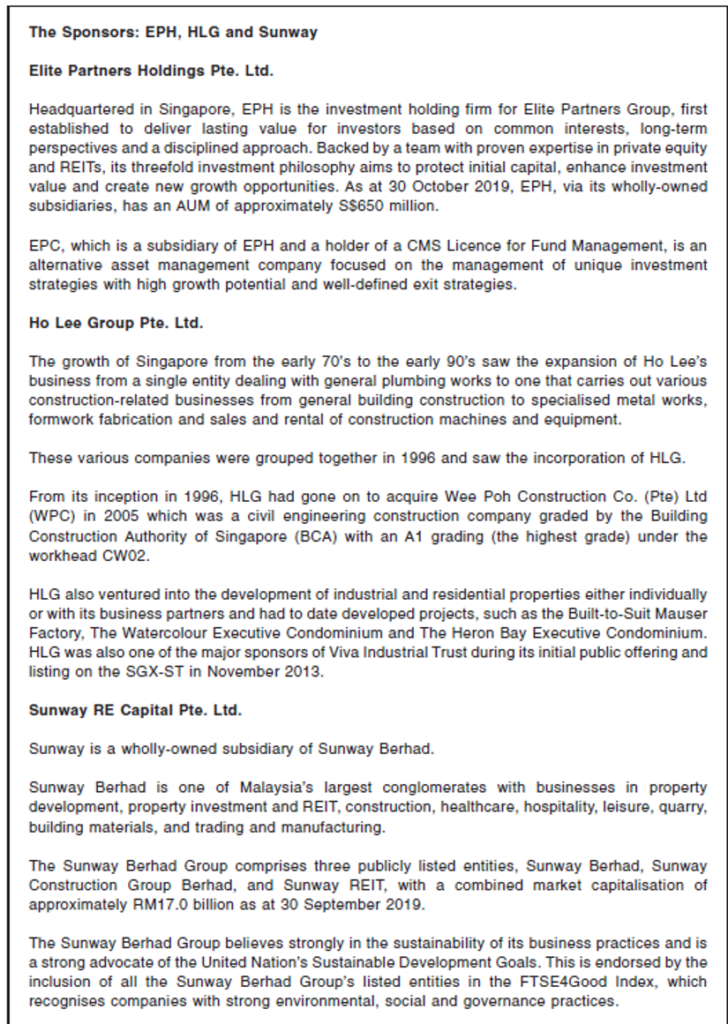

Who is the sponsor? What will alignment of interests look like?

Not naming names, but there was a recent IPO with foreign assets and a foreign sponsor that didn’t go so well. So it pays to be extra vigilant with sponsors, especially when we’re looking at foreign assets such as this.

This list of sponsors are set out below.

Elite Partners Capital is a Singapore-based private equity firm.

I googled them, and interestingly enough, this popped up (emphasis mine).

PUBLISHED NOV 26, 2018, 11:15 AM SGT

SINGAPORE – Singapore-based private equity firm Elite Partners Capital said on Monday (Nov 26) that it has acquired a portfolio of 97 commercial properties in the United Kingdom from British developer Telereal Trillium for £282.15 million (S$496 million).

The Hayhill Portfolio of freehold offices is mostly located in town centres across the UK and measures a combined 2.6 million square feet. It is currently let to the UK government’s Department for Work and Pensions on 10-year full repair and insurance leases with built-in rent uplifts until March 31, 2028. About 99.4 per cent of the rental income is secured against the covenant of the UK Secretary of State for Communities and Local Government.

The acquisition is the first significant transaction by the private equity firm’s Elite UK Commercial Fund, which focuses on UK real estate. The fund said that it has raised £120 million in equity and mezzanine funding from more than a dozen institutional investors, family offices and ultra-high net worth individuals.

Now I don’t know whether the 97 properties bought by Elite Partners Capital are the same 97 being injected into this IPO, but the coincidence is uncanny.

If indeed they are, then the portfolio valuation would have gone up from £282.15 million in Nov 2018 to £319 million about 1 year and 3 months later, which is a 13% increase.

I’m going to give them the benefit of doubt here, so I would say the valuation increase is not completely implausible. That said, we’ll want to do a deeper dive into the final prospectus before coming to any conclusions.

What I’ll also want to know, are the sponsors’ plan for Elite Commercial REIT post-IPO, what kinds of stakes they will be holding, and basically what kind of alignment of interests is on the cards here.

There’s nothing that annoys me as an investor more than when a sponsor is not aligned with the REIT.

But again, it’s way, way too early to comment, so let’s wait for the final prospectus of Elite Commercial REIT to be out. This could still turn out to go like hot bak kwa on 初一!

Final Prospectus should be out before 初一, so I’ll try to share my thoughts as and when I can grab a break during CNY visiting. Stay tuned!

Note: Given that the final prospectus has been registered, do also check out my updated thoughts in a more comprehensive article here!

*Reminder*

Back by popular demand, we’re launching a Chinese New Year promotion for the FH Course, at a discounted price of $288. For those of you who missed the Christmas promo, now’s a great time to grab it, as we probably won’t be doing another promo for a while!

What are your preliminary thoughts on Elite Commercial REIT’s IPO? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

All properties are in UK and the IPO is time just before BREXIT! Personally I will refrain as I am rather pessimistic about the UK after Brexit. Britain have may centuries had clutches – first the colonies and in more recent times the EU. No doubt that Britainnica stopped ruling the waves for a long time already but maybe going forward it may be at the trough!

Sori! Corrected for typo:

All properties are in UK and the IPO is timed just before BREXIT! Personally I will refrain as I am rather pessimistic about the UK after Brexit. Britain have for centuries had clutches – first the colonies and in more recent times the EU. No doubt that Britainnica stopped ruling the waves for a long time already but maybe going forward it may be at the trough!

Haha I’m going to refrain from commenting until my final review on Elite Commercial REIT. Ultimately, it all goes back to pricing! Lousy properties at the right price becomes great investments, and great properties at a lousy price become lousy investments.

I think it’s quite a big deal that a the UK govt is a major (99%!) tenant. It changes up the risk dynamics quite significantly because we know that, at the very least, they won’t go out of business tomorrow. Knowing the efficiencies of governments, the risk of them moving out upon lease expiry (earliest is 3 years I think?) won’t be the same as with private companies. A wale of 8 years ought to provide stable cash flow in the long term, although the downside is that rental escalations only kick in in 2023. Will probably pick up a bunch since I’m looking at holding longish-term.

Haha, I guess the big question is what will these properties be worth 7 years into the IPO and the leases are up for renewal. Of course, if you’re planning to exit way before that, then this may not be an issue!

I skimmed the preliminary prospectus over the weekend and 3 things jumped out:

1. Most of the buildings are rather old, i.e. built in the 1980s or earlier. Not sure if this is the norm for commercial buildings in the UK, since their land is freehold.

2. The WALE is 8.6 years, but 70% of the leases can be broken in 2023, which is just 3-4 years away. Of course it says in the prospectus that they expect only a small percentage of the leases to be broken, but you never know.

3. 20% – 25% of the buildings are in Scotland. If Scotland chooses to leave the UK, there’s probably no reason for the UK government to keep leasing the buildings there.

Thanks for sharing your thoughts, this is helpful. I’ll add my thoughts once the final prospectus is out too. 🙂