I was reading a report by Blackrock recently.

Here’s an excerpt:

The Great Moderation, a long period of steady growth and low inflation, has ended in our view. We see macro and market volatility reverberating through the new regime.

What changed? Production constraints triggered by the pandemic and the war in Ukraine are pressuring the economy and inflation. We see this persisting amid powerful structural trends like global fragmentation and sectoral shakeouts tied to the net-zero transition.

We expect higher risk premia for both equities and bonds – so investment decisions and horizons must adapt more quickly. Traditional portfolios, hedges and risk models won’t work anymore, we think.

Blackrock’s Advice?

Here’s their advice to investors:

First, do a blank-slate exercise – imagine you have realized all your gains and losses.

Then construct the ideal portfolio for the most likely market and macro environment over your time horizon.

That doesn’t mean abandoning long-standing investment processes.

Instead, consider portfolio changes without basing it on your historical portfolio holdings and performance.

How I will invest $1 million for the next 3 – 5 years (as a Singapore investor)

Regular readers know that I love this exercise.

Imagine you own no stocks / REITs today.

All you have, is $1 million in the bank.

How do you allocate it into the market?

I love this exercise because it forces you to ignore all your existing positions and biases, and approach investing on a blank slate.

With that in mind, these are the ground rules:

- Long only portfolio – This is a long only portfolio. So shorting is out of the question.

- 3 – 5 year holding period – Long enough to smooth out the short term volatility from Fed actions

- No more than 10 counters – To minimize difficulty in implementation

What would be my biggest macro concern over a 3 – 5 year period?

Inflation.

I’ve been doing a lot of thinking about inflation recently.

And the more I think about it, the concerned I get.

Is Inflation Cyclical (transitory), or Structural (here to stay)?

Most investors think that inflation is cyclical.

They think that inflation is high because of COVID lockdowns and excessive stimulus, which increased demand while decreasing supply – causing prices to go up.

They think that once the Feds raise rates to 3.5% by end of the year, inflation will roll over.

And by early 2023, the Feds will start cutting rates, and we “solve” inflation for good.

What if inflation is structural?

What if inflation doesn’t go away so easily?

What if inflation is caused by a messy transition into a new, multipolar world order no longer dominated by American hegemon.

What if the supply constraints due to underinvestment in commodities, lack of workers, energy disruptions, don’t go away?

What if cases like Malaysia not exporting chicken to Singapore, are not a one-off event, but a rolling series of disruptions?

What if inflation is structural?

I plan to write a longer article for Patrons to expand on my view that inflation may be structural, and that interest rates may be higher for longer.

But for current purposes, let’s try to imagine what are the implications on one’s portfolio.

What do you want to own in inflation + higher interest rates?

In a higher inflation, higher interest rates regime, what you want to own are:

- Commodities

- Dividend Stocks

- Treasury Inflation Protected Securities (TIPS)

- Investment Grade (IG) Credit

- Cash

- Maybe – Precious Metals, Crypto

While what you want to own less are:

- Unprofitable Tech

- US Treasuries

- Maybe – REITs (depending on interest rates)

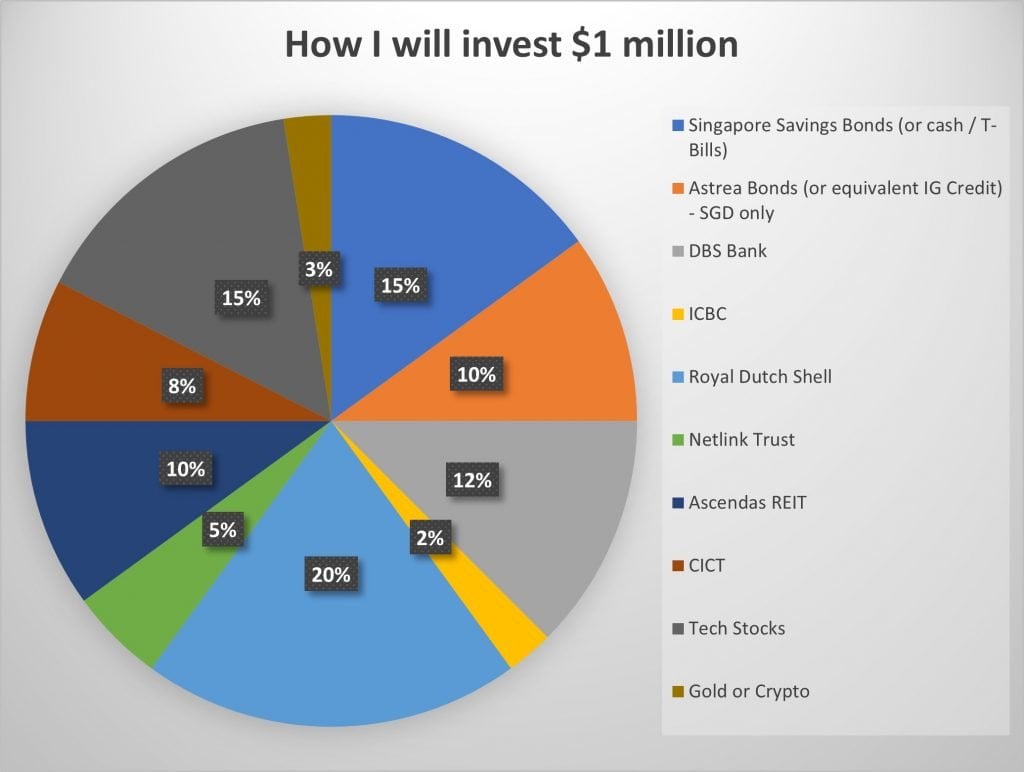

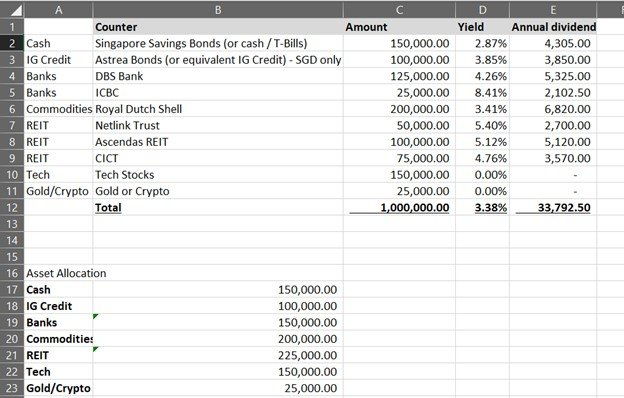

How I will invest $1 million for the next 3 – 5 years

With that in mind, this was the portfolio I came up with:

Here’s the portfolio in chart form:

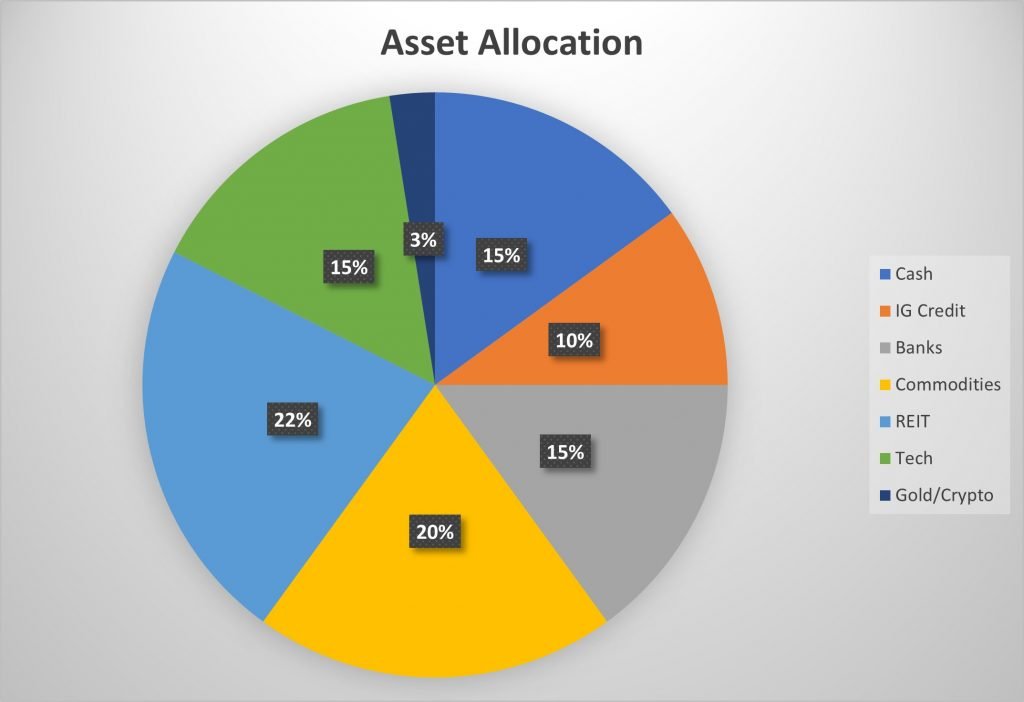

And here’s the asset allocation:

I know there will be a lot of queries, so let me address the big questions below.

BTW – We’re running a huge national day promo for the Stocks Masterclass. Learn how to invest in dividend and growth stocks in these volatile times. Find out more here.

What’s the biggest risk with this portfolio?

The biggest risk with this portfolio – is that I am wrong on my inflation outlook.

Inflation rolls over, interest rates go back below 2%.

In that case the commodities, banks, cash and IG credit (Investment Grade Bonds) do not do well.

How will I know if I’m wrong?

To guard against this, I would want to watch inflation and the Feds closely.

If I see inflation rolling over for good, or if I see a meaningful Fed pivot back towards easy money, I need to recognize that I am wrong.

And quickly switch portfolio allocations, back into what worked for the 2010s.

Basically long duration assets – long tech, long REITs, long crypto.

In investing, there’s nothing wrong with being wrong.

You just need to recognise it quickly, and cut losses quick.

Why so much dividend plays?

The reason why this portfolio is overweight on dividend plays – is that in a world where growth is slow and inflation / interest rates are high, dividend income is gold.

By its very nature these are more mature and stable businesses, so they are less likely to go under, and they have strong cash flows and pricing power.

With a portfolio like this, you’re getting about $34,000 a year in income.

That’s not too bad.

Why so much cash?

It’s not often talked about, but cash can do okay in a period of high inflation, mainly because of rising short term interest rates

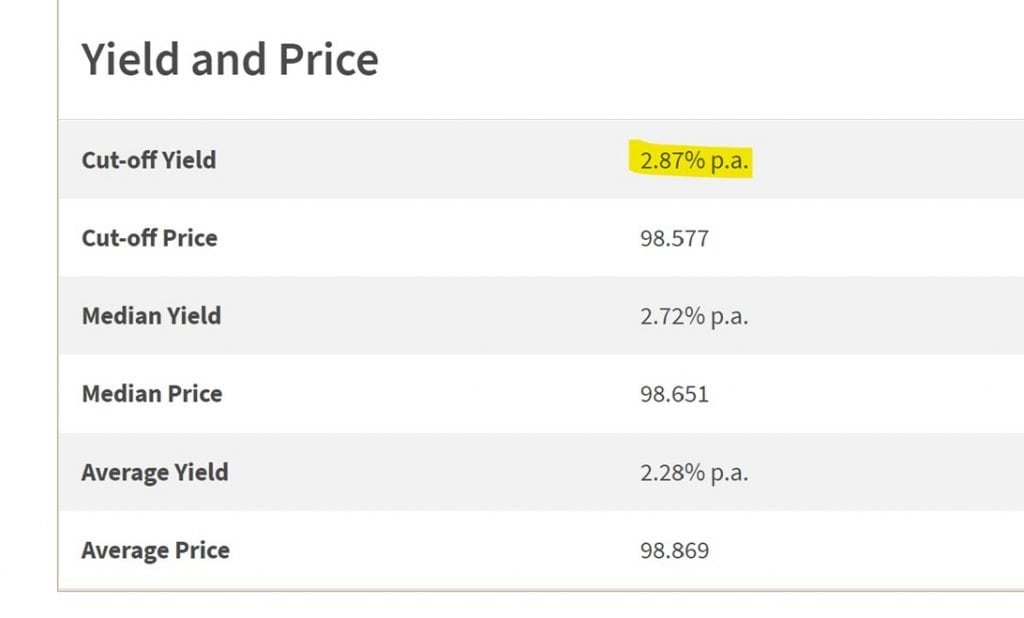

Look at the latest T-Bills auction.

You’re getting paid 2.87% p.a., completely risk free, to lend SGD to the Singapore government for a 6 month period.

For ZERO risk.

That’s one of the most attractive yields in a while.

Cash give you optionality

And in a more volatile macro environment, cash gives you optionality.

Cash gives you the confidence to take risk with the rest of your portfolio.

Worst case if you are wrong, cash allows you to buy the dip, or cover living expenses.

Why not more REITs?

Now I love REITs.

I’ve been dabbling in REITs since I started investing, and they are my favourite asset class, and one I am most familiar with.

My concern though – is that REITs did superbly well the past decade because of Fed fuelled liquidity.

A decade of low interest rates and QE powered real estate prices higher, while suppressing the cost of borrowing for REITs.

REITs are basically leveraged real estate plays, so they did fantastically well.

Now imagine we flip that regime on its head.

Imagine that going forward, interest rates go up, and stay up.

How sexy is Ascendas REIT with its 5% yield, if you can get 3.5% lending to the Singapore government risk free?

Now what if interest rates go up to 4.5% instead?

For the record though, I think high quality real estate in good locations can still do well in such a climate.

And what is why $225,000 goes into REITs.

But I didn’t want to overweight REITs because of this concern.

What about foreign REITs?

You may have realized that the REITs I picked are predominantly Singapore REITs.

And that’s by design.

I think over the next 3 – 5 years we are going to see significant FX volatility.

I think the Euro, Yen, USD are all going to have big moves, as central banks diverge on their monetary policies.

If you’re an active investor, there will be a ton of money to be made.

Just look at the kind of moves Daiwa REIT and Digital Core REIT are making. You can check out my more active views and positions on Patreon.

But for a long only portfolio, I decided to skip out all the drama altogether, and stick primarily to SGD real estate.

Am I buying commodities at a high?

With $200,000 allocated into commodities, I get that this is a risky play.

If we get a recession in 2023, there is a risk commodity prices come down in a big way.

The short term is very tough to call.

The way I see it though, is that the current solutions being proposed to solve the commodities undersupply are all wrong.

Most people credit Volcker with crushing inflation in the 1980s by raising interest rates.

But they conveniently leave out the fact that the 1970s saw US energy companies pour billions into new energy projects. While Reagan and Thatcher were busy breaking unions to reduce bargaining power of labour.

Look at the current solution being proposed.

Taxing windfall profits from Energy companies, and subsidizing fuel costs. Encouraging labour to unionise.

This is the exact opposite of what needs to be done to solve supply side constraints.

Biden went all the way to Riyadh, and the Saudis agreed to increase production from 12 million barrels a day to 13 million a day… by 2027.

Which means the Saudis will produce 1 million barrels more a day, in 5 years time, when the US is currently releasing 1 million barrels a day from the SPR.

The way I see it, until we see meaningful changes on the supply side, commodities inflation may stay tight.

And oil to me, is the purest hedge against commodities inflation.

I used Shell because of no dividend withholding tax for Singapore investors, but the US oil majors work well too if you don’t want the European risk.

Why not Treasury Inflation Protected Securities (TIPS)?

Another way to hedge inflation more directly might be via Treasury Inflation Protected Securities (TIPS).

These are US bonds that pay you a return that is pegged to inflation.

And frankly I think TIPS could be a good buy too, as the market may be under pricing inflation here.

My main concern as a Singapore investor though, is that TIPS exposes you to USD FX risk.

And over a 3 – 5 year period, I think there is a very real risk the USD goes lower versus the SGD.

Does the return from the TIPS outweigh the decline in the USD?

Maybe, but it’s not an easy call.

In any case I wasn’t confident on this one, so I just decided to skip TIPS entirely.

But I would love to hear your opinion.

What about Tech?

When I first came up with it, this portfolio did not contain tech.

But the more I thought about it, the more I realised that buying the right tech names can give you an inflation hedge, while also providing growth.

Semiconductors, monopoly platform plays, all of these have very real pricing power in today’s digital economy.

You do sacrifice the dividend income though, but you’re betting on capital gains.

The exact names to buy are probably beyond the scope of this article, but you can check out Patreon for the names I am keen on.

Why Gold or Crypto?

The problem with gold or crypto, is that they do not do well with rising real rates.

Real rates have been going up the past 6 months, so both have not been doing well.

At some point this cycle, the Feds are going to flip dovish.

Some may argue that this already happened last week on 27 July.

If so – gold and crypto could perform well.

Picking between gold and crypto

There’s no denying crypto is the more volatile asset here.

Which means more upside, and more downside.

But because I only allocated $25,000 to gold/crypto, I actually thought it made more sense for the money to go into crypto.

I see crypto as a long dated call option here.

If I am wrong, maybe I lose 50% on the crypto positions – which is only a 1.25% loss on the portfolio.

If I am right, crypto could go up a lot in the event that the Feds return to money printing.

Which really, is exactly how a long dated call option should work.

You’re risking a small amount of capital, for a small chance at a big upside.

It’s to hedge a right tail event if you like.

Closing Thoughts

For the record, I don’t profess to say that this is THE ideal portfolio to hedge inflation.

But if I am right, how to hedge inflation is going to be a question we will be asking ourselves repeatedly in the years to come.

And I would rather start asking the questions earlier rather than later.

I tried to take a first stab at it in the article above, but I do expect to be refining it as we move forward.

I leave you with this line from the Blackrock report:

Beware of behavioral biases in investing. We are guarding against their pitfalls because we believe the new regime requires an overhaul of portfolios. We’ve reduced portfolio risk throughout this year. Our latest tactical move: an up in-quality portfolio shift by downgrading developed market stocks and upgrading investment grade credit. We underweight U.S. Treasuries and overweight inflation-linked bonds, believing markets underestimate the new regime’s inflationary nature.

I know not all of you agree that inflation is here to stay.

I don’t profess to know the answer too.

But I encourage you to at the very least look at your portfolio, and imagine what would happen to it if we move into a regime of higher inflation and higher interest rates.

And decide accordingly.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

Do give it a try here.

As always, this article is written on 5 Aug 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH couple of thoughts,

IG credit actually does well when interest rates fall. Spread over treasuries is lower than HY, so they do function like treasury proxies. Astrea aside, an SGD IG credit etf can be considered as well.

On TIPs, it’s tricky as if you buy them outright, you actually suffer capital loss if real yields rise. You will have to hold to maturity to benefit from the higher inflation. Alternatively, you will have to long TIPs short USTs as a play on break even inflation being too low. Think there might be an etf for this but I haven’t checked!

On commodities, I do agree that energy is an apex commodity, ie the most important commodity that is used for the production of others. I would however include some of the metal miners (either BHP or RIO, both London listed) if we are looking at a 3-5Y time horizon. These are in short supply as well, and decarbonization is highly metals intensive (copper especially).

Hi Moomoo,

Great comments as always.

Some thoughts from me

1. I think the point of IG credit is to hold to maturity for the income. So some mark to market losses is probably acceptable. The problem with IG credit etf is that they will never mature as the fund manager will just roll over the funds, so at some point in a rising rate environment you will need to lock in the loss.

2. Interesting point on long tips short ust. Could work, might be something that needs further investigation. Might not fully solve the usd fx though.

3. I was looking at the miners too. The recent correction has been drastic. A lot of noise over potential recession and demand drops. Commodities are always tricky to predict in the short term without a deep understanding of the supply demand dynamics, and I just don’t have that kind of understanding with copper or metals. Which makes me wary of going in too deep.

Fantastic points though, lots of food for thought.

What about property?The last I heard, HDB flats are crossing the 1 million mark like nobody’s business

Yeah I like property, actually bought another property last year which has done well since. Not for everyone though, the liquidity, transaction costs, and leverage are real issues to consider. Not to mention that prices now are very high!

Why put 20% of the portfolio in RDS and take all that single issuer risk? Crazy. I’m old enough to remember Deep Water Horizon. Have a look at BP’s share price when that happened, and have a look at its competitors at the same time.

I’d go the ETF route. WNRG is a globally diversified UCITS with an index yield of 3.8%. VDE is the US flavoured option, with a very strong value tilt, similar yield and 0.10% charge. VDE has significantly more beta than XLE. A few weeks ago I was sitting on 200%+ gains after hoovering it up in October 2020. It’s a no brainer.

Do u think it is time to lock in some profits?

Cant decide whether to sell now to lock profits in bear market rally or just hold through. Could be heading for the last leg or last few legs down. Overall up 11%, bought lump sum cash in June.

Anyway FH I appreciate your blog. Do accept that if your blog is popular among actual investors, traders and finance bros, they are gonna say something. They might not agree, but they are actually reading your blog. Most other SG finance blogs are so bad, like teaching how to buy cheap things at NTUC or giving you a ton of data with no idea how to interpret the data.

Thanks! Appreciate the kind words this means a lot.

To answer the question – I think it depends on your asset allocation. If you’re v overweight on risk and felt uncomfortable in the recent decline, you’re prob overexposed and wouldn’t hurt to use this rally to reduce risk.

But if you have healthy cash allocations and don’t want to time, another option is to just hold as well. I still think market is mispricing recession risk here. A recession will likely come, but not as fast as the market is pricing in. Jobs and consumer data are still holding up well.

Oh yes you are right this is a great point. Agree with you, the energy position should be more diversified away from single issuer risk.

Thanks for raising this!

Hi FH,

Some good comments on TIPs and commodity ETFs here from sound investors.

Instead of investing in bonds or SSB or Astrea, why not consider that your CPF is already bond-like (income, dividends, albeit hold to maturity)? Reits in your portfolio already provide the income component with upside. Bonds are an asset class loser in high inflation, high interest rate regimes.

While commodity stocks are correlated with inflation, they have already rallied strongly, doubling even. That’s not to say there is no more upside, we just dont know. But these are highly cyclical stocks, strongly sensitive to recession cycles. If there is a recession as you say, I wouldn’t risk a portfolio overweight in commodity stocks. A broad based ETF in global or US equities would do with a market weight to commodity producers. Like Matt mentioned, I would be wary of single stock risk. RDS is exposed to GBP structural decline. I also remember share price shocks to BP, Rio and Glencore (mining). Commodity and energy stocks are old companies with entrenched cultures, it is hard to say when a pollution event or lawsuit could give your single stock position a 30-50% shock.

Just sharing my thoughts. Thanks for sharing your ideal portfolio!

Thanks, fantastic sharing.

Some quick thoughts from me:

1. Agree that cpf can replace cash or bonds. There are certain unique liquidity issues around cpf though, do it shouldn’t replace cash entirely, but can definitely play a part in the fixed income portion of the portfolio.

2. Agree on commodities being weak if there is a recession. I intentionally did not go into execution or timing issues in this article as that would add a further layer of complexity. Wanted to keep this article purely on asset allocation.

3. Agreed on single stock risk. Will remove rds and replace with an etf or at least a couple of stocks.

Sorry mate…I think your portfolio is confusing…on one hand you cap your risk by limiting Reits holding and buying into more bonds for peace of mind….but you took huge risk in crypto which can swing up down 10 20 percent overnight…at 25k it is small sum out of the 1M but your projected return of the entire portforlio is only 33k/yr…so I am not sure what is the purpuse of this 1M plan….to decay due to the inflation or to hedge? If the div raised further, Reits may suffer for short term but it will adjust itself when the rental is renewed….besides bank should do well during that period….the latest results of the 3 banks proven that….they will cancelled out the shortfall from other assets…to me keeping cash, gold or crypto in this junture is a waste of opportunity(to buy low) because they don’t pay while you wait…come back one year later to see if I am correct :p

Understand your point.

I think the problem is that this portfolio is designed to be a long only passive one, without active timing. So it’s designed to be safe and do broadly well over the next few years, but at the same time it would not be superbly well.

The 33k is dividend income only, doesn’t include potential capital gains.

But really good point though. Let me think about how to refine the portfolio further.

How to buy $100k worth of ssb when the demand so hot. Every person can only get like $10k. U have to wait for a long time to accumulate.

Inverted yield curve, recession coming. Why not hold cash??

If fed print money, then inflation will persist for sure. Actually isn’t inflation a year-on-year metric? If prices stay high unchanged then inflation for 2023 vs 2022 will be low.

For TIPS, not worth buying due to capital loss. See the tips etfs charts.

There is one etf directlinked to inflation: rinf. But now so high, dont dare to buy.

Can you share how tips work? Why the etfs dropped??

Can buy t bills or sgs for the rest. You do sacrifice a bit of liquidity, so it’s up to each investor to determine the right allocation for themselves.

Tips are tied to inflation expectations. Investors expect Powell to hike us into a slowdown which will crush inflation, hence forward expectations are low. If you disagree with this, then tips could be a good way to play that trade.

You mentioned that in the next 3-5 year Sgd likely to outperform USD. Can I have your thoughts on the impact on USD denominated property stock listed in SGX. ? Thanks

It will depend on the type of property in qn. The US real estate market is the largest in the world, it won’t be easy to generalise. Properties in NY could do well for example, while those in Chicago suffer. Answer will have to be nuanced and does not lend itself to easy generalisations.

Hi FH, when you said “I used Shell because of no dividend withholding tax for Singapore investors”, how does this work? By buying Shell from London stock exchange where dividends absolutely has no tax? Thanks in advance.

Yes, you’ll want to buy the Irish domiciled counter listed on the London Stock Exchange for no withholding tax into Singapore. 🙂

Cool thanks Sir. Thanks for the generous sharing 🙂

Glad it’s helpful!