What a week… again!

So many of you have reached out with questions on (1) what to buy in this market crash, and (2) when to start buying.

I’ll try my best to respond to each query, but do give me some time to work though the list.

On that note – we’re running a big Chinese New Year Promotion for the FH Stocks MasterClass now.

If you’re serious about deploying big money in 2022 – really do check it out.

This is going to be a big year dominated by macro, where the slightest mistake can easily wipe out tens of thousands of your hard earned money (just like we’ve seen the past few weeks).

So don’t be penny wise pound foolish here. Learn how to invest properly.

The course fee will pay for itself many times over. Check it out here.

When to start buying stocks in 2022?

I’ve set out a great question from a reader below:

Hi FH,

The Fed has signalled they are going to embark on a hiking cycle, and the US & SG market are selling off.

Do you have any thoughts on timing?

Specifically, how “fast” will this sell off be?

So my worry, is we are too slow in buying the dip, and stocks rally once the market shrugs off the “known facts of the Fed’s hike cycle”. I do have painful memories of missing out in March 2020, where the cycle was much faster than I had expected (in 2008, it took wayyy longer to play out). Should we be expecting the same this time around?

I have started adding in to some names I like, but I worry I am too early, and this might take a longer time to play out. In my mind, the difference between now and March 2020, is that that the Fed took a Bazooka out, cutting rates to zero and doing massive QE all in one swift move. So on hindsight, that dictated the speed of the move. This time around seems slower, as they will be hiking every few months and also thinking about how to unwind their balance sheet.

There’s basically 2 parts to this question:

- When to start buying (how to avoid buying too early)

- How quick to buy (do you all-in or average in)

My Short Answer

My short answer is:

I don’t know how long the sell-off would take to play out, but I don’t think this is the bottom for this credit cycle.

To me, the bottom will be when the Feds change their mind about rate hikes.

Just watch the Feds in 2022. If they do go “all-in”, so will I. If they hang fire, so will I.

So that’s the simple, 1 paragraph answer. Let me share why I think this way, and how I plan to invest my money in 2022.

Market Timing – Feel free to skip if you DCA

Now for obvious reasons, this will be market timing.

I know some of you are quite allergic to market timing and prefer to dollar cost average, in which case feel free to skip this section and jump to the part on what to buy.

The Most Hawkish Fed since 2018

In my view – everything will turn on the Feds in 2022.

So it’s wise to talk about the latest Press Conference that Jerome Powell did on Wednesday.

And to sum it up… This is the most hawkish Fed since 2018.

The answer to every single question thrown at him was basically… yeah well… we’re going to hike anyway.

To summarise:

- Nothing is off the table – hikes at every other meeting (7 hikes), 50 bps March hike, all possible

- No concrete details on Quantitative Tightening – other than that it will start shortly after rate hike in March

And the real kicker?

The comment from Powell that: “I think there’s quite a bit of room to raise interest rates without threatening the labor market,”

That was when risk assets puked across the board.

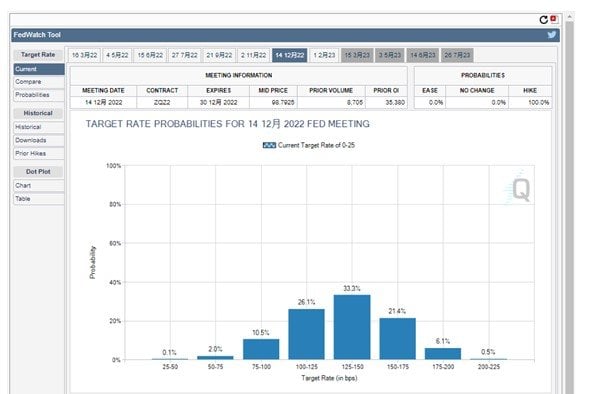

What is the market pricing in?

The market is now pricing in 5 rate hikes for 2022, which is just plain nuts if you think about it.

Market is also pricing in a real possibility of a 50 bps (0.5%) rate hike in March 2022, and 25 bps per quarter after.

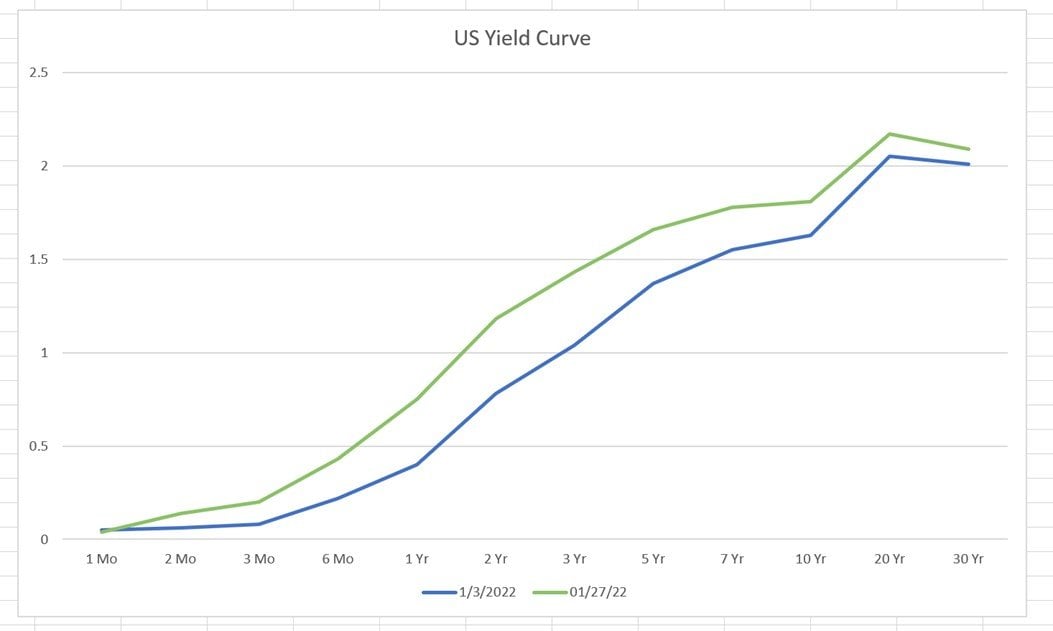

The yield curve has also steepened noticeably, as compared to just earlier this month:

2022 is a year to “Respect the Macro”

I’ve been repeating this for quite a while now, but I just want to put this out there again.

2022 is a year to respect the macro.

This is a year to respect the Feds, and respect fund flows.

Don’t get too cute with individual stock picking.

There will come a time to buy in size, but I don’t think we are there yet.

Stay big picture, until the macro picture turns favourable, and then go in big.

Can stocks bottom before the Feds blink?

As the reader pointed out above, what if the market bottoms before the Feds blink?

Such that by the time the Feds blink, stocks are already up 20%.

Historically speaking, this usually doesn’t happen. In all previous rate hiking cycles, 2018, 2008 etc, the market doesn’t bottom until the Feds pivot.

But I mean, I can’t say this is impossible.

What is required for this to happen, is:

- Stocks fall to an attractive enough valuation

- It becomes obvious that the Feds will reverse course

On (1) I think that ship has sailed. After a decade of easy money, the drop in valuations required for risk assets to become “fairly valued” is more pain than the western economy can bear.

Which leaves (2) – at what point does it become so obvious to the entire market that the Feds will be forced to reverse course?

In my mind, the only 3 possibilities are:

- S&P500 melts down 20-30%

- Treasury (or credit) markets break

- Inflation goes away

So let’s discuss each of them.

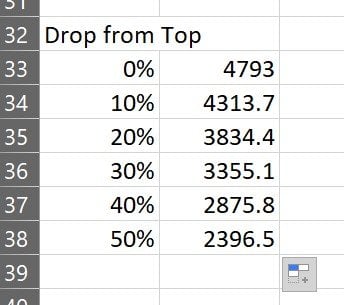

S&P500 drops 20-30%

Where we are today, the S&P500 is down only 10% from its top.

If we’re going to see a 20-30% drop from highs, there’s potentially a lot more pain to come in 2022.

Measured by this metric – the bottom for 2022 is not in yet.

Can the Feds change their mind before a 20-30% drop in the S&P500?

Unlikely – Fed’s short term goal is to curb inflation, even at the cost of financial markets.

If that wasn’t obvious to you before, that should be very clear now after Powell’s remarks on Wednesday.

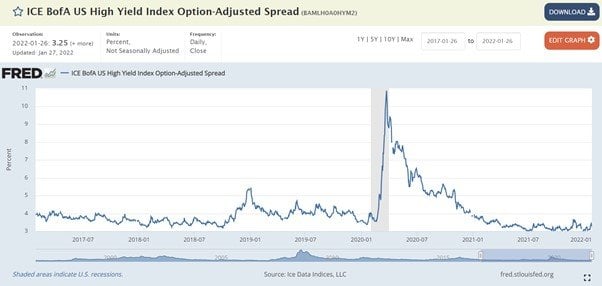

Treasury (or credit) Markets Malfunction

Credit spreads are holding up pretty well:

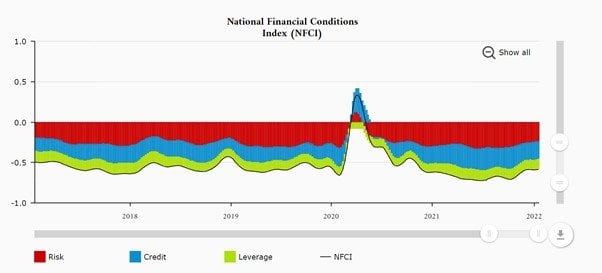

And financial conditions are still very loose:

Some of you may point out that these are lagging indicators, and I don’t disagree.

Credit markets can be quite opaque, so this one is a wildcard.

If the Feds hike 5 times and QT breaks the credit market, then yes absolutely, I agree the Feds will reverse rate hikes and I would absolutely all-in at that point.

That said – My personal view, is that with Reverse Repurchase Agreement Operations (RRP) and Supplementary Leverage Ratio (SLR) the Fed is much better placed than in 2019 (from a regulatory and reserves perspective) to manage any breakdown in credit/treasury markets.

It’s quite a mouthful, but all I’m trying to say is that don’t count on treasury / credit markets breaking down so soon.

Don’t expect treasury markets to collapse by March 2022, such that rate hikes and QT are off the take.

In fact I think we could see a fair bit of quantitative tightening before anything starts to really break in credit.

Inflation goes away

Spin it whatever way you want, but inflation is a political issue.

In a year with midterm elections, the political mandate is to curb inflation, even if it comes at the cost of the financial markets.

So naturally, if inflation goes away, then the Feds will stop hiking.

The problem though, lies in the feedback mechanism between monetary policy and rate hikes.

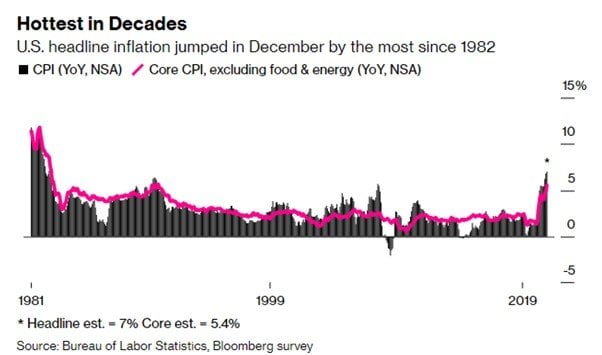

Don’t forget that despite US inflation being the highest since 1982, we’re still at zero interest rates and the Feds are still buying treasuries.

By the time they finally hike in March, it may take a while for that to feedback into the inflation numbers. Assuming 6 – 12 months, earliest we see the impact is in Q3.

There’s potentially a lot of pain between now and then.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What if I am wrong?

Let’s stress test my thinking with a couple of scenarios.

What if I am wrong, and this is the bottom?

The question then is what is my opportunity cost.

The opportunity cost of sitting in cash and missing out the bottom, is how much will stocks go up between now and the point that I decide to buy.

And I think the answer to that is – How much can stocks go up in a year when the Feds are hiking 5 times and going to start on Quantitative Tightening?

I just think that the risk reward is skewed here.

If indeed this is the bottom I frankly can’t see growth stocks screaming 50% higher in the face of 5 rate hikes.

Whereas if this is not the bottom, growth stocks still have a long way to fall to even come close to a reasonable valuation.

What if Stocks just trade sideways from here?

This is actually a real possibility too.

That after the January sell-off, stocks just trade sideways for the year.

The good part about this is that there is no opportunity cost, because you can just buy in later in the year at the same prices.

So while this is possible, this doesn’t create any downside.

What if the economy is strong enough to absorb rate hikes + QT

Actually, this is my base case.

I think the US economy could be strong enough to absorb rate hikes and QT.

I just don’t think the stock market is strong enough to absorb it.

So the Feds need to do this for the sake of the real economy, which will take down the stock market.

Once enough pain is inflicted, they will reverse course.

How “fast” will this selloff be?

As to how fast the selloff will be, I frankly don’t know.

That said, I would be highly surprised if the S&P500 plunges 30% from highs without even a bounce.

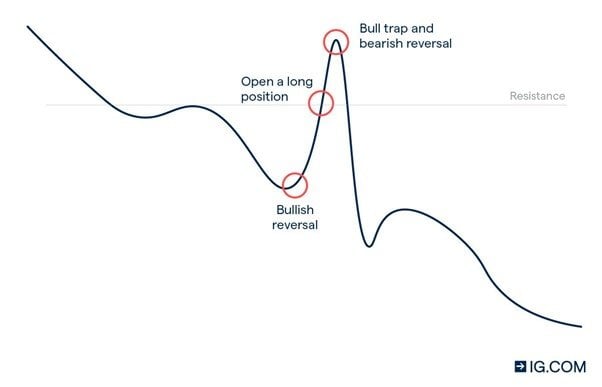

I would expect to see many bull traps on the way down, as that’s how the market extracts maximum pain:

You can argue that because of social media and information flows, the market structure is fundamentally different these days. You can also point to how March 2020 was a v-shaped recovery.

That’s possible, and like I said, I don’t have a strong view on the pace of the sell-off.

What I would say though, is that the market was poised for a rebound on Monday/Tuesday, but it broke through those support levels quite convincingly.

Yesterday’s close indicates the possibility of a short term rebound next week, but we’ll again need to see if the support levels hold.

If you want to trade markets day to day, then you need to be monitoring the charts very closely.

How “fast” will the recovery be?

In 2018 it was a v shaped recovery:

So was it in 2020, and 2008.

Personally I would expect the same here.

But in any case it’s way too early to call, the Feds haven’t even started on their first rate hike yet.

What I would say is that you really want to watch the Feds reaction.

If they switch to a reduced pace of hikes and slower QT, that might not call for a V shaped rebound.

If they slash rates to zero and embark on unlimited QE + buying junk bonds (like March 2020), then yeah absolutely you go all-in.

How am I investing?

As shared in previous articles, I’ve quite drastically slowed my rate of purchases since September 2021.

At this point in the cycle, I’m sitting on a lot of cash that I intend to deploy in 2022.

My plan is simple.

I do nothing until I see the Feds changing their mind.

And when the Feds change their mind, I buy the dip, in size.

Until the Feds change their mind, I see any big rallies as countertrend moves (in a broader decline).

Frankly I’ve already done most of my portfolio pruning late last year, so everything in my portfolio at this point are stocks I want to hold long term.

At some point this year, I may also take profit in my cyclicals like DBS/UOB, and free up that cash to buy beaten down stocks.

You can check out my full portfolio with weekly updates on Patreon.

How would I invest $100,000 in 2022?

I don’t see myself deploying most of this cash until perhaps Q2-Q3.

So it might be a bit early to talk about how to deploy the cash.

But for now, indicative plans are:

- 50% REITs

- 35% – MIT, MLT, Ascendas

- 15% – CICT

- 50% Stocks

- 30% – QQQ

- 20% – Stock Pick

BTW the $100,000 is just an indicative number for easy calculation. If you plan to invest $1 million, or $10,000, just adjust accordingly.

Why 50% REITs?

Simple answer is that I am very familiar with REITs, and I think they will do well long term, especially at these prices.

Don’t underestimate familiarity.

Sometimes in a bear market, being familiar with an asset class, and having looked the charts for years, will give you the conviction to buy in size.

For REITs I think current valuations are already very attractive for long term positions, and I may actually consider starting to buy some soon. But I still think a bigger shake up will come, and I might try to get greedy and wait for a better price.

I wrote a recent article on how I plan to deploy cash into REITs this year, all of which still remains relevant.

I don’t like taking too much risk in my REITs portfolio, so I will just stick with Mapletree and CapitaLand REITs.

Why overweight Industrial REITs?

Industrials REITs look to be the worst hit by rising rates, because comparatively speaking Retail and Office were already badly hit by COVID.

From my portfolio perspective, I’m quite overweight retail and office because I bought a lot during the COVID crisis.

So I’ll be looking to add heavily to Industrial REITs this year. MIT, MLT, Ascendas, all good stuff.

Why QQQ and stock picking?

Banks and Oil are red hot right now which makes me very nervous.

I’m up 50% – 100% on some of these positions, and I would expect to take profit by Q2/Q3 this year, especially for the banks.

By middle of the year I may start buying secular tech positions. Stuff like Cloud and Semiconductors which will continue to grow for this decade.

Like I said, this isn’t the year to get too cute with stock picking, so I’ll just put 30% into the QQQ.

The rest I would save for stock picking, to try and pick up heavily beaten down stocks. It’s my way of addressing the “itch” to do something.

Closing Thoughts

And there you have it!

How I plan to invest this year.

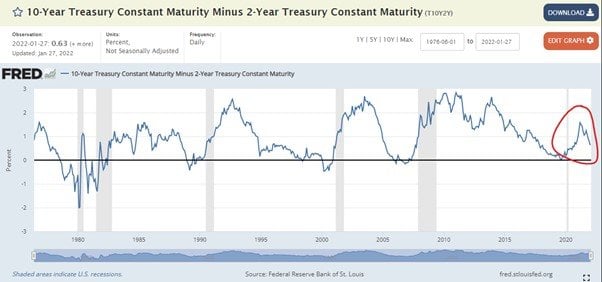

I wanted to leave you with this chart of the 10s-2s yield curve:

As you can see, the yield curve peaked in March 2021, and has reversed quite strongly since.

This indicates a much faster and shorter credit cycle this time around – which is fully consistent with what we’re seeing from the Feds.

So don’t think we’re early cycle anymore, we could be pretty advanced in this cycle, with a recession just around the corner.

For those who are serious about investing big money in 2022 – we’re running a big Chinese New Year Promotion for the FH Stocks MasterClass now.

If you’re serious about deploying cash in 2022 – really do check it out.

This is going to be a big year dominated by macro, where the slightest mistake can easily wipe out tens of thousands of your hard earned money (just like we’ve seen the past few weeks).

So don’t be penny wise pound foolish here. Learn how to invest properly.

The course fee will pay for itself many times over. Check it out here.

As always, this article is written on 29 Jan 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Since market already priced in 5 rate hike, why S&P will drop another 20 – 30%?

That’s a good question. I’m not saying the S&P will drop 20-30%, just saying that if none of the 3 conditions are met the Feds will just keep hiking until something breaks.

And if they keep hiking, at some point something will break.

In that case, will we know inflation (one of the condition) will ease from 2nd half of 2022 to early 2023? Should we cash out if any mini bull run to avoid bull trap?

I would say inflation should ease in 2H2022, but it is not wise to predict so far ahead. Many things will change over the next few months, and we will have a clearer picture soon.

When the facts change, just change your mind, and your investing strategy. Nothing is set in stone.

What is your advice for those already fully invested, should cash out now and wait until clearer to enter again?

By the way thanks for your good article.

That will have to depend on individual risk appetite, which I cannot advise on. The answer for a 30 year old drawing a stable income, and a 62 year old close to retirement are very different.

All I can do is to share how I think this year will play out, and what I plan to do based on information I have today. What to do with their own money, I leave for readers to decide for their own situations.

Hi FH, great post once again. For the sake of the real economy, I sincerely hope Biden will solve high oil, bring down short term inflation expectations, and help the long end of the yield curve to rise slightly, widening the 2s10s spread. I mean, the veggies at NTUC are getting expensive, this is kind of ridiculous.

But realistically speaking, I think we all know what is going to happen. The playbook is set in stone as mentioned in your post. We just need to control our emotions, don’t be a bogdanoff, and deploy when the time is right.

Yeah I agree inflation is becoming a real problem. For what it’s worth I do think their moves this year will help bring down inflation.

But whether inflation comes back next year or later this decade I’m not so sure, global supply chains seem to have been forever changed post-COVID.

But anyway, that’s not a question for this year. 🙂

The other thing that could cause the Fed to pause or reverse is geopolitics. Ukraine has the potential to cause serious headaches.

True, but I think it only matters to the extent that Ukraine hits one of the 3 points I mentioned.

Eg. If Ukraine causes further supply chain disruptions and exacerbates inflation, it’s hard to see the Feds changing course.

It is a big hope. Based on inverted yield curve, recession is likely late 2022/early 2023.

Should we wait til then to buy? It seems if fed keeps raising rates then a recession is inevitable. Instead of market timing, a tried and tested method is to buy and hold strong stocks that are fairly or undervalued. That is one simple way retail investors can survive any storm. By the way how u know market has priced in 5 hikes and 0.5% hike in mar?

Well, if there is a recession in late 2022, why the rush to buy now, unless the intention is to sell before that?

Sorry by market pricing in I meant the bond markets, you can check here: https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html . Eurodollar future will show the same numbers.

Anyway, this is definitely in the realm of market timing. I don’t agree that some investors may choose to just DCA. That’s perfectly fine.

Some analysts still say 4 hikes likely. Some say inflation is transitory. Who to believe ? So i dont think market has priced in the worst or price fully the risks yet. As such market could still be in for some nasty surprises. I think i will wait til s&p drops 30% before doing some averaging. If index drops, the whole market will continue to drop. Long term wise , stonks should go sideways or up depending on money supply. We have a reached a point where they have to keep printing to keep the entire system afloat. So i wouldnt be surprised stonks may melt upwards exponentially going forward in decades. Fundamentals will be further detached from valuations with maybe P/E 50 the norm due to excessive money supply. But will also be more and more volatile

Agree that longer term, the only way out will be to keep printing. So yea… longer term stonks will only go up.

Hi FH, great article, I like the split between REITs and stocks. Also, the advice to not to be cute for stock picks is a great advice for those of us with an itchy finger (peloton anyone?)

I wanted to understand the rationale for QQQ vs SPY vs Diversified World tracker. Seeing that they are diversified as well. How do you end up choosing QQQ?

That’s a good question, I think the answer really goes back to what you have in your portfolio currently.

For me I already have exposure to value stocks via oil and banks. For my ETF I wanted a long term secular play on tech. Hence I picked QQQ over SPY or IWDA.

But like I said, really depends on what you already own. If your portfolio is pure tech then yeah SPY would make sense.

What i mean is that if there are recessions then wait til it crashes then buy more

Hi FH,

For me, its very simple. I would buy SG bank stocks like OCBC.

Regards,

Gerald

https://sgwealthbuilder.com

Haha keeping it simple, I like it.

Just to highlight one potential problem if growth stocks bottom when the Feds pivot, that would also indicate the near term top for bank stocks. So you may not get an opportunity to buy banks cheap until the next cycle (when interest rates bottom out again).

Hi FH,

Good point. Thats why I am keeping a close monitor on the market and Fed movements. In any case, really like your macro analysis. Keep up the great work bro! Gong Xi Fa Cai 2022!!!

Regards,

Gerald

https://sgwealthbuilder.com

Thanks man, appreciate the kind words. Happy New Year to you too! 恭喜发财!!!

Regarding your 2022 indicative plans for 50% REITS and 50% stocks, why not invest a portion into bonds as well since this asset class have been beaten down and represent a good value play?

Why buy bonds when it’s clear the longer term picture is to print money? Bonds are ok as a short term tactical timing tool (like right now), but if the intention is to hold 5 – 10 years there are better places to park the money.

On a 2 years horizon, any insights? I am already losing alot since embarking on retirement. Bought the DBS Barbell Income (after fees, -6%) and the DBS Barbell Strategy (after fees, -7%) in just 1-2 months. Should I just cut? As these losses are not encouraging for my retirement ideal. My ex-colleague says try Fundsupermart. Are they good? Recently their seminar recommended Thai Beverage and HongKong Land. If not, I just sit on fixed deposits for now. Or put back into CPF.

Can’t advise for your situation specifically because it will need to depend on your risk appetite + asset allocation. For eg. how much cash do you have set aside, if your risk assets drawdown another 20% from here will you be able to hold etc.

My view is that rising rates with sticky inflation is a very tricky investing environment. For those looking to deploy cash long term, it would be a great opportunity. For those fully invested, some volatility is to be expected. Markets are at the end of the day, cyclical.

Where can u get a 7% return to beat inflation and reit is a no-no. Reit suck, always ask money form investore from eright issue, U end up paying them selves dividend, I hate to invest for divident. I will got for capital gain.

History have shown that tech stock will soar with inflation, wait for mkt to price that in, if u sell stock, where can u put yr money to beat inflation,, reit only pay ave 5% to 6%, u loss and when the stock price go down u loss even more.

No problem, feel free to invest in any way you deem fit.

All I’m doing is sharing how I plan to invest my own money. Not everyone may agree with my approach.

What I would add though, is that if you zoom out longer term, blue chip REITs could have a 1-2% capital gains. Add that to the 5-6% yield and that brings longer term average returns up to 7%. But this only holds true in the longer term, and not necessarily for the small cap REITs.

Hi FH. Thanks for the brilliant and clearly thought out answer to the “how much”, the “when”, and the “what to do” with regards to the present market sell off. I also like the way you stress test your thinking to see where you may be wrong; a good habit of kind that all of us would do well to adopt.

On what is priced, and where we go from here. I think with regards to the hikes, we are near peak hawkishness. So if the Feds hike, as long as it conforms to current market expectations (~5 hikes, 25bps with a chance of 50?), then my personal view is that stocks don’t have much further to fall from here.

Where I am unsure and why I’m hesitant to give the all clear buy signal is due to the following: 1) I am not sure what the terminal rate is going to be. Could be higher than what the market is expecting if we are indeed under going a persistently higher inflation regime shift. 2) there is not much detail yet on what quantitative tightening looks like. If it’s the drain is aggressive, it’s going to be really hard to fight. It’s like draining a pond of water, no matter how good your boat is, how high is it going to float when there is less water?

On what to buy, I actually favour some of the profitable FAANMG names. For some, Their underlying business fundamentals have not changed much, what is happening is a valuation re rating, so I’m pretty happy to be picking these up at a price I deem “fairer”. The same can be said about some of the higher flying small cap names (Cloudflare etc.). The secular tailwinds have not changed, so if one has skill and conviction in picking some of these, I would say time to get cute! As for myself, I feel more comfortable picking the big tech names, as there is current (not future) profit that I can cling on to to anchor my assessment of value.

On bonds, I actually am not averse to them, and I think the time to pick them up is when we are close to the peak of the hiking cycle. Still early days, but this is a spot I am watching closely. Very thankful to have bought Singapore Savings Bonds in 2018 during the previous Fed hiking cycle. They really have served me well as a portfolio anchor, cash equivalent, and source of yield.

Finally on what I am doing, I would say I am half and half. I intend to allocate half of my cash position over the first half. If the Fed gets cold feet great, if not and it pans out like FH predicts, then I will deploy the other half.

This cycle has been nothing short of truly odd. We have gone from deflation to massive inflation. Perhaps we snap back to the mean later this year like a rubber band! Who knows? Stay humble stay nimble and stay in the game! 🙂

Hi MooMoo, that is a great comment, it was very helpful for me to hear your thought analysis shared like this.

My thinking as follows:

1. I agree with you the market is pricing in 5 hikes in 2022. So if the Feds hike any less than 5 times that could actually trigger a relief rally. The wildcard is QT. Because of 5 hikes, the Feds need to bring the long end of the curve up to prevent inversion. I see QT as the best tool if they want to do so. And I think the market may be underpricing QT.

In short – there is a huge range of possibilities as to how 2022 can play out. For me I’m still comfortably invested in this market so if it does rally I have exposure, but personally I dont see myself adding in size until I see a narrative switch from the Feds.

2. I agree on FAANMG being great buys in 2022. They are generating an absolute ton of cash flow and could be great inflation hedges or some kind of antithesis to growth stocks. It’s also why I picked QQQ as the ETF as choice for when I do deploy.

3. Small cap is tricky this year. I love names like Cloudflare, Cloudstrike etc (and I hold long term positions). But I’m also very aware of the fact that narrative is a funny thing. What looks cheap at 50 times P/S in 2021, can look expensive at 10 times P/S in 2022. If shit hits the fan, it’s going to be really tough to call a bottom for small cap.

4. A cow after my own heart! I too, picked up a lot of SSBs in 2018, and they have served me very well in the years since, especially through March 2020. That said, I do see myself redeeming much of the 2018 SSBs this year, and redeploy them into REITs/stocks. 🙂

Absolutely agreed on staying humble, staying nimble, and staying in the game. This cycle has been a fast and furious one, with markets reacting equally quick. While this is how I see it today, things can change equally quick. No plan should be set in stone for this year.

Such a great comment MooMooCow.