Reminder: We’re running a limited Christmas promotion with $100 off the FH Investing Course. I think it’s the best investing course available on the market right now, so do check it out if you’re keen. Find out more here!

Following my previous article on the Top 5 Stocks / REITs for Singapore Investors (2020 Edition), I received quite a number of queries on how to invest in China banks.

I’d been monitoring China banks for quite a while now, so I figured this would be a good time to do an article.

Basics: How to Invest in China Banks as a Singapore Investor?

Very simply – there are 4 big banks in China. You can think of them as the big 4, the equivalent of the UOB/DBS/OCBC in Singapore.

These are China Construction Bank, Agricultural Bank of China, Bank of China, and ICBC (工商银行).

They are listed in Hong Kong (Hang Seng – H Shares), and on the onshore exchanges in China (A-Shares).

To buy the A-Shares listed in China, you need to open a brokerage account in China. This requires you to either be a PRC citizen, or possess a long-term residence permit together with up to 3 years’ worth of tax records. And because RMB is not a freely exchangeable currency, you’ll also need to figure out how to wire your RMB into your onshore China account, and how to get them out once you sell your shares (both are not easy, trust me).

So long story short, for now at least, I really don’t recommend going down the A-Shares route if you’re a foreigner, unless you’re based in China long term.

The much easier way, is to simply buy the H-Shares listed on the Hang Seng index. Most brokers out there will allow you to buy Hong Kong Shares (if your broker doesn’t work you can check out Saxo there is a new user bonus right now via the Financial Horse Affiliate Link).

Once you get your broker sorted, it’s pretty much business as usual. You just enter a buy order for the counter, and you’re done with it.

China Construction Bank’s stock code is 0939, and you can get the numbers for the other banks through a simple google search.

China Construction Bank

When I first came to China, I went to a number of banks but none of them were able to open a local account on the spot for me with my foreign visa.

It was China Construction Bank that eventually managed to do so. This was a godsend for me, because living in China without a bank account is a hell I would wish on no one.

So China Construction Bank holds a special place in my heart, which was why I wanted to start off this series by writing on them.

A quick note on China

As Singaporeans, most of us cannot comprehend the scope and scale of China.

To put things in perspective, Beijing (where China Construction Bank is headquartered), has a population of about 20 to 30 million people, which is handily around 3 to 4 times the size of Singapore. And that’s just Beijing. Once you start adding Guangdong, Fujian, Chengdu etc, it’s just incomprehensible to most of us.

And for the record, China Construction Bank’s market cap is around US$200 billion, which is around half of Singapore’s GDP.

Valuations

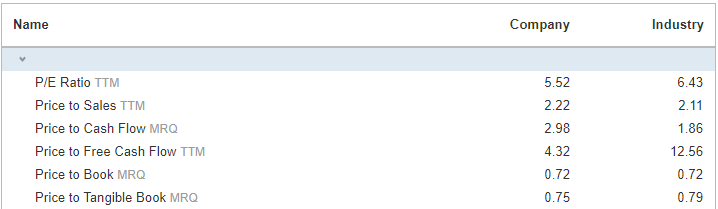

Valuations of China Construction Bank against industry averages (China banks) are set out below. Nothing out of the ordinary here, valuations are generally in line with market standards. Trailing twelve month yield is about 5.2%.

What is noteworthy though, is just how cheap the entire China banking sector is trading these days.

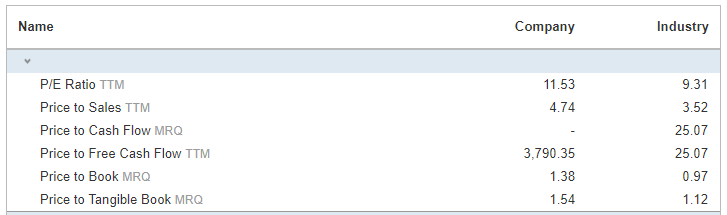

DBS’s valuations against Singapore banks valuations are set out below. As you can see, average Price to Book for the Singapore banks is around 1 (and 1.3 for DBS), versus around 0.7 for the China banks.

Business Model

Now China Construction Bank is a bank. And they make money like any other bank – by lending money:

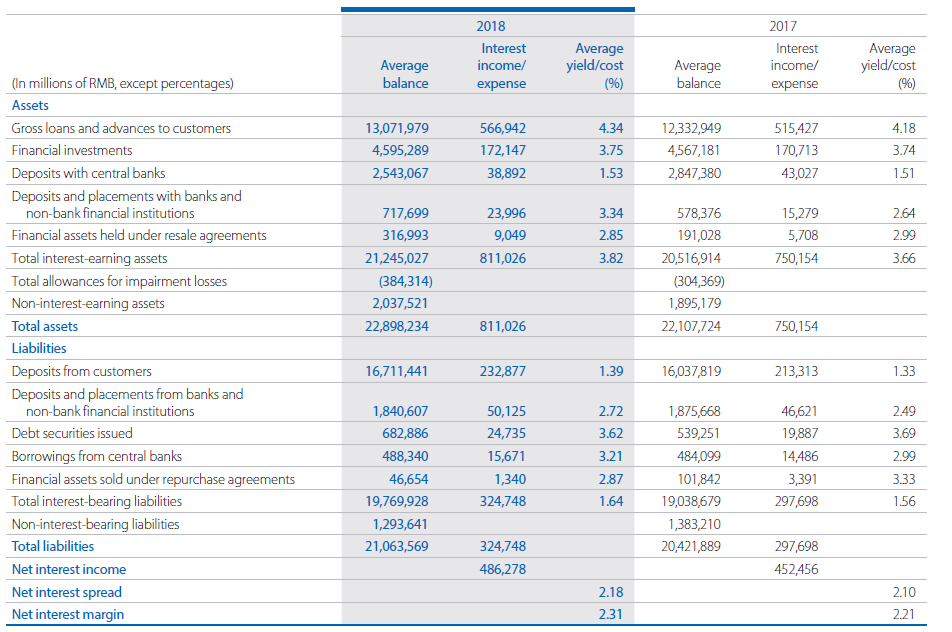

In 2018, the Group’s net interest income amounted to RMB486,278 million, an increase of RMB33,822 million, or 7.48% over 2017. The net interest income accounted for 76.73% of the operating income.

76% of the income comes in the form of net interest income, with the rest largely coming from fees and commissions (eg. Credit card or custodian fees).

Nothing out of the ordinary here.

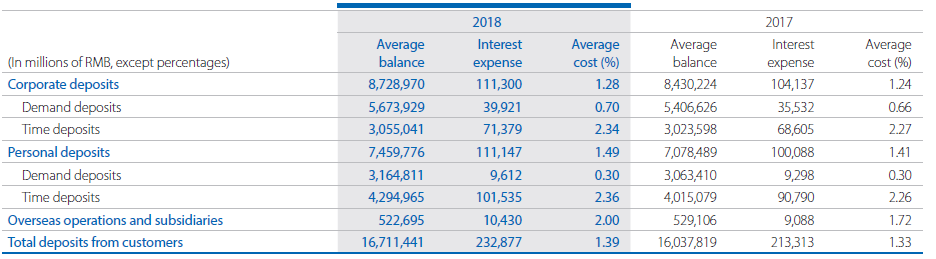

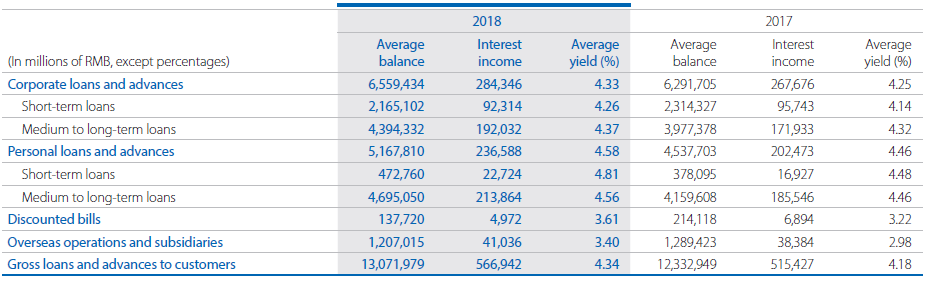

Funding Structure

Macro factors aside, the most important competitive advantage for a bank is its cost of funding. If you can borrow money cheaper than other banks, you can lend it out at a cheaper rate and still make money. It’s why DBS with it’s POSB acquisition is such a powerhouse in the Singapore market.

I’ve extracted some really great pics below that set out the average borrowing cost and lending costs for China Construction Bank.

To sum it up simply:

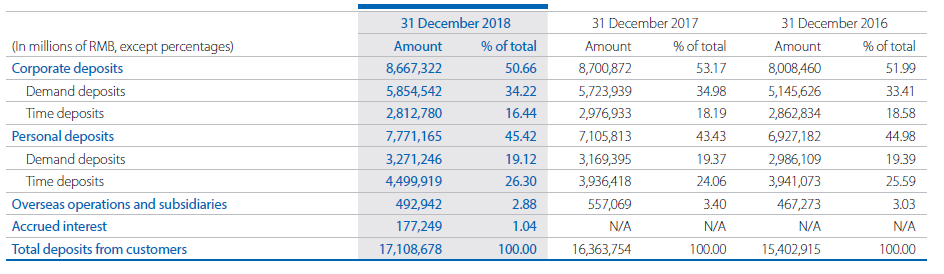

- The bulk of China Construction Bank’s funding comes from Corporate Deposits (50%) and Personal Deposits (45%).

- The average interest paid for the funding is around 1.3 to 1.5%

- The average interest on loans made by China Construction Bank is around 4%+

So China Construction Bank gets its funding from Companies and Individuals who deposit their money with the banks (on which it pays 1.5% interest), and it makes money by then lending that money out to companies and individuals at 4%+.

If that sounds unfair and a great way to make money, I completely agree. But hey, as an investor, I’m looking for companies that make money in unfair ways right? Who wants to invest in companies that fight fair?

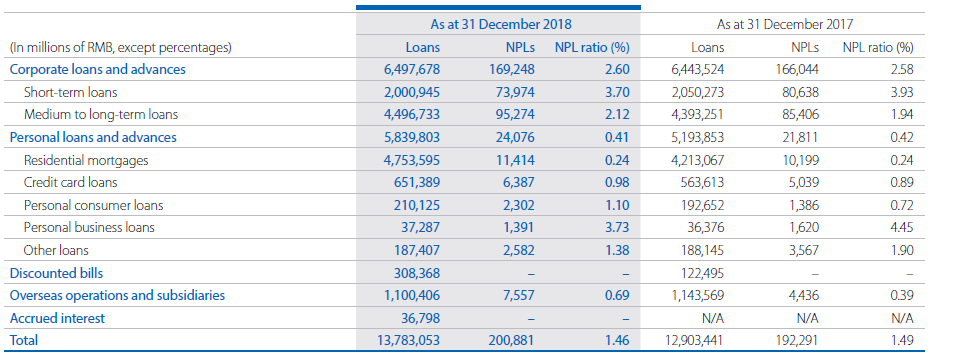

NPL

Non-performing Loan numbers (basically the amount of defaults on loans made) is set out below, and it’s a low 1.46%.

Ownership

China Construction Bank is 57% owned by Huijin, which is in turn owned by CIC (中投 – 中国投资有限责任公司), China’s Sovereign Wealth Fund.

Or in Singapore speak, China Construction Bank is majority owned by the China equivalent of Temasek. So everything you know about DBS’s relationship with Temasek, is probably somewhat true to China Construction Bank as well *wink wink*.

Investing in China?

To be honest, nothing on the corporate presentations or annual report will show you what investors are truly worried about with China Banks.

Because what investors truly fear, is how the future will play out for the China economy (and consequently how will China banks be affected), over the short and longer term.

And the fear plays out something like this:

Over the past 10 or 20 years, China has had an unprecedented economic boom. A large part of this was fuelled by an unprecedented credit growth that really accelerated after 2008. Huge amounts of debt were created that went into infrastructure spending, and a fair bit of it went into the housing market.

Now credit growth is okay if it is matched by an equivalent economic growth. So if you create $500 billion worth of debt each year, it’s completely ok if your economy grows by $500 billion as well.

The problem comes when economic growth starts to slow. It’s a bit of a chicken and egg, but in China the economic growth slowing is in part due to the breakneck credit growth, because it becomes harder and harder to allocate capital efficiently.

The way I like to think of it is to imagine that I am running a small farm. When the bank gives me a $100 million loan, I’m taking that money to improve the chicken farming process, install new high-tech equipment, hire new farm hands etc. Productivity soars, and both me and the bank are happy.

But when the bank gives me a $1 billion loan, I only need $100 million to improve the farm. What do I do with the remaining $900 million? I take it to buy a new farm. And what happens when every farmer has that same $1 billion loan. Who will be selling their farm in such a situation? Likely no one, so the net result is that farm prices go up (ie. asset price inflation).

So the $100 million loan was great because it created productivity growth. But upping the $100 million loan to $1 billion didn’t do so much for productivity in the short term, all it did was to increase asset prices (inflation of farm prices).

It’s a massive, massive simplification of how things work in reality, but it does illustrate the problems facing the China (and world) economy. Credit creation is useful – up to a certain extent. Beyond that point, economic growth comes from productivity growth, which comes from technological advancements (which in the farming example, will be new farming techniques that increase efficiency). So just extending more loans, isn’t necessarily going to grow productivity, it just creates inflation.

China is in a similar position where future credit growth has limited effectiveness. Future growth will need to come from structural reforms to the economy, and a shift towards a higher value added, consumption driven economy. Hence the emphasis on 5G, on Artificial Intelligence, Facial recognition etc.

But that takes time.

So in the shorter term, economic growth will start to slow. And once it does, a lot of the excesses of the past will come to fruition.

Back to the farm example – when every farmer had a $1 billion loan from the bank, every farmer was a happy farmer. So the lousier farmers who were less productive, produced lousier crops, and were less efficient in general, were still able to survive because they could use the loan to get by. But once you gradually start withdrawing the loans, then you’ll know which are the great farmers. So the great farmers that used the loans to improve their farms, upgrade their processes, those farmers will survive. Those that used it to pay their staff, buy new cars, or gamble, those farmers are going bankrupt pretty quick.

Warren Buffet has a great quote for this – “When the tide goes out, you see who’s swimming naked”.

So when economic growth starts to slow, as it will from 2020 onwards (general guidance for China in 2020 seems to be sub-6% growth), we’ll start to see who were the “lazy farmers”.

This will translate into more default in the economy, which is what we’ve started to see over the past 1 to 2 years. In fact the past week, a China SoE linked to the Tianjin government defaulted on its offshore bond payments. This was the first ever default by an SoE, which shows that even SoEs aren’t sacrosanct now. The China government will let some companies fail, the question is which ones, and how much.

How does this impact China Construction Bank?

So coming back to China Construction Bank. How does this impact China Construction Bank?

2 main ways:

- Book Value a question mark?

As the default rates on loans starts going up, the book value of China Construction Bank will be called into question. Sure, it’s trading at a 30% discount to book now, but if 30% of that book value goes bad, then suddenly China Construction Bank is trading book value, which makes it a lot less attractive.

So as investors, we don’t actually know how many of China Construction Bank’s current loans are being extended to the “bad farmers”, which makes an investment in China Construction Bank a bit of a leap of faith.

And don’t forget that a lot of these banks are heavily exposed to the property and infrastructure sector. As the property market starts to cool, it’s really tough to say how many firms will be allowed to go under, and the potential impact on China Constuction Bank’s book value.

There’s a lot of talk about how the government will loosen financial conditions in 2020, but it’s still really hard to say how things will play out.

- What happens in an economic slowdown?

The second one is an even bigger question mark.

In China, Business and Politics are one and the same thing. Business is politics, and politics is business.

In an economic slowdown when big SoEs start running into problems, the big banks may be called upon to extend loans to prop up SoEs. That could further impact their balance sheet in a downturn, which raises even more questions as to the quality of their book.

Closing Thoughts: Would I invest in China Construction Bank?

This article has become way longer than I expected. But to sum it up – Would I invest in China Construction Bank now?

It really all boils down to China’s economic growth. If China continues growing at about 5% average over the next 10 years, none of the above really matters, and China Construction Bank in 10 years probably trades at a higher share price than today. If China grows at much lower than that, well then the world economy probably has other big problems to deal with.

So I have no idea how things will play out over a 12 to 24 month period. The US-China Trade War, the China deleveraging cycle, and US elections, are all big wildcards that are impossible to predict with a high degree of certainty.

But over a 10-year period, my bet is that the Chinese economy will be significantly bigger than where it is today. And if so, I quite like China Construction Bank on a risk-reward basis.

I am giving China Construction Bank a 3 Horse rating to reflect that it’s a decent long-term investment, but could be highly volatile in the short term (12 to 24 month). It’ll be a wild ride, so hold on to your horses!

Reminder: We’re running a limited Christmas promotion with $100 off the FH Investing Course. I think it’s the best investing course available on the market right now, so do check it out if you’re keen. Find out more here!

Financial Horse Rating – China Construction Bank

Financial Horse Rating Scale

What do you guys think of China Construction Bank? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

I have some fund parked with Chartered bank in HK. Can you advise me how I can use the fund without transferring back to Singapore to invest in HS exchange. I have so far never invest other than SGX.

You can try setting up a brokerage account with SCB and draw on the HK funds directly to settle the trade. You’ll need to speak with SCB to see how this can be done.

Dear Sir,

Thanks for the article.

Can i check with you whether these 04 x big china bank pay out dividend regularly to their retail investor? If yes, are they consider generous or stingy if we compare with our local bank such as DBS, UOB.

Thank you

Yep they pay out regular dividends. Their track record isn’t as long as the local banks so it’s hard to comment. Based on trailing twelve month yields, they’re mostly at 5%+ yields now, compared to about 3 to 4% for Singapore, so I guess in that aspect they are “generous”.

Hope this helps!

Dear FH,

I am a young investor (19) looking to diversify geographically.

If i were to be looking at the long-term(10++) years, what would you recommend is the best way to gain exposure to China? Currently i am only eyeing investing in their banks or buying a china ETF on the HKEX.

Thanks 🙂

Haha that’s another tough one. There’s no easy way to get exposure to China at this stage. The options are (1) passive indexing via Hang Seng Index or China A50 (not ideal because China market is inefficient) or (2) active management (either DIY or fund manager).

Which one you pick, really depends on what kind of investor you are. Do you prefer to go with the low cost option and achieve average returns, or do you want to try your hand at selection (DIY), or do you want to try to pick a fund manager but pay high fees for that?

Hi FH,

there’s a low quantum way of investing in HK / China banks, which is investing in BMO HONG KONG BANKS ETF (HKEX:3143) via Fundsupermart RSP, what’s your view on this?

Haven’t looked at that closely to be honest. So can’t really comment.

Hi FH,

China banks have gotten significantly cheaper since this article and a lot of things have changed with the pandemic.

Would be interested to hear your views on investing in China banks now. If you had to pick between the Big 4 China banks, which one would you pick?

Thanks!

That’s an interesting question. There are still big structural problems with all the credit/solvency issues, but I suppose averaging in could make sense at these prices. I would probably go with ICBC/CCB.

There’s always a leap of faith with China banks. You never know the true book value or how many bad loans there are, and you just accept that CCP will not allow a big bank to fail or shareholders to take the fall. But if that’s a risk you’re ok with, the dividends are very strong though.

Thanks. I guess the question is whether one believes in investing in banks at this time as they all have credit/solvency issues all over the world.

But if one does believe in investing in this sector, then it seems that the Chinese banks are potentially the most overlooked at this moment.

If one prioritizes safety, then the Big 4 are not just the largest banks in China but the largest in the world so they are so systematically important that collapse would mean that the Chinese economy or government has collapsed. Possible given the sustained attacks of the US but perhaps not that likely and so far the recovery in the Chinese economy is the fastest of any large market. Provisions for bad loans have also been increased so maybe this provides some additional safety as well.

If one considers profitability, then the Chinese economy is one of the few that is still functioning with traditional economics and interest rates still at “normal” levels rather than being cut to zero or negative, which means that banks can still earn a decent NIM, something not found in any other major economy today.

If one considers valuation, then they are trading at multi-year lows with price/book values at extreme levels – BOC for example, is trading at 0.35x book, close to multi-decade lows, with dividend yield at 8% and CCB is trading at 0.5x book so the margin of safety seems quite wide.

The question I guess is when to start accumulating. I started too early with Shell at GBP15 but continued averaging in all the way down to GBP8.5 so overall it has worked out with the recent recovery but could have been better if I had started accumulating later.

Perhaps worth a deep-dive in one of your future articles?

Thanks CMC, all very valid concerns.

Like you said, the big question is when to start accumulating. I thought ICBC at $4 and CCB at $5 just a few months ago was a great time, and if it goes back there I may look to add. I definitely don’t think 2021 is one way up for China, there are going to be real structural issues that need to be addressed. So I think this is a trade that we can be patient on.