After last week’s article on Grab, an overwhelming number of you asked for my thoughts on Facebook (Meta) stock.

Facebook’s high in September 2021 was $384.

At yesterday’s $219, Facebook has fallen 42% from its high.

That’s almost $450 billion in market cap wiped out in 4 months.

Is Facebook the screaming buy of the year? Or value trap?

Why did Facebook drop 25% after earnings?

2 big reasons:

- Declining Users

- Slowing Revenue Growth due to

- Apple’s App Tracking Transparency (ATT)

- Competition from Video

1. Declining Users

At this point, literally everybody and their grandmother has a Facebook account.

And it’s starting to show.

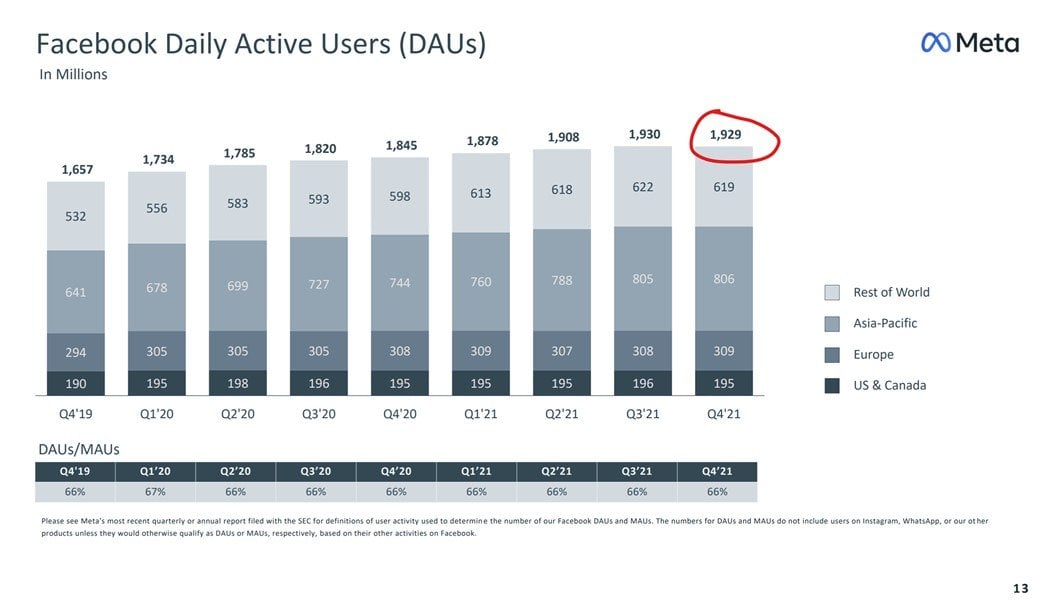

For the first time ever, Facebook Daily Active Users declined – from 1.93 billion to 1.929 billion.

It’s a small decline, but the symbolism was not lost on investors.

Is this the start of the end of Facebook?

Facebook is no longer “cool”

A lot of the younger kids are moving over to Tik Tok.

Sure, Whatsapp and Instagram are still relevant, but it remains to be seen if they can monetise at the same rates as Facebook.

Whatever the case, the days of breakneck user growth are over.

Going forward, the focus needs to be on increasing revenue per user.

Value extraction, rather than value creation.

2. Slowing Revenue Growth

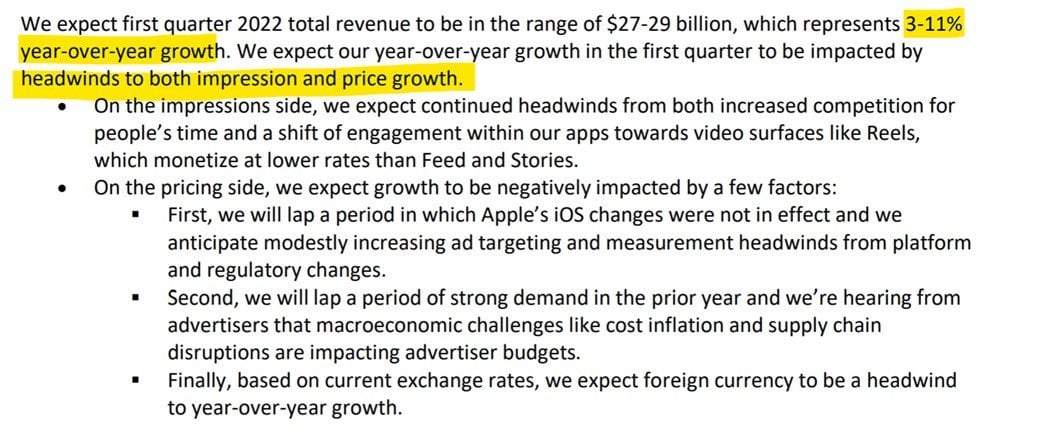

For Q1 2022, Facebook’s forecast is for only 3 – 11% year on year revenue growth.

That’s a massive drop from the past when Facebook grew at 35% each year.

Facebook cited 2 main reasons:

- Apple’s App Tracking Transparency (ATT)

- Competition from Video

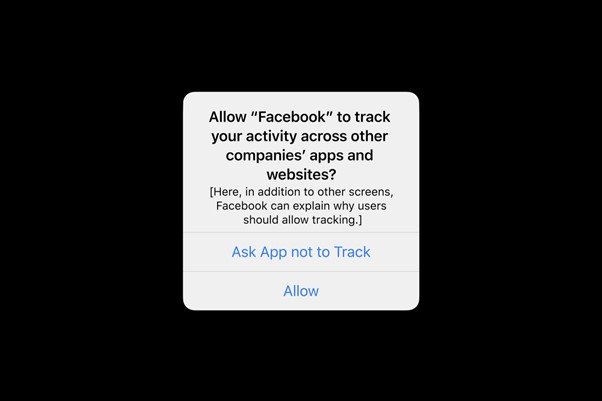

a. Apple’s App Tracking Transparency (ATT)

From The Verge:

The feature, introduced in iOS 14.5, is meant to prevent app-makers from tracking what you do and selling that information to advertisers. Companies like Facebook cried foul when it was introduced, saying that it would hurt their ability to show targeted, personalized ads, and therefore hurt businesses that relied on those ads.

Apple’s App Tracking Transparency is basically this box below:

If you click no, Facebook (or any other app developer) can no longer track your activity across other apps and websites.

According to Facebook, this has impacted their ability to track users, and deliver targeted ads.

Lower ROI for Ads = Lower Revenue

Spin it whatever way you want, but Facebook is an advertising company.

They make money by selling ads to advertisers.

And what advertisers care about, is their return on investment.

Let’s say I’m Nike.

For every successful customer I get, I make $20 from him.

This means that I can spend up to $20 in ads, and still make money.

The problem with the apple changes, is that Facebook ability to target ads is affected.

Facebook can no longer track that I am browsing Nike shoes on Shopee, and show me Nike ads.

This reduces the efficiency of the ad. Instead of spending $20 to get a customer in the past, I may now need to spend $25.

So the ROI drops, the ad no longer makes economical sense, and I may take my ad dollars to Tik Tok or Google instead.

Are Facebook Ads still relevant in 2022?

Stratechery has a great article on the competitive landscape for Facebook that is worth reading if you’re serious about Facebook.

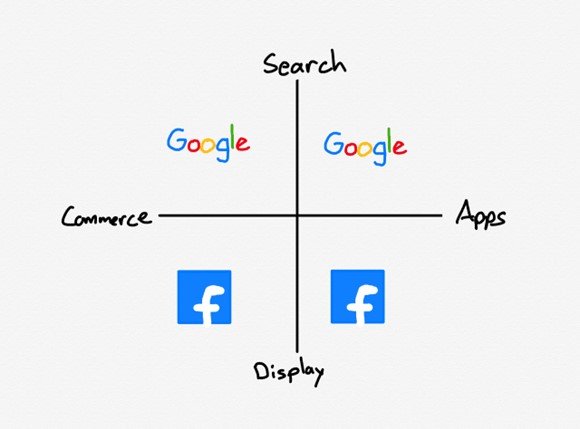

To sum up – This is what that market looked like back in 2016.

There were only 2 players back then.

Google if you want to use search, and Facebook if you want to use display.

Search is for high intent advertising. People going to google to search for “Buy Wine Singapore” know exactly what they want.

Display on the other hand is more open ended. People scrolling through Facebook don’t know that they want a pair of Nike shoes, until they see that great display ad.

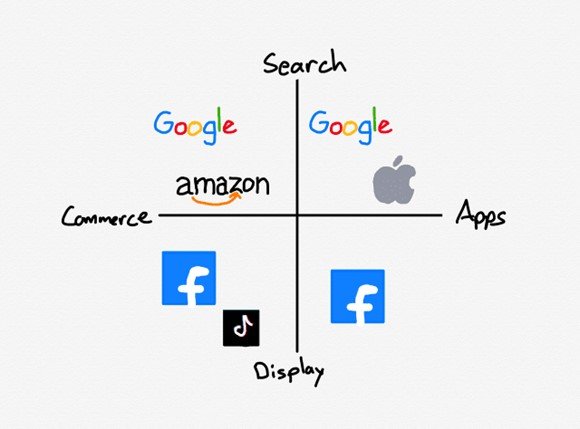

b. Competition from Video

Which brings us to the next problem – Video.

Remember that with Display Ads, the key commodity you need to command is attention.

Once you have user’s attention, you can then show them ads, and monetise it.

Video is all the rage now, and Facebook is probably the worst positioned for video.

Google has Youtube, while Bytedance has Tik Tok.

Facebook understands this problem, and they’re rushing to develop Reels which is a short form video format.

But during this transition period as Facebook pivots to video, Reels will not monetise as effectively as Feed or Stories.

For investors, this introduces uncertainty in the sense that you don’t know whether (1) Facebook can do video effectively, and (2) will video monetise well?

So this is the competitive landscape in 2022: where Tik Tok is muscling in on Display Ads.

Sure, Tik Tok is a small player now, but back in 2012 so was Facebook.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Is Facebook the weakest FAANG?

Think about it this way.

Google has Search and Android.

Amazon has logistics, fulfilment centers and AWS.

Microsoft has Microsoft Office and Azure (and now a very solid gaming arm).

Apple has iPhone and iOS.

Facebook has… a Facebook app?

Of the FAANG, you can argue that Facebook is the weakest player with the weakest moat.

As Facebook is just an app, they are incredibly dependent on iOS and Android, and so far Apple has demonstrated a willingness to exploit this dependency.

My personal take on Facebook’s core business

For what it’s worth – My personal take is that most of the short term woes are probably overblown.

Facebook will not fade away overnight.

They are still an advertising juggernaut, with $25 billion in revenue a quarter.

There is virtually no other advertising platform around that is this effective at display advertising, and which offers this amount of targeting.

If some advertisers go away, more will come to fill the void. Facebook made possible a whole new wave of Facebook native retailers, and I don’t see that changing any time soon.

Video is a problem, but I’m confident they will be able to navigate the issue, just like they did in the past with Mobile, Feed and Stories.

Zuckerberg is a shrewd executor, backed by the best talent money can buy (and not held back by traditional silicon valley norms).

What about the longer term outlook for Facebook?

Where I get a bit concerned, is the longer term.

If you look 3 – 5 years out – let’s say Facebook’s popularity continues to wane.

More people move to Tik Tok, or whatever app comes after Tik Tok.

What next?

Where is the long term moat to protect Facebook over a 5 year horizon? Where is next $10 billion a quarter going to come from, 5 years from now?

Put in this light, you kind of understand why Zuckerberg keeps talking about the Metaverse.

Of course it may not succeed, but you still have to try.

Can Facebook pull off the Metaverse?

Some of you have asked for my views on the Metaverse, given that Facebook is pouring $25 billion a year into it.

The view of this simple horse is that I do believe the metaverse will eventually be built. It’s a logical extension of the internet, and a natural evolution for a generation of users who grew up in online gaming worlds.

But whether it’s going to be Facebook to dominate the metaverse, that I’m much less certain.

Among the other FAANG, Microsoft has already made a good claim with their big purchase of Activision Blizzard and all the valuable IP that comes with it.

And from a philosophical perspective, the community is more inclined to coalesce around an open source, decentralised version of the metaverse rather than one controll by Facebook.

So the metaverse will probably be built, but Facebook’s role, and their ability to monetise, is much less certain.

Adverse Macro Environment

The problem with a stock like Facebook is that earnings is just 50% of the story.

The other 50% is macro.

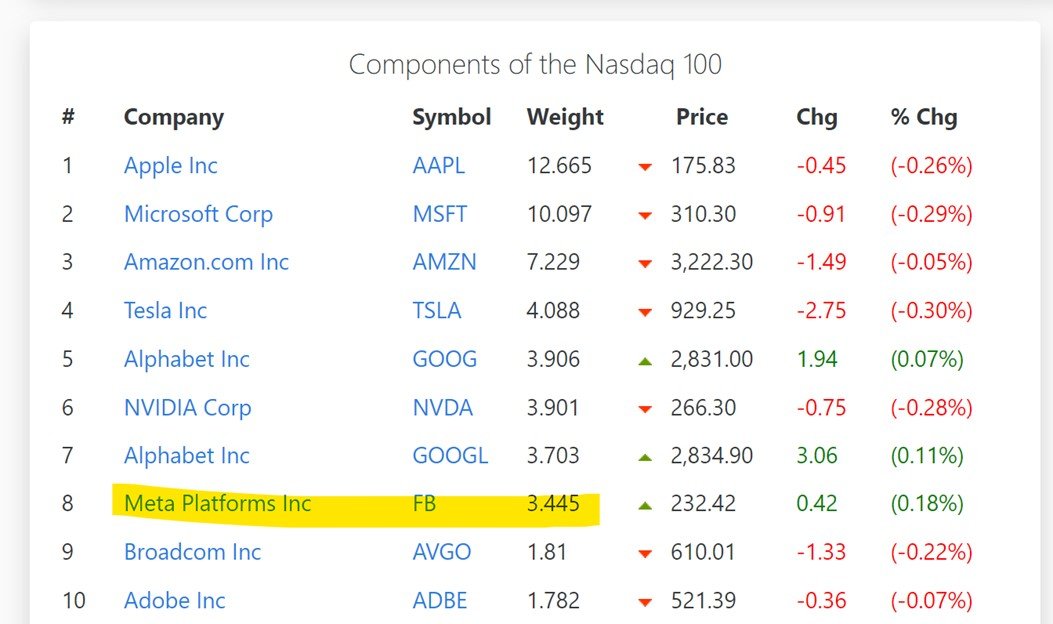

As a member of the FAANG, Facebook makes up 3.5% of the NASDAQ.

This makes it very vulnerable to passive index flows. This same dynamic that pushed Facebook up the past 10 years, can reverse in the short term if there are macro outflows.

I’ve been complaining about the macro for week after week now, so am not going to belabour the point.

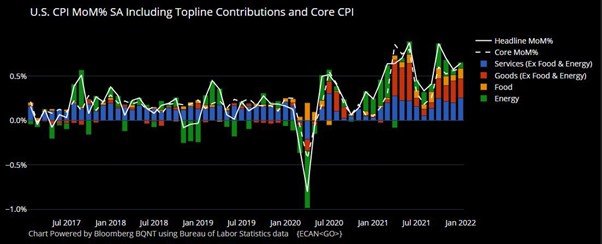

What I would add though, is that the latest 7.5% CPI print for the US is very troubling.

If you look under the surface, it shows that inflation is starting to get more entrenched. Services inflation is picking up, and goods inflation not coming down. We’re also starting to get more entrenched wage spiral increases.

This means that the Feds are going to be forced to do even more if they want to bring inflation under control.

Just like you didn’t want to fight the Feds the past 2 years, it doesn’t make sense to fight them here as well.

Feds are going to have to tighten monetary conditions this year, which could bring a lot of pain for risk assets across the board.

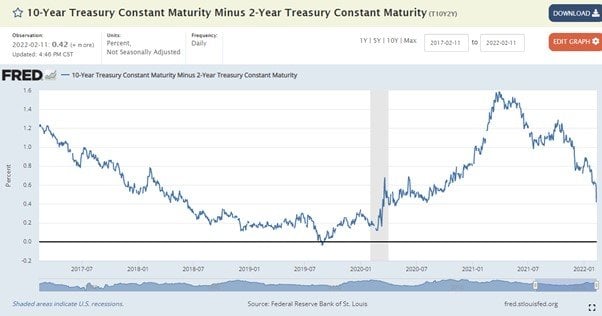

Just look at the 2s10s yield curve – it’s starting to point towards economic slowdown and recession.

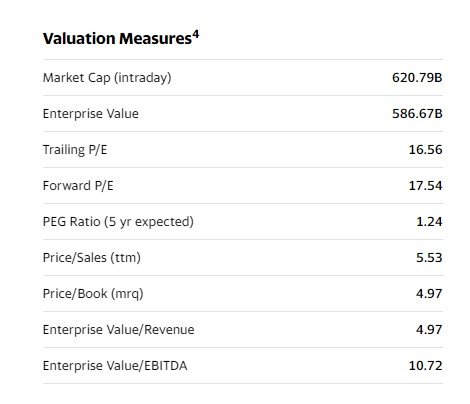

Valuations for Facebook (Meta) Stock are dirt cheap

That said, there’s no denying that valuations are cheap.

PEG at 1.1 is the cheapest of the FAANG.

And PE at 16 makes it look like an old world company, when this is actually a FAANG with 10%+ revenue growth.

Will I buy Facebook (Meta) Stock at $219?

Full Disclosure that I hold Facebook stock bought from years ago (still comfortably in the green after the drop), and I also have indirect exposure via the NASDAQ ETFs I hold.

I still think from an earnings perspective, the short-term woes are overblown.

Yes user growth is slowing, but it’s slowing from 2.8 billion users.

If you take out China, the young and the old, there’s literally nobody left to be onboarded on Facebook.

Apple’s iOS changes are a problem and will hurt ad targeting, but at the end of the day, if you’re a display advertiser and you want to drop Facebook, where do you go?

Google is search which cannot replace display ads, and Tik Tok doesn’t have the kind of targeting or broad reach to rival Facebook just yet.

Video is a problem, but in Zuckerberg you have a shrewd operator who has successfully navigated these challenges in the past.

So I think the short term doomsday picture for Facebook earnings is probably overblown.

What concerns me though, is the macro climate, and the longer-term outlook for Facebook.

Timing wise I’ve always said the time to buy is when the Feds switch their stance, and we’re nowhere near that yet. Heck, we haven’t even had the first rate hike.

And longer term, Facebook has the weakest moat of the FAANG. Facebook is ultimately just a social app with network effects, whereas the other FAANG tend to have more tangible real world moats.

There’s no denying that valuation is dirt cheap of course.

But in a year with rising rates, how do you really model “fair value” for Facebook?

Know when to swing, and when not to

There’s this quote from Warren Buffet that I absolutely love.

“The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, ‘Swing, you bum!,’ ignore them.”

The lesson for investors, is that you don’t have to swing at every pitch.

There are unlimited opportunities in the market.

But as investors, we have limited resources.

There’s no need to buy every “bargain stock” that comes by. Bide your time, wait for the sweet spot, and swing hard.

Sure you may miss out on some gains, but as long as you focus on your process and manage risk, longer term you still make money consistently. And it’s the consistency that really matters.

Facebook for me – It’s probably a decent buy, but not necessarily one that might be right for me. If it goes even lower sure, but if it doesn’t I’m happy to just hold my existing position and my QQQ.

I just think from a macro perspective, rising rates and QT in 2022 are going to create a lot more buying opportunities.

For those who are keen, you can view my full portfolio and the stocks I am keen to buy on Patreon.

Closing Thoughts: Is Mark Zuckerberg engineering this crash?

We talked above about how Facebook is moving from the value creation to value extraction phase.

Whenever that happens, the regulators usually want to come after you.

Think Alibaba or Tencent.

So Facebook is facing a ton of problems with US regulatory authorities, including a potential forced reversal of the Instagram merger, which would be an absolute disaster. Long shot yes, but don’t forget they’ve been ordered by the British regulators to sell Giphy.

There’s one way to see it which is that Facebook is intentionally sandbagging its guidance and overplaying the competitive effect of TikTok and Apple, in order to get regulatory authorities off their back.

This being Mark Zuckerberg, I wouldn’t rule out this possibility entirely.

In any case – I wanted to leave you with this chart. Look at how closely Facebook tracked the Nasdaq (purple), until this month.

Will Facebook catch up to the purple line, or will the purple line catch down to Facebook?

As always, this article is written on 12 Feb 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Fb is boomers network. Probably will grow old and die with its users.

Gen z is joining instagram and tiktok. Whatsapp monetization is almost nonexistent. Instagram also so-so. I will probably just sell and invest in the next big thing. If tiktok copies fb /instagram with chat and feed, the stock will drop more, like u said very weak moat. Used to think social has wide moat but no longer

Well the short term earnings should still be strong. But longer term, what you mentioned is a real concern.

Hmm short term wise macro environment also not good. Things can also change pretty fast short term. Like the meteoric rise of tiktok in just 3 years.. the fastest social media to reach massive revenue and billion users. I would not touch fb at all. I would have cashed out near the peak.

Plus meetaverse is a big risky bet. How to monetise meta verse ? Thats the big qn. Sell goggles? Sell more expensive ads in virtual world? How many will buy the goggles? Most of fb users quite poor in developing countries.. Go into gaming? Dont think these will make a dent in the revenue… if say $5bn additional revenue from selling goggles that’s only 5% growth. Gaming is also very competitive . And gamers usually wont use Fb and real names to play games , a big turn off.

Remember libra and crypto? Hyped so much. In the end gone case. Remember google glass? Also dead. Lol. I bet this meta verse will be underwhelming. Maybe it will be more exciting for gamers. I really dont see companies buying one goggle for each employee just so they can meet in virtual world LOL. What’s the value proposition?

Hey FH, great article as usual! I absolutely agree with your macro analysis along with the financial headwinds that Meta will face in the short term.

However, just providing an additional perspective here as a software engineer – I think many observers are unaware of the internet reach that FB has, unless they’re in the tech space. Many of our modern websites are built with technologies that FB actually developed and made open-source: React.js & Redux (a very popular front-end stack for websites), GraphQL (a query language for graph databases which is getting highly popular). It remains to be seen how they can directly monetise their open-source releases, but the sheer popularity of their technologies is a testament to their engineering prowess. This also means that it is easy for websites to interact with FB’s API (native support through React) – granting them more reach across the Internet.

PyTorch is also a highly popular deep-learning library that was developed by FB (c.f. TensorFlow by Google) – so I wouldn’t discount their dominance in the ML and computer vision space yet.

I’m personally keeping an eye on FB myself! Not really bullish on their ad revenue growth, but more of what else they can innovate and bring to the table in the years ahead 🙂

Thank you! That’s really interesting, appreciate the sharing from a different perspective.

How are they going to monetise the opensource? Like mongodb? Burning lots of cash? Red hat linux?

These opensource wont make a dent — precisely why they open source in the first place. A lot of the code is their internal code repackaged to be opensource. They do opensource for various reasons: attract talents, give back to the community , influence the dev world but definitely not to be a substantial biz.

Developing frameworks dont make them ‘dominant’ in ML space lol. Its HOW they use it, ie, the algos that matter most. You need to see from investor perspective. Plus if their core biz is suffering or slowing down, they might not continue pouring as much resources into opensource. You sound like a naive noobie investor conflating things.

https://www.joelonsoftware.com/2002/06/12/strategy-letter-v/

Have fun reading this – funnily enough, I do think you’re very short-sighted and naive on the workings of open source software. FH has already given an in-depth review of the financial side of things; while I’ve offered thoughts on how they could use their tech to create new revenue streams in the years ahead.

Feel free to disagree with me, that’s what makes a market anyway. We’ll see in the years ahead~

And I’ll further add on, from reading your replies to another user above, that all of what you’ve said is public information that has seen much media coverage.

I too am cautious about their metaverse ambitions, but alpha is generated when an investor spots something before the wider public acknowledges it. (which is just another example of k-level cognitive theory at play).

Would the stock trade sideways or underperform in the short term? Very possibly. But at such attractive valuations, a solid cash generating business with potential technological upside, I’m placing a bet for the medium-term rebound for this.