A couple of you have reached out for my views on the latest Green SGS Bonds.

They’re quite an interesting investment product, so I wanted to share some views in this article.

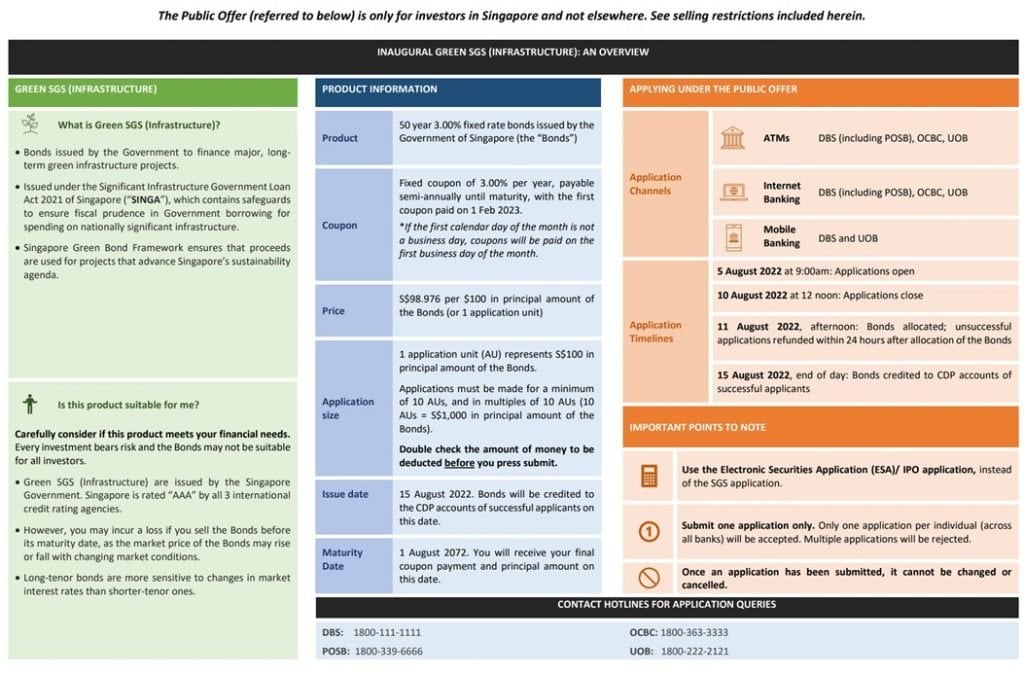

Features of the Green Singapore Government Security (SGS) Bond

|

Tenor |

50 Years |

|

Public Offer |

S$50 million (Total offer size is $2.4 billion, but public offer is only S$50 million) |

|

Minimum Investment Amount |

$1,000, in multiples of S$1000 |

|

Issue Date |

15 August 2022 |

|

Price |

S$98.976 per $100 |

|

Maturity Date |

1 August 2072 |

|

Coupon Rate |

3.0% Fixed rate |

|

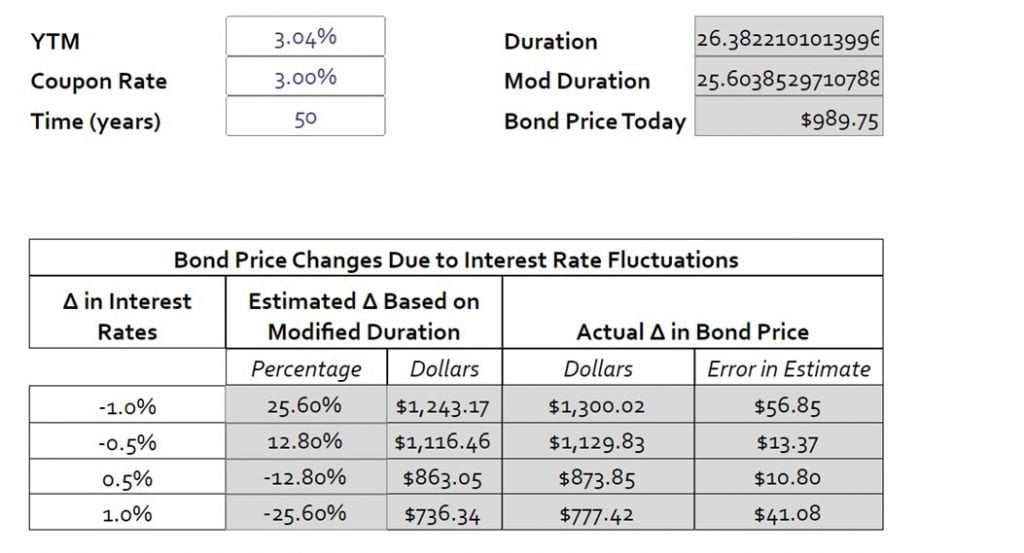

Yield to Maturity |

3.04% per annum |

|

Coupon Payment Dates |

Semi-annual coupon. 1 February and 1 August of each year |

To sum up the key features of the Green SGS Bonds:

- 50 year duration – Yep you heard that right, these are 50 year bonds, maturing in August 2072

- 3.04% yield – Yield to maturity is 3.04%

- Backed by the Singapore Government – These are backed by the Singapore government, so basically zero risk

- Listed on the SGX – they are listed on the SGX, so you can buy/sell on the SGX

You can also refer to the Offering Circular here or the Factsheet here.

The total offer size is $2.4 billion, but the public offer tranche is only a miniscule S$50 million.

That said, it was still nice that they threw retail investors a bone with the retail tranche, so big kudos to the government for doing so.

Let’s discuss some of the bigger questions below.

Is this zero risk?

For the record, these Green SGS Bonds are backed by the Singapore government.

Exactly the same as Singapore Savings Bonds, T-Bills, and SGS Bonds.

So yes, this is basically zero risk.

The risk you are taking on is the risk of default by the Singapore government.

Is the yield on the Green SGS Bonds attractive (3.04%)?

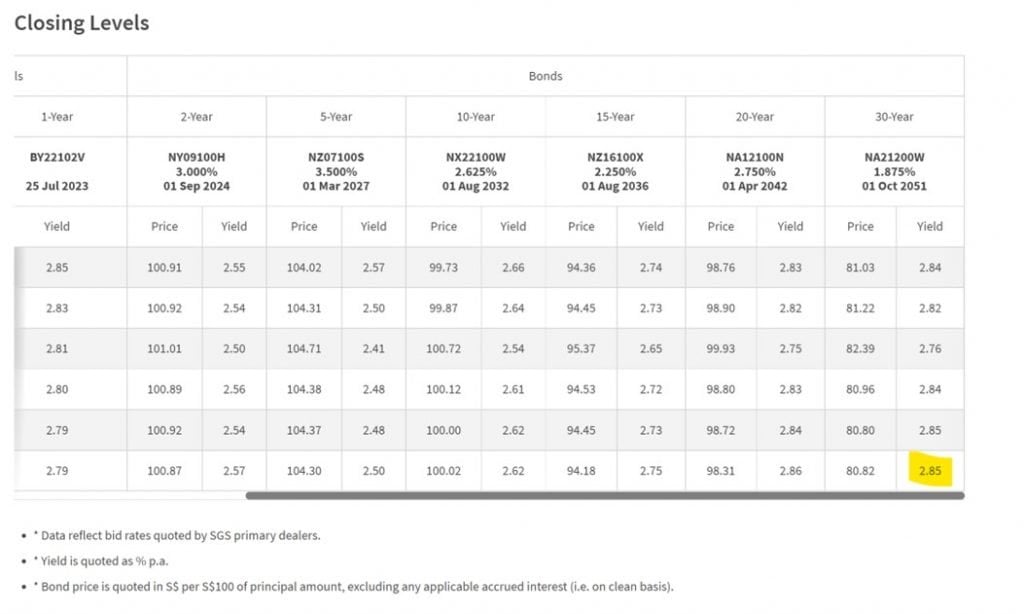

The latest 30 year SGS bond yields 2.85%.

So these 50 year Green SGS Bonds with their 3.04% yield are issued at a 0.19% yield spread vs the 30 year yield.

Personally I don’t think that is attractive enough for the duration risk (I mean it’s a 50 year bond for crying out loud).

But it’s also hard to say that the bonds are mispriced.

They’re just being issued at market prices, and the yields were after a competitive book building process.

What is the advantage of the Green SGS Bonds (vs Singapore Savings Bonds)

The main advantage of the green SGS Bonds in my view, is that there is no limit to how much an investor can buy.

With Singapore Savings Bonds, you’re limited to $200,000 per person.

But if you’re a high net worth individual or institutional investor looking to throw a couple of million into these Green SGS Bonds – you’re perfectly free to do so.

This itself is probably the main advantage of SGS or T-Bills, especially for investors who have more than $200,000 cash.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What is the disadvantage of Green SGS Bonds (vs Singapore Savings Bonds)

But of course, there’s no free lunch in this world.

There are quite a few notable disadvantages:

- No early redemption

- Liquidity

- Potential for Capital Loss if not held to maturity

No early redemption for Green SGS Bonds

Unlike Singapore Savings Bonds where you can redeem anytime to get back your full principle + accrued interest.

You cannot do the same with the Green SGS Bonds.

If you want to exit your investment before maturity, the only way is to sell on the open market.

Which means that:

- You are subject to liquidity constraints on the market

- You are subject to the price on the open market

Liquidity of Green SGS Bonds

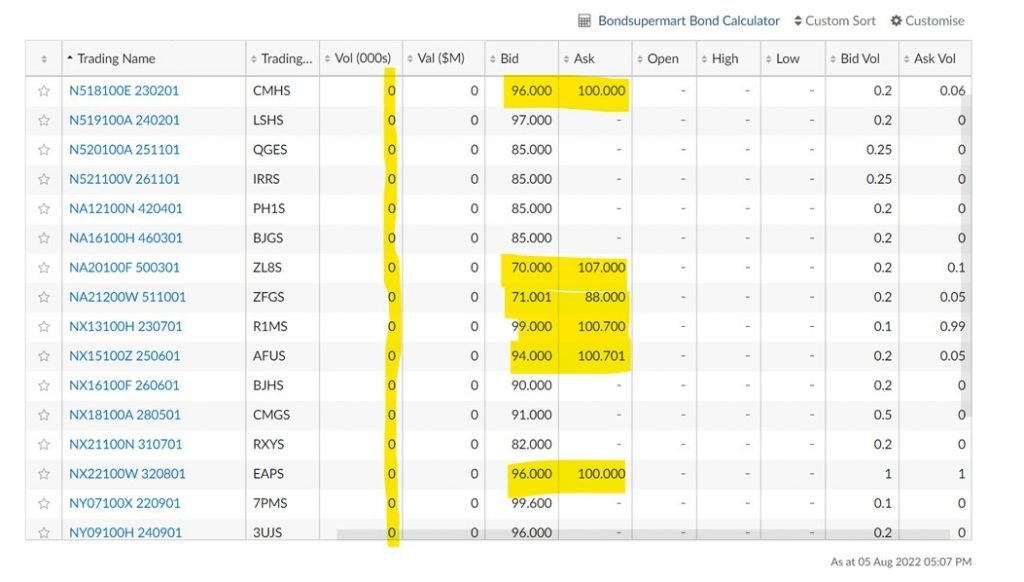

For the record, this is the liquidity of the SGS bonds that are listed on the SGX:

Just look at the trading volume.

A grand total of 0.

And look at the bid-ask spread.

You could fly a Boeing 747 through that spread.

I would expect the same with these Green SGS Bonds.

Expect low liquidity, and large bid-ask spreads.

If you do subscribe for these Green SGS Bonds, you may not be able to sell large positions on the SGX quickly unless you price them at a discount.

Potential for Capital Loss if not held to maturity

And of course, if you want to sell SGS on the open market – you’re at the mercy of market prices.

Bonds trade inversely to interest rates.

So if interest rates go up, bond prices go down.

Extra duration risk with a 50-year bond

This is especially true with you’re holding a 50 year bond, where any move in interest rates is greatly amplified.

You can take a look at how a small change in interest rates can result in massive capital losses when you’re holding a bond with this long duration.

A 1.0% move up in interest rates, will result in a whopping -25% capital loss on these Green SGS Bonds.

What if interest rates drop?

But of course you can argue that if interest rates go down, you stand to make a lot of money on these Green SGS Bonds.

If the 50 year SGS interest rate goes down to 2.0%, you’re potentially looking at a 25% capital gains.

Can these Green SGS Bonds be used to take a position on interest rates?

Which of course raises the question – can you use these Green SGS Bonds as a way to bet on interest rate movements?

And I think your main constraint would be the liquidity.

Looking at how poor liquidity on the SGS bonds are historically, this may not be an efficient way to bet on interest rates.

Any order would take ages to fill, with a large bid-ask spread

You’re probably better off just buying puts/calls on the TLT, or playing the Eurodollar curve directly. Especially how the SGD interest rates are very closely linked to the US interest rates.

And if you don’t know what those are, you probably shouldn’t be betting on interest rates.

Potential for Capital Loss if not held to maturity

Long story short – If interest rates go up, and you need your cash back in a hurry, you may not be able to exit your Green SGS Bonds without taking capital loss.

Heck, even if interest rates don’t move significantly, you may not be able to exit your Green SGS Bonds quickly because of the poor liquidity and large bid-ask spread.

This inability to redeem directly from the government, and only being to sell on the open market, is a very key difference vs Singapore Savings Bonds.

Why I am skipping the Green SGS Bonds

It’s quite clear for me that I am going to be skipping these Green SGS Bonds.

As shared in yesterday’s article, I think the path forward this decade lies with higher inflation and higher interest rates.

In an environment like that, holding long duration government bonds is probably one of the worst investments you can make.

Not only would you get hammered by capital loss if interest rates go up, the 3.04% yield may also not be sufficient to cover inflation.

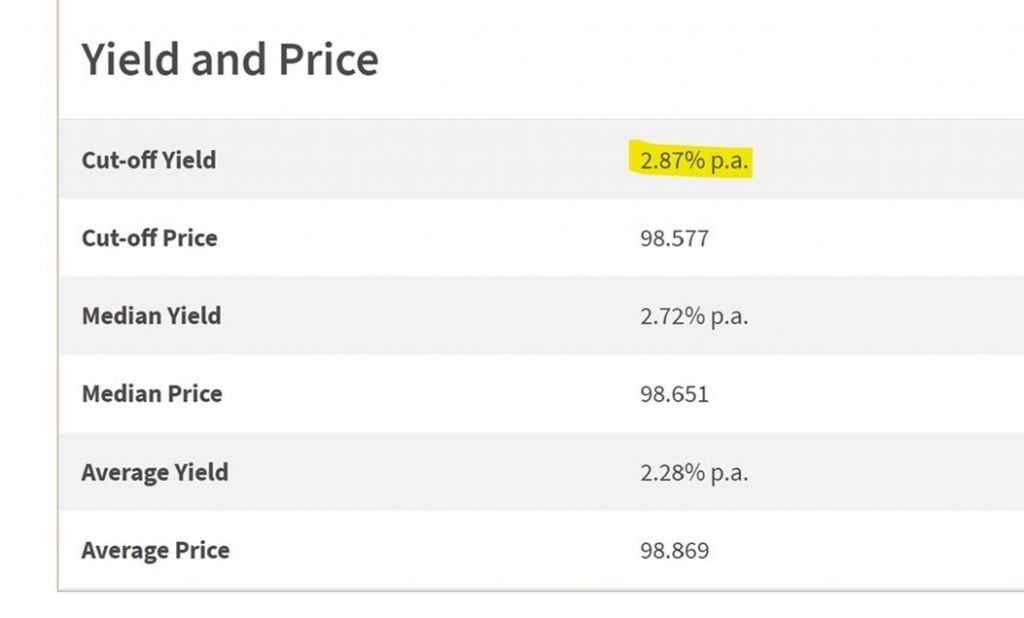

In any case, just look at the latest T-Bills auction below.

You’re getting 2.87% to lend to the government for 6 months, completely risk free.

In a climate like this, I’m probably holding most of my cash in short duration bonds, because I really do not want to take on the long duration risk.

Who might like these Green SGS Bonds?

That said, I can see how institutional or high net worth individuals will still want to subscribe for these Green SGS Bonds.

If you’ve got a billion or two lying around, putting some of that into these bonds at a 3.04% yield is a pretty safe investment.

SGD denominated too, so you eliminate a lot of the FX risk.

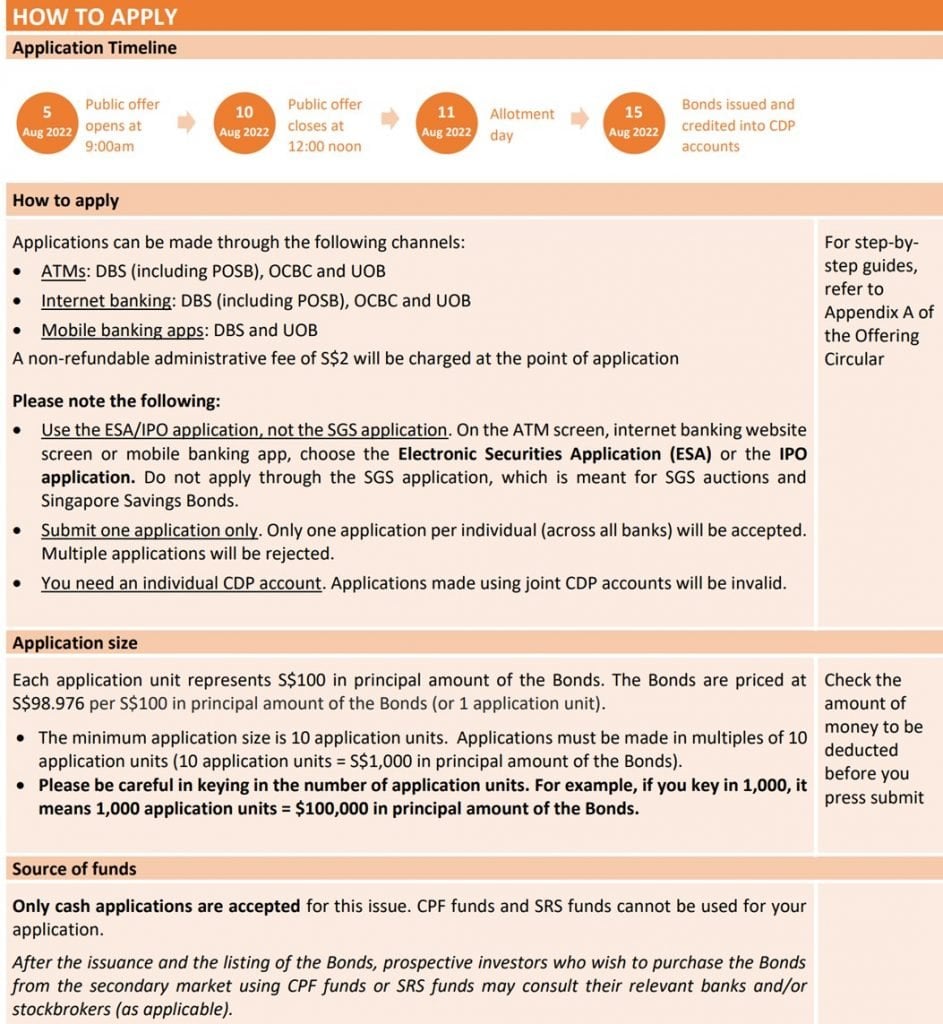

How to apply for the Green SGS Bonds?

If you do want to apply, public offer is now open (opened at 9am on 5 August).

Last day to apply is 12 noon on Wednesday, 10 August.

Application method is the same as Singapore Savings Bonds / IPO – via any of the 3 local banks!

Do note that only cash applications are allowed. You can’t use SRS or CPF to subscribe for these Green SGS Bonds.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try here.

As always, this article is written on 6 Aug 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH,

Good post and agree with your thoughts on why this might not suit for retail investors, as it does not meet or there are better alternatives for the goals a retail investor might be hoping to achieve. The example you gave on TLT to play for a fall in interest rates is case in point. Purer play and better liquidity.

From an institution’s perspective, it might suit because:

-a lot of the demand actually comes from Singaporean insurance companies. Their liabilities are extremely long dated and so they try to match this with a long dated asset like this. Also, they are not trying to beat the market here, and are likely just looking at a particular hurdle rate (say >3%) to beat.

-liquidity less of an issue for them, as instis can trade this over the counter with the big banks. As such, could still use this as a play on super long duration interest rates falling.

-it probably adds some desirable ESG traits to their portfolios. There has been much commentary the green framework on these bonds as a positive example for other countries to follow.

So in sum, what might not make sense for us retail investors might make total sense to other investors in the market place. There are various players in the market playing different games. So we gotta decide what game we want to play and choose the instruments that best meet our needs to maximise our odds of success.

Absolutely fantastic comment Moomoo.

Nothing more I would add – agreed with all the points you raised.

It doesn’t make sense for retail, but I can see why instis or family offices would be dying to get their hands on these bonds. It’s all a matter of perspective.

Heartening to see the SGS market developing in this way though!