Frasers Property Limited just released a new retail bond.

These Green Notes yield 4.49% per annum, with a 5-year tenor.

I’ve been getting quite a few questions about whether they are worth subscribing for, so I wanted to share views in this article.

Basics: Frasers Property Green Notes Review (4.49% yield, 5-year duration)

The key points for the Frasers Property Green Notes are set out below:

- 5-year Tenor (due Sep 2027)

- 4.49% interest per annum (payable two times a year)

- Minimum subscription size is S$1,000

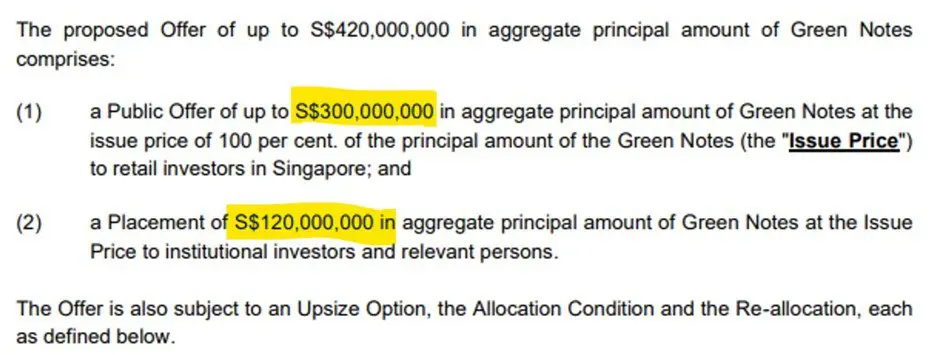

- Issue size is $420 million (with potential upsize to $650 million)

- Public offer size of $300 million, Private Placement of $120 million

Subscription is cash only, you cannot use CPF or SRS to subscribe.

Why is the public offer size so big?

Okay so the first point that jumped out at me was the size of the public offer.

Why is the public offer size so big?!

A bit of background, usually with big debt offerings, you are targeting the institutionals and high net worth individuals.

So most of the time, the private placement will be the big one, then you save maybe 10% of the issue size to throw retail investors a bone.

With this offering – it’s the opposite.

At $300 million out of $420 million, the retail tranche is a whopping 71.4% of the total offer size.

It looks like Frasers Property used the institutional tranche mainly for bookbuilding (to determine price), and then gave the bulk of the issuance to retail investors.

I suppose there are 2 ways of seeing this:

- Frasers Property being generous to retail investors – They are genuinely being nice to retail investors, and want to give retail a chance to subscribe for a decent amount.

- No demand from institutional – It’s quite clear that institutional liquidity is drying up globally with tightening monetary policy. So another way of seeing it is that the institutional tranche is small because they can’t find enough buyers.

I’ll leave you to decide on which is the more accurate interpretation.

For the record though, the last time Frasers Property issued a retail bond – they did the same thing.

Back in 2015, the retail tranche was 150m, and the institutional tranche was 50m, with retail making up 75% of the offering size.

So who knows, maybe this is just the way Frasers Property does things.

Update: I’m hearing from the ground that the Institutional Placement was hot. Original placement size of $75 million had $230 million in orders, and was closed early – and resulted in a lower coupon of 4.49% (original indicative yield was 4.75%). I’m not able to verify this independently, so anyone who can confirm just leave a comment below!

Is the 4.49% yield on these Frasers Property Green Notes attractive?

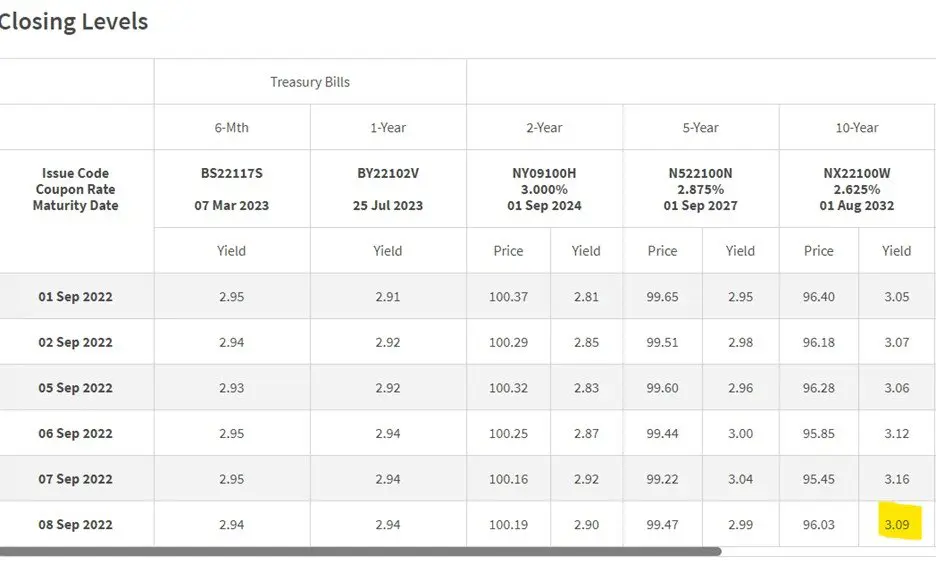

At a 4.49%, you’re looking at a 1.4% yield spread against the latest 10-year Singapore Government Security.

Or a 1.5% yield spread against an equivalent 5-year Singapore Government Security.

As a rough benchmark, the average yield spread for investment grade bonds in the US right now is about 1.5%.

Viewed in that light, I suppose these Frasers Property Green Notes are fairly priced.

Whether the yield is sufficient for you to buy it is a different question, but it’s hard to say that these Green Notes are under/over priced given market pricing today.

Should you wait for higher interest rates?

Another point worth discussing, is whether it makes sense to buy these Frasers Property Green Notes at 4.49% yield now, when interest rates are going up rapidly.

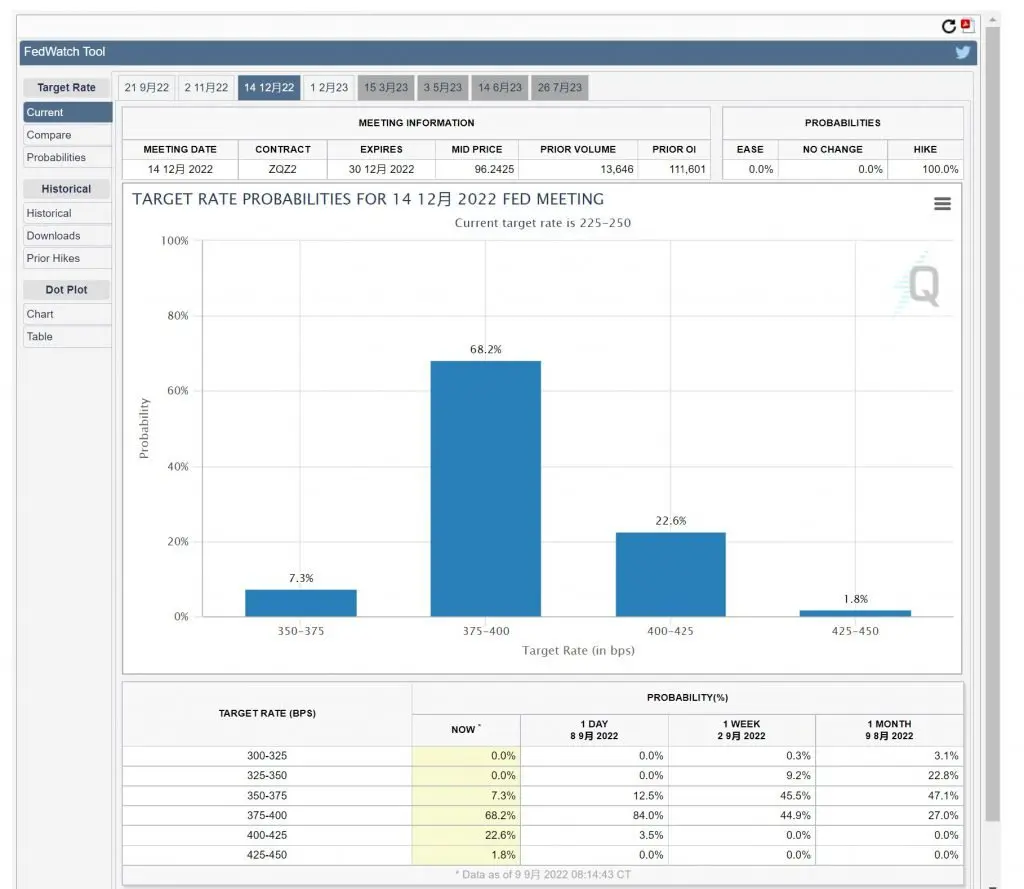

Markets are pricing in a 68% chance that the Fed Funds Rates will be at 3.75% by December 2022.

So this looks like a good time to be borrowing money at a fixed rate, and less so to be lending money at a fixed rate.

You can literally just sit on your hands for 3 months, and you’ll get a much higher interest rate on the market in a couple of months.

Which could easily translate to capital losses on these Frasers Property Green Notes.

Remember, these Frasers Property Green Notes are for a 5 year duration, and if you want to get your money out before that, you need to sell on the open market, at the market price.

And when interest rates go up, bond prices go down.

Is there a chance of default? Hyflux 2.0?

I know what you’re going to ask.

What is the chance of default?

Is this Hyflux 2.0?

To answer this – let’s take a closer look at Frasers Property.

What is Frasers Property Limited?

Frasers Property Limited has quite a long and illustrious history.

They were originally part of Cold Storage Limited.

In 1987, they were bought over by F&N.

In 2013, F&N itself was acquired by Thai Billionaire Charoen Sirivadhanabhakdi’s TCC Group, and the property arm was listed on the SGX as Frasers Centrepoint Limited.

In 2018 Frasers Centrepoint Limited was renamed Frasers Property Limited.

REIT investors will know Frasers Property Limited as the sponsor of Frasers Centrepoint Trust and Frasers Logistics & Commercial Trust.

Frasers Property Limited today

Frasers Property has a market cap of $4.2 billion today.

And here’s the share price performance going back to 2014.

Unlike some other developers like CapitaLand, Frasers Property never really recovered from COVID, and you can see their share price languishing at COVID levels even till this day.

Shareholders of Frasers Property

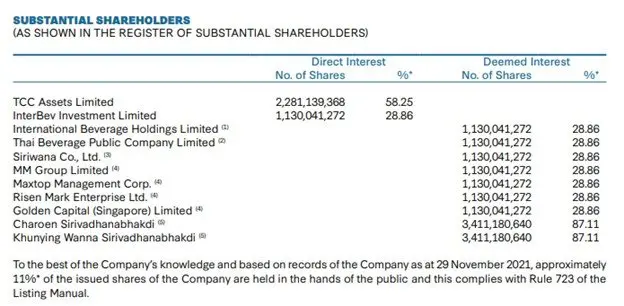

For the record – Frasers Property is NOT an “Ah-Gong” backed company.

I repeat, they are NOT Temasek backed.

They are majority owned by Thai Billionaire Charoen Sirivadhanabhakdi (via TCC Group), who owns 58.25% of Frasers Property Limited.

Bond Investors are a different breed from Equity Investors

Now analyzing bonds is quite different from analyzing equities for one very simple reason – as a bond investor you do not care how well the company does.

There is only 1 thing you care about, and that is solvency.

So while equities investors are narrative driven, and love fancy stories about how the company will grow to new heights.

As a bond investor literally the only thing you care about is whether they can pay their debt.

Frasers Property can lose a billion a year, and the share price can plunge 80%, but you wouldn’t care as long as they can find enough cash to repay their debts.

Because of that bond investors spend a lot of time looking at financial statements, which of course is a skill many investors have lost after a decade of Fed fueled liquidity.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

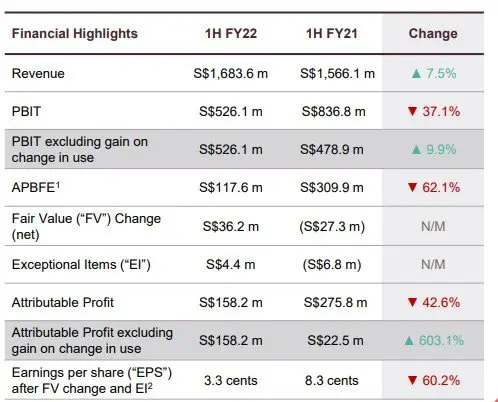

P&L of Frasers Property

Here’s the P&L.

Revenue is growing nicely, but PBIT is down quite a bit.

Fair value change is minimal at $36.2m, so at least they’re not padding the numbers with property revaluation gains.

That said, with property developers their earnings can be quite lumpy because of how property sales work, so we need to dive a bit deeper into cash flow.

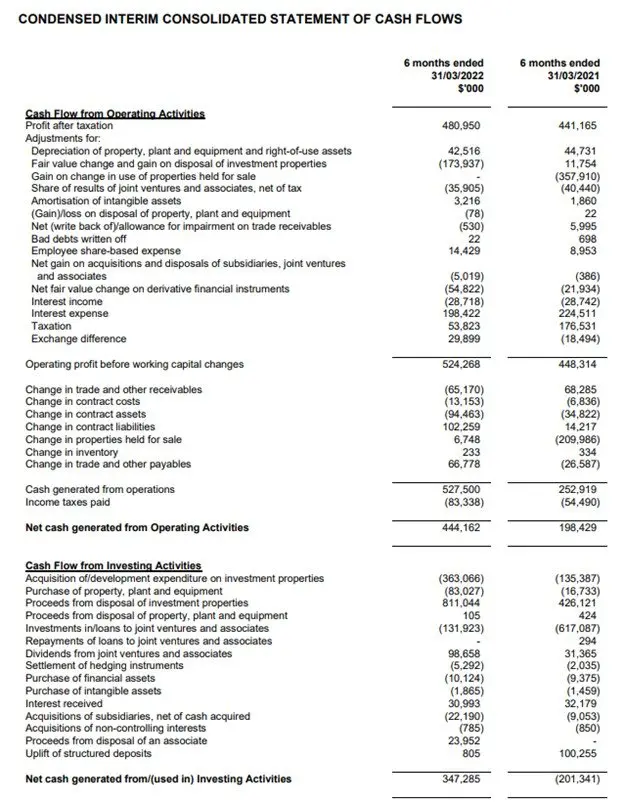

Cash flow of Frasers Property

Cash flow is set out below (bigger version here).

Like I said, it’s a bit lumpy because of how selling properties works (you book a big profit / cash in the quarter that you sell), but no big red flags so far.

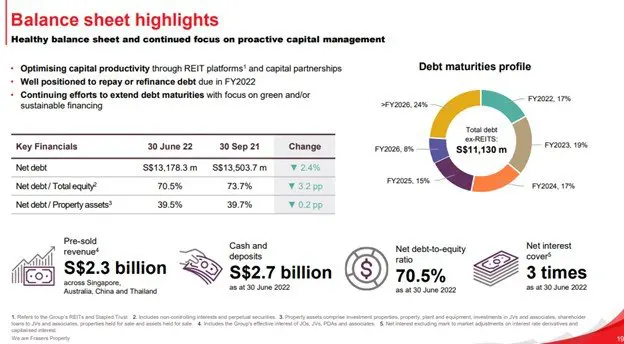

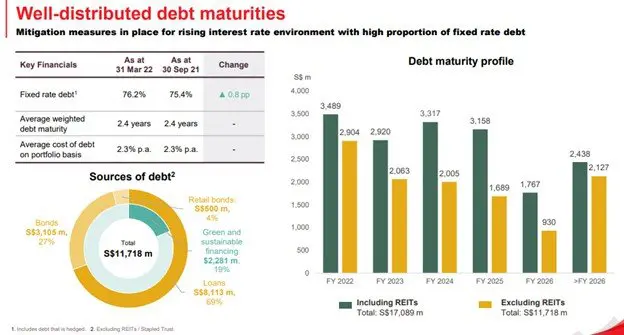

Balance Sheet of Frasers Property

Here’s the latest balance sheet.

Frasers Property has $2.7 billion of cash on their balance sheet.

Net Debt / Property is 39.7%.

Interest Coverage Ratio is 3 times, which is probably on the low side.

75% of debt is fixed, but a weighted debt maturity of 2.4 years means they are going to be refinancing a lot of debt over the next 1 – 2 years, into much higher interest rates.

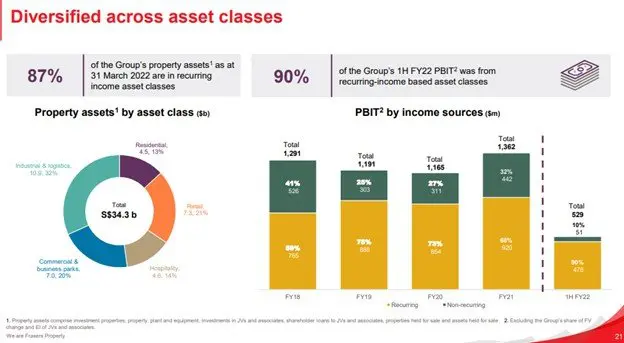

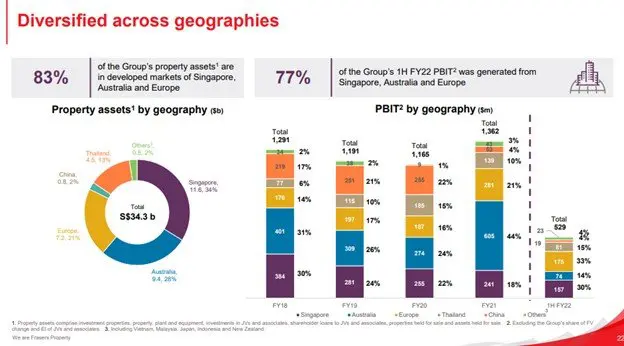

For what it’s worth, Frasers Property’s income and asset base is quite broadly diversified across geographies and asset classes.

So FH… Will these Frasers Property Green Note / Retail Bonds default?

Gun to my head, I will say the risk is low.

Absolutely not.

I think you have to accept that this is not a Temasek Bond or a Singapore Government Security where the risk is zero.

With these Frasers Property Green Notes, it is 100% clear that they are not risk free.

There is a chance of default here.

But… Is the Risk-Reward worth it?

For the record, a 1.5% yield spread against the risk free is similar to what the Astrea series of Retail Bonds were issued at.

Between the Astrea series and these Frasers Property Bonds, I think the Astrea Bonds have better risk reward.

With Astrea Bonds you have fairly mature PE Funds (vintage > 5 years), and you have a very broadly diversified asset base. The risk you’re taking on is a meltdown in the global financial system.

With the Frasers Property Bonds – on top of the macro risk, you’re also taking on single issuer risk, the risk that something goes wrong with Frasers Property.

And again for the record, I do think risk of default here is low.

If Frasers Property defaults, unitholders of Frasers Centrepoint Trust and Frasers Logistics & Commercial Trust are going to be in a world of pain.

So it’s probably a low probability event, but that said 5 years is a long time.

Can you buy/sell these Frasers Property Green notes on the open market?

Unfortunately the previous 2015 Frasers Property Retail Bonds have been fully redeemed, so I wasn’t able to pull up liquidity information.

If the past retail bonds on the SGX are anything to go by, liquidity is probably going to be poor.

You should still be able to sell these bonds, but you may not be able to unload a big position quickly unless you price at a discount.

And don’t forget that if interest rates go up, you could be sitting on capital losses if you sell before maturity.

Will I buy these Retail Bonds – Frasers Property Green Notes Review (4.49% yield, 5 year tenor)?

I thought about it for a bit.

And I’m *probably* going to skip these 4.49% Frasers Property Green Notes.

If you’ve been following Financial Horse for a while, you’ll know that I’ve been bearish on the macro since Jan 2022.

A lot of the fears we’ve been talking about, are starting to play out rapidly.

We have a hawkish Fed, we have a hawkish European Central Bank, and we have a stubborn Bank of Japan.

Meanwhile China is imploding from COVID zero and property debt, and cannot stimulate without triggering a depreciation in the RMB (which will bring inflation).

There’s a real risk of a sovereign debt crisis and Asian Financial Crisis 2.0 in the months ahead. And I suppose a European recession is already a foregone conclusion.

Why am I skipping these 4.49% Frasers Property Green Notes?

The way I see it, there are 2 ways the next 12 – 18 months will play out.

Either (1) the economy / markets break forcing the Feds to turn dovish, or (2) Governments inject huge fiscal stimulus in the face of tightening monetary policy.

If we get (1), which is probably my base case, then I want all the liquidity I can get to go max long when the event comes.

Remember, once the Feds flip dovish, the next phase is going to be inflationary.

It will be debasement of fiat currency.

So you don’t want to be stuck holding too much cash in the next phase, and you need to hold as much real assets as you can.

With these Frasers Property Bonds, I’m not sure if I can get the money back quickly, without taking a capital loss.

If it’s (2), this would mean we skip the market crash, and go straight into inflation.

In which case do I necessarily want to be stuck holding 4.49% yielding 5 year bonds from Frasers Property?

As things stand, I’m holding record levels of liquidity that surpass even Jan 2020 levels.

And all that liquidity is going into risk-free stuff I can access at a moment’s notice – stuff like Singapore Savings Bonds or high yield savings accounts or perhaps Fixed Deposits.

If I see the Feds flipping dovish, or I see governments pumping in massive fiscal, I will need to start deploying that liquidity.

In any case, you can check out the stocks / REITs I am keen to buy, and the target prices, on Patreon.

But… I think a certain type of investor will like these Frasers Property Green Notes

But hey – that’s just me.

For the record, I still think risk of default is low, and the yield on these Frasers Property Green Notes is decent (at today’s prices).

But interest rates are going up rapidly, so that is a big risk you need to note.

For certain kinds of investors though, I think this could be a decent buy.

For example if you have a ton of cash, don’t want to take a lot of risk, but want a return higher than Singapore Savings Bonds.

And you’re happy to have the cash locked up for the next 5 years.

Then I think these Frasers Property Green Notes are a decent buy.

Sure, interest rates are going up in the short term, but who knows they may easily be cut in 2023/2024. With these retail bonds if you hold to maturity, you’re guaranteed a 4.49% yield as long as Frasers Property does not default.

Just don’t be deluded into thinking these retail bonds are risk free though.

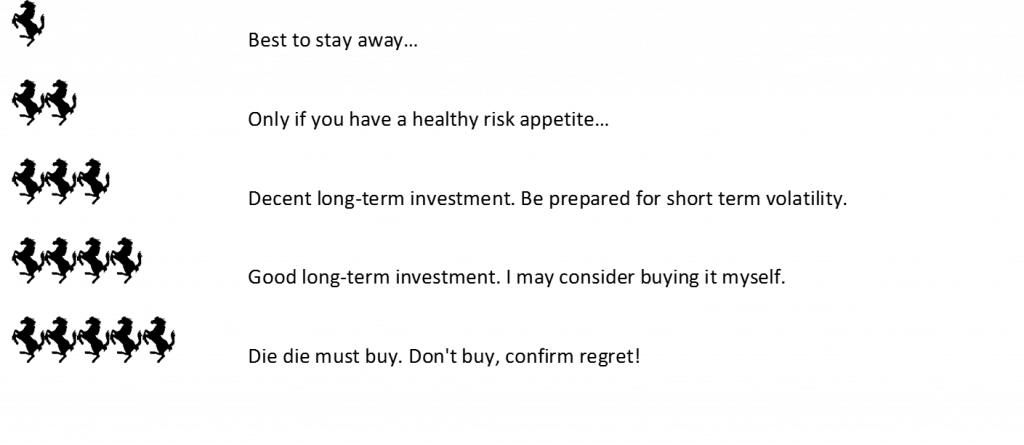

In any case, these Frasers Property Green Notes are a 4 horse rating for me (out of 5).

i think they’re a decent investment, they just don’t fit into my portfolio.

Frasers Property Green Notes – FH Rating: 4 out of 5

Rating Scale

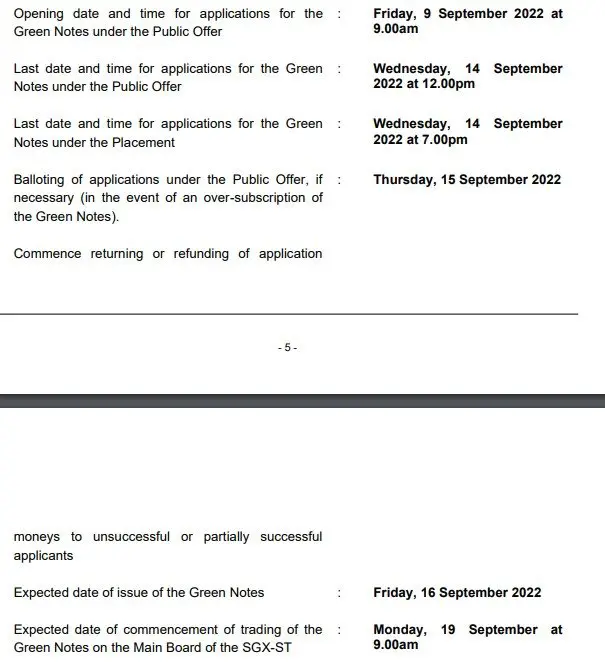

Timeline for Frasers Property Green Notes

Timeline for subscription is set out below.

If you are keen, do subscribe before 7pm on Wed, 14 September.

Subscription is the same as any IPO – via any of the 3 local banks! ATM, or internet banking!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try here.

As always, this article is written on 9 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

There’s a typo at the top – “49% interest per annum”. Nice article BTW. 🙂

Sorry my bad – corrected the typo. Appreciate the heads up. 🙂

Is this going to be exchange traded? On SGX mainboard?

Yes. But how good the trading liquidity is remains to be seen.

Hi – is capital guaranteed at end of 5 yrs? seems not?

The risk you are taking on is Frasers Property’s credit risk. So the principal will be paid back after 5 years – unless Frasers Property defaults.

any rating for this green bond”

Hm doesn’t seem like it…