As you guys have probably heard by now, ABSD (Additional Buyer Stamp Duty) rates have gone up yet again.

You can see the changes summarised below.

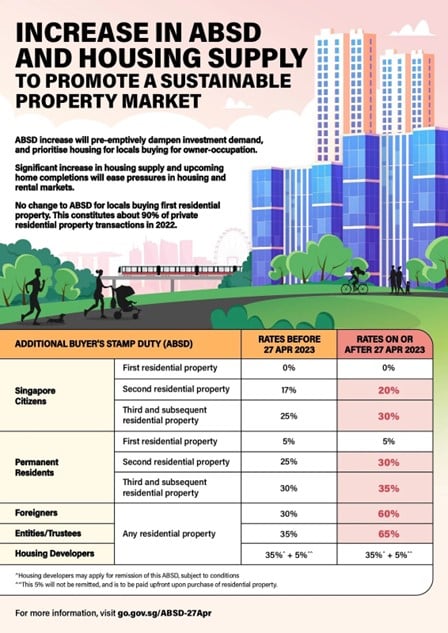

Singapore Citizens buying a second home now pay 20% ABSD (up from 17%).

And the big one – Foreigners buying property now pay 60% ABSD (up from 30%).

What is the impact of this round of ABSD changes on Singapore House prices?

Here’s a question posed in the Telegram chat:

Heard on youtube and spoken to several agents and they think new ABSD will not affect property prices and they think property prices will continue to climb upwards and here advise to buy asap before prices get out of reach. What’s your view?

I mean first off – take everything from Youtube and from Property agents with a healthy pinch of salt.

In my experience, ask a property agent anything and they will tell you that property prices are likely to “continue to climb upwards”.

There’s a fair bit of conflict of interests there if you ask me.

Sharing my personal views on the ABSD changes

But in any case the issue is a bit more nuanced than meets the eye.

Broadly speaking, there are 2 key changes to ABSD.

- Foreigners ABSD – affects the high end properties in Singapore

- Singapore Citizens/PRs – affects private property more generally in Singapore

It’s a long weekend and I don’t want to waste anyone’s time, so let me keep this piece short and sweet.

Note: This is a premium Patreon post. I am releasing it to all readers as I have been getting quite a few questions on this – and hopefully this might help you in your investing journey.

For latest views, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Foreigners ABSD (30% -> 60%) – affects the high end properties in Singapore

Let’s start by discussing foreigners first.

The background here, is that after COVID, Singapore has been very successful in attracting the ultra high net worth individuals (UHNW) to come here.

And Singapore’s house prices at the super high end does not match up to the levels of Hong Kong, New York or London.

So if you think the UHNW money is going to continue to come into Singapore (and I don’t see any reason why it wouldn’t)

Then logically the price of high end properties will continue to go up (at least until they equalise with Hong Kong).

In which case the government has 2 options.

Do you allow the sellers to profit from increasing prices of high end properties.

Or do you immediately raise the price of the high end properties via ABSD (and benefit the country’s coffers).

Answer is an easy one in my view.

But… will this affect foreigners demand?

So I can completely understand why this ABSD increase for foreigners had to be made.

But let’s look at it on the flip side.

Let’s say you’re an UHNW.

You want to put your money somewhere.

Your options are Hong Kong, New York, London, Singapore.

With this round of changes, Singapore property prices (after accounting for tax) are somewhat in line with the first three.

Will that deter you from buying a high end Singapore property?

Frankly don’t see it making a big difference.

If you were going to pick Singapore, it is because of the rule of law and the safe haven / financial centre status.

And also because of the fact that it is not Hong Kong (this matters for certain Chinese investors), and also because it is not New York or London (being countries very closely related to the US, if you get what I mean).

None of that has changed.

Sure you’re now paying an extra 30% in tax, but when you’re an UHNW – frankly that kind of money doesn’t even factor into the consideration.

Singapore Citizens/PRs – affects private property more generally in Singapore

Now I started by discussing foreigners because I felt the point was easier to illustrate when the stakes are bigger.

But the same consideration applies to Singapore Citizens/PRs too.

Let me put it this way.

Imagine that you’re a Singapore citizen planning to buy a second residential property (valued at $2 million).

Before this round of changes, you needed to pay:

- $340,000 in ABSD

- $69,600 BSD (Buyer Stamp Duty)

- $1.1 million upfront payment (because you can only borrow 45% LTV for the second property)

Basically, a Singapore citizen buying a second residential property had to pay $1,509,600 in cash upfront for their second property.

After this round of changes, the ABSD bill has now gone up to $400,000.

Which means that the Singapore citizen now has to pay $1,569,600 in cash upfront.

That’s a 4% increase, or $60,000 increase in the amount he has to pay.

So… is that really going to deter someone who was prepared to pay $1.5 million in cash upfront for his second property?

That after 27 April, he decides nah that extra $60,000 is a step too far for me, let’s put off the purchase.

I leave readers to reach their own conclusion.

So what happens next to Singapore property prices?

So just to be very clear.

I am NOT making any predictions on Singapore property prices here.

The point that I am trying to make, is that I am not so sure if the ABSD changes themselves will have that big an impact on demand for Singapore property (and consequently prices).

Instead what I think will have a very real impact, are:

- Interest Rates

- Supply vs demand

Interest Rates

Mortgage rates have gone from 1% to close to 4% in the span of 18 months.

That means homebuyers could be looking at 40 – 50% increases in mortgage repayments.

That’s the kind of stuff that moves property markets.

You haven’t really seen the full impact of it yet because many owners are locked into 2 – 3 year fixed rates.

But as time goes by, the fixed rates will expire, and the pain from higher mortgage rates will become very real.

Supply vs Demand

To sum up the problem with the Singapore property market – not enough housing supply, and too much demand for houses.

The solution is to either build more houses, or bring demand down.

Yes more houses are already being built, but it takes years for construction to complete.

So supply side will be solved eventually, but it takes time.

As for demand, do the changes above hit demand materially?

As shared above, I do have my doubts on this.

I think demand will moderate eventually due to higher interest rates and affordability, I’m just not so sure it comes down simply because of higher ABSD.

FH… What’s your view on Singapore house prices

I know many of you will want a straight answer from me – as to my views on where Singapore house prices are going.

So I’ll try my best to share, but do note that this takes us into forecast territory, so do take it with a healthy pinch of salt.

Simple view is that I think in the short run, prices can continue to march higher.

The key problem is supply vs demand, which had not really been addressed yet.

But mid term, there is little doubt that the supply vs demand problems will ease.

New supply will come online, demand will moderate, bringing the market into better balance.

While higher interest rates will start to impact affordability and valuations.

So mid term, I think the prices will start to moderate.

But hey – that’s just me.

I welcome contrary views as always!

Note: This is a premium Patreon post. I am releasing it to all readers as I have been getting quite a few questions on this – and hopefully this might help you in your investing journey.

For latest views, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!