Unless you’ve been living under a rock the past few month, you probably heard about the buy T-Bills with CPF-OA trick.

CPF-OA pays 2.5%, so if you buy T-Bills yielding 3.88%, you’re basically earning the extra return risk free.

The main drawback before this was that you had to go down to the bank physically to make the application.

But DBS has just rolled out the option to buy T-Bills online using CPF-OA.

Which removes a lot of the friction behind the process, and makes it a bit of a no brainer to earn the extra interest now.

Should you buy T-Bills (or Fixed Deposit) with CPF-OA?

Previously the 2 biggest drawbacks of buying T-Bills with CPF-OA were that:

- Will CPF-OA rates will be increased going forward?

- Cannot be bought online – had to go down to the bank

Sidenote that you will lose about 1 month’s CPF-OA interest with this trick, but usually as long as the T-Bills interest is above 3% it will make up for the lost CPF-OA interest.

Will CPF-OA rates will be increased going forward?

Straits Times did a very interesting article on buying T-Bills with CPF-OA recently.

Apparently, Manpower Minister Tan See Leng was asked in parliament this week whether CPF-OA interest rates will be increased moving forward.

This was his response:

“On Tuesday, Manpower Minister Tan See Leng responded to a parliamentary question on whether there are plans to incentivise CPF members with high OA savings to tap alternative options for higher interest earnings.

He said they could put their CPF funds into short-term Singapore Government Securities (SGS) products like T-bills.

He added that OCBC and UOB customers will be able to use their CPF savings to apply for T-bills online by the first quarter of 2023, after DBS Bank first allowed customers to do so in late January.

OCBC confirmed to The Straits Times on Tuesday evening that its customers will be able to use their mobile apps and Internet banking accounts to invest their OA and Special Account (SA) funds in T-bills from March.”

Okay I’m not the best horse at interpreting political decisions.

And whether CPF-OA interest rates will go up is quite a tricky political discussion that I don’t want to wade into.

So I leave you to draw your own conclusions on this.

Cannot be bought online – had to go down to the bank

The other big concern of course, is that before this you can to go down to the bank to buy T-Bills with CPF-OA in person.

This meant an hour wait at the bank, because it couldn’t be done online.

Well, that’s been solved now…

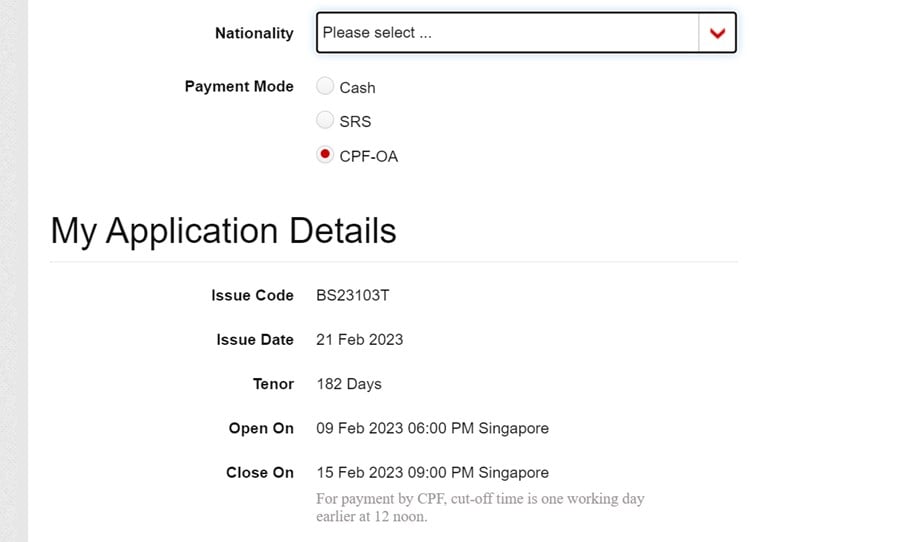

Buy T-Bills online with CPF-OA (DBS Online Banking only)

Here’s a big shoutout that you can now buy T-Bills online using CPF-OA.

Do note that this is exclusive to DBS online banking only (for now).

This means that you MUST have your CPF-IA account with DBS.

The application process is exactly the same as how you would normally buy T-Bills.

The only difference is that when you get to the application page you select “CPF-OA” instead of cash or SRS:

What if your CPF-IA account is not with DBS?

If your CPF-IA account is not with DBS, then your options are:

- Transfer your CPF-IA account to DBS

- Wait for UOB/OCBC to implement the online feature

Transfer your CPF-IA account from UOB/OCBC to DBS

To transfer your CPF-IA account to DBS, you need to go down physically to the bank branch to fill up some forms.

And it does take some time to complete the transfer, so it’s a bit of a hassle.

Although I do recall some members in the FH Group Chat complaining that other local banks (not naming names) cannot be contacted by phone if there are any problems, whereas DBS can.

If this matters a lot for you, then I do suppose transferring your CPF-IA account could make sense.

Wait for UOB/OCBC to implement the feature

Alternatively you could just wait for UOB or OCBC to implement online applications for T-Bills via CPF-OA.

Per timeline from the Straits Times, it should likely be done by the first quarter this year, which means 1 – 2 more months wait tops:

“He added that OCBC and UOB customers will be able to use their CPF savings to apply for T-bills online by the first quarter of 2023, after DBS Bank first allowed customers to do so in late January.

OCBC confirmed to The Straits Times on Tuesday evening that its customers will be able to use their mobile apps and Internet banking accounts to invest their OA and Special Account (SA) funds in T-bills from March.”

If it were me I would probably just wait – seems funny that to avoid the hassle of going down to the bank to apply T-Bills in person, your preference is to go down to the bank to transfer your CPF-IA account to another bank so that you can apply for T-Bills online.

But hey – I’m not judging, and I’m lucky because my CPF-IA account is held with DBS.

Do note that if you do note have a CPF-IA account currently, then it’s a simple choice to just go with DBS so you can buy T-Bills with CPF-OA immediately. Note that if you’re opening CPF-IA account for the first time you need to complete a quiz (CPF Investment Scheme Self-Awareness Questionnaire) to judge that you know the risks of investing your CPF-OA.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

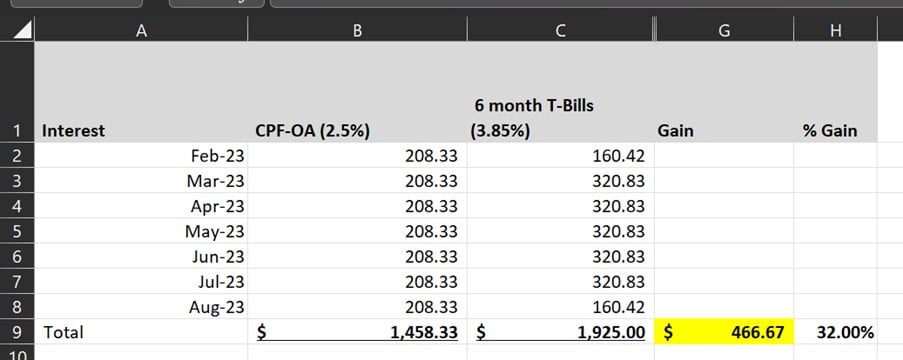

Is it worth it to buy 6 month T-Bills using CPF-OA?

I know many of you are asking this question, so I decided to run the numbers.

Let’s say we assume that:

- $100,000 of T-Bills are bought at 3.85% (using CPF-OA)

- CPF-OA interest rate does not change for the next 6 months (stays at 2.5%)

Then you will make an extra $466.67 over the next 6 months by buying T-Bills with CPF-OA.

Which is a 32.0% increase in the interest earned.

This is even after accounting for the 1 month lost CPF-OA interest from buying the 6 month T-Bills.

Is this worth it?

I mean previously when you had to go down to the bank to queue for an hour I think it was debateable depending on how much you valued your time.

But when you can do it online, I suppose there really is no excuse to avoid doing it.

Even if you are not so IT savvy it takes maybe a couple minutes tops to get it done, and the 32.0% increase in interest is not so shabby.

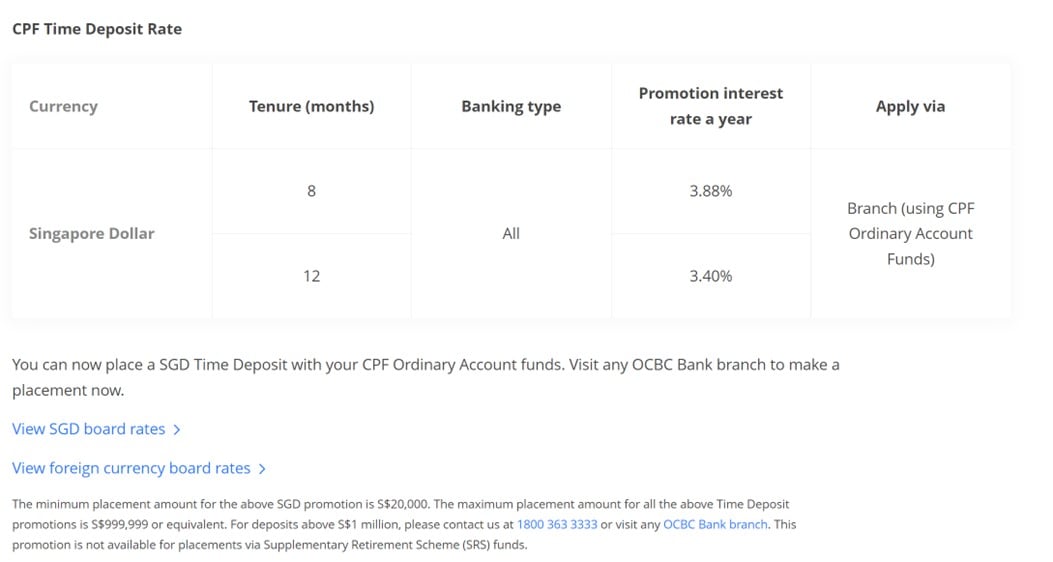

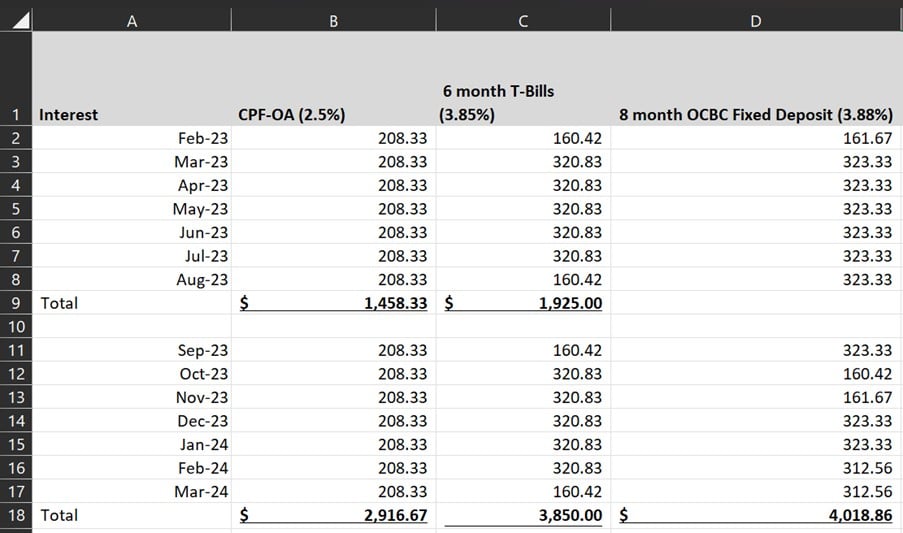

Is OCBC Fixed Deposit for CPF a better buy? 3.88% for 8 months

When it rains, it pours.

Because on top of the T-Bills, CPF-OA investors now have a new choice:

OCBC just unveiled a new fixed deposit for CPF-OA accounts this week.

Offering a 3.88% interest on CPF-OA:

The drawback of course is that this cannot be done online, and you need to go down to OCBC in person (you don’t need to have your CPF-IA account with OCBC).

But assuming you do, is this a better deal than 6 month T-Bills?

I ran the numbers below, assuming that:

- $100,000 of T-Bills are bought at 3.85% vs the same amount in OCBC’s 8 month Fixed Deposit

- In both cases – I assumed that the T-Bills/Fixed Deposit are not rolled over the same month upon maturity, but the following month (ie. You lose 1 month of CPF-OA interest)

Here are the results over the next 12 months:

As you can see, the numbers are very close.

The reason why the 8 month OCBC Fixed Deposit comes out on top slightly is because I am using a 12 month period.

Which means for the 8 month OCBC Fixed Deposit you only count 1.5 cycles, whereas with the 6 month T-Bills you are counting 2 full cycles.

Ie. With the 6 month T-Bills you lose 2 months interest using this method of calculation, whereas with the 8 month Fixed Deposit you lose 1.5 months interest only.

So this is purely down to the method of calculation, and if you run it over a 16 month period for example then the results look very different.

Long story short – the returns between the 6 month T-Bills vs the OCBC Fixed Deposit are probably very close.

The biggest factor would probably be what interest rate the T-Bills / Fixed Deposit is rolled over at when they mature in 6 / 8 months time.

What are the factors to consider when buying T-Bills or Fixed Deposit with CPF-OA?

Whether you are buying T-Bills or Fixed Deposit with CPF-OA though, the main considerations are broadly the same.

Namely – you want to get it done early in the month to avoid losing a second month of CPF interest.

This is because of a quirk in how CPF calculates the interest – in that you will lose the whole month of CPF-OA interest regardless of whether you withdraw/deposit from CPF-OA at the start of the month or the end of the month.

So if you buy using CPF-OA at the end of the month, you still lose that whole month’s CPF-OA interest.

And when it matures down the road, you get the money at the end of that month.

That doesn’t give you enough time to return the money into CPF-OA (about 3 working days), or to roll over into new T-Bills (need to wait for the next T-Bill auction).

It spills over into the next month, and you lose the next month’s CPF-OA interest.

So as far as possible, you want to try to buy the T-Bills or Fixed Deposit earlier in the month, rather than later in the month.

To get the most bang for your buck, so to speak.

So… Buy T-Bills or OCBC Fixed Deposit with CPF-OA?

I think the performance for the two will be frankly very close.

The biggest factor would probably be what interest rate the T-Bills / Fixed Deposit is rolled over at when they mature.

As many of you know, my current view is that interest rates will go down or stay flattish in the short term.

Before going up again mid term as economic growth (and inflation) starts to pick up again.

But as to whether interest rates go up in 6 months or 8 months, that’s not an easy call.

Gun to my head, I’ll probably just go with T-Bills online because it avoids the hassle of going down to the bank physically.

But you guys can see the analysis above, and decide accordingly for yourself.

Deadline to apply for 6 month T-Bills auction

The next 6 month T-Bills auction is on 16 February.

My estimated yield for the next 6 month T-Bills auction is 3.85 – 3.95% (see yesterday’s article for an indication on how I arrived at these numbers).

If you don’t want to do competitive bidding you could probably put in a non-competitive bid as they have been seeing 100% allotment the past few auctions.

This does open you up to the possibility of a freak result though, so I would probably still stick with competitive bids.

Deadline wise, you need to submit by 12 noon on 14 February 2023 if you are buying using CPF-OA.

Otherwise, deadline is 9pm on 15 February 2023 if you are buying with cash / SRS.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH,

For the 2 upcoming 6-Month T-Bills in Feb-23 (Announcement Dates = 09-Feb & 23-Feb), is it right to say that buying the 23-Feb is better as it matures 05-Sep & allows us time to roll over & buy T-Bills in same month (Sep-23) to avoid loss of revenue (since CPF not pay in that month) ?

T-Bill / Announcement Date 09-Feb / Maturity Date 22-Aug

T-Bill / Announcement Date 23-Feb / Maturity Date 05-Sep

Yes, I suppose you can say that.

Of course with the 9 Feb T-Bills you will start getting the higher interest earlier, which does make for it a bit.

Thanks! Actually trying to follow your advice to minimize loss of CPF interest. Getting confused from some other online comments saying the following using past T-Bill as example (Auction Date 29 Sep 2022 / Issue Date 04 Oct 2022 / Maturity Date 04 Apr 2023) such that “you might lose 8 months of CPF interest by investing in this issuance from September 2022 to April 2023. This represents an additional loss of CPF interest of 2 months compared to the 6-month maturity of the T-bill.”

1) Verified that DBS deducts CPF funds only on Issue Date, so above is inaccurate, given loss of CPF interest is from Oct (not Sep) & results in 7 months loss of CPF interest?

2) For following 2 upcoming T-Bills, both will result in only 1 month loss of CPF interest if we either roll over or transfer back to CPF OA during the month of maturity (Aug-23 & Sep-23 respectively) right?

(2a) Issue Date 21 Feb 2023 / Maturity Date 22 Aug 2023

(2b) Issue Date 07 Mar 2023 / Maturity Date 05 Sep 2023

Sorry for the delayed reply. Yes that is right, assuming that you can transfer back to CPF-OA (or roll into new investments) the same month of maturity.

Yes you are right that CPF funds are only deducted on the T-Bills issue date too. 🙂