Following my previous En-Bloc article targeted at a home-owner in her 60s, I recently received this question:

Hi Financial Horse, I am in a similar situation. I am getting a portion of the en bloc income which my parents will get from the en bloc sale of the condo we currently live in. I will be getting around 800k. Initially, I wanted to buy a condo as I thought private property was a good investment vehicle in Singapore, however that all changed after the Government released more tightening measures to clamp down on residential property investment.

So I already sourced for a very cheap HDB, which will cost around 600k, which I am planning to take up a 400k bank loan. Which effectively leaves me around 600k in cash, whilst I know that I am in an extremely advantageous situation at 25 years of age and having been exposed to investing through interest, I have never been given the responsibility of such a large sum of money and all of a sudden, it seems like the risk considerations would definitely differ in terms of my decisions purely because the quantum is so much bigger now.

I already plan to allocate the max allocations to SSB and a promotional fixed deposit plan which has a guaranteed return of 2.1%. These allocations will only take up 200k at most. I also plan to allocate some cash into new bond ETF that will be released in August. All these provides a comfortable base with relatively low risk in my perspective. Hence naturally I want into increase my equity exposure in hope of higher returns for wealth accumulation. The problem is there seems to be many signs pointing towards an impending recession, which makes me extremely hesitant in entering the equity with a large sum of money. One option I thought of would be to make a monthly investment into an ETF maybe at 5000 monthly. OR would it be prudent to hold large proportion (50%) of my portfolio in cash to enter when the recession strikes? I would really appreciate if you can shed some of your wisdom. Perhaps you can do the same article but this time targeted to the millennial who will be receiving a windfall from their parents property.

I was absolutely blown away by this question. So I took the time out to really ponder this question, and I penned the following open note, to this young reader after my own heart.

Dear Reader

You are in a massively advantageous financial situation, as from a financial perspective, it is akin to striking the lottery at the age of 25. This represents huge opportunity to achieve your financial goals, or to pursue other objectives in life. But at the same time, countless stories have shown that people who suddenly win a lottery more often than not end up bankrupt in a few years due to mismanagement of their finances. So while there is huge opportunity here, there is also risk if not managed properly.

Basics: Asset Allocation

Let’s take a closer look at your intended allocation. Essentially, it is:

| Asset | Amount | Percentage |

| Real Estate (Resale HDB downpayment) | S$200,000 | 25% |

| Cash (SSBs) | S$100,000 | 12.5% |

| Cash (Fixed Deposit) | S$100,000 | 12.5% |

| Remainder | S$400,000 | 50% |

In a previous article on the Ideal Asset Allocation for Singaporeans, I set out the following template as a base case scenario:

| Recommended Asset Allocation By Age – Base Case | ||||||

| Age | Years Worked | Stocks/REITs | Bonds | Real Estate | Cash Buffer (includes CPF OA) | Alternative Investments |

| 25 | 1 | 50% | 0% | 0% | 50% | 0% |

| 27 | 3 | 70% | 0% | 0% | 30% | 0% |

| 30 | 6 | 50% | 0% | 40% | 10% | 0% |

| 33 | 9 | 55% | 0% | 35% | 10% | 0% |

| 35 | 11 | 55% | 0% | 30% | 15% | 0% |

| 40 | 16 | 50% | 10% | 25% | 15% | 0% |

| 45 | 21 | 45% | 15% | 25% | 15% | 0% |

| 50 | 26 | 35% | 25% | 25% | 15% | 0% |

| 55 | 31 | 35% | 25% | 25% | 15% | 0% |

| 60 | 36 | 30% | 30% | 30% | 10% | 0% |

| 65+ | 41+ | 30% | 30% | 30% | 10% | 0% |

| Source: FinancialHorse.com | ||||||

Using this allocation, you are already at a massive advantage due to your windfall, which is why real estate as a proportion of your assets is quite low. From the table above, your situation will fall somewhere in the range of a 35 year old who has about 10 years working experience, which puts you about 10 years ahead of your peers in terms of financial maturity. Such a 35 year old would have about 55% of his net worth in stock/REITs, which applied to you, would mean that you should put all your S$400,000 into equity based investments. Unfortunately, the template assumes that one would have had 10 years to build up the necessary knowledge, experience, and also to average into the market. Would the analysis change if it were now a lump sum investment?

Lump sum investment vs dollar cost averaging?

You mentioned that you fear an impending recession. There’s little doubt that a recession will eventually come around, the only question is when. People have been calling for a recession since 2012, and those who have believed such calls have sat out an unbelievable bull run in equities. Which is why personally for me, sitting on a large cash position for an extended period is not an option (unless you need the money for a big ticket purchase). The rule that I employ for myself is to continually invest money that I have no immediate use for in the near term.

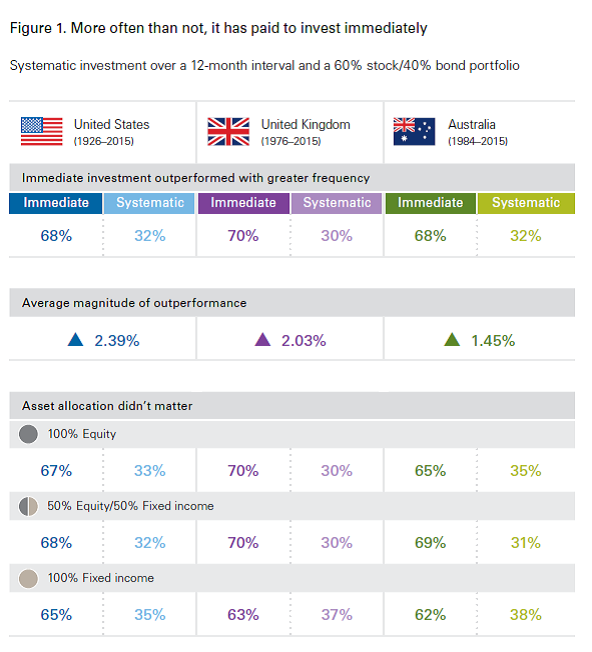

Vanguard did a great study on lump sum investment vs systematic investing that I recommend you take a look at. In particular, what they found was that on a historical basis, a lump sum investment tends to outperform a dollar cost average strategy, regardless of what asset allocation was employed.

They go on to add that:

Though the data demonstrate that immediate investment has, on average, outperformed, those who choose a systematic investment plan are likely more concerned about worstcase scenarios than averages or probabilities.

For investors with a large cash balance on hand, the stakes are high. Out of worry that an investment will quickly lose value, they may gradually ease into the market. Such an approach can minimize feelings of regret by providing short-term, downside protection against a rapid decline in a portfolio’s value.

…

And because there’s a risk that investors may begin to invest-—but fail to fully invest— the cash balance for a number of reasons (including potential feelings of regret), they will be left with a more conservative asset allocation for what can become an extended period of time—or forever. In turn, such an allocation would suggest lower future returns for a portfolio with a greater weight in cash.

So the problem we have here is this. Historically, lump sum investing tends to outperform dollar cost averaging 70% of the time. But a number of stock market metrics are all pointing towards valuations being at a record high, and chances are that we may actually be in the other 30% of the situation, as this Bloomberg article helpfully suggests.

But the problem with dollar cost averaging is the amount of discipline it takes to systematically make investments into the market every month on the same day for 12 month. It’s one of those things that sounds easy on paper, until real life gets in your way. Perhaps you are tired today and decide not to invest for this month. Perhaps the market tanks and you decide to wait a few days in the hope that it will drop even more. Human being are not robots, and I can guarantee you (from past experience) that executing a dollar cost averaging strategy when you have a lump sum to invest is much harder to execute that you can imagine. And don’t forget that in the interim, the cash being parked in a low yield account will also be losing value to inflation every day.

So I know that this may be controversial and not everyone is going to agree with me, but if I were in your situation, I would take the S$400,000 and invest it completely into the equity markets over the next 2 to 3 months.

Protecting your downside

The other part of this equation, is to limit your risk. Remember when I mentioned that I will only invest money I do not need in the near term?

Unfortunately in this case I have no indication as to how much savings you have, or your current income. If I assume that you are an average 25 year old Singaporean, you probably graduated from university 1 or 2 years back, and with 1 or 2 years work experience you are probably drawing a S$3,000 to S$5,000 salary. Assuming a S$1,000 monthly expenses, and a S$1,500 monthly mortgage repayment (on the S$400,000 loan), that works out to be S$2,500 in expenses a month on average. So if you lose your job tomorrow, and assuming you have no other savings at all, the S$200,000 cash position is enough to support you for 80 months, which is about 6.5 years. So there is conservative, and there is zombie apocalypse-prudent. This massive cash position is definitely skewed towards the latter.

Don’t forget that in reality, I suppose you are living with your parents, so the resale HDB is being rented out to generate rental income. You are also working a day job, which is more than sufficient to support your lifestyle. So you can actually get by on a day to day basis (and save up money) without eating into either your S$200,000 cash, or your S$400,000 investments. This to me indicates that the S$400,000 is money that you can afford to lose, and for that reason it should be invested completely.

What would Financial Horse do?

I actually get that I am talking about this in abstract. It sounds easily when you’re talking about arcane figures like that, but actually sitting down in front of your computer and entering buy orders for up to half a million dollars worth of stocks is not exactly the easiest thing in the world. But that’s exactly what I would do. Over a long 20 to 30 year period, no other asset class will come close to stocks or real estate in terms of potential returns. So yes, the market may be on a high now. But when you invest in equities long term, you are investing not in the moods of other investors, you are investing in the collective improvement in earnings of the entire market. Technological progress, and the advancement of the human race is inevitable. There may be short term hiccups, but as long as you stay invested, and don’t panic sell, you will be fine. And with a S$200,000 cash buffer, you should be better placed than anyone else to weather the storm.

The next question then, is what stocks should you buy? I could easily talk about how for retail investors the best way to invest long term is to buy a broad based index fund and forget about it. But you mentioned that you have an interest in investing, and from your entire letter, you seem to be a well-educated and prudent young millennial. A man (or woman) after my own heart indeed! So I will accord you the respect you deserve and not dumb this down. Rather, I will share with you my own personal investment strategy, and you can decide if you would like to follow this fellow millennial.

And my strategy is this:

1. Despite all the uncertainty over the trade war and the talk about this being the Asian century, the US market is still too dynamic and competitive for any investor to avoid. For young investors like me, I can afford to take the risk, so I allocate a 40% allocation to the US equities. Within this I hold a bulk of them in ETF positions (SPY and QQQ), while I use the remainder to take positions in specific counters that I like. I’ve been a huge tech nut since I was young, so I have a relatively stronger grasp of the industry (as compared to something like healthcare), so I typically deploy my remaining capital into tech counters. Passive index investing is boring as hell, and I find that this gives me an outlet to take positions in counters I like, so that I don’t get restless and touch my ETFs.

2. That being said, as a Singaporean investor, it is not prudent to take on excessive forex risk, given that we ultimately live in Singapore and spend in SGD. For that reason, I deploy the remaining 60% of my capital in the Singapore market. I don’t like the STI or REIT ETFs, for reasons I catalogued previously. As such, there is no shortcut to stock picking in Singapore.

Unfortunately, I’m not particularly enamoured on any single Singapore company, so I simply hold positions in the local banks to gain broad exposure to the economy.

At the same time, I am a huge believer in the Singapore REIT market. I truly believe that the Singapore REITs are the most competitive in all of asia, and no other market comes close. For this reason I am heavily invested in S-REITs (in fact, the bulk of my Singapore capital is in REITs). You can take a look at my previous article on what to look out for when it comes to picking REITs, but as a general note, only stick to those from strong sponsors such as Mapletree, CapitaLand, Frasers, CDL etc. You’ll thank me for that later.

3. The problem with this strategy of course, is that the exposure to the Asian economy is largely through Singapore companies, which from a diversification perspective, is not entirely prudent. So if you are so inclined, you can buy a broad EM ETF such as the VWO, which should theoretically address that issue somewhat.

Closing Thoughts

So there you have it, what Financial Horse would do if I were in your situation! The other thing that I haven’t touched on so far, is what receiving S$800,000 when you are 25 can do to your outlook on life. Few people are in a situation as advantageous as the one you are currently. Yet this situation affords you great opportunity. A lot of people are stuck in their day jobs simply because they need the income. For your situation, you can quit your dayjob, take S$100,000 out of your portfolio, and travel the world, start a business, study for an MBA, live in Europe for a year, anything that you’ve always wanted to do but never got the chance to. Life is short, and there is plenty of time to earn money back. When you are older, you will never remember the one year that you spent at 25 working for a salary. But you will never forget the one year you took to travel the world. You don’t have to do it now, but perhaps when you are older you may discover a passion you always wanted to fulfil, and you can do it then.

To quote a recent article I was reading: “In this unexpected outcome there is an important lesson that even Hetty never learned—no matter how you much money you acquire in life, you can’t take it with you. No matter how hard how you work, no matter how much you save, one day it will all end. As one of my favorite speeches about getting rich concludes, “It all goes back in the box.”

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Brilliant article. Take the money and invest or do something for a young 25 year old guy instead of stuffing the money in the bank. You have a lifetime to make money.

Hi financialhorse, I was camping daily for your response and when it finally came out, i was absolutely blown away by your response and the amount of thought and effort that was put in, it definitely provided new perspectives for me in my situation, and it definitely answered my questions wrt to lump sum vs dca and of course added value to my life. I ploughed through many of your posts before garnering the courage to ask you what i asked and i am so glad that i did. I have many other questions to ask as a result of this article but I shall not make you feel obligated by throwing these questions on you haha. Instead I really want to thank you for what you do for this blog as I will be a loyal follower for sure.

Hi Young&Hungry,

Wow, thanks very much for reaching out. You are in an absolutely fantastic position for a 25 year old, and I must congratulate you both on the good fortune, and on the wisdom is managing your money properly. I truly believe that you are many years ahead of your peers financially. But that being said, after a certain point, money just becomes another number, and more money doesn’t necessarily make you a happier person. So I would encourage you to discover what you want out of life, and to pursue something that gives you greater meaning.

Feel free to let me know if there are any issues you want me to elaborate on! I love hearing from readers, and I’m always searching for great new topics to write on. 😉

Cheers!