I’ve been getting quite a few questions about Frasers Hospitality Trust’s privatisation recently.

I was looking over the privatisation details recently, and it was actually pretty interesting.

So I wanted to share some of my key takeaways in this article.

Note: This article is a premium article that first appeared on Patron. If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Basics: Frasers Hospitality Trust privatized at $0.70

In one sentence – Frasers Hospitality Trust is being privatized at S$0.70 by the Sponsor (Frasers Property Limited).

$0.70 is marked by the dotted line below.

As you can see, whether you find $0.70 a good price, will depend very much on when you bought Frasers Hospitality Trust.

If you bought before 2020 – chances are you hate the privatisation.

If you bought after 2020 – well maybe you don’t love the price, but at least you won’t be losing money.

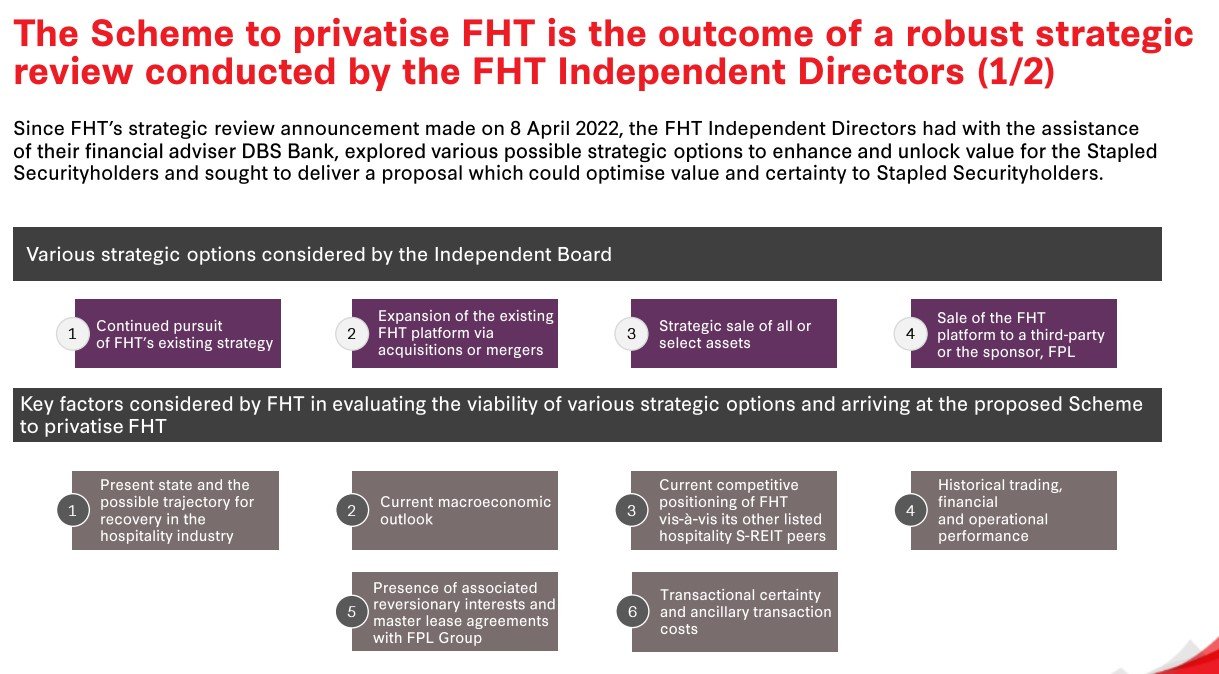

According to the manager, the Frasers Hospitality Trust privatisation is the result of a “robust strategic review”.

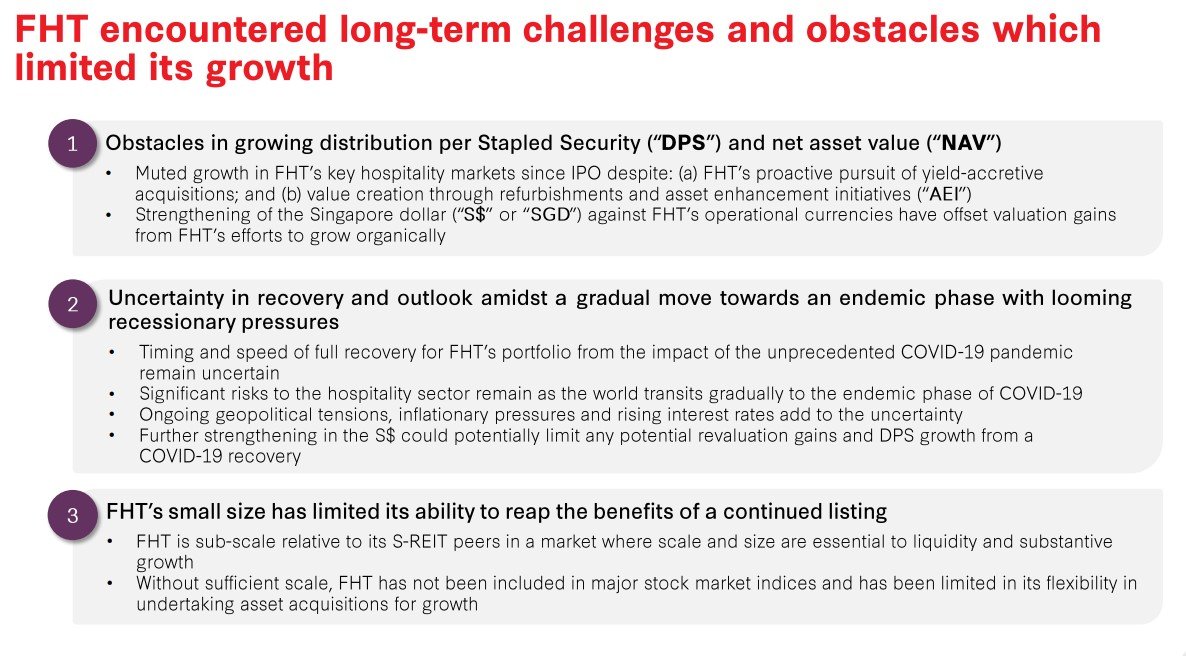

The long term challenges faced by Frasers Hospitality Trust are:

- Difficulty in growing the REIT

- Macro conditions in the short term are poor

- Frasers Hospitality Trust is too small to reap the benefits of being publicly listed

Other options considered for Frasers Hospitality Trust include:

- Continuing with the existing strategy

- Expand via acquisition or merger

- Strategic Sale of all of some of the assets

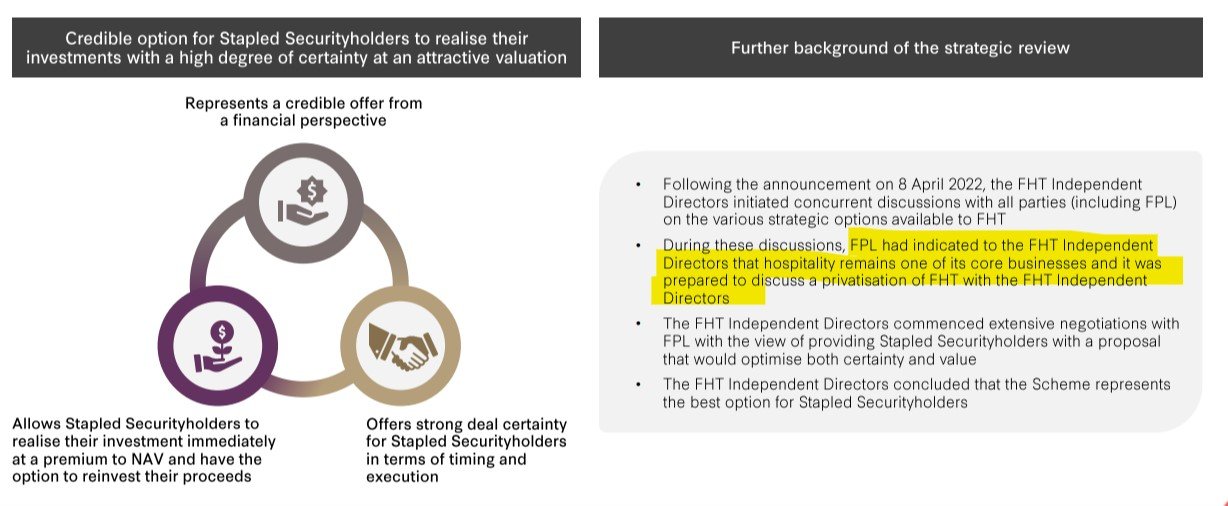

There’s an interesting nugget buried in one of the slides, where they basically said that the Sponsor, Frasers Property Limited, views hospitality as one of its core business – which was why they seriously considered a privatisation of Frasers Hospitality Trust.

3 Key Takeaways on Frasers Hospitality Trust’s Privatisation

3 key takeaways from me:

- Timing is convenient…

- Price is okay-ish

- Small REITs are in trouble

1. Timing is convenient…

Okay I get it.

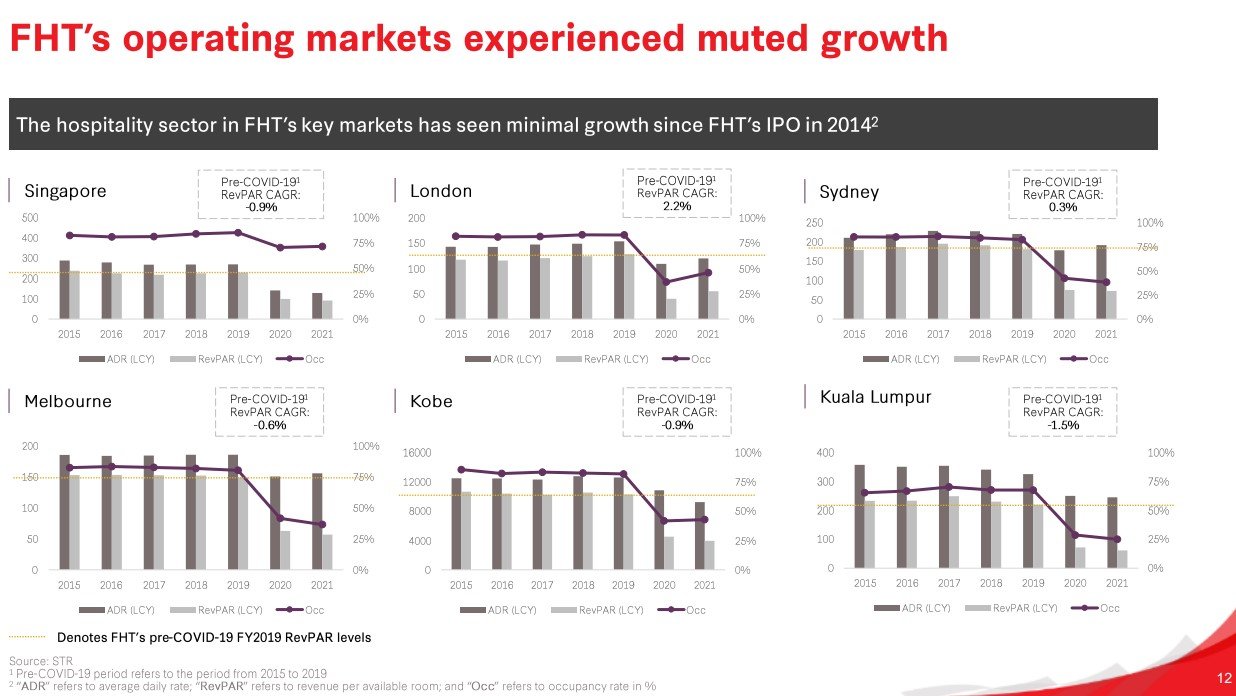

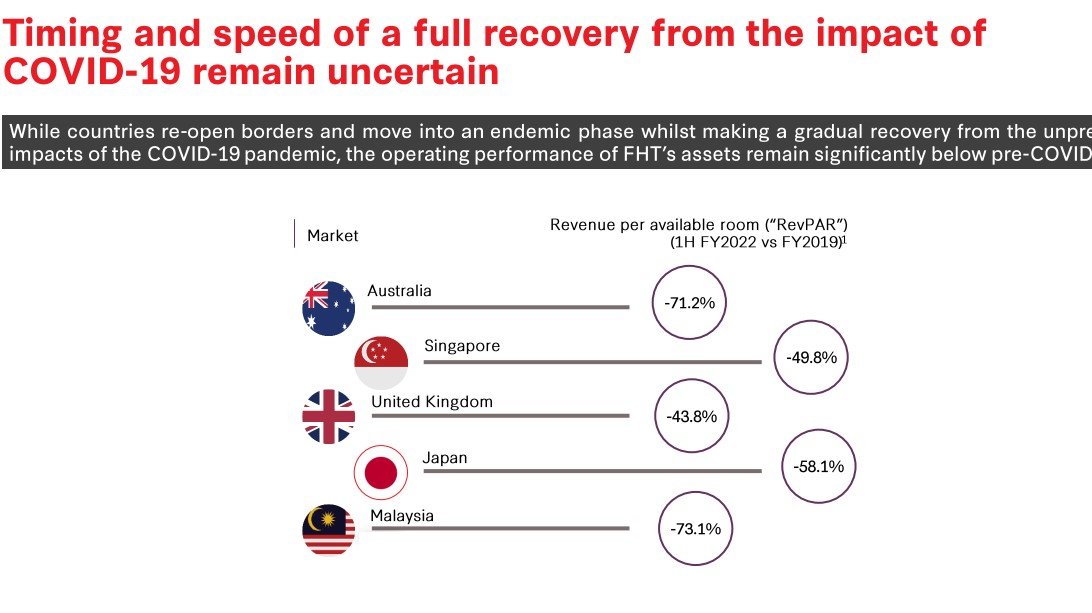

Hospitality is not doing well.

When you have a global pandemic that shuts most of global air travel for the better part of 2 years, I don’t doubt for a second that the hospitality sector will not be doing well.

And that is clear from all the charts below:

What is very convenient though, is that the privatisation only happens just as we are about to emerge from the depths of COVID.

They could have privatised Frasers Hospitality Trust any time in the past 2 years, but no, they did it only when global airtravel and tourism is about to reopen fully.

To be fair to them – you can argue that maybe the Sponsor had difficulty raising financing the past 2 years to finance a big privatisation like this.

And that’s probably a fair point.

It’s possible that the timing could just be a coincidence.

Who knows.

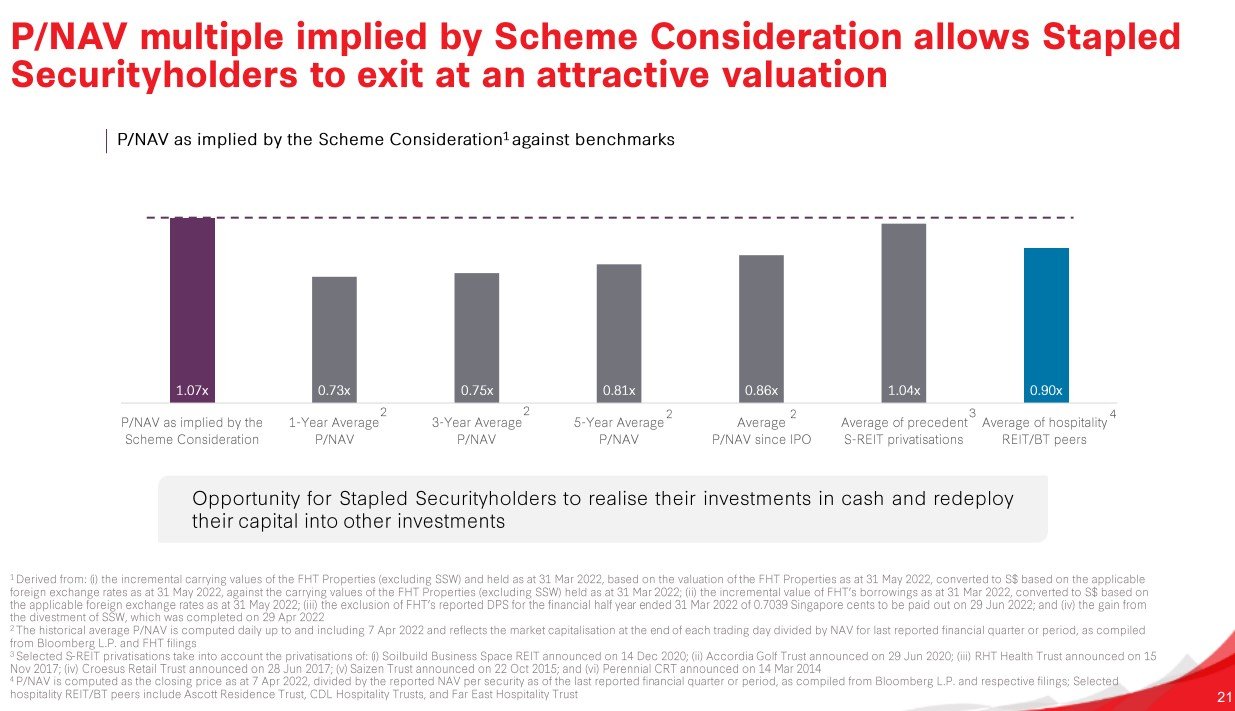

2. Price is okay-ish

To give credit where credit is due – I actually thought the price offered for Frasers Hospitality Trust is okay-ish.

Sure it’s not “jump out of your seat because I just won the lottery” kind of price that you usually get with a privatisation.

But it’s still a decent premium to the long term P/NAV of Frasers Hospitality Trust.

At 1.07 P/NAV, that’s quite a decent multiple for a hospitality REIT in this market. And a nice premium to the long term average P/NAV, whatever way you slice it.

I know a lot of unitholders are not pleased with the pricing.

They think that if they were to hold onto Frasers Hospitality Trust for another 1 – 2 years, price could recover even more.

I get that.

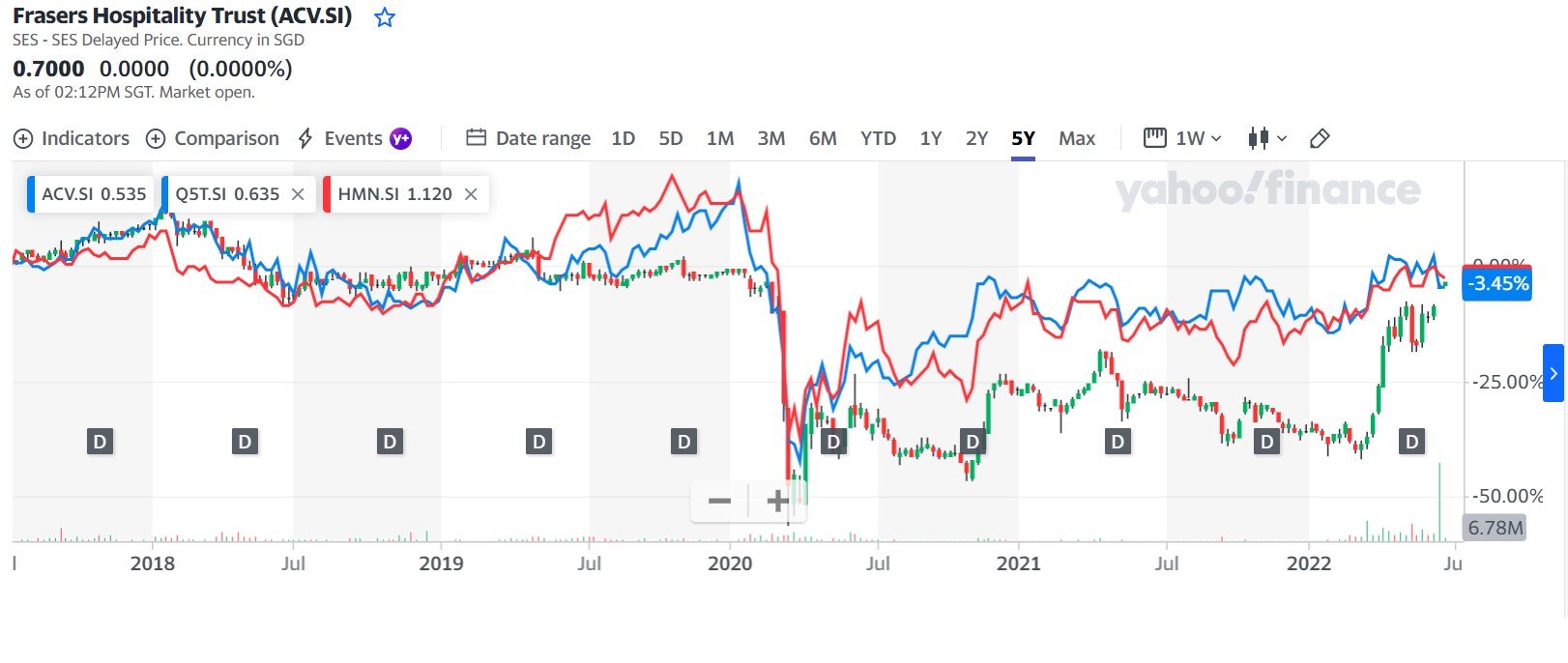

That said if you compare the performance of Frasers Hospitality Trust against some other Singapore hospitality REITs, you’ll find that the performance of FHT doesn’t lag behind all that much.

See below – where Blue is Far East Hospitality Trust and Red is Ascott Residence Trust.

Frasers Hospitality Trust lags a bit, but it’s not necessarily a massive gap.

So yes – I get that the privatisation price could be even better.

But my personal opinion, I actually think it’s a fair offer, all things considered.

I’m not a unitholder, but if I were I would probably just take the cash and flip it into another REIT.

Lots of buying opportunities right now, and likely even more will open up in the months ahead.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

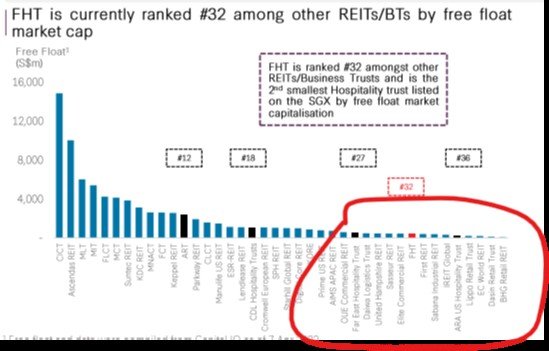

3. Small REITs are in trouble

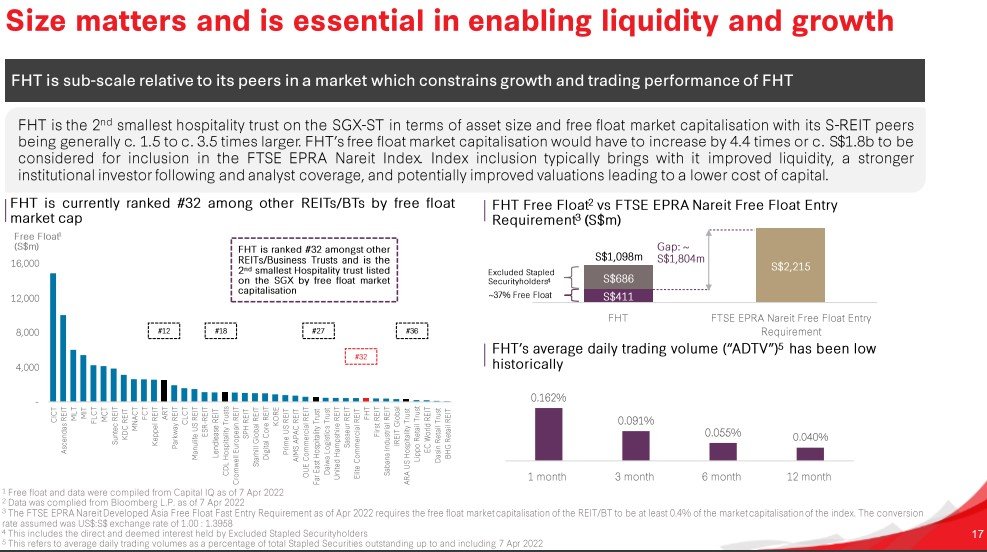

Probably the biggest takeaway for me – Small REITs are in trouble.

A spate of recent REIT mergers, from CCT/CMT to MCT/MNACT to ESR-REIT/ARA LOGOS Logistics Trust, should have already made that very clear to you.

Just like how the US REIT market consolidated over time to favour bigger REITs – we see the exact same thing happening to the Singapore REIT market.

If your REIT is too small, you:

- Cannot get included in REIT Indices – resulting in lower valuations and liquidity

- Cannot raise money easily – making it hard to grow

- Cannot buy other properties easily – making it hard to grow

It’s just not a good place to be in, for small REITs.

Your options are to (1) privatise, (2) merge with another REIT, or (3) languish around as a small cap REIT.

Just look at the chart below of all the smaller REITs.

If you’re holding one of those REITs within the red circle, at the very least you should be aware of this risk.

You may want to buy and hold the REIT forever, but if someone else comes along and buys out your REIT, you may be forced to sell at that price.

As always – love to hear what you think!

Note: This article is a premium article that first appeared on Patron. If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.