As promised, I’ve been meaning to do an article on commodities for the longest time now.

If I am right, commodities investing might become a big part of this decade, so it’s worth spending some time to understand the basics.

Let’s talk about the commodities industries generally, and what drives the commodities market and commodities prices.

Now I know that this part might come across as being boring, but trust me it is important. Trying to invest in commodities without understanding the fundamentals is like trying to run before you learn to walk.

You need to have a sound understanding of the basics that drive commodities prices before you move on to the more complex equity and futures plays.

Basics: What are the key types of commodities?

Broadly speaking, there are 3 types of commodities:

- Energy (Oil, Natural Gas, Coal, etc)

- Agriculture (Corn, Wheat, Soybeans, Cattle, etc)

- Metals (Steel, Copper, Aluminium, Uranium, etc)

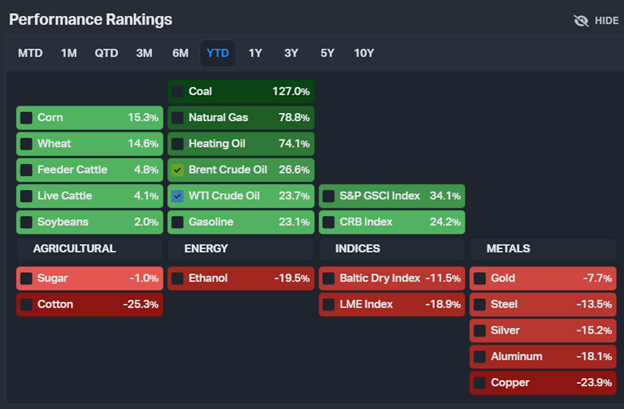

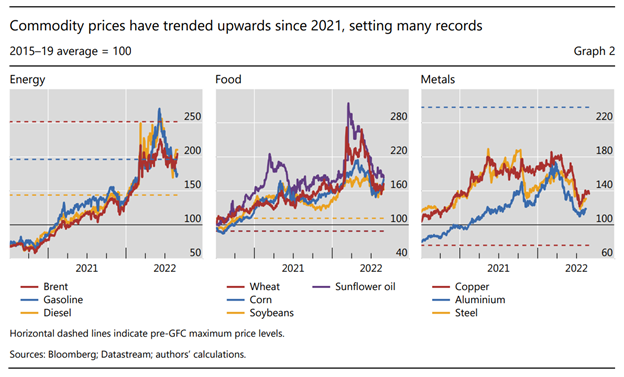

You can see the big commodities (and their year-to-date performance) below:

I know that precious metals (Gold and Silver) can be viewed as a form of metal.

But in my view, I find that precious metals behave more like a store of value, and have investment characteristics quite different from commodities.

Because of that, I find it more helpful to view precious metals as a totally separate asset class, separate from commodities.

FYI, you can trade commodities via SaxoTraderGo, find out more here!

Connect with Saxo on their Telegram channel!

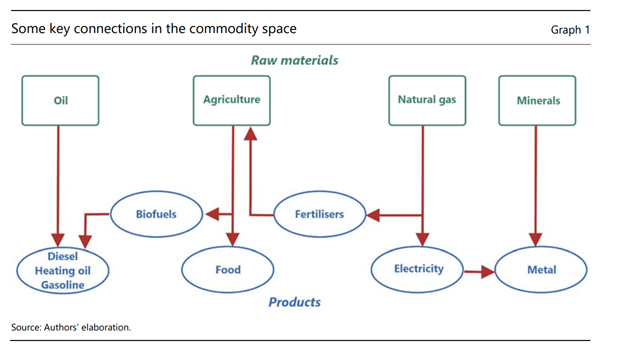

What is the relationship between the different types of commodities?

The chart above sets out a great visualization on how the commodities all come together.

Let’s walk through it.

Oil is the alpha commodity (for now…)

Simply put – almost every commodity is directly or indirectly affected by the price of oil.

So if you only want to get exposure to one commodity and not fuss over it, oil is probably the best choice (for now).

Take natural gas for example – Natural gas is a byproduct of oil drilling, and the transportation of LNG via boat requires oil, all of which trace back to oil’s price.

With agriculture, farmers need diesel to power tractors, and transport the final products to consumers. While fertilizer comes from Natural Gas via the Haber Process, which again traces back to oil.

With metal, the ore is transported on boats/trucks using oil, and when smelted require lots of electricity which traces back to Natural Gas and back to oil.

In the 1970s, oil powered everything. From heating to electricity to transportation, it all ran on oil.

These days however, the bulk of electricity generation comes from natural gas (and to a lesser extent coal).

Today, oil is primarily used only in transportation – cars, planes, boats, tractors etc. But for what it’s worth, that’s still a huge and vital part of the global economy.

But… transition to Renewables is real

But of course, that is only for the short to mid-term.

In the long term, I think it’s safe to say that the world will likely transition into renewables energy given the massive investments into it.

So, oil is the alpha commodity for now, but one wonders if the days for oil are numbered.

What drives commodities prices? – Supply vs Demand

What drives commodities prices?

It’s as simple as supply, vs demand.

Demand

How much demand is there for the commodity?

Demand is largely driven by economic growth.

The stronger the economic growth, the larger the demand for commodities (most of the time).

Which is why right now as we are going into a broad global recession, many investors are worried about the demand outlook for commodities going forward (leaving aside the supply side discussion).

This is why short oil / short commodities has become a popular play for many hedge funds the past few months.

Interestingly, BHP, the world’s largest iron ore producer, sees China emerging as a source of stable commodity demand in 2023. According to BHP, sales of iron ore to China currently make up 65% of BHP’s business, and sales to China have been increasing for half a decade as China has drastically increased its demand for iron ore (the key element in steel).

Commodities demand is heavily linked

The complexity though, is that as prices of one commodity go up, buyers may switch to another cheaper commodity, driving prices of the other commodity up.

Think about it as Malaysia banning the export of live chickens to Singapore. The net effect, is that the price of pork and fish goes up in the short term, as consumers switch to alternative products. Multiply this, on a global level.

To give an example – corn can be used to produce ethanol, which can be blended with diesel to produce biodiesel.

Which means that as the price of oil goes up, the demand for substitutes (e.g. ethanol, which comes from corn) goes up – driving up the price of corn.

Or if Russia shuts off natural gas to Germany, Germany is forced to buy Liquefied Natural Gas from the open market, driving up the price of natural gas, which drives up the price of fertilizer (because natural gas is a key input for ammonia used to produce fertilizer), which drives up the price of grain, which drives up the price of cattle, and so on.

Complex systems are not easy to predict

The key takeaway here is that the global commodities supply chain is heavily interconnected, and highly complex.

And with all complex systems, a small change in one part of the system, can have broadly profound second and third order effects on the rest of the system.

So when you look at commodities, I encourage you to always look beyond the first order effects, and look at the second and third order effects.

Take the EU discussing oil price caps on Russian oil in September this year, for example.

First order effects would be to think that this will drive oil prices down, because of the price cap.

Second order effects would be to think that Russia will simply sell to Asia instead, and the supply that Asia does not buy will be bought by Europe, so oil balances out.

Third order effects would be to think that OPEC fears that price caps will be used against them one day, which leads to OPEC+ cutting supply, which leads to oil prices going up.

As you can see, a simple move designed to bring the price of oil down, can easily drive the price of oil up once you account for higher order effects.

Supply

With commodities – the supply usually has a long lead time (just like real estate).

Supply investment decisions are made on prices 3 – 5 years out.

The decision to invest in new production capacity is not made on today’s prices, but on prices 3 – 5 years out.

For example, a new coal mine can take anywhere from 3 – 5 years to come online.

If you’re a CEO thinking about whether to invest in a coal mine that will come online 5 years later, you’re not making that decision on coal prices today, you’re going to look at the prices of coal in 5 years time.

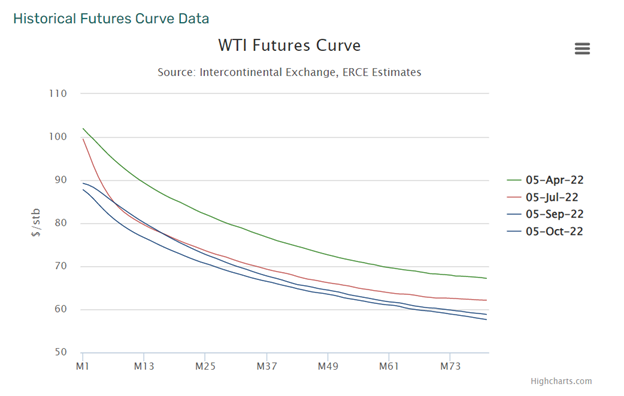

And if you look at most commodities curves right now, they generally look like this:

Prices of commodities are high in the short term, but 3 – 5 years out, they drop quite drastically.

So if you’re a commodities producer, you won’t invest heavily in new supply in an environment like that, since you’ll just be selling into a market where coal is a lot cheaper.

Especially not when every government is talking about the transition to green energy, and how they’re going to tax your “windfall profits” if you make too much.

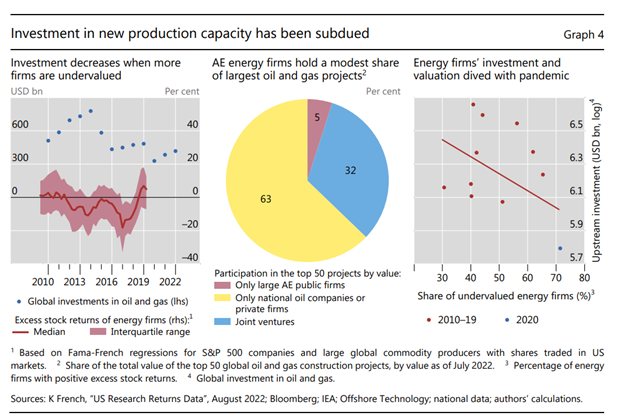

This, coupled with the past 10 years of commodities bust, means that despite soaring commodities prices, investment into new commodities supply is still very low:

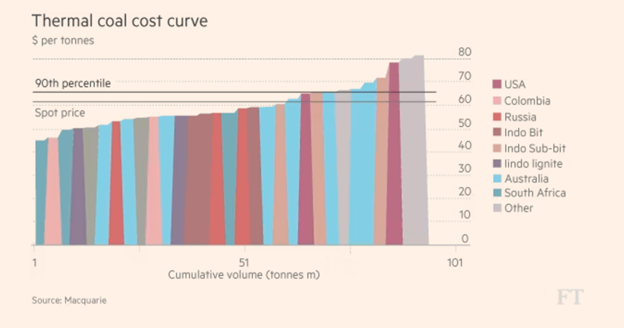

Understanding Cost Curves

When investing in commodities, it is wise to understand cost curves.

What is a cost curve?

Basically, it’s a graph that plots the production capacity and costs of an entire industry, see the case below. On the X-Axis, cumulative production is ranked. Producers (or projects) are laid out from low to high cost and bars are used to indicate their output — the wider the bar the more they churn out. On the Y-Axis is the cost of production. The result is rather ugly looking bar chart that slopes upward; left to right. (see below)

In other words – a cost curve tells you the cost structure of a commodity.

At a high level, looking at spot price vs the cost structure gives you an idea of how many producers are making money vs losing money.

This gives you an idea of how they will think about investing in new capacity, which has big implications on future supply.

And on a micro level, generally speaking, you want to invest in producers that have a cheaper cost profile.

Other unique characteristics of Commodities

Now there are a few other interesting characteristics about commodities markets, that I wanted to discuss below:

- Commodities are priced at the margin

- Commodities markets are rigged

- Commodities prices are not easy to call in the short term

- Commodities are prone to boom bust cycles

- Physical vs Paper Prices can diverge

Commodities are priced at the margin

The funny thing about supply vs demand, is that it is the marginal producer that determines the price.

To put it simply, let’s imagine there are 1000 barrels for oil in the market, and buyers for 1001 barrels of oil.

999 barrels of oil will be matched with no problem.

But the final barrel of oil is the problem.

And it is the price that the buyer is willing to pay for this last barrel of oil, that determines the marginal price of oil.

So when you see the price of commodities in the market or in futures market, you are looking at pricing at the margin.

This is why a small demand-supply mismatch can create massive changes in pricing.

Look at what happened in 2015 with oil when OPEC increased production slightly (oil prices crashed), and look at what happened in 2020 when demand fell a bit more than supply (oil prices went negative).

Commodities markets are rigged?

The other thing to note, is that commodities markets is often alleged to be heavily manipulated.

Manipulation has been a vexing subject in the commodity futures markets from the mid-19th century.

Trading on inside information is something that is observed and called-out in the industry.

In commodities, there are the presence of cartels like OPEC+, where they come together to increase and decrease supply to influence prices.

Commodities prices are not easy to call in the short term

Because of this, commodities prices can be very volatile and very hard to predict in the short term.

I’ve learned the hard way that unless you have an edge (read: inside information), you pretty much DO NOT want to trade an OPEC meeting.

If you’re a short term trader, I find it best to just sit out the OPEC meeting.

And for long term investors, the short term day to day usually doesn’t mean so much for the longer term outlook. In fact you would look to capitalize on short term inefficiencies in the market, to buy long term positions.

Commodities are prone to boom bust cycles

Because of the long lead time for new supply, commodities markets (just like semiconductors and real estate) are prone to big boom bust cycles.

When prices are high, everyone invests heavily in new production capacity.

Eventually, all the new production capacity comes online at the same time, and the new supply is much larger than the demand.

And because commodities are priced at the margins, this can create spectacular crashes in commodities prices.

Because of this, commodities equities are funny in that the stocks look the cheapest (from a P/E perspective) at the peak of the cycle. This is when commodities prices are at a high, and the companies are pulling in record earnings.

And at the bottom, after commodities prices have collapsed, they look the most expensive from a P/E perspective.

So this is a key point to note when looking at commodities stocks, the valuations can be very deceptive.

You want to buy at the bottom of the cycle when they look the most expensive from a P/E perspective, and you sell at the top when they look the cheapest from a P/E perspective.

Physical vs Paper Prices can diverge

The other thing about commodities, is that unlike stocks which are purely financial instruments, with commodities there are theoretically 2 prices:

- Paper price (priced in futures markets on exchanges)

- Price for physical delivery

Most of the time, (1) and (2) are very close.

But in times of tight supply, (1) and (2) can diverge.

Which creates a problem because with the development of financial markets, most producers will price their commodities based on the price reflected on futures markets.

Which becomes a case of the tail wagging the dog, where futures prices are manipulated down, and producers then sell at that lower price.

Recently, you may hear the Saudis talking about how they are not pleased that the paper price of oil is so low, when there is record tightness in the oil market for physical delivery.

This is something you may hear from gold and silver investors as well, where some investors claim that bullion banks manipulate gold / silver paper prices.

In this article, we’ve covered some fundamentals of investing in commodities. We’ll try to do a second part soon, where we’ll do a deeper dive into how to invest in commodities (using stocks vs futures vs ETFs).

Trade Commodities via SaxoTraderGo

Interested in commodities trading? You can trade commodities futures via SaxoTraderGO!

Check out SaxoTraderGo’s instant demo here!

Connect with Saxo on their newly launched Telegram channel!

Financial Horse x Saxo Opening Account Promo

For FH readers, there is special cash account opening bonus for new Saxo account holders (drop email to [email protected] for full steps): Financial Horse x Saxo Affiliate Link

Note: This post is in collaboration with Saxo Markets. All views and opinions expressed in this post are from Financial Horse.

This advertisement has not been reviewed by the Monetary Authority of Singapore.