For dividend investors, 2022 has been like Christmas come early.

Singapore Savings Bonds paying higher than CPF (2.71%).

Astrea 7 Bonds at 6% yield.

And solid, blue-chip S-REITs trading at 5.5% yield.

Dividend investors are spoilt for choice in this market.

6 months ago I shared my game plan on how I would invest $100,000 into S-REITs in 2022.

6 months on – with big changes in REIT prices, big changes in global macro, I figured it was well overdue for an update.

Rules to invest $1 million in Singapore REITs in 2022 (at 6% dividend)

The rules are simple:

Using today’s prices – I will take REIT prices as they are today.

How I would do it – I will use my own risk appetite, and my own portfolio.

How I will invest $1 million in REITs in 2022 (as a Singapore Investor)

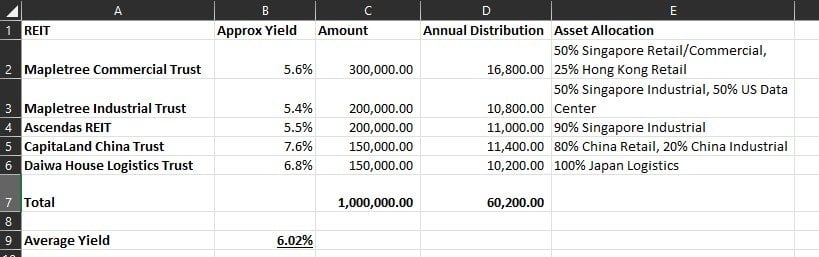

Here’s how I would invest $1 million in Singapore REITs in 2022, at a 6% yield:

In word form:

- Mapletree Commercial Trust (5.6%) – $300,000.00

- Mapletree Industrial Trust (5.4%) – $200,000.00

- Ascendas REIT (5.5%) – $200,000.00

- CapitaLand China Trust (7.6%) – $150,000.00

- Daiwa House Logistics Trust (6.8%) – $150,000.00

Approximate yield for this REIT portfolio is about 6.0%, or about $60,000 a year.

Update: Been getting some questions on how I computed the yield above. To explain, I mostly took the latest DPU figures and annualised them. And for MCT I am using the pro-forma numbers assuming the merger with MNACT merger is complete. That would explain some of the discrepancy with the other yields you guys are using.

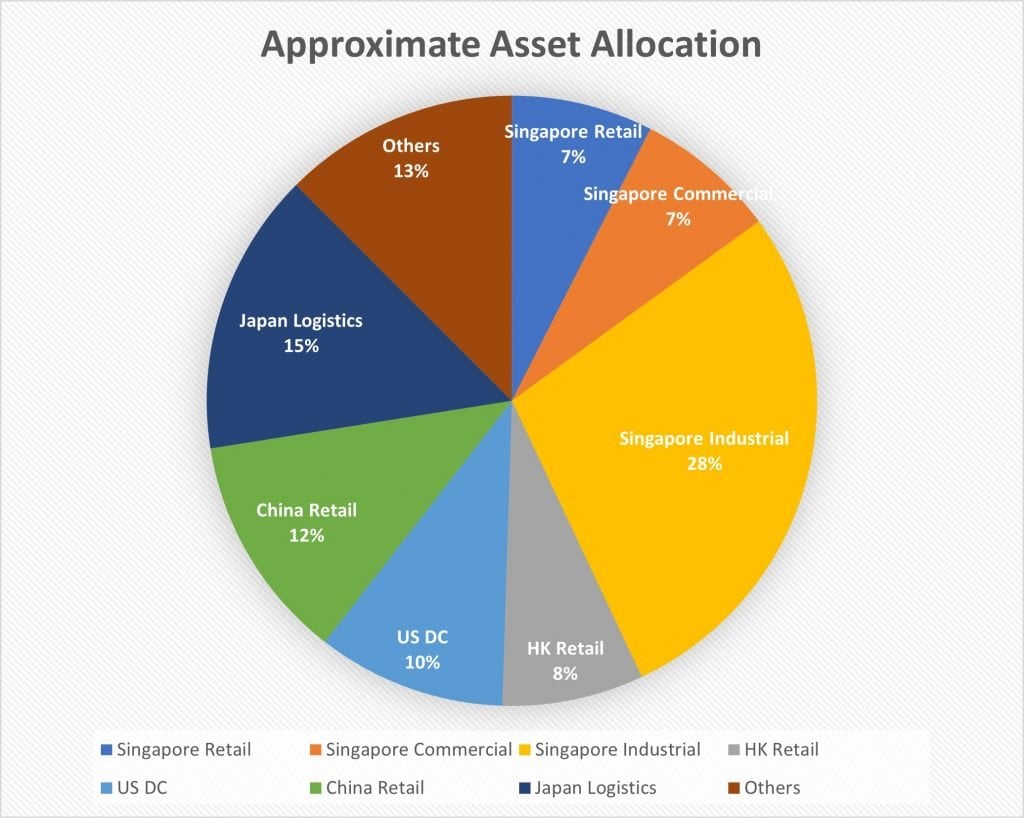

And the broad asset allocation is set out below.

I know there are going to be a ton of questions, so let me address the biggest ones below.

High level questions (Macro / Portfolio)

What about rising interest rates? Do you lump sum, DCA or market time?

The elephant in the room – rising interest rates.

How do you invest $1 million in REITs in 2022, with a rising interest rate environment?

Do you lump sum at one go?

Do you dollar cost average over a 12 month period?

Do you try to time the bottom based on macro conditions?

How I would do invest $1 million in REITs?

The answer will differ for each investor.

For me personally, I would try to time the market entry.

My personal view, is that REITs at current prices are already attractive for long term positions.

If you buy now and hold for 10 years, you’re *probably* not going to lose money.

And to put money where my mouth is, I’ve been buying REITs the past few months (you can see what I’m buying and my full personal portfolio on Patreon).

My only qualifier is that I don’t think interest rates have peaked just yet. And I don’t think equity markets have bottomed just yet.

So yes REITs are cheap, but they could get even cheaper.

What signals would I watch out for to start buying REITs in 2022?

Pricing wise, blue-chip REITs like Ascendas REIT bottomed out at a 6% yield in 2018, so that would be my line in the sand (they are 5.5% yield now).

And macro wise I would be watching out for the peak in interest rates.

I think the 10 year Treasury will cross 3% again before this is over, and markets may reprice the terminal rate.

That would be an important signal for me in signalling the bottom for fixed income.

How confident am I in calling the bottom in S-REITs?

Not confident.

The tricky part is that I may be right in calling the top in US Bond yields, but completely wrong in calling the bottom in REITs.

Think back to 2008.

The Feds started cutting in June 2007. But the equities market didn’t bottom until early 2009, almost 1.5 years later.

Whether this is going to look like 2008 or more like 2011 / 2018 / 2020 (with a quicker bottom), is anyone’s guess.

But personally I am preparing for both scenarios, and I will adapt my investment strategy once it becomes clearer which path we will take.

As investors, it’s important not to be dogmatic.

When the facts change, don’t be afraid to change your mind.

If you are keen, I share updated views on Patreon as this plays out.

Why so much Industrial REITs exposure?

So the market has its own little moods.

There are days when it loves Stock A.

And days when it hates Stock A.

But the long term fundamentals of the Stock seldom changes all that much.

As a long term investor, you want to invest countercyclically. Buy Stock A on the days when the market hates it.

Retail and Office REITs were hated for much of the past 2 years. While Industrial and Data Centre REITs were the golden boy.

And now in 2022, we’re seeing the exact opposite. Industrial and Data Centre REITs are the unwanted child, while Retail and Office REITs are much loved.

Well, to succeed as a long term investor, just do the exact opposite.

I’ve accumulated retail and office REITs the past 2 years heavily.

In 2022 and moving forward, I see myself likely to be accumulating Industrial, logistics and Data Center REITs.

That’s just where I see the most value right now, for my kind of time periods (very long term).

Why so little Retail / Office REITs?

Take CICT for example.

It’s my largest REIT position, and it trades at a 4.7% yield.

Would I rather buy CICT, or go with Ascendas REIT / Mapletree Industrial Trust at a 5.5% yield today?

Personally I would go for the latter, and come back to retail/office when prices turn more attractive again.

Why so little Singapore REIT exposure?

Okay that’s a really good question actually.

Singapore exposure comes in at less than 50% of this REIT portfolio.

Why so little?

It really comes down to a risk-reward question.

Singapore real estate is safe, but for that safety you’re sacrificing yield.

If you build a pure Singapore REIT portfolio you’re probably looking at low 5% yields.

No way around it – that’s just how real estate is priced in this market.

You can complain that Singapore real estate is overpriced, but if you want to invest in today’s market, that’s the price you have to pay.

Personally for me I didn’t mind taking some measured risks, in order to juice the REIT portfolio up to 6% dividend yield.

The measured risk I wanted to take are mainly:

- Japan Logistics (Daiwa House Logistics Trust)

- China Retail (CapitaLand China Trust) and

- Hong Kong Retail (Mapletree Commercial Trust).

It’s probably worth discussing each of them, because those are the most controversial parts of this portfolio.

I don’t think anyone will have much questions over the Ascendas REIT / Mapletree Industrial Trust positions.

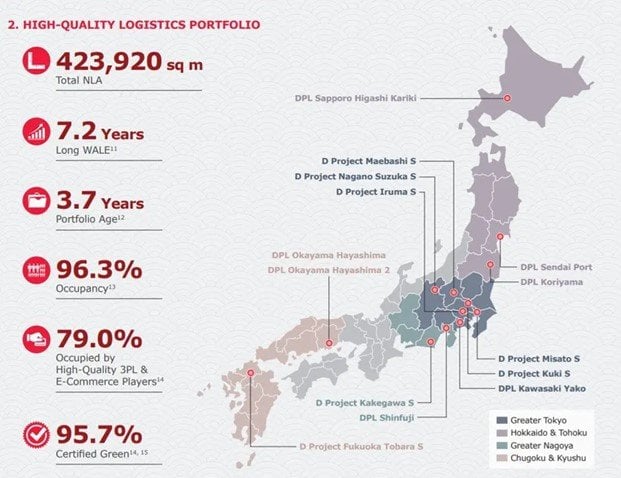

Japan Logistics (Daiwa House Logistics Trust) – 6.8% Dividend Yield

Daiwa House Logistics Trust IPO-ed the same month as Digital Core REIT.

And for some reason the latter got all the attention, and Daiwa House just flew under the radar.

I applied for both, and funnily enough only got Digital Core REIT.

Whatever the case, I’ve flipped my Digital Core REIT for a profit, and now it’s Daiwa House that I am looking to open a long term position in.

I dunno – Japan logistics portfolio, backed by a solid Japan sponsor, at a 6.8% yield, pretty attractive in my books.

Of course the sponsor is an unknown in the Singapore scene, and they are likely to expand into Asian logistics over time so they will need to do a lot of fundraising. Conflict of interest is an issue too.

But like I said, if you want something lower risk stick with the blue chip REITs at a 5%+ yield.

There’s really no free lunch.

China Retail (CapitaLand China Trust) – 7.6% Dividend Yield

Regular readers know that I am a long term China bull.

The difficult part about investing in China, is (1) finding ways to profit from China’s growth, (2) having long term holding power, and (3) investing via reputable managers.

CapitaLand is one of the best operators out there, and being offshore and Temasek backed gives them access to financing and credibility that many of the onshore players lack.

This gives you holding power as well, as you don’t need to worry about default risk.

Which only leaves (1) – will this real estate portfolio profit from China’s long term growth?

Personally I like its real estate portfolio with almost 50% allocation to Tier 1 cities, but hey it’s your money.

Whatever the case, this REIT trades at a 30% discount to book and a 7.6% yield right now.

Hong Kong Retail (Mapletree Commercial Trust) – 5.6% Dividend Yield

Let me put it out there – I’m not the biggest fan of Festival Walk (Hong Kong Retail Mall).

But at the right price, I could be convinced to buy.

My fair value for MCT is about $1.8, and with the REIT trading at 1.7+ it does look quite attractively valued.

It’s also now the only way to get exposure to Vivocity and Mapletree Business City, and at a 5.6% yield, there are worse REITs out there.

Pretty attractive yield spread vs CICT too, which trades at a 4.7% yield.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

What other Singapore REITs did I consider investing in?

For the record, I looked at a whole bunch of other REITs as well.

I know many of you write in to ask my views on them, so I wanted to try my best to cover what I can.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

- Lendlease REIT (5%)

- CICT (4.7%)

- Keppel REIT (5.0%)

- Keppel DC REIT (4.4%)

- Mapletree Logistics Trust (5.22%)

- AIMS APAC / ESR Logos (7%)

- FLCT (5.5%)

- Ascendas India (6.8%)

Lendlease REIT (5%)

As shared in an earlier article, I opened a position in Lendlease REIT recently.

I like this REIT for the decent sponsor and great real estate portfolio.

What I don’t like about it today is the price.

Ideally I would want to pick it up in the low to mid 70s, which is a 5.5%+ yield.

CapitaLand Integrated Commercial Trust (4.7%)

Fantastic REIT, one of the bedrock positions in my portfolio.

Looks a bit pricey as things stand, ideally I would want a 5%+ yield to add.

Keppel DC REIT (4.4%)

I never really got the appeal of data center REITs.

They’re just buildings that house a bunch of computers.

Real value lies in the guy who makes the semiconductors, or who owns the data.

At a 5%+ yield sure I would consider, but at 4% yields Keppel DC REIT doesn’t look all that attractive.

Mapletree Logistics Trust (5.22%)

Okay I have a position in MLT, and I think it’s a good REIT.

But with their 20% exposure to China and 22% to Hong Kong, I think the yield is on the low side to add.

5.5% – 6% and we’re talking.

AIMS APAC REIT / ESR Logos REIT (7%)

Take nothing away from the smaller REITs, but the quality of a sponsor is a deal breaker for me.

I almost never invest in REITs where I am not comfortable with the sponsor.

AIMS APAC REIT, ESR LOGOS REIT, they’re probably decent REITs, and I know many people love them.

But personally I don’t think the 1.5% yield spread vs a blue chip like Ascendas REIT / Mapletree Industrial Trust justifies the additional risk you’re taking on with the real estate portfolio and the sponsor.

But really – it’s your call.

Frasers Logistics & Commercial Trust (5.5%)

I know many of you love Frasers Logistics & Commercial Trust.

It’s done very well since IPO, mostly thanks its Australian portfolio.

At current price though, it trades at a 5.5% yield, which is on par with stuff like Ascendas REIT.

And for me I’m not familiar with Aussie real estate the way I know Singapore real estate.

So if you give me a choice between 2 blue chip REITs at the same yield, 1 with Singapore exposure and 1 with Aussie exposure, I go for the Singapore REIT any day.

But I could just be an ignorant horse, and FLCT lovers – please educate me on why I am wrong.

Ascendas India Trust (6.8%)

Many of you have asked, and unfortunately I don’t follow Indian real estate, so I really can’t comment on Ascendas India Trust.

Real estate is a local business.

If you can’t be bothered to take the time to understand the intricacies of the local market, you’re better off not investing.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Closing Thoughts: Don’t underestimate the macro

I think a lot of investors may be underestimating the macro volatility that lies ahead.

Most people are assuming a market crash -> Feds cutting -> buy the dip.

I mean of course that is possible, but that belies the true range of possibilities.

The tail risks are just very fat here – both on the upside and the downside.

Imagine the Feds Funds Rate at 2.5% in December 2022, but oil trading at $200.

What is that going to do the terminal rate?

Or think about a Ukraine-Russia ceasefire, and oil dumping to $80.

How much do stocks rally in that scenario?

Recession not necessarily a done deal

All the forecasters out there calling a recession like a done deal – I think it’s too premature.

Sure all the macro data is pointing towards a slowdown, but whether it’s just a slowdown or a recession to me is not very clear yet.

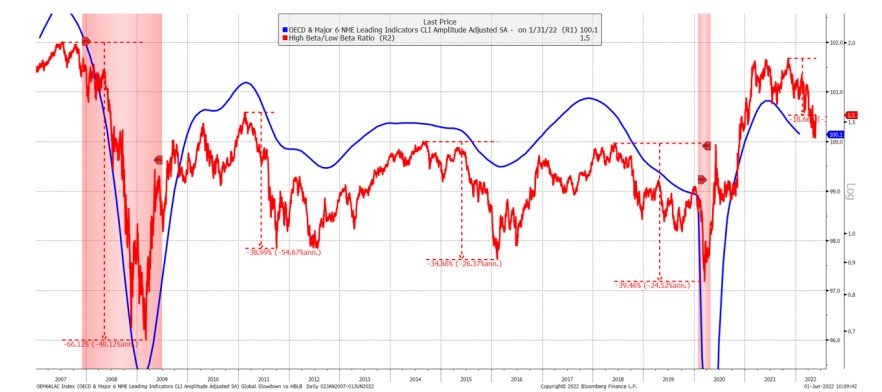

The chart below puts this into perspective.

We’re about 20% down in the S&P500 high beta/low beta index.

In 2011, 2015 and 2018 (no recession, just slowdown), the bottom was about 30-40% down. Which means we are halfway there if this is just a plain slowdown.

In 2008 (recession), the bottom was 66% down. Which would mean we’re not even one third there if this is going to be a broader recession.

The point I’m trying to make, is to be alive to the risks, both to the upside and downside.

The path forward isn’t 100% clear, and it would be wise to position accordingly.

As always, this article is written on 3 June 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hello

I’m a bit new to S-Reits but in your article you listed the approx. yield for the 5 S-Reits (set out below) – but looking at the SGX website under valuation and then dividend yield for these 5 S-Reits there is quite a difference and I wondered why? – are your numbers forward looking while to SGX website is looking at the past?

(apologies is the formatting of the table below is mis-aligned)

Figures taken from SGX website on 04Jun22

Fin Horse SGX Yield Diff +/-

Approx. Yield

Mapletree Commercial Trust 5.60% 4.29% 1.32%

Mapletree Industrial Trust 5.40% 4.74% 0.66%

Ascendas REIT 5.50% 4.80% 0.70%

CapitaLand China Trust 7.60% 7.53% 0.07%

Daiwa House Logistics Trust 6.80%

Apologies I should have explained this in the article. I added a note to clarify this point, extracted below:

Update: Been getting some questions on how I computed the yield above. To explain, I mostly took the latest DPU figures and annualised them. And for MCT I am using the pro-forma numbers assuming the merger with MNACT merger is complete. That would explain some of the discrepancy with the other yields you guys are using.

Never ever invest for dividend , u will end up paying them dividend.

Hahaha

Hi FH, Thanks for the article.

There are reits like lendlease, frasers centrepoint, mapletree commercial, capitaland china and the US Reits, where with Dividend Payout Ratio of more than 100%, would this be a concern ?

Yes of course. But the better question is to ask why is payout ratio so high, and whether it is a symptom of a deeper underlying problem, or a one-off.

The payout ratio is just the symptom, one needs to dig deeper to find the “disease” to decide what is the risk in play.

Hi FH, Thanks for the article.

There are reits like lendlease, frasers centrepoint, mapletree commercial, capitaland china and the US Reits, where with Dividend Payout Ratio of more than 100%, would this be a concern ?