A couple of you have reached out to ask for my thoughts on the proposed merger between ESR REIT and ARA LOGOS Logistics Trust.

I finally got around to taking a look at this merger, and it’s a pretty interesting one.

So I wanted to take the opportunity to share my key takeaways.

What is going on: ESR REIT is acquiring ARA LOGOS Logistics Trust?

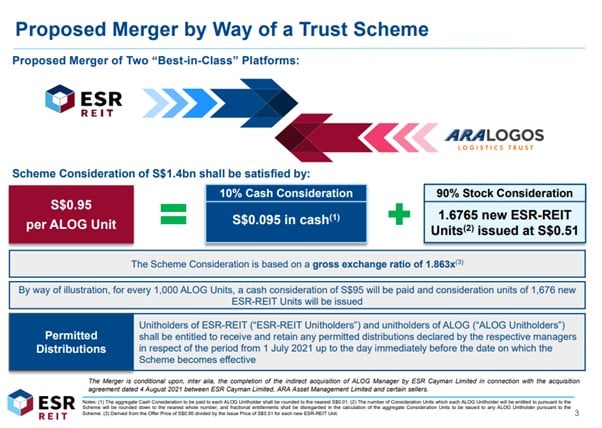

Very simply, ESR REIT is acquiring ARA LOGOS Logistics Trust.

ARA LOGOS Logistics Trust unitholders will get:

- $0.095 in cash

- 6765 new ESR REIT Units issued at $0.51

Totalling a consideration of S$0.95.

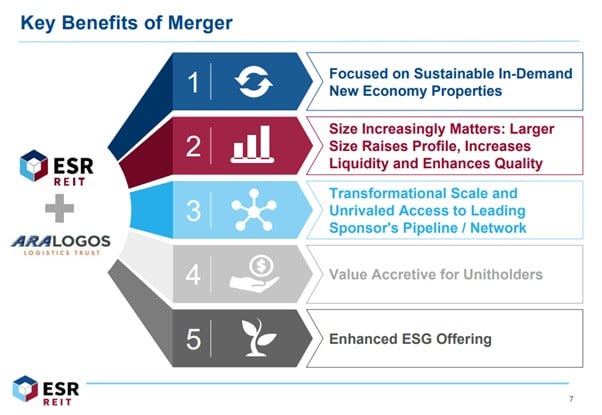

The benefits of the merger / acquisition of the 2 REITs are broadly:

- Economies of scale

- Bigger size

- Increased exposure to new economy and freehold properties

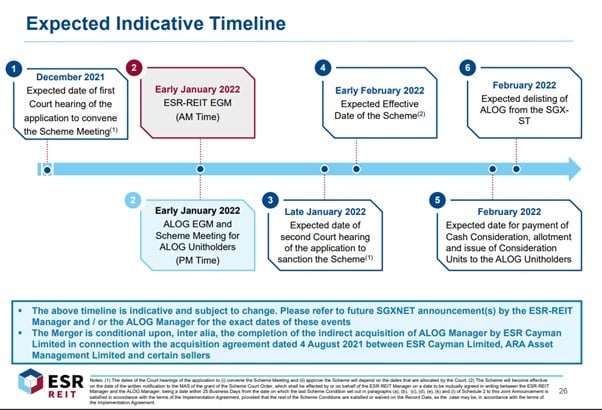

The timeline is set out below.

If all goes well, the EGM to approve the merger will be in early Jan, with the merger to complete by February 2022.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

A bit of background about ESR REIT

ESR REIT has been very aggressive with acquisitions.

In fact their Sponsor, ESR Cayman, is merging with ARA Asset Management as we speak.

A few years back, ESR merged with Viva Industrial Trust, and also attempted a takeover of Sabana REIT.

Merger with Sabana REIT failed

However, the merger was rejected by Sabana REIT unitholders, in a rare moment of shareholder activism for the local exchange.

It was all very exciting stuff, extract from Straits Times below (emphasis mine):

Investors in a Singapore real estate investment trust (Reit) voted down a merger with a larger rival on Friday (Dec 4), in a rare win for shareholder activism in a market dominated by retail investors.

…

The activists had said the deal between Sabana Reit and ESR-Reit, whose managers are both owned by a unit of Asian logistics giant ESR Cayman, had undervalued Sabana Reit.

“This is the first time in the 18-year history of Singapore Exchange’s Reit market that a proposed merger has been voted down,” Quarz Capital and Black Crane said in a statement.

…

Quarz Capital had proposed Sabana Reit and ESR-Reit merge last year in a cash-plus-stock deal that would value Sabana Reit at 54.5 cents a unit, while Black Crane had voiced concerns about Sabana Reit’s market valuations.

When both Reits announced an all-stock deal in July – just as the pandemic pummelled the sector – valuing Sabana Reit at $397 million or 37.7 cents a unit, both activists rejected it.

They said last month that Sabana Reit had failed to close the net asset value discount and had recommended “a value destructive merger with a Reit controlled by its owner.”

To press their point, the funds set up a website called “Save Sabana Reit” stacked with presentations against the merger, sent letters to management and held webinars to win over retail investors.

They also sought regulatory intervention to disallow ESR Cayman from managing both Reits if the merger fails, although the central bank has said there are no rules restricting such arrangements.

What was my initial reaction? Deal favours ESR REIT over ARA LOGOS Logistics REIT?

Full disclosure – I am not a unitholder of either ESR REIT or ARA LOGOS Logistics REIT. So I have no skin in the game, and take everything I say with a pinch of salt.

My initial reaction looking at the merger was that the deal marginally favoured ESR REIT, but only by a little.

You can take a look at the charts below.

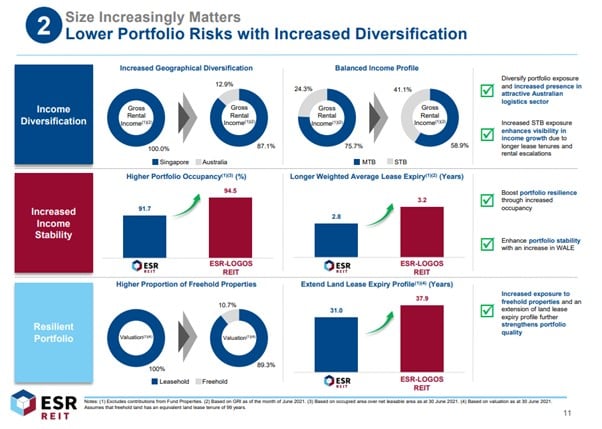

By completing the merger, ESR REIT will increase its exposure to the new economy properties of High Specs Industrial and Logistics / Warehouse. While increasing its proportion of freehold properties, its Weighted Average Lease Expiry (WALE), and Lease Expiry Profile.

The only way this makes sense, is if ARA LOGOS Logistics REIT’s portfolio itself has a higher allocation to High Specs Industrial and Logistics/Warehouse, more freehold properties, longer WALE, you get the idea.

Suggesting that ARA LOGOS Logistics REIT has a superior property portfolio.

ARA LOGOS Logistics Trust trades at about 1.2x book value, while ESR REIT trades at around 1.1x book value, which kind of backs up this observation.

What was the market reaction?

The market reaction upon announcement was very interesting:

- ESR-REIT climbed as much as 5.4 per cent or S$0.025 to S$0.49

- ARA Logos dropped as much as 5.9 per cent or SS$0.055 to S$0.88

Which indicates the market also thinks the merger favours ESR REIT at the expense of ARA LOGOS Logistics REIT.

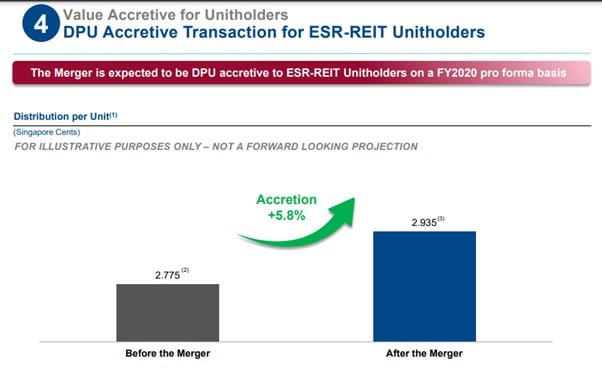

Value Accretive for ESR REIT?

Apparently, the deal is DPU accretive for ESR-REIT unitholders (5.8%).

ESR REIT issued a full list of FAQs, well worth the read if you’re invested.

They shared this very interesting nugget of information:

The DPU accretion of 5.8% to ESR-REIT Unitholders (on a FY2020 pro forma basis) is driven largely by the following factors:

- Refinancing 100% of ALOG’s borrowings at lower financing cost: The new banking facilities have a lower weighted average “all-in” finance cost of 2.25% per annum versus ALOG’s existing “all-in” financing cost of 2.92% per annum as at 30 June 2021.

- Reduction in land rent expenses: As shown in the pro forma financials, assuming the land premium has been paid upfront to JTC, ESR-LOGOS REIT will not incur any land rent expenses for the ALOG SG Real Properties in FY2020 amounting to approximately S$5.6 million (representing c.6.4% of the estimated upfront land premium). As the estimated upfront land premium is expected to be funded by the new banking facilities which has a lower cost of debt of 2.25%, this translates to cost savings for unitholders and as such, DPU accretion.

In other words, the DPU accretion is driven largely by (1) refinancing ARA Logistics Trust’s borrowings, and (2) by paying the land premium to JTC upfront instead of monthly.

Which begs the question – why didn’t ARA LOGOS Logistics Trust do this themselves in the past, to enjoy the DPU accretion?

Not sure if I’m missing something, but none of these are dependent on the merger?

Merger is NAV dilutive for ESR REIT

The merger is also NAV dilutive for ESR REIT.

This was the response from ESR REIT’s FAQs (emphasis mine):

Why should we support the Merger given it is NAV dilutive?

- While the Merger is NAV dilutive, the Merger allows ESR-REIT to increase its proportion of freehold Portfolio Properties to 10.7% while also increasing its land lease expiry profile from 31.0 years to 37.9 years. A larger portion of freehold assets and longer land lease expiry profile will reduce the decline in NAV per unit over time driven by land lease expiry of JTC industrial land that is under a fixed 30-year lease tenure.

- An enlarged ESR-LOGOS REIT with a stronger financial profile (e.g. more competitive cost of financing and longer WADE) and access to wider pools of capital (e.g. perpetual securities and bond markets) will have greater flexibility to pursue the acquisitions of assets with either freehold land or longer land lease tenure to further prevent the reduction in NAV per unit over time due to land lease expiry of the shorter 30-year lease of JTC industrial land.

- Post-Merger, the enlarged size of ESR-LOGOS REIT also accelerates the ability to divest the non-core assets to balance the expected NAV per unit dilution over time.

- As a result, ESR-REIT Unitholders should evaluate the transaction objectively and, in its entirety on the basis of the longer-term commercial merits that could be achieved from this Merger.

Which again seems to point back towards the fact that the deal is good for ESR REIT because it absorbs the ARA LOGOS Logistics Trust portfolio, which is superior because it has a larger proportion of freehold properties and longer land lease expiry profile.

I suppose you would argue that for ARA LOGOS Logistics Trust unitholders they get a larger AUM and hence better liquidity, but I leave it up to you to decide if that’s worth it.

My Personal View on the ESR REIT Merger with ARA LOGOS Logistics Trust:?

Gut feel for me is that this is a 1 + 1 = 2 transaction.

Sure the merger might be marginally better for ESR REIT unitholder, but it definitely isn’t so imbalanced to the point of Sabana REIT, where unitholders would band together to kill the merger.

I can see why they want to merge both REITs though, especially since ESR Cayman and ARA Asset Management are going to merge.

It’s like after CapitaLand and Ascendas merged, and Ascott REIT was merged with Ascendas Hospitality Trust.

Similar logic here. Can’t justify keeping 2 CEOs and 2 CFOs and 2 Investor Relation teams, when both are owned by the same Sponsor and hold industrial properties.

That said, it’s hard to see big value emerging from this merger.

Putting together the portfolio from ESR REIT and ARA LOGOS Logistics Trust to me is a 1 + 1 = 2 transaction.

The properties don’t magically go up in value by 50% overnight simply because they’re owned by the same REIT.

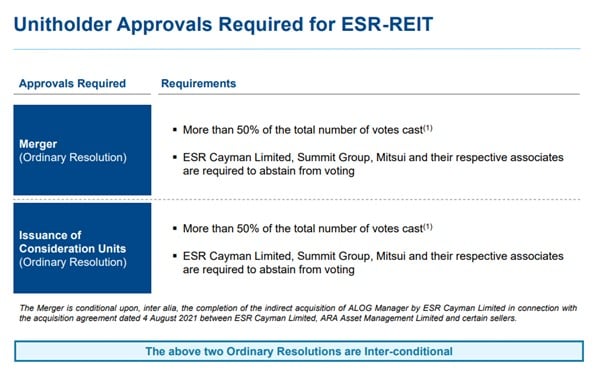

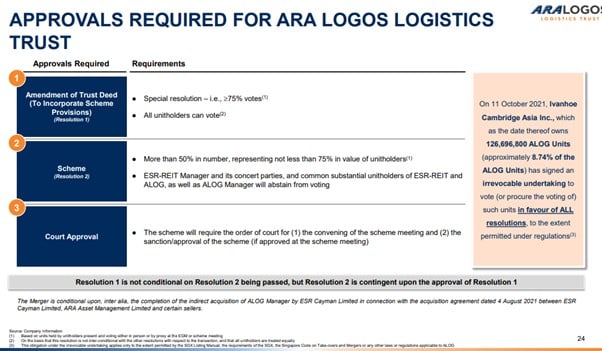

Should unitholders vote in favour of the merger?

ESR REIT requires 50% of unitholder approval, with the Sponsor unable to vote.

ARA LOGOS Logistics Trust requires 75% approval, but Ivanhoe who controls 8.74% of the units has already committed to vote in favour for the transaction.

If I were an ESR REIT unitholder, I’ll likely vote in favour of the transaction. Looks like a good deal to me.

If I were an ARA LOGOS Logistics Trust unitholder, I’ll be a bit more on the fence. Whether it goes through or not, doesn’t really make a difference to me.

But that’s just me, and like I said, I don’t own a stake in either REIT.

Closing Thoughts: More Mergers coming for ARA Sponsored REITs?

Just this week, ESR Cayman shareholders approved the acquisition of ARA Asset Management.

With the Sponsors merging, it definitely makes sense for both industrial REITs to merge as well.

ARA has two other Singapore REITs, Suntec REIT and ARA US Hospitality Trust.

Perhaps some other “synergies” might be coming soon there?

As always, this article is written on 6 Nov 2021 and will not be updated.

For my latest views, including my full portfolio and stock watch (including REITs), do check out Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Well-written post. You may want to correct the Sabana Industrial REIT name, you typo it as Surbana REIT. I have noticed many have (including banks) mentioned that ARA is the sponsor of Suntec REIT, however, can’t get this officially from the website or annual report.

Thanks for the spot! Have corrected this. Yes ARA is the sponsor, they do state it on their website: https://www.ara-group.com/businesses/reits/suntec-reit

The ARA website merely mentioned the REITs they managing. No info from the Suntec website, annual report, or quarterly report. Even the SGX monthly REIT report also shows its sponsor as “Suntec Development” instead of ARA. But ALOG and ARAHT did mention ARA as sponsor though. I could be way wrong, just raise it for info.