Unless you’ve been living under a rock the past few months, you’ve probably already heard of the whole “buy T-Bills with CPF-OA” trick.

CPF-OA pays 2.5% after the first $20,000.

Latest 6 month T-Bills pay 3.83%.

So buying the T-Bills with CPF-OA is a simple way of increasing the interest earned on your CPF-OA.

As of today, all 3 of the local banks allow you to buy T-Bills using CPF-OA moneys online.

There’s no need to queue for an hour at the bank anymore.

So if you have some cash lying around in your CPF-OA, do consider buying some T-Bills for a higher interest.

In this article, I wanted to discuss:

- What are the risks of buying T-Bills with CPF-OA?

- Is it worth it to buy T-Bills with CPF-OA?

- Estimated Yield of the next 6 months T-Bills

What are the risks of buying T-Bills with CPF-OA?

T-Bills are issued by the Singapore government, so risk of default is negligible.

The main risks though, are:

- CPF-OA interest rates going up

- Losing CPF-OA interest

- Won’t be able to use the CPF-OA money

CPF-OA interest rates going up

Think of it this way.

If you buy 3.8% yielding T-Bills.

And CPF-OA rates go up to 4.0%.

You would have been better off just leaving the money in CPF-OA instead.

So the question then is (1) will CPF-OA interest rates go up, and (2) if yes – when will they go up?

This is a bit of a political question and every man and his dog is going to have an answer, so I’m not going to wade into this debate.

If you think CPF-OA interest rates will go up, and go up soon, then yes leave your cash in CPF-OA.

If you don’t think so, then you can consider buying T-Bills.

Losing CPF-OA interest

Do note that the way CPF-OA interest works, is that if you withdraw CPF-OA money for even 1 day in the month, you are going to lose CPF-OA interest for the whole month.

Because of this you generally want to avoid T-Bills with an auction date towards the end of the month, and go with T-Bills with an auction date at the start of the month.

This helps you minimise the amount of CPF-OA interest lost.

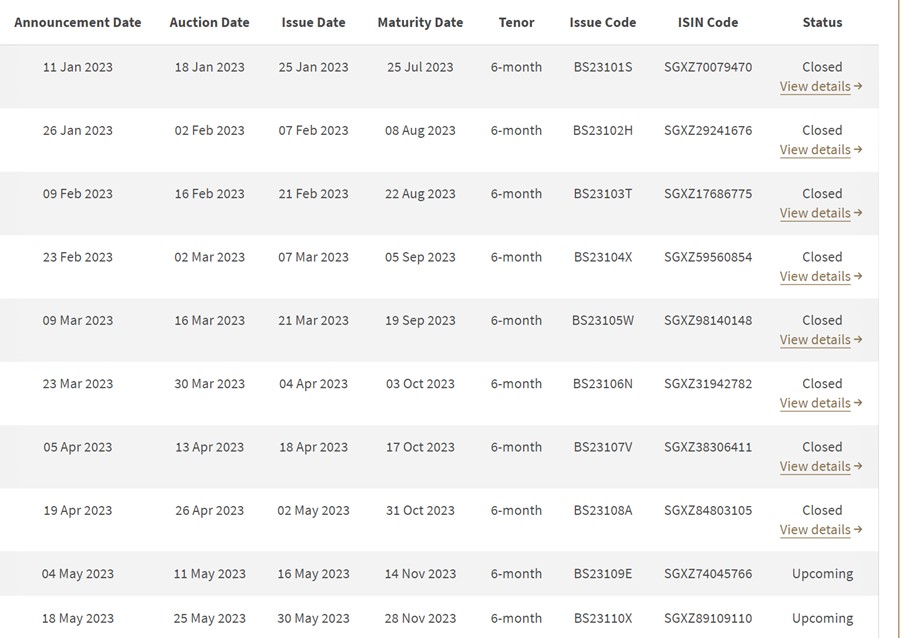

Next T-Bills Auction on 11 May

This was a big problem with the previous round of T-Bills, because the auction date was 26 April, while the Issue date was 2 May 2023.

So CPF-OA buyers would have lost the full month of April CPF-OA interest.

No such issue with the latest T-Bills auction though.

Because auction date is 11 May 2023.

Won’t be able to use the CPF-OA money

The final risk of course, is that if you buy T-Bills with CPF-OA money, you won’t be able to use the CPF-OA moneys.

Big point to note if you’re paying your mortgage using CPF-OA funds.

Do also note that you’ll need to leave at least $20,000 in CPF-OA, and you can only invest the rest.

Is it worth it to buy T-Bills with CPF-OA? What is the Estimated Yield of the next 6 months T-Bills?

Is it worth it to buy T-Bills with CPF-OA?

To answer this question we’ll need to have some rough estimate of where the T-Bills interest rates will close for the next auction.

Let’s try to make an educated guess based off market pricing.

What is the Estimated Yield of the next 6 months T-Bills?

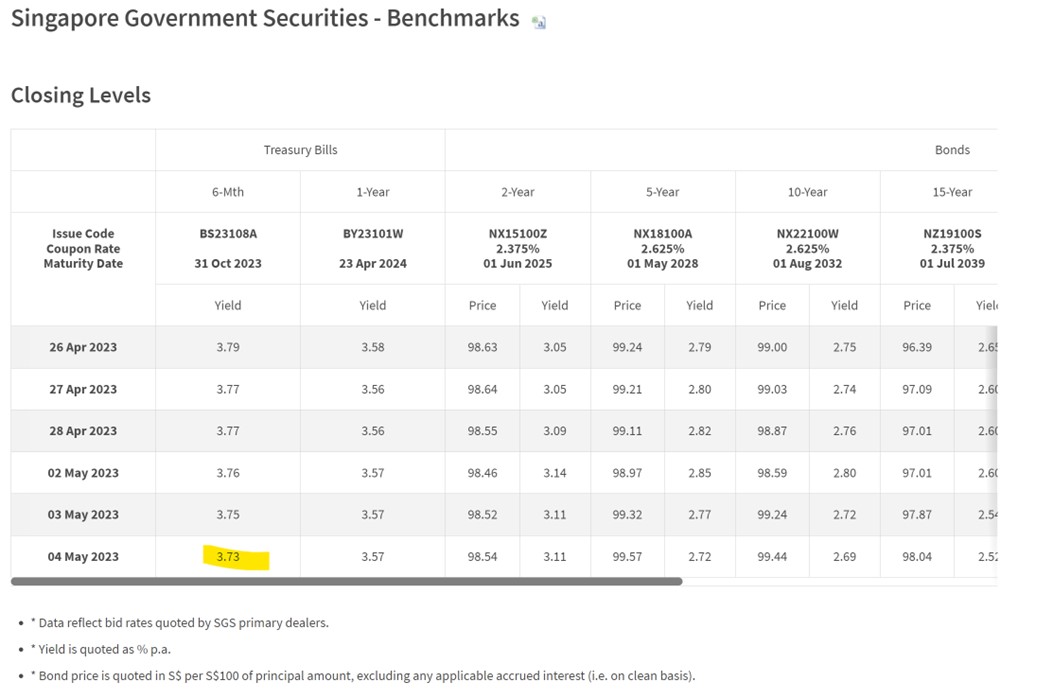

SGS Yields – 3.75%

The latest 6 month T-Bills are trading at 3.75% on the open market.

12 week MAS Bills

While the latest 12 week MAS Bills trade at 3.92%.

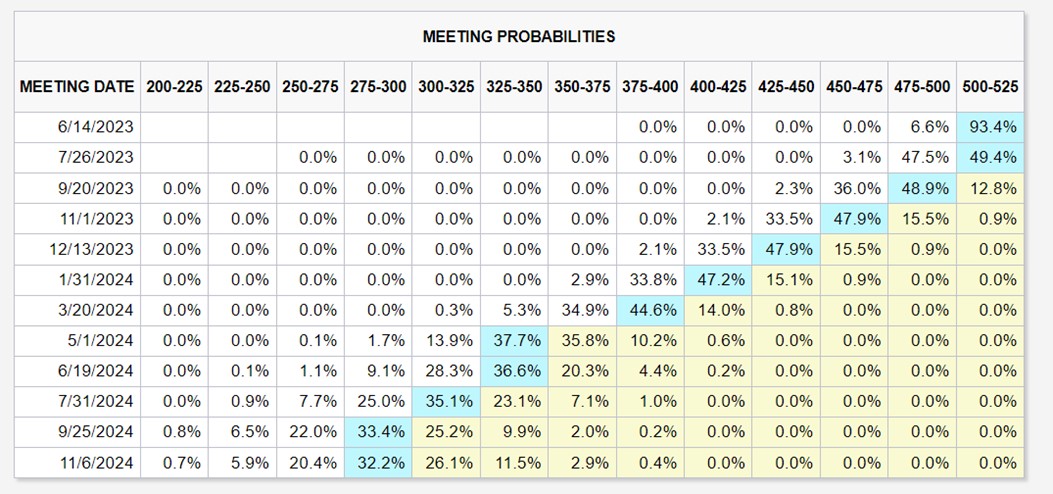

Jerome Powell vs the Market – who is going to be right on interest rates?

The Federal Reserve hiked 0.25% this week.

They also hinted strongly at a pause, but left the door open to another rate hike.

Despite this though, the market just refuses to believe him at this point.

Market is pricing in no more rate hikes this year, with rate cuts to begin as soon as July’s FOMC:

As shared previously, I think market pricing on rate cuts is way too aggressive.

Unfortunately, none of this matters for T-Bills, because it will price in the current interest rate curve.

Which is pricing in rate cuts very soon.

In plain English – this is not good for T-Bills yields.

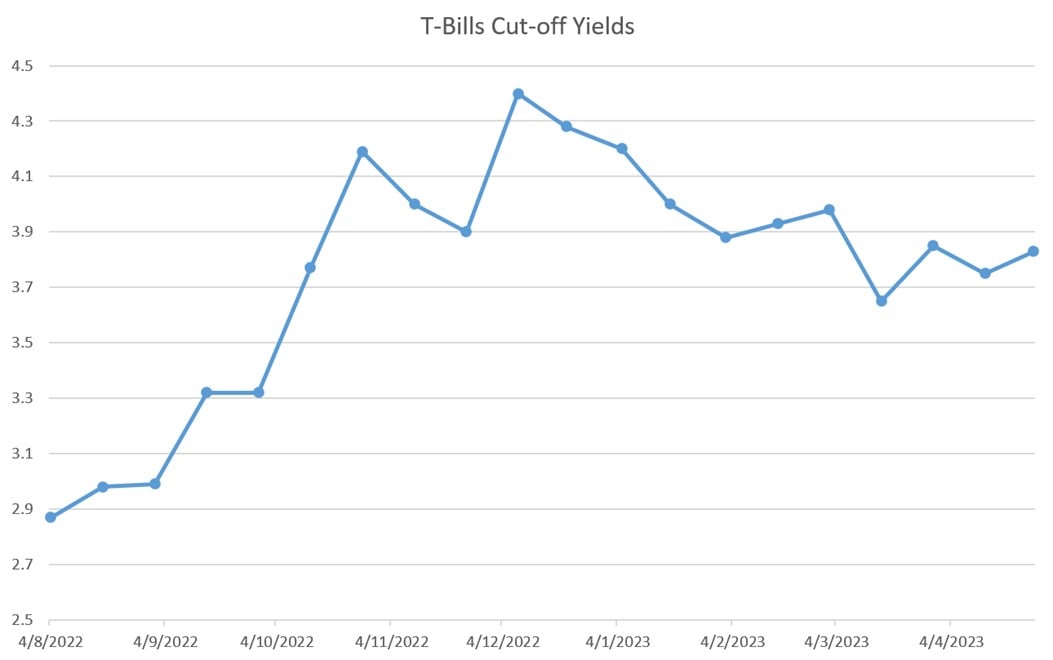

Latest 6 month T-Bills auction went up to 3.83% yield

Interestingly the most recent 6 month T-Bills auction went up to 3.83% yield:

Demand for the previous auction was low due to CPF-OA buyers

However, do note that the previous round of T-Bills was particularly bad for CPF-OA buyers.

The auction date was 26 April, which means that CPF-OA funds would have been deducted one day after auction on 27 April.

So CPF-OA buyers would have lost CPF-OA interest for the whole month of April, while T-Bills interest only kicks in in May.

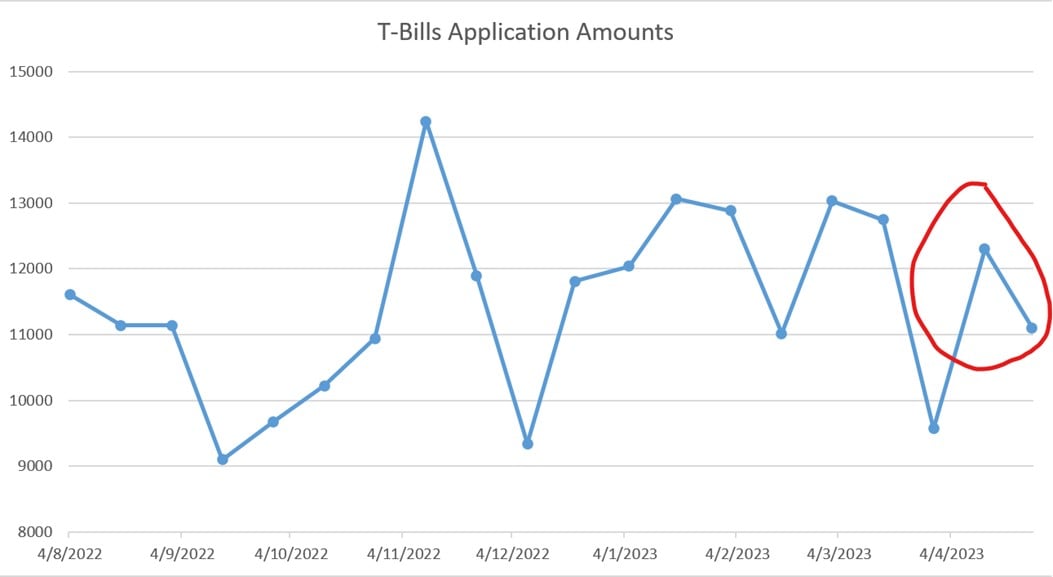

Because of that you do see a sharp drop in application amounts for the previous auction.

That may lead to a bit of “pent-up” demand for this round of T-Bills, so you may see demand bounce back quite strongly.

Especially when you realise that most of the banks have revised their May 2023 Fixed Deposit rates down to the 3.5-ish range, which means that T-Bills becomes more attractive relative to Fixed Deposit.

Long story short – demand may rebound strongly for this round of T-Bills, which does cast a bit of uncertainty over the final T-Bills cut-off yields.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Estimated Yield of the next 6-month T-Bills – 3.70 – 3.80%?

Put that all together, and my estimated yield for the next 6-month T-Bills auction will be 3.70% – 3.80%.

As always, I encourage readers to submit a competitive bid to protect yourself against any freak results.

For example if you’re buying with CPF-OA and don’t mind buying as long as T-Bills close above 3.60%, then you can submit a competitive bid for 3.60%.

Or if you’re a cash buyer and only want to buy above 3.75%, then you can bid accordingly.

Do consider opportunity cost when bidding though, because if you don’t get any allotment you are effectively losing the interest on the cash (until you redeploy it).

Is it worth it to buy T-Bills with CPF-OA?

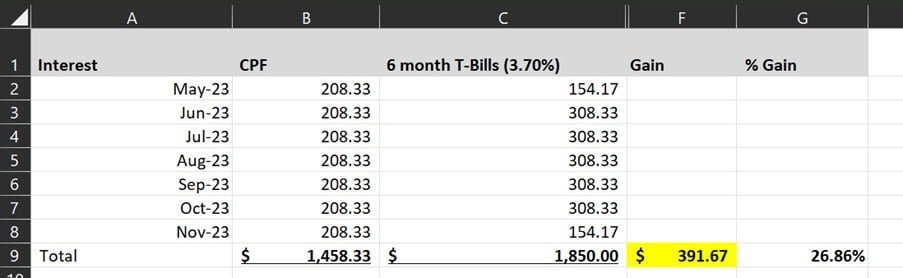

Let’s assume that:

- 6 months T-Bills close at 3.70% (the lower end of the range)

- You have $100,000 in CPF-OA to invest in T-Bills

In that case you are making an extra $391.67 over 6 months by doing this “trick”.

Or a 26.8% increase in interest earned.

Is it worth it?

I mean you tell me.

Personal view though – now that you can do it completely online, it really shouldn’t take you more than 5 minutes tops to get it done (okay, maybe 10 minutes if you are not so familiar with the process).

Close to $400 for 5 – 10 minutes worth of work is probably worth is in my view.

But it really depends on how much CPF-OA you have available, and of course do note the risks that I flagged above (eg. if CPF-OA rates go up, if you need to use CPF-OA etc).

I leave it up to each investor to decide for themselves.

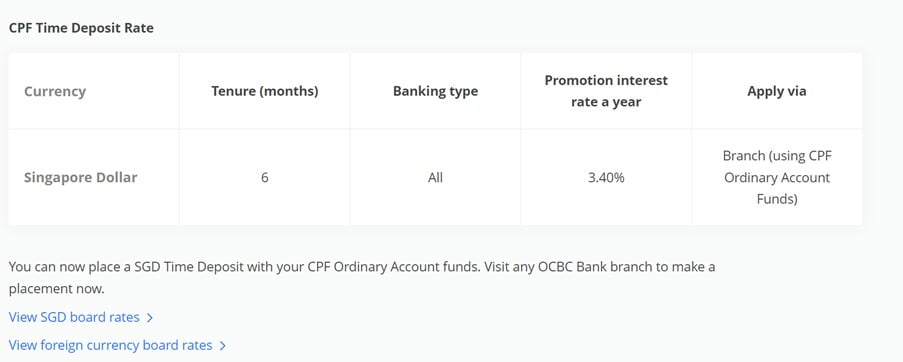

Is there any alternative to buying T-Bills with CPF-OA

A couple of you have asked if there is any alternative to buying T-Bills with CPF-OA.

For the record, the only alternative I know of is 3.40% for 6 months with OCBC.

Not very attractive, so for now T-Bills are your best bet.

This article is written on 5 May 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!