Earlier this year – Frasers announced that they were going to privatise Frasers Hospitality Trust at $0.70.

Back then, I thought the timing was very convenient (I mean they chose to privatise a hospitality REIT right before COVID reopening).

But in all fairness, I also thought that the $0.70 being offered was a very reasonable offer.

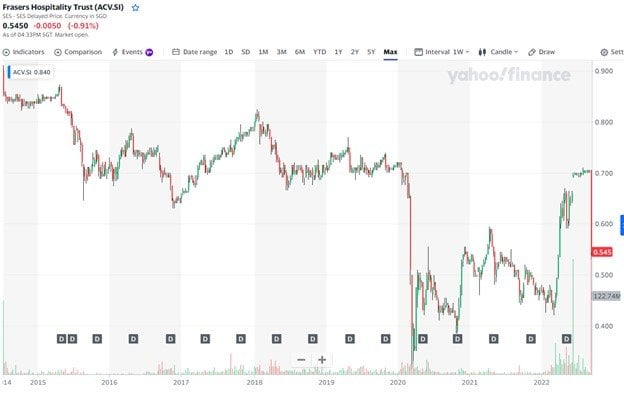

Fast forward to this week, and imagine my surprise when the privatization was rejected by unitholders.

The market was equally surprised.

Frasers Hospitality Trust was trading at $0.705 right before the EGM, pricing in very little risk of rejection.

After the results was released, it plunged 25% to intraday lows of $0.525.

So… is Frasers Hospitality Trust a good buy?

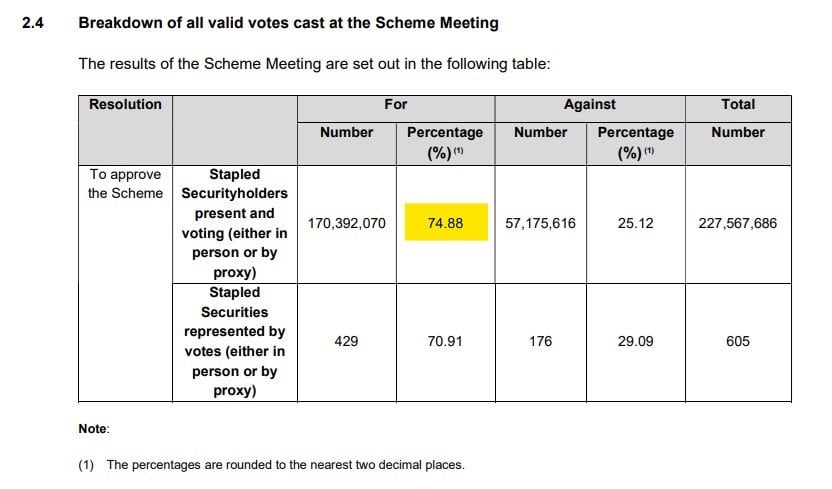

Frasers Hospitality Trust EGM Results (to approve Privatisation)

EGM results are set out below.

For what it’s worth, it came down incredibly close to the wire.

Frasers Hospitality Trust needed 75% of votes to approve the privatization.

They received 74.88%.

Ouch.

You do have to feel bad for the guys who worked on this deal, only for it to be rejected like this.

My views on the Frasers Hospitality Trust privatisation

I looked at the privatization back in June, and you can see my full views here if you are keen.

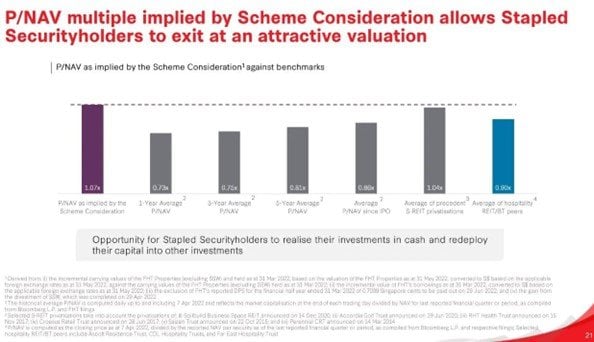

I actually thought the price of $0.70 was a reasonable offer.

At 1.07x book value, it was a decent premium to the long term average Price/NAV of 0.86x.

Left alone, I don’t see the market price trading near there for quite a while.

My views on Hospitality as an Asset Class

Full disclosure – I don’t hold any hospitality REITs.

The last hospitality REIT I held was Ascott Residence Trust, and I sold it all in January 2020 after news of a “Novel Coronavirus” in Wuhan (feels like a lifetime ago).

Simply put – I don’t like hospitality real estate after COVID.

I think if you want to bet on hospitality, you play it via the booking platforms instead.

You buy Booking.com, or you buy Airbnb.

But of course, as the goes – “there’s no such thing as bad real estate, only a bad price”.

I don’t like hospitality as an asset class.

But at the right price, of course I would still be tempted.

And after the 25% plunge, I was actually quite keen to see if value has emerged in Frasers Hospitality Trust.

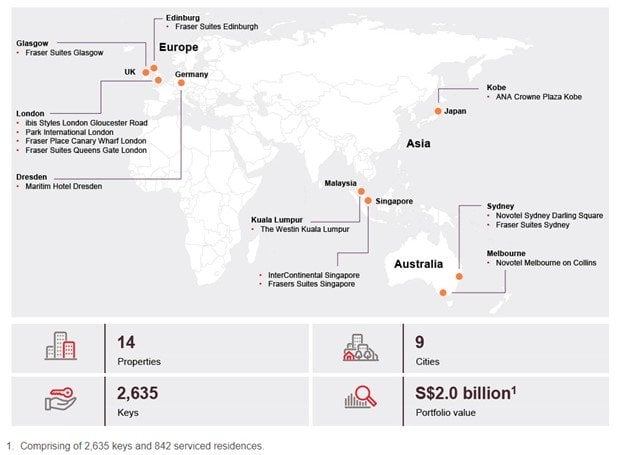

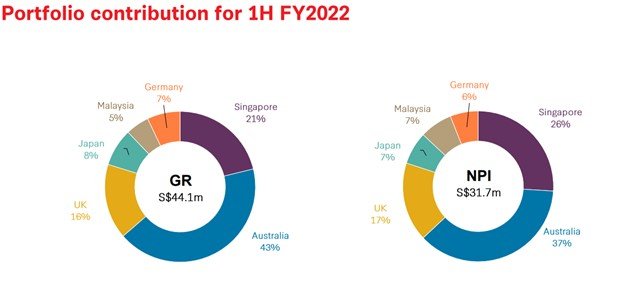

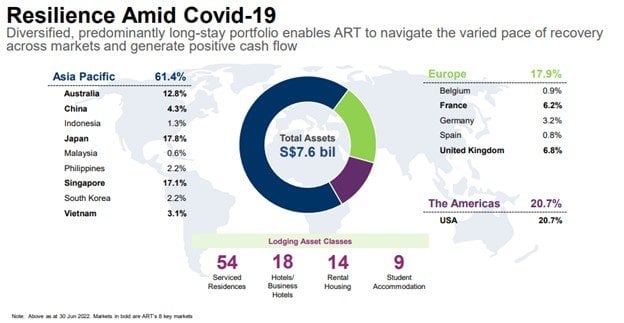

Property Portfolio of Frasers Hospitality Trust

Frasers Hospitality Trust property portfolio is set out below.

To sum up, the 3 biggest markets are Australia, Singapore and the UK.

With Japan, Malaysia and Germany making up the rest.

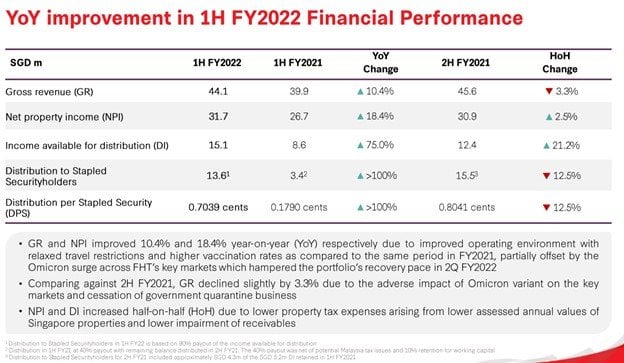

Financial Performance of Frasers Hospitality Trust

Latest Financial Results are set out below.

Year on year comparisons are positive, with nice improvements in almost every metric.

Although that said, these comps are against 1H2021, which was a really bad period in COVID.

You can see the operational numbers improving after the COVID reopening.

No doubt this will start to accelerate in the months ahead, as global travel starts to resume in earnest.

The problem though, is that we look to now be heading into a global recession.

Frasers Hospitality Trust has a decent amount of serviced residences, which could be impacted by reduced business travel. The hotels may also suffer depending on how prolonged this recession is.

Balance Sheet of Frasers Hospitality Trust

Gearing is on the tad high side at 39%.

Weighted average debt to maturity is 1.95 years, which means they’re going to be refinancing almost 50% of outstanding debt over the next 2 years.

That’s not pretty – this is not a good time to be refinancing.

I don’t think Frasers Hospitality Trust will run into refinancing issues given their backing by Frasers Property (and TCC Group), but sometimes you never know.

Even if they can refinance, higher interest expense will weigh on the DPU.

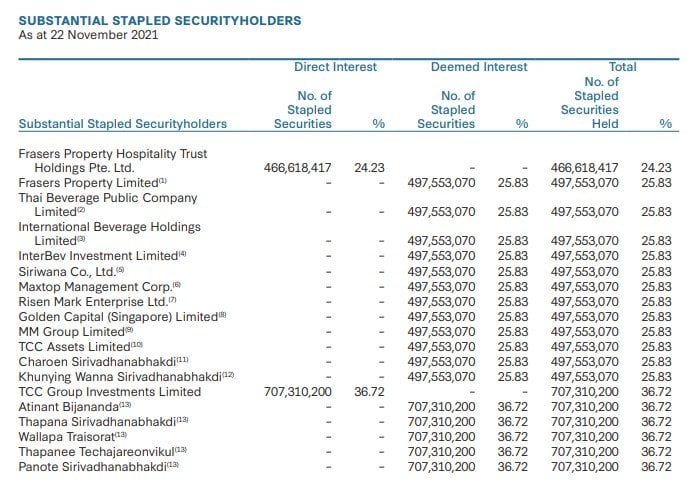

Frasers Property is the Sponsor

Frasers Hospitality Trust is 36% owned by the TCC Group, the owner of Frasers Property (which we covered last week under the Frasers Property Green Notes).

Regular readers know my views on Frasers as a sponsor.

They’re a very decent sponsor, but maybe not in the same league as Mapletree/CapitaLand – which comes with “implicit” Temasek backing.

Dividend Yield of Frasers Hospitality Trust

Dividend yield is tricky.

If you use trailing 12 month numbers, the yield is 2.79%.

If you use pre-COVID numbers, the yield is 8.17%.

The problem though, is that trailing 12 month doesn’t really make sense because there COVID reopenings will improve dividend materially.

At the same time, pre-COVID numbers don’t make sense because the pre-COVID world is over.

The world has changed since COVID, and I just don’t think you can place much reliance on pre-COVID numbers anymore.

So then how do we value Frasers Hospitality Trust?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Book Value of Frasers Hospitality Trust

I think book value is probably the best approach.

Latest NAV of Frasers Hospitality Trust is $0.65.

At $0.54, that works out to 0.83x book value.

What is a fair valuation for a Hospitality REIT today?

Let’s compare that against the other Singapore listed hospitality REITs:

- Ascott Residence Trust: 0.85x

- CDL Hospitality Trust: 0.97x

- Far East Hospitality Trust: 0.725x

- Frasers Hospitality Trust: 0.83x

Ascott Residence Trust is probably the closest proxy to Frasers Hospitality Trust, with assets in Australia, Singapore and Europe.

But Ascott is a much bigger REIT (with different fee structure), so it should trade at a premium to Frasers Hospitality Trust.

CDL Hospitality Trust is primarily Singapore assets, so it should trade at a big premium to Frasers Hospitality Trust.

Far East Hospitality Trust is probably the weakest of the lot based on their property portfolio, and should trade at a discount to Frasers Hospitality Trust.

Using this very rough analysis, it gives us a fair Price/NAV valuation of about 0.75x – 0.85x for Frasers Hospitality Trust.

At the current 0.83x, it’s hard to say that Frasers Hospitality Trust is trading at deep bargain price.

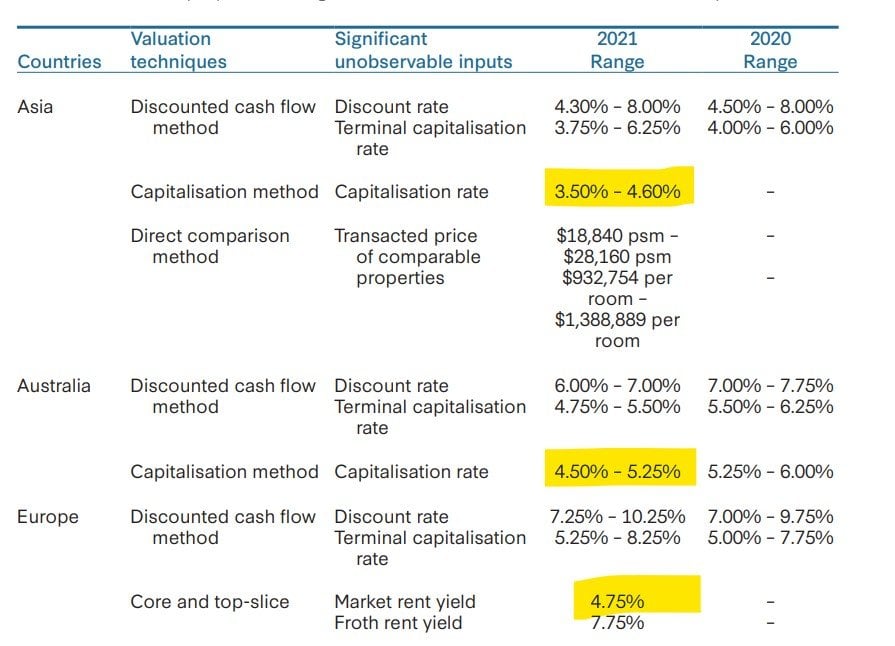

Frasers Hospitality Trust – What capitalisation rates do they use?

Now let’s dive a bit deeper into the real estate valuations used by Frasers Hospitality Trust.

The table below gives you a rough idea of the cap rates they are using for their valuations.

3.5% -4.6% for Asia and 4.5% – 5.25% for Australia.

Now with the latest US CPI print, I think you’re looking at a terminal Fed Funds Rate of 4%+ this cycle.

Market is pricing in 4.3%, but I think 4.5% (or beyond) is possible.

With that in mind… do these cap rates look cheap to you?

Long Term Average Price to Book for Frasers Hospitality Trust

Long term average price to book (since IPO) is 0.86x.

Using current book value, that implies a price of $0.56.

Using pre-COVID book value (0.70), that’s $0.6.

That said, I struggle to see why I would pay anything close to long term average book value in this rising rate climate.

Especially when the cap rates used by Frasers Hospitality Trust look to be on the aggressive side.

Long story short – just doing a tabletop analysis on book value, I find it hard to see value in Frasers Hospitality Trust at the moment.

But FH… S-REITs are all equally expensive

I suppose you may counter that S-REITs as an asset class are all equally expensive right now.

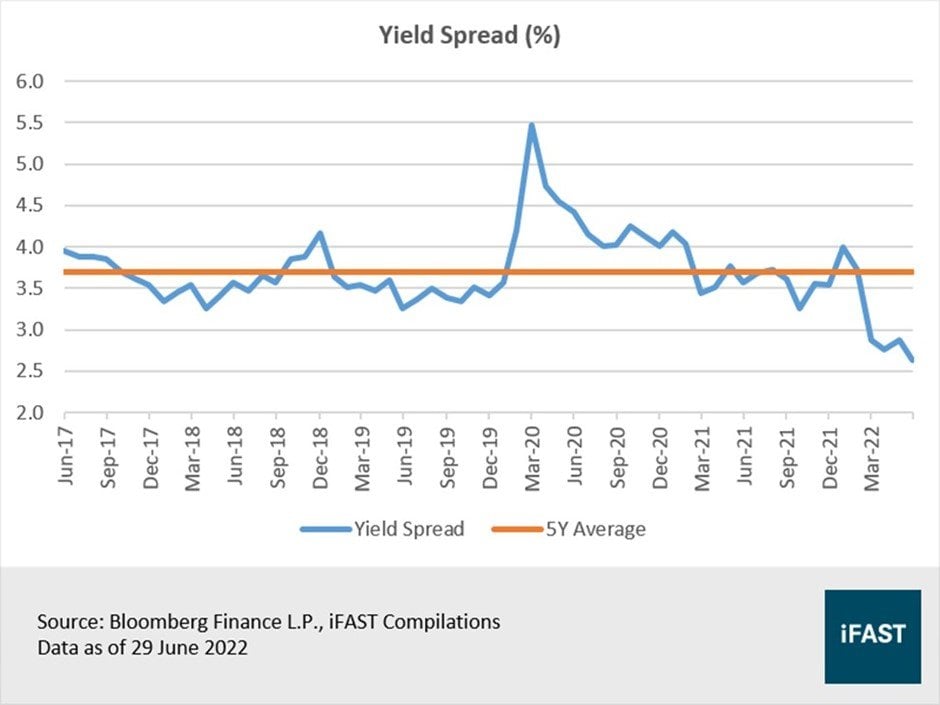

Long term average yield spread is about 3.5%, which means with the SGD risk free going to 3.5% and beyond, REITs need to trade at a 7% yield to be fairly valued.

That’s crazy talk you say.

No way we get there.

FH if you value REITs on yield spread you will never buy anything.

Who knows, you may well be right on this.

The way I see it though, I will start buying REITs when (a) I see the Feds start to pivot, or (b) when I see value emerging at a fundamental level.

As shared above, I don’t see value at this price for Frasers Hospitality Trust.

And as shared to death on Financial Horse, I think talks of a Fed pivot are too early. A Fed pivot will come, but not just yet.

In any case, you can see my latest macro views on when to buy, and what stocks / REITs I am keen to buy, on Patreon.

What next for Frasers Hospitality Trust?

Earlier this year, Frasers shared 3 possible alternatives to privatization:

- Continuing with the existing strategy

- Expand via acquisition or merger

- Strategic Sale of all of some of the assets

Let’s discuss each of them.

Continuing with the existing strategy

Frasers Hospitality Trust tried this for the past 7 years, and results have been mediocre.

Why would this change suddenly?

It’s tough to grow a small cap REIT these days, you just lack the scale and size to do anything.

Can’t make a big transaction without an equity fundraise, and you can’t equity fundraise when your unit price is poor.

Expand via acquisition or merger

Well – they tried this, and it just got rejected.

Will Frasers Property come back with a revised offer?

That’s a good question, frankly don’t know the answer.

It’s possible, but I don’t have any edge here, so I won’t be buying Frasers Hospitality Trust just on the hope the Sponsor comes back with a higher offer.

Strategic Sale of all of some of the assets

The crown jewels would be the Singapore, Australia and London assets.

I suppose you could break up the REIT and sell all the properties individually. That could be one way to realise value.

This is unprecedented though, and I doubt a sponsor the quality of Frasers would do this to their REIT.

They could sell their smaller assets to realise value, but usually the demand for these assets is not as strong so you won’t really move the needle this way.

Closing Thoughts: I’m not buying Frasers Hospitality Trust unless something changes

I’m not a fan of hospitality REITs, and nothing I’ve seen today has changed my mind.

Frasers Hospitality Trust is a small cap REIT, with a lot of refinancing coming up, with average hospitality assets.

I could be tempted to buy if the price is right, but at $0.54, it just looks very fair value to me.

And I don’t want to buy fair value hospitality assets when interest rates are rising this quick.

I’m staying on the sidelines with Frasers Hospitality Trust for now, unless something changes materially with the REIT, or with the global macro.

Until then, it’s just Singapore Savings Bonds and Fixed Deposits for me.

In any case, you can see my latest macro views on when to buy, and what stocks / REITs I am keen to buy, on Patreon.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try here.

As always, this article is written on 16 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Interest rate n pending recession is not down yet. More fun to come.

Am inclined to agree… 😉

I like your simplistic arguments. No fanciful writing style or financial jargon to confuse or impress.

Thanks for the kind words – appreciated!