We’ve been doing a lot of short term focussed macro pieces recently.

A lot of the investing in 2022 / 2023 is just one big metagame of predicting where inflation will go and how will the Feds be forced to respond, and positioning accordingly.

So in today’s article, I wanted to take a more long term view on investing (I will do another more short term focussed piece this week).

Let’s say we cut out all the noise over the next 12 – 24 months.

And we are investing for a 5 to 10 year timeframe.

What will the world look like over such a time period.

And how best to invest in a world like that?

A world of higher geopolitical tension

I was reading some of Zoltan Pozsar (the famed Credit Suisse rates strategist) pieces recently.

It’s definitely one of the better frameworks to approach this decade that I’ve seen to date.

You may not necessarily agree with his vision, but you do need to at least understand how a future like this may possibly play out.

I’ve attached the series of articles to the Patreon post if you want to do a deep dive, but the essence of the argument can be summarised as follows (paraphrased and edited with some of my own interpretation for clarity).

- War is inflationary

- War means industry

- War encumbers commodities

- War cuts new financial channels

- War upsets all 4 prices of money

This was a premium Patreon post published a while back. I am making it available to all readers in the hopes that this might help you in your investing journey, as the content remains very relevant.

If you find this useful, do support Financial Horse as a Patreon. You can get regular, up to date macro updates just like this, together with my full REIT and stock watchlist.

Sign up here.

1) War is inflationary

This “War” started in 2018 when then US President Trump started a trade war on China.

The “War” then continued in the form of a war on COVID-19.

And more recently, a hot war against Ukraine.

Taking a step back, the world since World War II (and especially so after the fall of the Soviet Union) was a unipolar world order (Pax Americana) enforced by the US.

In the world that we currently live in today, all the financial, logistics, trade and industrial systems have been built under the assumption of American dominance, and the US led world order.

Take global supply chains for example.

The iPhone processor is designed in the US (Apple), based off of British designs (ARM), manufactured in Taiwan (TSMC – which itself draws on technologies from around the world in the fabrication process), shipped to China for assembly (Foxconn), before being shipped around the world for sales.

And that’s just the processor – a similar supply chain takes place for almost every single part in the iPhone.

A system like that, only makes sense when there is complete freedom of trade between countries, and little to no geopolitical tensions.

A world of just in time supply chains, starts to break down when you don’t know if Japanese components can still be shipped to China for assembly tomorrow, or whether Chinese products can enter the US without a tariff.

So the system that has been enforced by the US since the end of WWII is now being challenged by the rise of China (and the rest of the BRICS).

At the same time, the America of today is not the America of the past 60 years, willing to spend American money, American resources, and American lives to defend the world order.

Today’s America is less engaged in the world’s affairs, and more content to focus their time and effort on domestic issues.

So the rise of China (and the rest), is coinciding with the withdrawal of America from the global stage.

2) War means industry

The low inflation regime of the past 20 years was built on 3 key pillars:

- Cheap immigrant labour

- Cheap Chinese goods

- Cheap Russian commodities fuelling European industry

Due to various factors over the past 5 years, all 3 of the above are being disrupted.

Chinese goods are no longer so “cheap” or accessible due to US sanctions, trade tariffs, and Chinese domestic problems among other things.

Europe is effectively cut off from Russian commodities and energy, forcing them to buy from alternative (more expensive) sources.

COVID, the financial responses to COVID, and the resulting inflation has disrupted the flow and supply of immigrant labour, resulting in higher labour costs.

The theory of economic independence states that when great powers have positive expectations of future trade environment, they want to remain at peace in order to secure the economic benefits that enhance long term economic power.

When great powers have negative expectations of the future trade environment, leaders are likely to fear a loss of access to raw materials and markets. This gives them an incentive to initiate crises to protect their commercial interests.

Due to higher geopolitical tensions, global trust is breaking down.

You only need to take a look at US sanctions on China’s access to semiconductors, US sanctions against Russia, US trade tariffs against China, to get an understanding of how the previous regime of global access to trade that has dominated since WWII is starting to change.

Without trust, global trade does not work.

Today’s supply chains can involve parts being built in Germany, sent to Japan for value add, then sent to China for assembly, and then sent to the US for sale.

In a world with higher geopolitical tension, such a model does not work.

This will result in the West being forced to:

- Rearm – rebuild armies to be able to defend national interests. Take Germany for example, no longer being able to rely on American promises of security, and having to invest heavily in defence

- Reshore – if you can no longer trust global trade for key supply components, you need to start reshoring. You need to ensure your key supply chains are in your country, or at least in countries that are near / friendly to you

- Restock and invest – with commodities supply in question, this will spark a need to secure and invest in reliable commodities and energy supply

- Rewire – and navigate the green energy transition at the same time as all the above is playing out

This “rearming and reshoring” will:

- Require a lot of commodities to build the infrastructure of tomorrow

- Require a lot of capital to pay for all that spending

- Be interest rate insensitive because this is for national security and will be spent regardless of the cost, crowding out private sector spending

- Be uninvestible for Asian companies due to national security reasons

3) War encumbers commodities

From an energy standpoint, there are only 3 big producers of Energy in the world:

- North America

- Middle East

- Russia

It is fairly easy to see how the distribution of energy will be split in this new world.

North America will supply America and Europe.

Russia and Middle East will supply Asia.

Look at it this way, and you start to understand why the Saudis are starting to reject US overtures and getting cosy with China.

And also why the US is so eager to cut off Europe from Russian energy.

It’s just a matter of economics – China (and Asia) will increasingly become the largest buyer of Middle Eastern energy as this century plays out. And Europe will become increasingly dependent on US energy.

The complication of course, is that China no longer wants to pay for energy in USD.

After Russia, it’s fairly obvious what will happen to China once they are no longer in the US’s good books. If they make one wrong move over Taiwan for example.

For China, for as long as they pay for energy in USD, they will have this proverbial sword of Damocles dangling over their head.

So China wants to pay in RMB.

And to sweeten the deal for the Middle East, they are willing to invest in the Middle East, to supply goods, services, and invest in building infrastructure.

All of which can be paid for using RMB, which the Middle East will get by selling energy to China.

The Middle East is a lot less cosy with the US these days

From the Middle Eastern standpoint, it’s not too bad a deal too.

US since the shale revolution is energy independent (so they are less dependant on Middle Eastern oil), which means less leverage for the Middle East.

This isn’t the US of old which would go to war to defend the Middle East status quo, as they did with Kuwait in the 1990s.

This means the US cannot be counted upon to defend the Middle East when push comes to shove. We already see this in the dialling back of US military support for the Saudis, and increasing reluctance to sell the most advanced weapon systems to the Saudis.

And these days – receiving USD as payment for oil is a lot less sexy when it has been shown that you can lose access to all your USD assets overnight if the US deems fit (see Russia).

And worst still, it’s fairly clear that over the medium term (5 – 10 years), the US government is going to be issuing a lot more government debt (US Treasuries) to fund the increased government spending – which will result in the depreciation of the USD.

So holding USD is starting to carry with it a lot of risks, and it’s not a bad idea to diversify to RMB.

RMB can be used to pay for Chinese goods and services (the variety of which is increasing day by day).

And since 2016, RMB can technically be converted to gold on the Shanghai exchange, which provides an alternative route to “redeem” RMB.

4) War cuts new financial channels

Now the world that we live in today, is dominated by the USD.

Let’s say Singapore wants to buy oil from the Saudis.

Singapore needs to buy USD from a US bank. Pay it to the Saudis via a US bank. Who then changes the USD back into whatever currency they want.

This is the system that has prevailed since the USD was taken off the gold standard in the 1970s, and the world moves to the Petrodollar.

And the key that underpins it, is as the Petrodollar name suggests – the tying of energy to USD.

In a world where the marginal barrel of oil may be priced in RMB (or say Indian Rupee), you can start to see how the USD will start to lose its shine.

Just to be clear – Nobody is saying the USD will lose its reserve currency status overnight. The USD is far to deeply entrenched into global trade and finance for that to happen.

But things move slowly, and then all at once.

And as this decade plays out, we’ll start to see more and more trade being priced in currencies other than USD.

Demise of the USD as reserve currency?

How exactly this will play out is not so straightforward.

The USD reserve currency system works off Western Banks as correspondent banks to transfer USD. When you want to transfer USD from Singapore to Saudi Arabia to pay for oil, you might go via JP Morgan who effects the USD transaction.

This makes it vulnerable to US financial sanctions, as any correspondent bank carrying out the USD transaction is ultimately accountable to the US, and vulnerable to US sanctions.

Zoltan suggests an alternative system that could take shape – where every central bank issues their own central bank digital currency, which is then backed up by a bilateral currency swap line with other central banks.

This allows central banks to serve as FX dealers to intermediate currency flows between local banking systems, without referencing the USD or the western banking system.

In plain English, what this means is that instead of Singapore paying the Saudis in USD with JP Morgan as the intermediary bank.

You pay the Saudis in SGD, and the Saudis can then swap the SGD for RMB (or whatever currency they want) directly with the central bank – which effects the transaction via a swap line between the respective central bank.

So instead of the USD backstopped by the Western correspondent banking system.

You have a system of many local currencies, each backstopped by their own local central bank, itself backstopped by a bilateral swap line between the various central banks.

Take it one step further, and you can see why China is advocating for the creation of a new third party neutral currency, backed up by commodities.

Back in WWII, this was itself one of the systems mooted by Keynes as an alternative to the Bretton Woods system (and is broadly the concept underpinning the IMF’s special drawing rights).

Both systems will be much more impervious to US financial sanctions.

What does this mean, in plain English?

Now all this is a bit technical, but the crux of it can be summed up as follows:

- China will become by far the largest energy buyer going forward (especially with US energy independence). This gives them a lot of say in how they pay for energy. Which is the backbone of the USD reserve currency status

- It is not in China’s interests to pay for energy in USD, because this makes them vulnerable to US financial sanctions. You only need to take a look at Russia and China’s semiconductor ban to realise that these fears are not fantasy and are very much grounded in reality

- Reports indicate that as of today, China already pays for Russian and Middle East energy in RMB. Even if that is not the case, you would assume that this will happen in some form this decade

- This will eventually create an alternative global system of financial payments, that can be used as an alternative to the USD.

Long story short, in the new world, you can either pay for energy (or trade) in USD.

Or you can use whatever alternative system China and rest of the not so US friendly countries are going to build in this decade.

5) War upsets all 4 prices of money

Now remember – finance is priced at the margin.

It is the marginal rate of change that matters more than the absolute level.

What happens in a world where the marginal demand for the USD is falling away.

Just as the West is forced to invest into “rearming and reshoring” due to higher geopolitical tensions.

The simple answer, is that a lot of new government debt will need to be issued to fund the new spending.

In a world where the East (and private sector) is increasingly reluctant to hold Western government debt.

Who is going to be buying up all this new government debt to be issued?

The logical conclusion is that at some point this decade, we will go down the route of what has been done in every major war in the past – the government will start to monetise the debt. In other words, they will print money to buy the debt to finance the “war”.

How exactly we get from here to there is less than straightforward.

But at the very least, this suggest a world where inflation is much more unstable (volatile).

Because central bank interest rates will respond to inflation conditions, this means much more unstable (volatile) interest rates conditions.

Which itself creates chaos for FX, and the value of money itself (when valued vs real goods).

Ie. We may be moving into a world of higher inflation volatility and higher structural inflation. And consequently a world of higher interest rates volatility, and higher structural interest rates.

How to invest in a world like that? For the next 5 to 10 years?

For what it’s worth, Zoltan offers some suggestions on how to position one’s portfolio for this new world:

The key takeaways, with my own additions where applicable, can be summed up as follows:

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

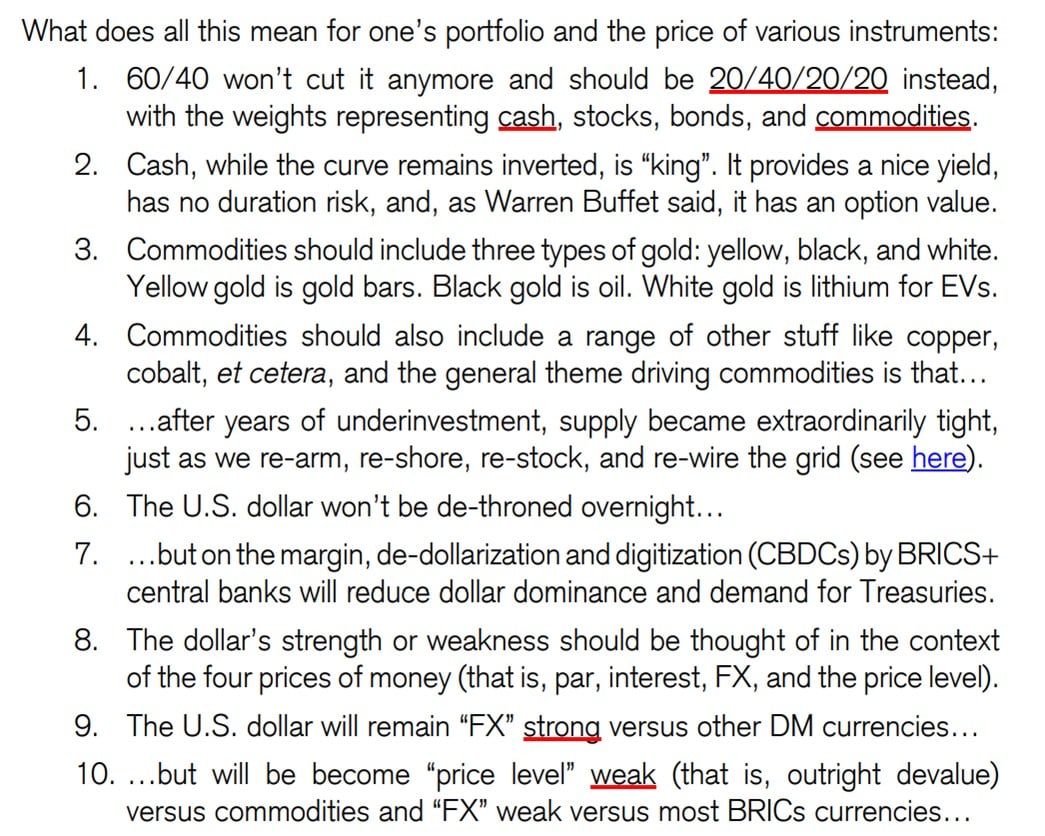

60/40 doesn’t work anymore – hail the 20/40/20/20

Higher structural inflation means government bonds will underperform inflation over the long term.

Over a multi year period, government bonds are almost guaranteed to lose you money vs inflation.

Think a 10 year SGS yielding 2.8%, in a decade where inflation averages 3 – 4%.

And in a true equities sell-off, the ability of government bonds to hedge equity risk is questionable, because the ability of central banks to cut interest rates is hindered in a climate of higher inflation.

So long term government bonds are almost guaranteed to lose you money long term, and short term they may not even hedge equities risk.

60/40 as a long term portfolio allocation no longer makes sense.

Zoltan proposes an alternative ideal allocation to replace 60/40:

20% cash

40% stocks

20% bonds

20% commodities

Some comments for Singapore investors

I like this asset allocation a lot as a starting point for asset allocation, but I think some nuance is required for Singapore investors who are likely to be heavy on (1) real estate (given our nation’s real estate prices) and (2) CPF.

The points that I would add, is to use this 20/40/20/20 portfolio only for the portion of your portfolio excluding real estate.

So for eg. If you have $10 million net worth, and $4 million is in property, you will only apply the asset allocation above to the $6 million of your net worth excluding property.

And if you are holding a lot of real estate, you probably want to dial back on long duration assets in the stock portion of your portfolio (eg. REITs or Tech). Otherwise you risk being overexposed to rising interest rate risk.

I would also add that you should reduce the stocks / commodities portion based on how much real estate you are holding, and increase the cash / bonds component to provide an appropriate buffer against market volatility.

On CPF – this can be viewed as either cash / bonds depending on your age and how close you are to retirement. Older investors can count CPF-SA as cash (they can access it sooner), while younger investors can count CPF-OA as cash (can be used to pay mortgage or buy real estate), while CPF-SA as a long term bond that cannot easily be accessed.

Cash is king for as long as the yield curve is inverted (short rates higher than long rates)

When the yield curve is inverted like right now.

You can get 4%+ on a 6 month T-Bill.

While only 2.8% on a 10 year SGS bond.

The latter of which carries duration risk – because if long term interest rates goes down, you will be sitting on capital loss.

In situations like that, holding elevated cash positions (in T-Bills) makes a lot of sense.

At 4%+, the yield on cash is decent.

There is no duration risk (because you can just hold to maturity and there will not be capital losses regardless of where interest rates goes).

And cash gives you option value, because it gives you optionality to buy risk assets in a sell-off.

Commodities should be a mix of gold, oil and lithium

Of the 3, I would probably overweight oil.

Medium term, I see oil as the alpha commodity that will drive inflation (up or down). Oil is the purest inflation hedge.

And I think Lithium could be combined (or replaced) with copper.

But the core logic here is to buy oil to hedge rising energy prices.

Buy gold as the only form of hard money, to protect against devaluation of fiat currency.

And Lithium (or copper) to invest in the green energy transition, which will require a lot of both.

USD will remain strong vs other DM currencies, but weak vs commodities and BRICs

The implication of this is that almost all fiat currencies (save for BRICS or Emerging Markets with lots of commodities exposure), will see their currency depreciate against real assets like commodities or energy.

Which is why a 100% allocation to cash does not work too, because you need to hold risk assets to hedge inflation.

While a 100% allocation to risk assets does not work too, because this is a regime of significantly higher asset volatility, and you need the cash to survive in a regime like that (and to buy dips).

Don’t underestimate FX volatility

The other point I would add, is to not underestimate FX volatility in this new regime of higher geopolitical tension, and diverging central bank monetary policies.

For Singapore Investors, this could favour increasing exposure to SGD or Asian currency denominated assets, over USD or Euro denominated assets.

This was a premium Patreon post published a while back. I am making it available to all readers in the hopes that this might help you in your investing journey, as the content remains very relevant.

If you find this useful, do support Financial Horse as a Patreon. You can get regular, up to date macro updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH, have been seeing you making call on commodities, esp oil. In your opinion, what oil related companies we can look at (I know you have a position in Shell – if not mistaken) or oil ETFs that carry less risks. Thanks !

Really depends on what kind of play you are going for.

If you just want an ETF something like XLE works. Or you can buy the oil majors like XOM or CVX or Shell for a relatively lower risk play.

If you want something more adventurous, you can check out oil services (eg. Schlumberger, Halliburton).

If you want even more leverage you can even go into the smaller oilfield services / exploratory plays.

There are a million ways to play the same macro theme, depends very much on you as the investor! 🙂

Surprised the articles did not mention Aussie as a key energy supplier. Seems that Aussie is probably a triumph card for BRICs or the West and both side will probably court for Aussie’s allegiance. Any thoughts on investing in Aussie in this perspective? But aiming to avoid potential drags from a downturn in Aussie ppty.

When you say invest in Aussie do you mean in Aussie commodity stocks? Or banks? Or real estate? Or just a broad ETF generally?

Like you said, Aussie market is very exposed to the commodity cycle, and they are also navigating a downturn in their real estate market.

If you want to stock pick in commodities, Australia is definitely a massive market you can’t leave out.

But more macro focussed investors who just want to play broad themes via ETFs may not need to go into this level of detail.

Australia’s actually pretty interesting. They are home to the big miners Rio Tinto and BHP. For Gas they have Woodside Petroleum. Heard their banks are well run and profitable as well. But I would certainly consider some Australian equities for the mining exposure. Issue I have is both Rio and BHP have 50% of their revenue coming from iron ore which is very closely tied to china’s investment cycle.

Dear FH

Thanks

Very difficult to plan so far ahead although the broad principles enunciated here are very relevant

What is not clear is the commodity bit ! The 20% essentially would entail equity exposure only for the majority f retail investors in the form of common equity , difficult to deal with the “real stuff”

This would eventually mean a 60% equity exposure! I would say that history has consistently shown that predicting commodity cycles leave alone super cycles, is notoriously difficult

However, I agree on oil and copper in that order- the best and easily feasible way for retail investors is to go for the equity or ETF option for oil and equity for copper and iron producers

This would eventually mean that the 40% would automatically fall into cash/bonds and FD and perhaps a tiny amount of non yielding gold

Of course, property is not in this calculation a you put it for local investors who are all very heavy on real estate – often by default!

Regards

Garudadri

Very good points!

I do agree that 60% equity exposure looks very high.

I think the better way to see it is that this is a broad high level framework to think about asset allocation. But for Singapore investors who will have a very high allocation to real estate and/or CPF, it will make sense to make the necessary changes as required.

On energy – last night OPEC+ supply cut shows the difficulty in trying to predict where prices can go. As much as the Feds want to bring energy prices down through higher interest rates, OPEC+ can easily play supply cuts.

And if it’s going to come down vs how high the Feds can hike vs how much OPEC+ can cut supply, there’s only going to be one winner here.

Just goes to show that this fight against inflation is nowhere near over.