Remember when REITs used to be popular?

Yeah… this horse is old enough to remember that too.

REITs have traded sideways for a whole year, so investors got bored with REITs in favour of stuff like Tesla and NVIDIA.

Just look at the chart of Ascendas REIT, CICT, MCT and MLT – they’ve gone nowhere for a whole year.

Are REITs undervalued now?

But then I figured this may not be a bad thing.

In a world where US growth looks quite richly valued, and China’s crackdown is still playing out, maybe the best place to invest is right in front of my nose.

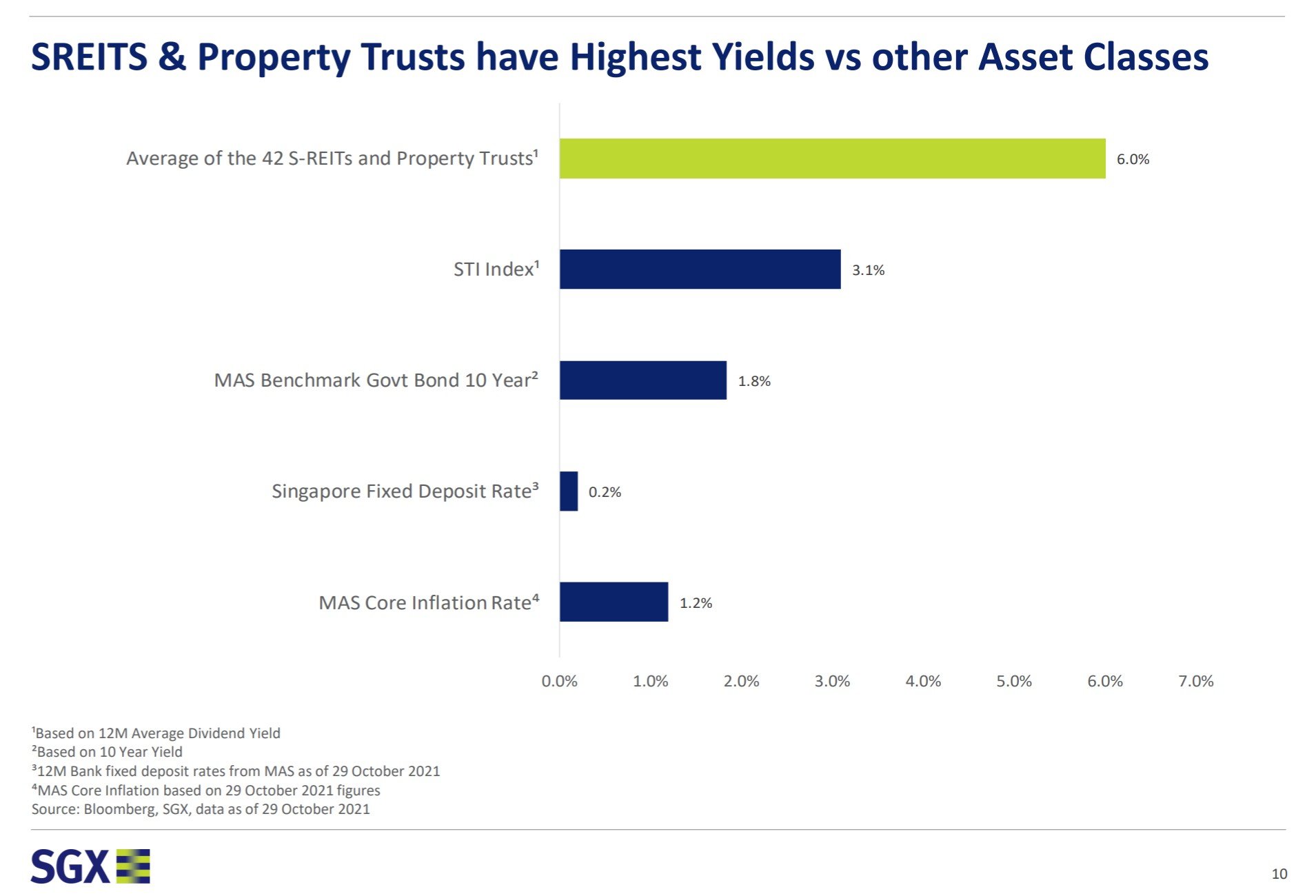

Average yield for S-REITs sits at 6.0% today.

Throw in 1 – 2 % long term capital growth from a rise in real estate prices, you could be looking at a 7% – 8% long term annualised return.

Which really isn’t too shabby.

Why are REITs underperforming?

It’s worth discussing the elephant in the room:

- Rising interest rates

- Unwind of the COVID trade – for industrial and data centres

- COVID fears – for retail and office

Rising Interest Rates

Probably the biggest one – fear of rising interest rates.

Inflation is high, so Feds are going to hike rates. When rates go up, borrowing cost for REIT goes up, REITs sell-off.

But the reality is a bit more nuanced.

Depending on how inflation plays out, REITs can provide a hedge in the form of (1) rising rents and (2) rising property prices.

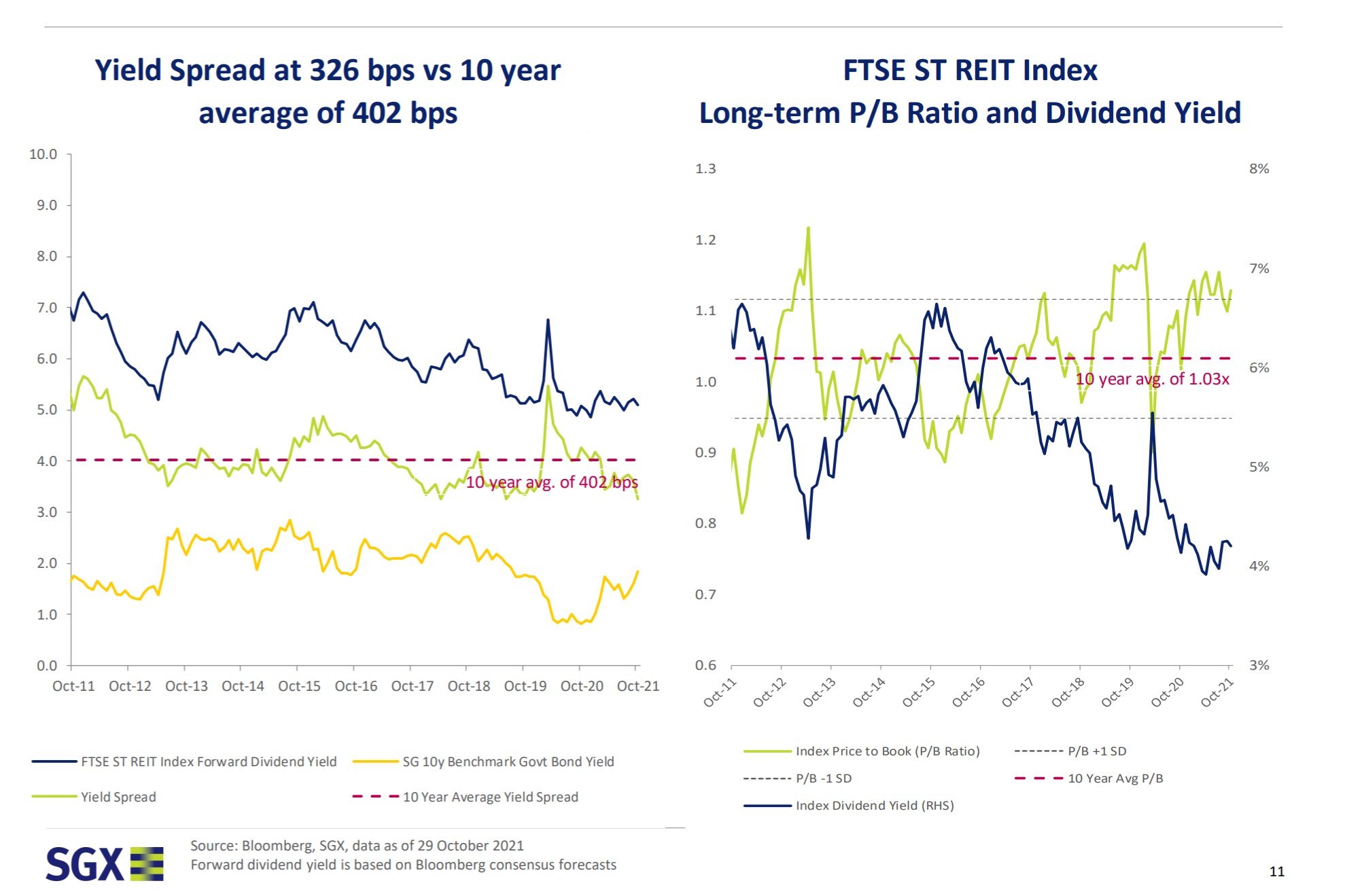

The starting price matters too.

REITs are not that richly valued compared to previous cycles, which suggests the selloff (if any) wouldn’t be that bad:

Unwind of the COVID trade – for industrial and data centres

For some REITs like Keppel DC and Mapletree Industrial / Logistics, they were bid up very strongly last year. After the whole COVID trade started to unwind, a lot of them sold off.

COVID fears – for retail and office

Whereas for retail and office, they’ve also been impacted by COVID lockdown fears, and the work from home trend.

Invest counter-cyclically?

But that’s all just short-term thinking.

As a long-term investor, I’m more than happy to invest countercyclically.

In fact, when I look at the chart below, my preference is to buy the stuff that short term investors are selling – Office, Retail and Industrial REITs.

How I will invest $100,000 in REITs in 2022 (as a Singapore Investor)

Couple of rules:

- 5 year holding period

- 5 REITs maximum (for easy administration)

- My own risk appetite

- Based on today’s prices

The risk appetite varies for each investor.

For my own REIT portfolio, I wanted something that was low to medium risk / volatility.

The reason why is that I take on a lot of risk in my growth portfolio, with lots of exposure to cloud stocks with their earnings very far in the future. That portion of the portfolio can swing 5% – 10% a day. You can view my full portfolio on Patreon if you’re keen.

So for my REITs I didn’t need the same kind of excitement. The more boring it is, the better – as long as it pays a good yield.

There’s no right or wrong here. If you want more excitement in your REITs portfolio, feel free to add in more high yielding small cap REITs.

How I will invest $100,000 in REITs in 2022 (as a Singapore Investor)

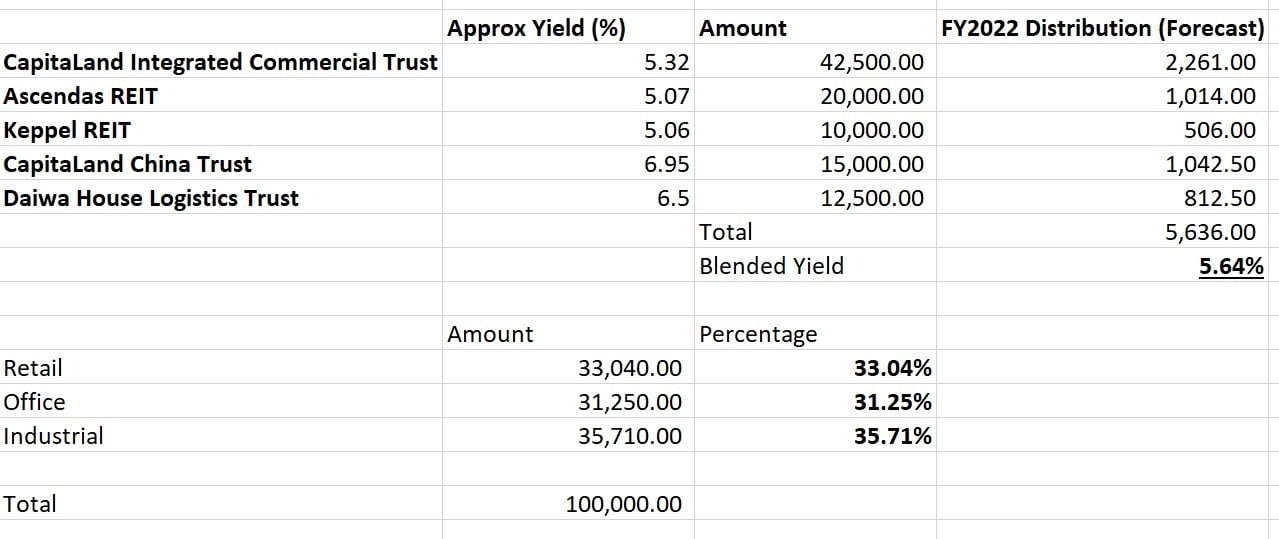

Here’s the allocation I would go for to invest $100,000 in REITs:

- Core Portfolio ($72,500)

- CapitaLand Integrated Commercial Trust – $42,500

- Ascendas REIT – $20,000

- Keppel REIT – $10,000

- To Juice Yield ($27,500)

- CapitaLand China Trust – $15,000

- Daiwa House Logistics Trust – $12,500

The thinking is to build the bedrock of the portfolio using very stable Singapore commercial real estate.

Then layer on some higher yielding foreign real estate to juice the yield slightly, at the expense of more risk.

Forecast yield for the portfolio is 5.6%.

Split between the asset classes is broadly:

- 33% Retail

- 31% Office

- 35% Industrial/logistics

I’ll share more on the thought process below.

CapitaLand Integrated Commercial Trust

Price to Book: 0.99x

Trailing 12 month yield: 5.32%

CapitaLand Mall Trust and CapitaLand Commercial Trust used to be 2 of my favourite REITs.

Then they merged to form CapitaLand Integrated Commercial Trust (CICT), which I suppose makes it my doubly favourite REIT.

If you want a buy and forget REIT to get pure exposure to Retail + Office assets in Singapore, there’s really only 2 choices: (1) CICT, or (2) Mapletree Commercial Trust (MCT).

I love MCT, and in fact it’s one of the largest positions in my portfolio.

Loyal readers of Financial Horse know that I’ve been gushing about Mapletree as a Sponsor since the inception of this blog.

The main problem with Mapletree for me at the moment, is that perhaps they’ve been too successful.

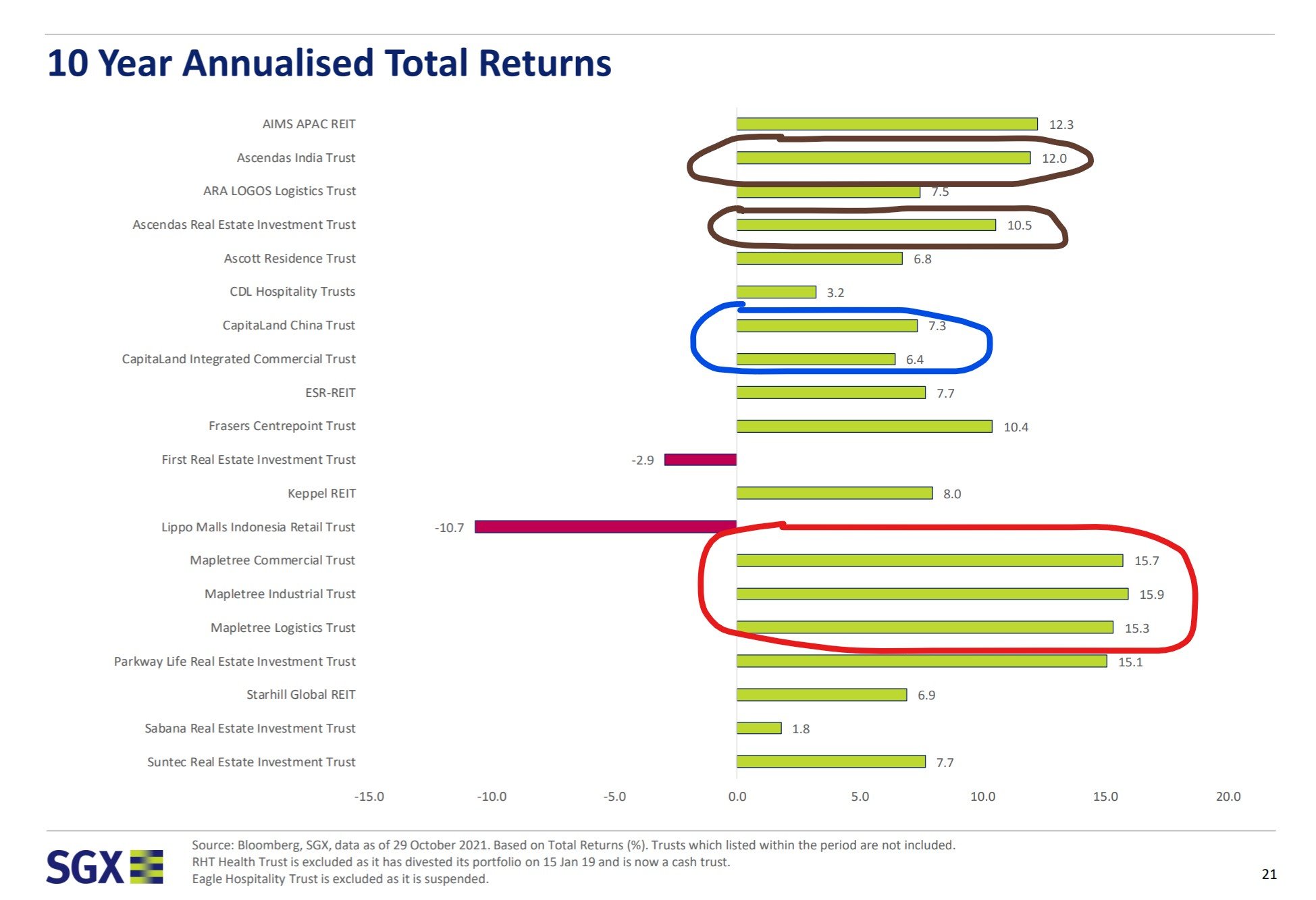

10 year annualised returns for their 3 REITs are a mind blowing 15%, significantly higher than that for Ascendas (10-12%) or CapitaLand (6-7%).

The problem is that this is real estate, not a tech company.

There’s only so much you can do to improve real estate.

I’m happy to pay 10 times sales for a fast-growing SaaS stock. But no way I am paying 1.8x book for brick-and-mortar real estate.

So while I like Mapletree REITs, my concern is that the valuations they are trading at today, will translate into weaker returns going forward.

MCT trades at a 4.74% yield and 1.19x book value today.

Compared to CICT at 0.99x book value and 5.3% yield, I just felt that CICT was the better choice at these prices.

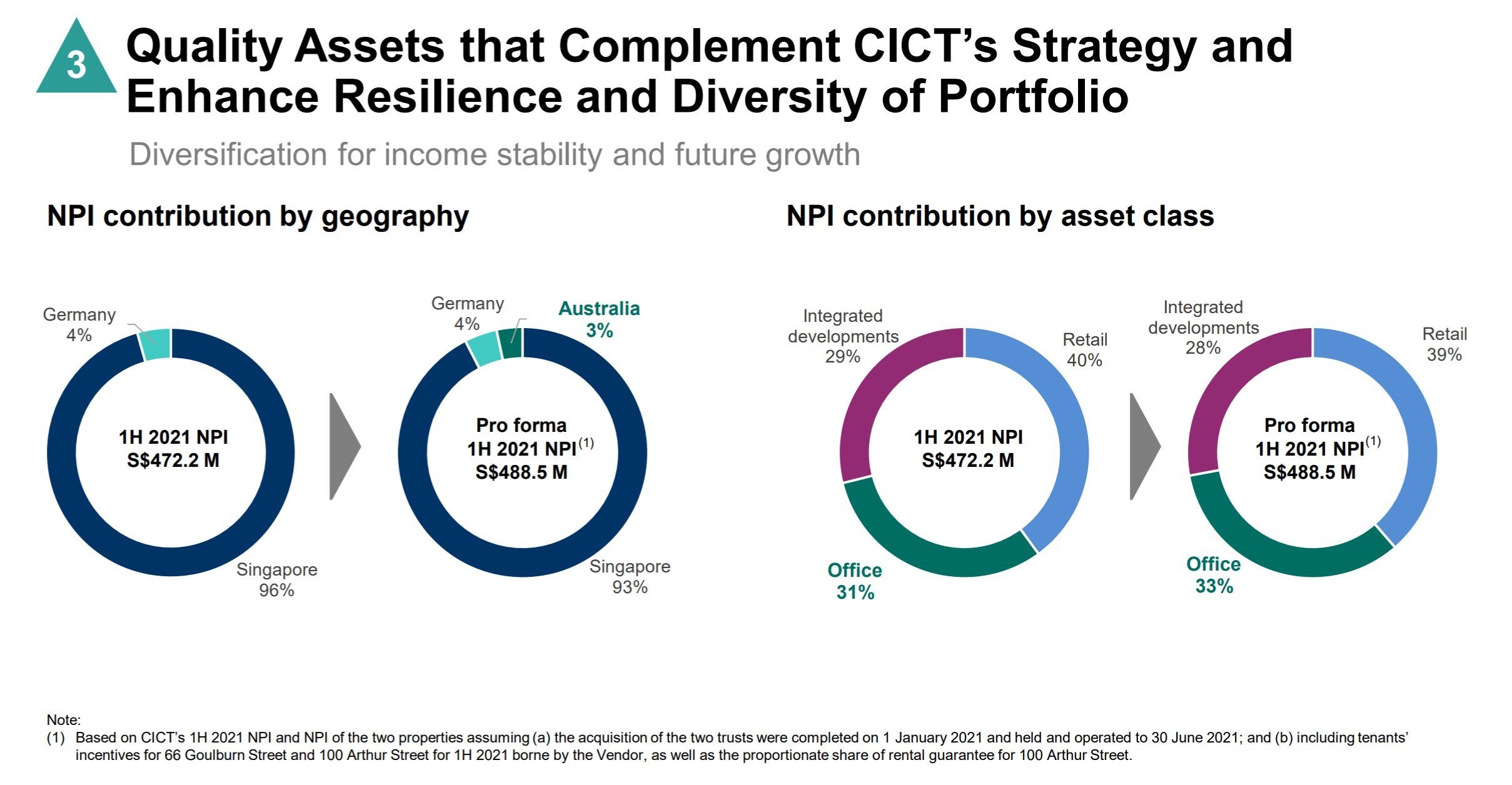

Despite the diversification into Germany and Australia, 93% of CICT’s income still comes from Singapore, and fairly split between retail and office.

Singapore real estate is very stable as an asset class, so I wanted this to form the bedrock of my REIT portfolio.

42.5% (or $42,500) goes into CICT.

Ascendas REIT – $20,000

Price to Book: 1.27x

Trailing 12 month yield: 5.07%

With Singapore Retail and Office exposure out of the way, I wanted exposure to industrial/logistics.

Again, the choice came down to CapitaLand vs Mapletree.

Just like with CICT, I decided to go with Ascendas REIT for this pick.

Unlike Mapletree Industrial Trust which has 50% exposure to data centre in the US, Ascendas REIT is more of a pure play Singapore industrial REIT.

Which was what I wanted.

If you don’t like Ascendas you can swap it out with Mapletree Industrial Trust at 1.42x book value and 4.97% yield.

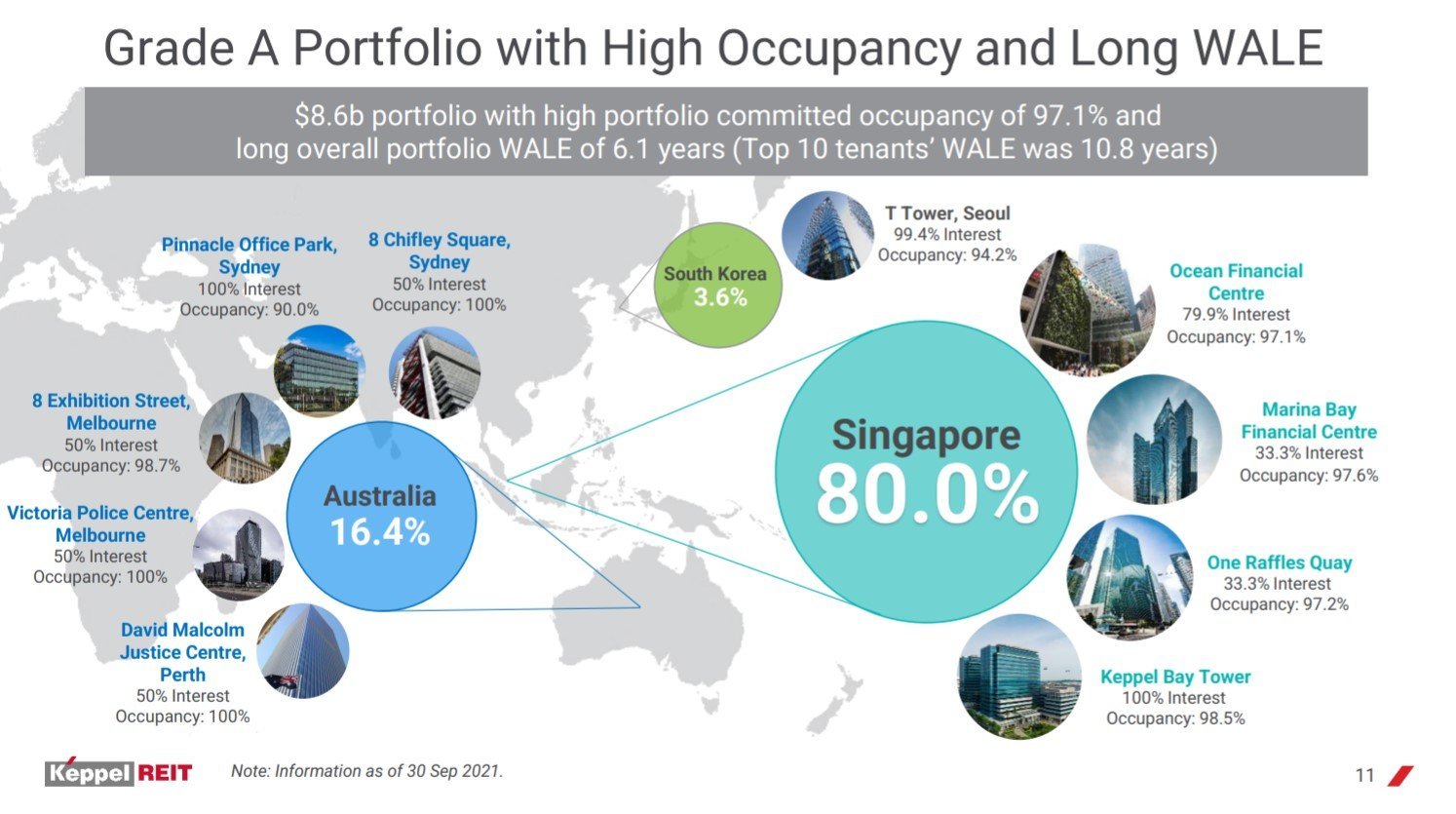

Keppel REIT – $10,000

Price to Book: 0.826x

Trailing Twelve Month yield: 5.06% yield

With CICT and Ascendas REIT, the portfolio was quite tilted towards retail and industrial properties.

So I wanted to add on more office exposure.

I know many of you are not a fan of office because of the work from home trend.

I’m a bit more sanguine.

I don’t think we’ll ever return to 5 days in an office style working. But I think the death of the office is overrated too.

At current valuations, I think Grade A office space in Singapore is attractive enough that I want to add at these prices.

I bought some Keppel REIT recently when it sold off after the Keppel-SPH saga (Keppel offered to buy SPH using Keppel REIT units).

Price has recovered a fair bit since, but I still think it’s a decent price given the kind of Grade a Office exposure they hold – Marina Bay Financial Centre, One Raffles Quay, Ocean Financial Centre etc.

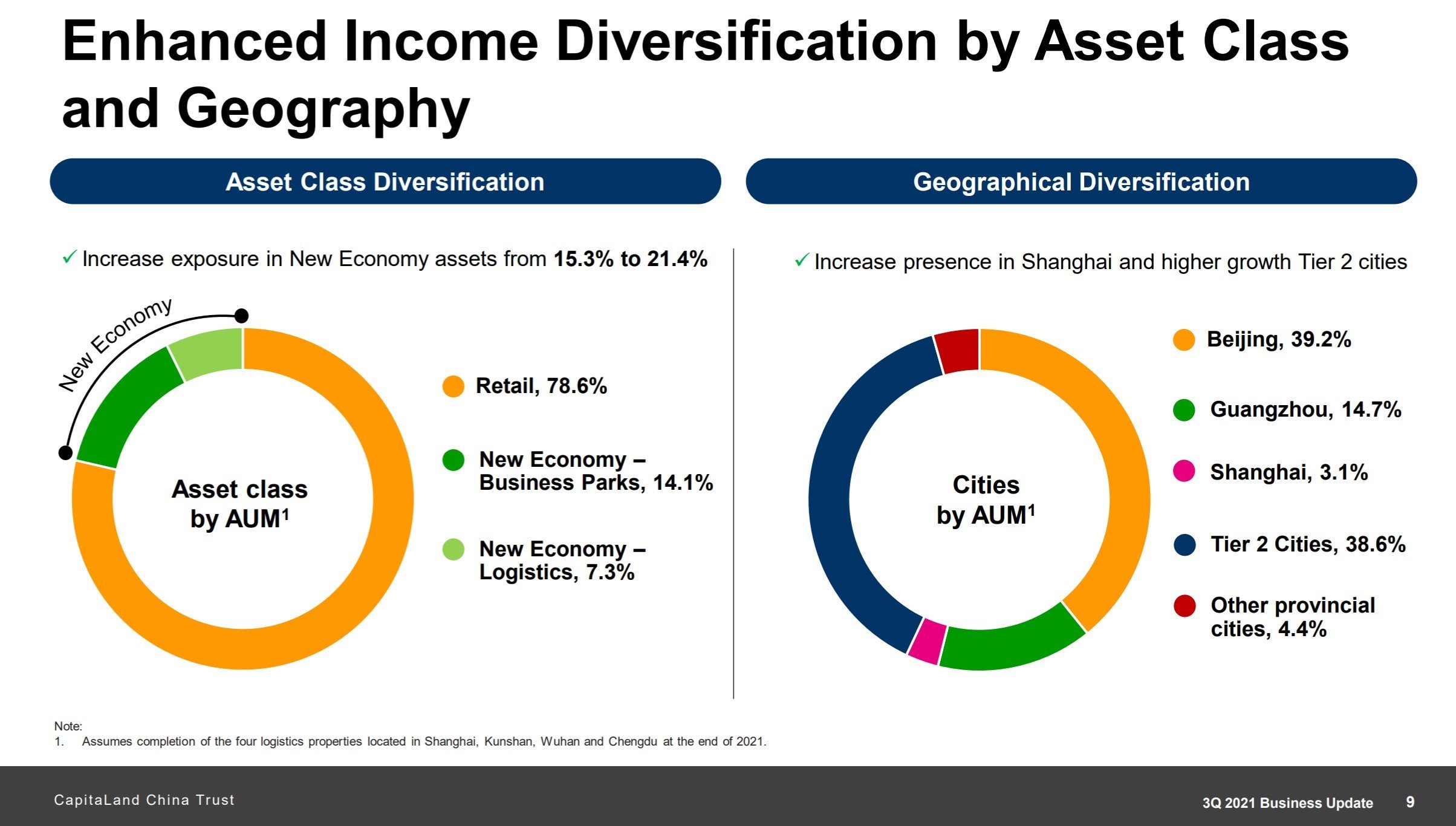

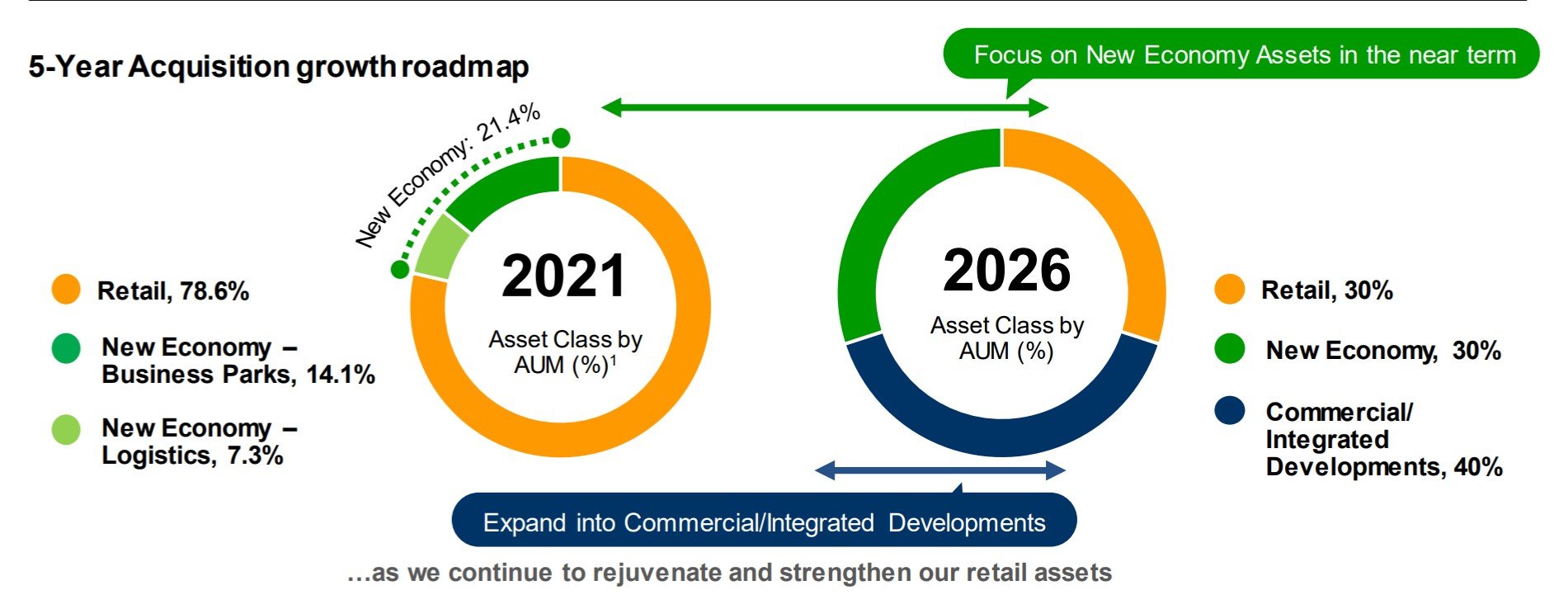

CapitaLand China Trust – $15,000

Price to Book: 0.71x

Trailing 12 month yield: 6.95%

So that’s the core portfolio, which is 72.5% of the portfolio.

The problem if you just use Singapore real estate is that you’ll end up with a low 5% yielding portfolio, which was a little too low for my liking.

So I wanted to juice the yield up closer to 6%, and take some measured risks with the REIT portfolio.

I talked about CapitaLand China Trust last week, and how it’s one of my preferred ways to play China real estate.

The main highlight for me is the presence of CapitaLand as a sponsor, which brings with it access to offshore financing.

The portfolio is predominantly retail for now, but the roadmap going forward is to significantly increase exposure to business parks, logistics, and integrated developments.

The true gem for me would be if CapitaLand divests their Raffles City Integrated Developments into CapitaLand China Trust.

That would be a truly transformative acquisition for this REIT.

Throw us retail investors a bone, maybe?

This is pure China real estate, so timing is important.

Current prices are decent, but they could get even better as Evergrande plays out like a slow-mo train wreck.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Daiwa House Logistics Trust – $12,500

Price to Book: 0.93x

FY2022 forecast yield: 6.5%

Compared to Digital Core REIT which soared 30% post IPO, Daiwa House Logistics Trust has had a much more muted IPO (still trading close to IPO price).

That presents opportunity.

It might just be this horse’s wishful thinking, but I see Daiwa House Logistics Trust as a potential poor man’s version of Mapletree Logistics Trust.

You know how Mapletree Logistics Trust started off with a base of Singapore logistics assets, then layers on exposure to South East Asia?

Well, Daiwa House Logistics Trust starts off with a core base of Japanese logistics assets, with plans to layer in South East Asia assets from the sponsor going forward.

Daiwa is a solid sponsor in Japan, being the sponsor of the Daiwa House REIT in Japan.

The REIT will need some time to prove its track record to Singapore investors though. So the short term trading could be choppy.

But compared to Mapletree Logistics Trust at 1.325x book value and 4.23% yield, I’m willing to take the chance with Daiwa House Logistics Trust.

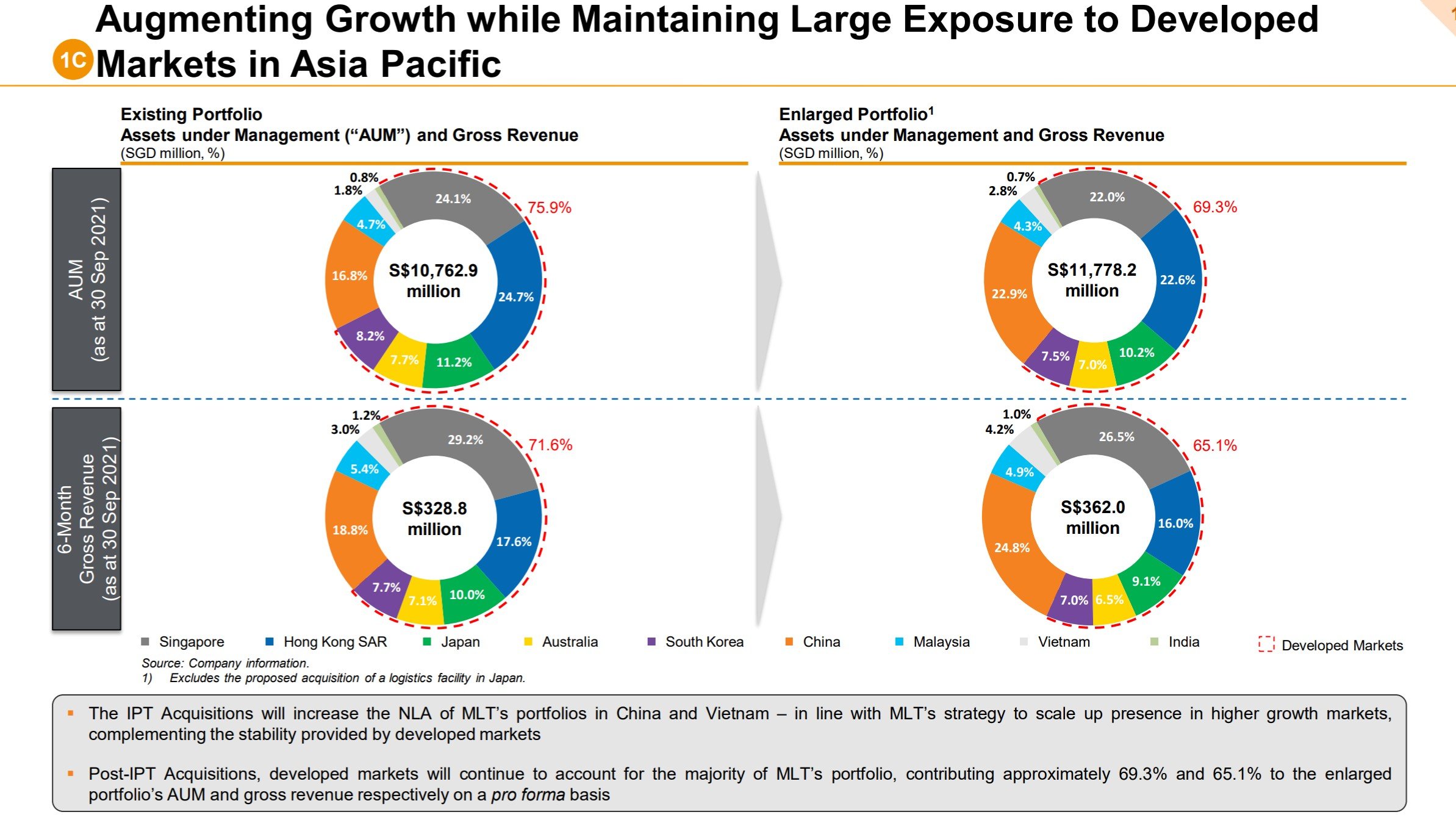

I really wasn’t a huge fan of the recent acquisition by MLT where they bought $1 billion worth of China real estate from the sponsor.

I get that this is a long-term move, but to do it right smack when Evergrande is playing out wasn’t ideal for me.

Why No Hospitality or Healthcare REITs?

This REITs portfolio has zero exposure to hospitality and healthcare, and that’s by design.

At these prices, I’m just not a fan of healthcare or hospitality.

If you really wanted hospitality exposure Ascott REIT, Far East Hospitality Trust and CDL Hospitality Trust are worth checking out.

But I don’t find they compelling at these prices, and I prefer to play the travel recovery via travel operators like Airbnb/Booking.com, or even via oil.

For healthcare Parkway Life REIT is the default choice, but at 2.7% yield it’s looking just like a bond to me right now. You’ll need to tack on a fair bit of leverage for it to make sense, which opens the possibility of capital losses into a rising rate environment in 2022.

Closing Thoughts: How I will invest $100,000 in REITs in 2022 as a Singapore based investor

And there you have it!

How I will invest $100,000 in REITs in 2022, as a Singapore based investor.

For obvious reasons the $100,000 is an approximate number, and I reserve the right to scale it up or down depending on how things play out. If prices change materially, I will also swap out REITs on this list with others.

I’ve also taken into account my existing exposure and risk appetite when constructing this portfolio, and you will need to do the same with yours.

For my latest Stock Watchlist, including a detailed breakdown of my portfolio with updates on when I buy/sell, do check out Patreon.

But the point remains that with US stocks at record valuations, China’s crackdown playing out in earnest, and Singapore bank stocks at all time highs, S-REITs are the one bright spot in this market where valuations look more reasonable.

Would love to hear what you think though.

What would you do differently if you were investing $100,000 into REITs in 2022?

As always, this article is written on 10 Dec 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Huge Christmas Promo for Investing MasterClasses!

Sign up now and get massive discounts and limited Freebies!

Find out more here.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

How about US office reits like Manulife US reit, Prime reit? They are trading at corrected valuations, highly attractive yields with strong sponsor and a appreciating to US dollar to SGD. Love to hear your thoughts!

Real estate is a very local business, and I don’t know enough about US real estate to comment on this.

Hence I usually stay away from US REITs, Digital Core REIT was probably one of the rare exceptions.

Look forward to your next piece on US office property reits then .. the thesis for office recovery is largely similar to that of Singapore and these office pure-play reits come with strong sponsor such as the likes of Manulife and yet remain under the radar on SGX trading at attractive yields and p/bv levels. Probably good time to look into it before potential reopening thesis play out in 2022

Real estate is a local business, and unfortunately I don’t know enough about the US real estate market to comment in depth. For now, I prefer to stick to Asia based real estate. 🙂

Hi FH,

Notice that you do not favor Suntec reit, can I understand why? Thank you

I think CICT/MCT has a stronger sponsor (vs ARA) and better asset base. So Suntec REIT should trade at a higher yield, which is does.

Ultimately a personal choice, but for me I wanted a low risk REIT to allow me to take more risk with other portions of my portfolio. Hence I went with CapitaLand/Mapletree sponsored REITs.

Why you don’t consider any of the Mapletree REITs?

MIT is probably interchangeable with Ascendas if I wanted more data centre exposure. MCT I felt valuations are not compelling right now, especially when compared with CICT – and in any case I already own a lot of MCT.

MLT if it corrects more then sure. 🙂

Hi FH,

Personally at the moment I’ll stay out of China for the time being… and so I’ll swap out your Capitaland China for Ascendas India.

Interesting, I don’t know enough about Indian real estate to comment. Able to share the bull thesis?

I would have preferred Mapletree Industrial Trust in place of Ascendas REIT or Keppel DC REIT. As MIT has both industrial and DC mix. And price and yield is better too. Just my own 2 cents worth of thought.

Actually I was just thinking the same too.

Due to artificial constraints for this article (the 5 REITs rule) I has to choose between either MIT or Ascendas. In the real world I don’t have this constraint, so I think what I will likely do is to buy both.

But yeah, I agree with you on the thinking.

Hi FH,

Given that Fed is likely to increase interest rates next year, will S-Reit unit prices crashed like what it did in 2015? After all, many of them are highly leveraged?

Regards,

Gerald

https://sgwealthbuilder.com

Definitely possible, but starting valuations for REITs this time around aren’t that aggressive. I would be far more concerned with other risk assets like growth/crypto.

In any case, if REITs sell-off that would be a great buying opportunity. I loaded up heavily in previous tightening cycles too.

Hi FH,

Thanks. I have the same strategy. I am holding MLT shares at the moment. Will accumulate more next year when Fed increases interest rates and the unit prices drop.

Regards,

Gerald

https://sgwealthbuilder.com

Curious to hear your views – why MLT in particular, and not the rest?

I like the pipeline of PRC projects that MIPL is transferring to MLT. Over the long run, I am confident that e-commerce will continue to grow and logistic S-REITs like MLT will benefit. I do not think China technology crackdown will damper the e-commerce growth.

Regards,

Gerald

https://sgwealthbuilder.com

Why not CapitaLand China trust then? If you’re bullish on China.

what if one really want a 100% buy and forget, forgoing that 1%+ for REIT ETF like clr instead to avoid a meltdown like that of firstreit?

Yeah I would say REIT ETF or something like Syfe REIT. REIT ETFs have quite poor liquidity though so if that’s a concern then the latter may be a better choice.

Dear all

Thanks FH for the article

While I agree with your overall hypothesis regarding REITS and the rationale supporting investment at this time , there are a few points I wished to highlight

1- Agree that the MCT MLT MIT trio is fully valued. Value will emerge under 2$, 1.75$ and 2.60$ respectively. The market gives a higher premium to this trio and therefore they trade at current levels. These target prices will be my add on buying price and that might also offer a fair margin of safety against anticipated interest rate hikes

2- CICT has just diluted equity with a big private placement and this makes it unattractive above 2$. The BV is 2$ and the current yield is not attractive enough to warrant a big commitment in my opinion. Value emerges under 1.95

3- You have quoted that Daiwa is trading below BV. As far as I recollect it’s BV is 76 cents . I sat out the IPO but agree that it is a buy. I will buy only under 80 cents IPO price as I feel they will

come out with expansion plans

MOST IMPORTANTLY- Many of the SG REITS are using the current Low interest rate environment and aggressively buying assets

Most of these are funded through private placements thereby destroying value for existing shareholders who have no say !!

The only way the small investors can ‘catch up’ would be by buying later after the unit prices fall post-placement

This is not ideal and unless you are flush with funds not always feasible

The yields are offset by this equity dilution

Examples from the current month are MLT CICT Manulife US Office REIT

Regards

Garudadri

Hi Gaudari,

Thanks for sharing your views. I add some of my comments below.

2. Agree on CICT and the placement. I actually added to my position after the private placement. While I agree that below 1.95 would be great if we get a pullback, I think low 2.0 is already good enough for me to add.

3. It depends on how you calculate the NAV. The sponsor injected the assets into the REIT at a discount to NAV, so if you factor that discount in the book value the number I am using will be the correct figure. If you assume the post-discount price to be the NAV then your number will be correct.

4. I agree on the private placement point, lots of big private placements recently like you said that are issued at a discount. But as retail investors what is the option to us? If we don’t like it, do we just walk away and invest in another asset class? It seems to be part and parcel of investing in REITs this day.

I agree it’s a real problem, but I havent come up with a good solution yet. Let me know if you do!

The only solution is to be patient and at least partially ‘maintain your stake’ by buying post placement at some stage, as close to the placement price as feasible

I will be doing that for CICT MUST and again for MLT

For MLT, I applied for just a few excess rather than more as the private and preferential offer price are quite close to current share price . MLT has been aggressive of late and equity dilution will Ensure I can buy more under 1.80!

Regards

Garudadri

Thanks! Appreciate the sharing. 🙂

Dear FH

CICT on an acquisition spree! Another half a billion in North Sydney

Gearing going up and with threat of rising rates, my 1.95 is almost upon us and probably 1.90 in early 2022. The CEO of the Management’s declared aim is to go up to 20% non SG assets! Shudder to think what else they will buy next

Garudadri

To be fair they’re not doing another placement for this, but using the proceeds from the previous PP. So the impact on the unit price wouldn’t be as bad.

Can totally see why they want to go up to 20% non-SG though. SG valuations are too high, not possible to find yield accretive deals if they stick purely to Singapore anymore. And with these REITs it’s always about growing AUM to grow fees.