After the March that we had, the past week felt like a breeze.

Lots to cover though, so I’ll skip the introduction.

As always, this article is written as at 3 April 2020, and will not be updated going forward. Updated thoughts are on Patron.

Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Basics: What happened the past week

The past week was a lot less action packed in terms of big events.

This supports my thinking that Phase I of the Virus panic is now over. Phase I was characterized by forced deleveraging, and was a disorderly exit.

Phase II on the other hand, will be characterized by corporate defaults, and will play out more like a plain vanilla recession (or depression).

2 big events to talk about: (1) COVID-19 Bill, and (2) Asymptomatic Transmission.

COVID-19 Bill in Singapore

I wouldn’t say that yesterday’s shutdown had a material effect on share prices. The way I see it, once we started getting signs of community transmission in Singapore, an escalation in the shutdown was bound to happen – the only question was timing. Now that it’s happened, the timer starts running on when COVID19 in Singapore will come under control, which I see as a good thing.

What was unexpected though, was the implementation of the COVID-19 bill.

I genuinely did a double take when I saw this one.

For those who missed it (details here), this bill temporarily suspends all contractual obligations for parties hit by COVID19.

So let’s say you run a shop in a mall, selling stuffed toys to schoolkids. You think that COVID19 has hit your business. So you write an email to your landlord telling him how tough business is because of this virus. Now you no longer need to pay rent for the next 6 months, and the landlord cannot evict you, nor can they sue you. The rent is deferred, and you only pay the rent after the 6 months period if over (government has an option to extend for another 6 months). Oh, and don’t forget that you can just declare bankruptcy after 6 months, so the landlord never gets the rent.

Based on my reading of the Business Times article (correct me if its wrong), that’s what this new bill does. So I genuinely had a double take when I read this.

If it goes through in its current form, I think it’s not just going to be pain for the landlords, its going to be an insolvency event for the smaller REITs and more leveraged developers. A significant drop in the cash flow like that would bankrupt many real estate players.

To my mind, there’s an almost zero percent chance of this bill coming into effect in this form as reported. Almost zero.

The only way it comes into effect in this form is if government also delays all repayment obligations on the part of the landlord to the bank. Basically allowing the REITs and developers not to repay their property loans, and allowing them to defer any refinancing during this 6 month period. Or extending new lines of credit to the landlords.

Which then means the banks are in trouble.

So yeah, my suspicion is that this bill will be tweaked before being passed. Chances are it will be done via a change to a definition somewhere, or to create a carve out.

Whatever the case, the market (rightly so) freaked out once it saw this. REITs have been selling off ever since news of this bill came out on Wednesday night.

Why COVID-19 could be worse than what everyone is expecting

After last week’s article, I had a few great comments pointing out how I may be underplaying the virus situation.

So this week, I went into a deep dive into all virus related material.

And I started getting really worried.

I think the key here that many people are missing out on (myself included), is asymptomatic transmission.

Asymptomatic Transmission

The latest reports from China show that once the virus has been contained, asymptomatic transmission then becomes a problem. There are people in the population who have the virus, and are transmissible, but they have no visible symptoms. How do you weed them out from the system?

Now imagine Europe and US in May/June, after the shutdown is over.

They do a phased reopen.

They then discover new infections across the country, from asymptomatic transmissions. How do they respond?

And that’s happening in China right now, where after a 2 month shutdown, they now have asymptomatic transmission, forcing them to shut another county the past week.

Dark Forest thinking

Fans of the Three Body Problem are familiar with the Dark Forest thinking. To simplify – This theory states that because civilizations never know what other civilizations are thinking, they always have to assume the worst. I love it because it’s a very realistic take on human psychology – rather than the utopian Star Wars style thinking.

Let’s apply that logic here. It is now June, and Indonesia says that they have completely eradicated COVID19 on their shores. Brazil says the same. Does Singapore go on to allow Indonesians and Brazilians to enter Singapore freely? What about the US? What about Australia? Does the world believe each other?

The problem with COVID19 and asymptomatic transmission, is that it will be hard for countries to trust each other once this is over.

In the interests of protecting their own citizens and avoiding a new shutdown, every country will err on the side of caution. No country wants to be the first to lift COVID19 travel restrictions. It could become a game of trust, played out at a national level.

Now I don’t know exactly how this will play out, but my current thinking is that some form of COVID19 restrictions will remain in place well into Q3, even after the lockdowns have been lifted.

The economic impact could be massive.

How to invest in 2020?

As always, how to invest in 2020 is unique to your own risk appetite and investment objectives. You need to decide for yourself. No one can tell you how to invest, other than yourself.

In the second part of this article, I will share my own approach to investing in 2020, and you guys can decide if its relevant for you.

Step 1 – Decide Asset Allocation

The first step to investing, and one that should have been done way before 2020. This requires me to decide the asset allocation I want to adopt, based on my risk appetite, and my read of the global macro cycle.

Broad asset classes are: Stocks, REITs, Bonds, Cash, Gold, Commodities.

For me personally, my current asset allocation is heavily tilted towards gold, cash and bonds, and as 2020 – 2021 plays out, it will gradually rotate into stocks and REITs.

My full portfolio breakdown is available on Patron for those who are interested.

Step 2 – Decide Final Portfolio Allocation

Next I will decide what I want my final portfolio to look like after the COVID19 crisis is over. I break it down by asset class, and within each class I break it down into individual components. So I decide how much REITs I want to own, and then decide how much of each REIT. It’s a dream list for stocks if you like.

In 2020, I think quality will be king in the coming months, because a lot of the smaller players are going bankrupt. My rules for stock selection are:

- Sound balance sheet to outlast COVID-19

- Resilient business model that will rebound after COVID-19. Ideally:

- Products that are loved by consumers and add customer value

- Competitive advantage

- Good margins

- Cash flow – can’t stress this enough, cash flow is king. Look for companies with strong cash flow

Stocks on my watchlist are on Patron.

Step 3 – Execute

So now I know the start, and I know the end. The next part, and the hardest part, is the execution.

I view the buy window as being open for 2020, and what’s going on out there right now is just a stock picker’s dream. Active investing is a MUST in this climate. Certain counters are selling are firesale prices, while others are at ridiculous valuations. If you index, you’re just buying the average of the market, and the average doesn’t look at cheap to me right now.

In particular, I think the Singapore market has a lot of high quality gems available, at fantastic prices. US and China/HK markets less so (especially for the big caps) – but we will get there in the coming months. For US/China/HK, the small and mid caps have already been decimated, so lots of value if you can pick up the high quality ones. But remember to look for cash flow and balance sheet strength, the wave of corporate defaults hasn’t even started.

What macro signals to monitor for 2020 – Phase II?

What I also wanted to share, was the macro framework to approach investing in this market.

The 3 buy signals I used for Phase I of this crisis have worked really well, and I wanted to build on them for Phase II.

As always, I’m searching for contrary views here. Let me know where you disagree, let me know where I am wrong, and we can discuss in the comments section below.

Macro Signal 1 – Virus Situation

The virus situation HAS to be number 1. Everything flows back to the virus situation. If this isn’t contained, the economy cannot restart, and stocks continue to freefall.

My base case assumes Europe and US doing phased reopens in May/June, with COVID-19 restrictions remaining in place until Q3.

I suspect COVID-19 restrictions only go away once a vaccine is developed.

Now I am not a doctor so I have no idea when this will come into play, but from what I’m reading – Absolute best case scenario, all the stars align style situation – we’re probably looking at Q3/Q4 earliest for a vaccine.

Base case? Probably 2021 for a vaccine.

A lot of news surrounding the use of Chloroquine as a treatment. If this works, the problem could go away quickly, so it’s definitely one to monitor – but for now, I’m not that optimistic.

I am very worried about the situation in Latam (esp Brazil), Africa, and Indonesia. If the virus gets out of hand there, the human tragedy could be unbelievable. So all those are at the top of my radar.

Macro Signal 2 – USD Strength and EM collapse

My latest thinking is that the peak in USD strength, may mark the bottoming out of this crisis.

It’s a bold call I know, so I wanted to break it down.

A few weeks ago (read this for more context), I talked about how the King Dollar (USD) will wreck the global economy. The underlying thesis is that companies and countries borrowed in USD in the good times, and entered into USD obligations. Business has now dried up, so they no longer get paid in USD. But the obligations remain. So all these companies and countries are now scrambling to find USD.

I also talked about how the swap lines extended by the Feds will solve the short term strength in the USD, but that will be short lived. The USD will come roaring back.

And that has played out exactly like we discussed.

USD transmission

Why do the swap lines not work? The simple answer is transmission. The swap lines go to the central banks, but it is the companies that need the USD the most.

And how do companies get USD from the central bank?

They can’t, so they need to borrow via a bank, who then borrows from the Central Bank. And the real problem now, is that no bank wants to lend, because why do they want to take on the credit risk? There is a real chance the company cannot repay the bank, which puts the bank in a tough spot.

So USD transmission is going to be a problem in the days ahead, and until that is solved, the USD will soar. Remember that the companies and countries continue to owe USD obligations, so the stronger the USD, the harder it is for them to repay those obligations.

My thinking is that the USD will continue to soar, and this will spell doom for many Emerging Market (EM) countries and companies. My thinking is also that this saga will be so bad, that it will spell the start of the end for the USD as a reserve currency. Once all this is over, people will be seriously looking for an alternative to the USD.

EM collapse

But closer to home, the short term impact on EM could be massive. These guys are hit by a double whammy of capital outflows (investors pulling cash out of the country) and falling earnings (commodities price collapse, fall in global demand), which impacts their ability to repay.

It plays out broadly like the Asian Financial Crisis, with a few notable exceptions.

I think this time around, Asian EM is not as highly leveraged. They’ve learnt the lessons of 97, so they are better prepared. It will still be bad, but not 1997 style bad.

The most vulnerable to me are Indonesia (IDR), Malaysia (MYR) and Australia (AUD). Australia is lucky because they have a direct USD swap line to the Feds that has rescued the AUD, but Indonesia and Malaysia don’t have such swap lines.

So yeah, it’s going to get worse before it gets better. Don’t forget that no man is an Island, so a weak Malaysia and Indonesia, is really bad news for Singapore as well.

Watching how this dynamic plays out will be highly instructive for buy signals. USD peaking could mark the bottom.

Macro Signal 3 – Policy Responses (including regulatory policy, or Fiscal and Monetary Stimulus)

Policy responses to address the economic fallout of COVID19 can be split into 3:

- Regulatory Policy – stuff like the COVID19 Bill

- Fiscal Stimulus – like the 2T package from the US, and Singapore’s supplemental budget

- Monetary Stimulus –action from the Feds and ECB going forward

Whatever that’s been done so far, only goes towards helping Phase I.

Phase II will play out rapidly in the coming months, and more of the 3 measures above will be required.

The speed and effectiveness of the policies as they are being rolled out will be key to determine the impact on financial markets, and the timing at which I buy.

I will share my analysis on all these in the months ahead, every weekend, rain or shine, so just check back on Financial Horse every weekend.

Macro Signal 4 – Corporate bankruptcies and Layoffs

The past week has given us a taste of this, with a huge wave of corporate downgrades, and the first oil bankruptcy (Whiting Petroleum).

Make no mistake, this is just the start. I expect a massive wave of corporate bankruptcies and layoffs over the next quarter or two.

In particular, I’m very worried about a big name bankruptcy. In 2008 we had Lehman brothers. In 2020, which household name is going to go under?

WeWork in particular is high on my list. I just don’t see how they can survive in this market. Cash flow is in shreds (all the freelancers have cancelled) and Softbank has pulled out of the $3 billion share buyout. The Softbank loan was conditional on the share buyout, so that’s gone too.

Who else can or will bail out WeWork in times like this?

Don’t forget that WeWork is the number 1 tenant in many key markets, so a WeWork bankruptcy kills the corporate real estate (CRE) market globally. If it happens, that just could be this crisis’s Lehman Brothers.

The worse the news coming out of this area, the stronger the buy signal. I know it’s a bit of a schadenfreude, which does make me sad too.

Closing Thoughts: Marathon, not a race

A lot of people are still thinking we get a V shaped recovery (in absolute terms, not QoQ). I don’t know what these guys are on, but I wouldn’t mind having some.

But I hope to be proven wrong, because just like you, I want this recession to be over quick.

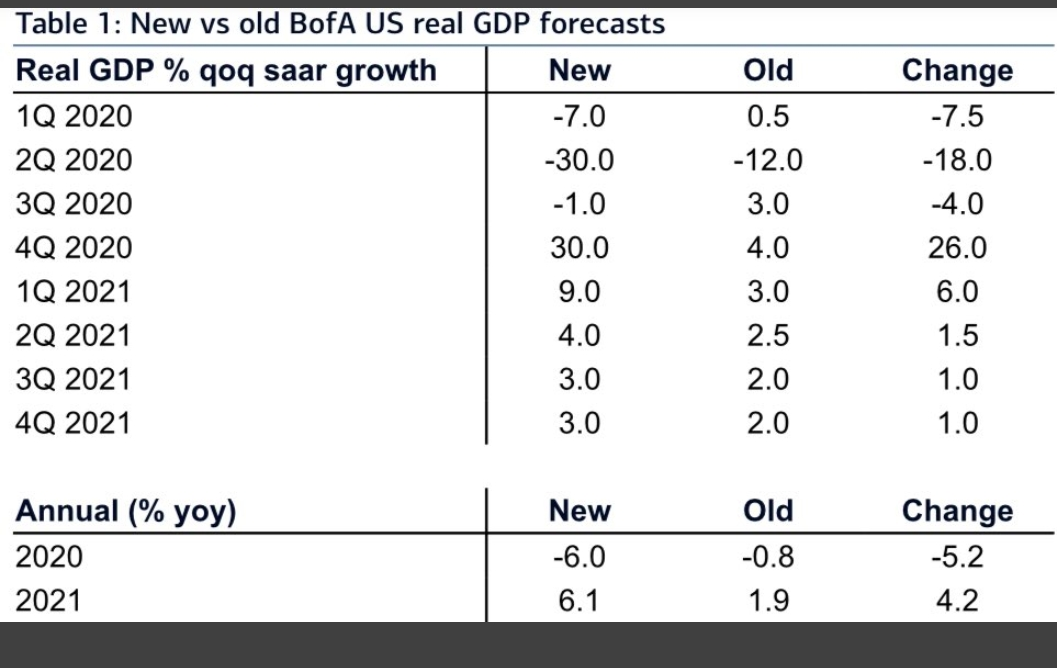

For reference though, here are Bank of America’s latest GDP forecasts, which are stunning. -30% QoQ annualized for Q2, and -6% YoY for 2020. Unbelievable if true.

If numbers like these are to be believed, then this race should be treated as a marathon, not a sprint.

I think that the real decline may lie ahead of us, not behind.

In particular, I think that commercial real estate prices are going to collapse in 2020, and this is going to be a generational opportunity to pick up high quality REITs on the cheap. ?

I think we’re getting there, but we’re not there just yet.

For those who want to seriously invest in REITs in 2020, you want to learn about REITs NOW, so that when the collapse happens, you are ready to execute your buy orders.

The REITs Masterclass that we just launched is by far the most in depth and comprehensive REITs course in Singapore right now, nothing else even comes close. It’s an online course so it’s a perfect way to make use of your time while stuck at home. ?

There’s also a launch promotion so it’s 25% off until next Sunday (12 April). Sign up now and you also get free 3 months access to the highest tier of Patron (worth $150). Truly a fantastic deal so don’t wait! Link here for more details!

Share your comments below!

Do like and follow our Facebook Page. We share great links and infographics there.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Join our Facebook Group to continue the discussion, we have a great community of people who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors. We genuinely think it’s the highest quality and best value investment course out there today!

Hi FH,

First of all great article as always. Don’t think you need any more compliments about your analytical writing style that you haven’t already heard from your other readers. Clear, concise, and straight to the point – laying out various pieces of information, assessing each of them one by one, then presenting your thesis based on the sum of those information. Hope you’re getting an increase in readership and site traffic lately. You deserve it.

About the proposed bill that impacts S-REITs – You have already seen my comments on Patreon yesterday. Utter insanity. They’ve got to pass the pain further upstream to the banks, and then take measures to help the banks tide through this. It’s easier anyway to just help the 3 banks rather than have to deal with a massive fallout of landlords getting destroyed, the sheer scale of which wouldn’t be beneficial for the tenants in the long run anyway… I mean are the tenants really saved after 6 months if the whole REIT goes insolvent after 4 months? *Facepalm*

About your macro signals and entry strategy for stocks in 2020, clearly you have put a lot of thought into this in the past week and they’re great views. I do have a few questions/points and am keen to hear your thoughts.

1) About the USD peaking being a correlation for stocks bottoming, I agree with this view. Curious to know your thoughts though on how the oil situation may impact the reliability of this signal? It’s something that really impacts USD, yet I think oil this year is really a hell of an unknown, both supply side and demand side.

2) On Signal 4, would you say the impact of a large bankruptcy is less likely to spill over to other sectors (vs the sector of the bankrupted company) than the Lehman Brothers case? Firstly, Lehman was an investment bank and their bankruptcy (together with Merril Lynch and AIG a day later) caused a huge loss of investor confidence in financial instruments as a whole. Secondly, it was also the initiating cause of the panic selloff, whereas this time the initial selloff was caused by the virus and has already came and went. Hence, I think the impact of a big bankruptcy this time would not only be of a lower order of magnitude, which I think you probably agree, but more specifically, may perhaps also be contained within the same sector. For example, a Delta Airlines and British Airlines bankruptcy within the same month would be big news, but it may not cause too significant an impact on say, FAANG stocks. It will, however, impact all the other airline stocks for sure. And if we’re already staying away from travel/hospitality for a while, and generally all companies with weak balance sheets, then wouldn’t the bankruptcies not be of a major concern to our watchlist? I may be missing something here. Curious to hear your thoughts.

3) Say we’ve triggered all 4 signals and the economy is re-opening up. What are your thoughts on a drawn out US stagflation phase creating further prolonged downside? I can’t imagine what would their unemployment rate be at that time and how long it would take for that to recover. Meanwhile, interest rates would still be at zero, and at this point the USD should be starting to weaken based on your analysis. That points to a stagflation risk. I think another watch point here could be to monitor closely the policy actions (or the reversals of them) during this recovery phase, particularly US interest rates. Throw in an election right around that time, and they can really screw this up.

Hope this wasn’t too long. I’m almost like requesting for a follow-up article. Haha.

Appreciate your time as always.

Regards,

Zach

Amazing comment Zach. Keep it coming, nothing I love more than being able to stress test my thinking (and engage) with great minds out there!

Very, very good points that you raised – all of which we will be unpacking for the rest of the year. For now, my preminary thoughts below:

1) Oil is super super tricky. Base case thinking, is that Saudis and Russia only cut if US cuts. If so, we may see a small cut come out, but this will be insufficient to offset the plunge in demand. So regardless of what happens on Monday, I think mid term we still see too much oil. So unlikely to affect the USD narrative significantly.

2) In some ways, we may be in the 1H2008 period now, where prevailing thinking is that this will be bad, but that policy action will save us all. A big bankrupcty could be the catalyst that shakes up the narrative. Viewed in this light, the fact that the bankruptcy may come from say CRE (eg. WeWork) doesnt matter, it still spills over to the rest of the economy because the narrative that the government will (or has) saved the economy is shattered. In times like this, it’s less about the actual impact, and more about the narrative and investor psychology.

Really great point you raised though. We will see if this turns out to be correct.

3) I think 2020 is deflation, that’s probably clear. 2021 onwards, 2 ways it plays out – (1) more deflation, or (2) inflation. Suspicion is that they will go with 2, because it’s the less painful option, and the quicker one. This could potentially result in a stagflation scenario like you mentioned (esp if we get that big oil cut in 2021). I have already made some moves to prepare my portfolio for such a scneario, and the closer we get to such an event, the more I will adjust asset allocation accordingly.

Amazing amazing comments. Feel free to jump in if you disagree on any point.

Hi FH,

Thanks for the response. Yeah I think bankruptcies would be interesting to watch this time round. Agree it’s about psychology and confidence rather than the actual cross-sector impact. What’s weird though is that these days the market doesn’t seem to even respond to news of 10 million jobless claims in a span of 2 weeks (I mean yes there’s the $2t in everyone’s minds but still…) Hence it’ll be really interesting to watch how the bankruptcies play out. I think it also depends on the industry as well. Most people may be more or less mentally prepared for at least one big airline going down, but agree that something like CRE or perhaps an European bank going down would have a larger, and wider, impact. Stagflation would be interesting too (and dreadful, obviously) as we go into recovery phase. I think you’re quite well positioned. I have zero Gold so for me personally it’s something to take note of.

Thanks and looking forward to your articles! Next week could be interesting, with a few major reveals on Monday, both globally and closer to home.

Regards,

Zach

Hi FH

Nice analysis there. When you say “commercial real estate prices are going to collapse in 2020” – what exactly is “commercial real estate” you are referring to? Is it retail vs office vs industrial? I can see retail being hit badly but on the latter two, not to that extent yet you reckon?

Haha actually I meant all of them. But it’s just a thesis at this stage, I could be wrong. 😉

Great read. Seems like you are a dollar bull. Have u caught Brent Johnson’s dollar Milkshake theory yet?

Yes, am familiar with Dollar Milkshake Theory. 🙂

Wow nice. So after watching will u be long equities lesser ? Or will still be finding equities to long?

For me personally I feel the dollar kurgan will win eventually now.

Haha why would I long equities less? Because USD strength?

Yeah cause of the “theory” that dollar strength will wreck havoc on the equities market.

But main impact with be global equities right? Less so of US equities.

Hi FH,

Thanks for your great analysis as always. You have mentioned that your current asset allocation is tilted towards the “safer” assets i.e. bonds, cash and gold. I share your view that the stock market should perform in line with the macro signals that you have mentioned and am also hoping to pick up REITs on the cheap.

However, seeing the strong performance of the stock market the past 2 weeks, I can’t help but feel that:

1) the virus situation has been fully priced in, and, given how governments are prepared to pull out all the stops to combat the resulting economic slowdown / any potential liquidity crunch, we can expect further stimulus as required (in other words, a full backstop by governments, whether through monetary or fiscal stimulus, or even in an extreme case, directly buying ETFs).

2) The greatest difference between now and GFC is the stability of the banks. Since banks are currently relatively stable, there is unlikely to be any systemic risk and resulting contagion to stock markets, even though we may still see some corporate bankruptcies

3) this bear market appears to be functioning on a “compressed” timeline, and stocks could already have entered an accumulation phase

Given the above, the current situation where we can pick up stocks on a discount (rather than at “lelong” prices) seems to already be the best we can get. Do you see a case for more aggressive deployment of funds into stocks / REITs over the next few months (or even weeks?), rather than a gradual shift over the course of 2020 and 2021?

Fantastic comments. All of which are perfectly valid.

If you are a Patron member, you will have full access to my personal portfolio – which should give you a better idea of how I am positioned : https://www.patreon.com/financialhorse

Long story short, despite the tilt towards bond and cash, I still have big gold and equity/REIT positions that will benefit if governments turn on the liquidity spigot and this causes stocks to rally to new ATHs.

My current base case thinking is that Phase I panic is over, this could see a short term rally, but eventually Phase II will set in when the insolvencies start to appear. The virus situation is also likely to see restricted economic activity well into Q3 – which caps economic growth. The current facts are still in line with my base case, so I haven’t made changes to my buying plan.

I do recognise that I can be wrong, which is why I am maintaining the equity positions, and continuing to buy into this market (added last week).

Ultimately though, you need to make the call for yourself. Decide what is the right tilt in your allocation, to be able to capture the best returns going forward. How is your portfolio positioned if your thesis is correct. What if you are wrong? Which do you think is more likely, and which would you want to bet on?

Cheers! 🙂

There are clearly investment opportunities but it’s hard to know where is likely to provide long term value. I agree with your thesis about real estate collapsing, but I am more skeptical about its recovery.

Bricks and mortar retail is dying (if not already dead) in large parts of the US and UK, where the online economy is some years ahead of Singapore’s, though it is growing here and will certainly catch up eventually. I walk around malls and can already see lack of occupancy in all but the most premium locations like Orchard. Long term the amount of mall space is unsustainable. Having said that, malls play a bigger role in Singapore’s social life than in the West. Personally I wouldn’t touch any physical retail at all.

Forcing companies to telecommute is likely have residual effects. We could be witnessing a generational shift towards remote working. Tech companies are already ahead in this regard, but more traditional companies will catch up when they realise there are huge savings to be had on office footprint. Once you have a remote workforce and the required tooling to support it, offshoring becomes an easier step to contemplate also. My team has been fully remote since the start of February and it’s unlikely we will ever return to the status quo ante.

Manufacturing is an interesting case counterpoint though. The deglobalisation that was already underway and has been accelerated by COVID19, coupled with advances in robotics, could see outsourced supply chains brought back onshore as cost benefits fall and risks rise.

Healthcare real estate could also be a promising area post COVID19. Western populations are likely to demand significant investment in health provision when the dust settles.

What are your thoughts FinancialHorse?

Really good comments.

My thinking though, is that real estate is ultimately a very local business. It’s not accurate to look at brick and mortar in US/UK dying, and making the same generalisation for Singapore. Ecommerce in US is way more developed than Singapore, the country is way bigger, shopper habits are different, and the mall density per capita is almost double that of Singapore. I agree that I would never touch retail malls in US/UK, but in Singapore’s context, I can still see Vivocity / Plaza Singapura remaining relevant and bustling 10 years from now. So for real estate – focus on the property. Well located malls with great build quality will always remain relevant, at least in my books.

I agree on telecommuting. I think that could be bearish for office spaces, especially Grade B CBD offices. But Grade A offices in CBD – every top FI will still need to maintain that space for front office, simpy for the prestige factor.

So my thinking now, is that while CRE will probably drop in 2020 – there’s lots of opportunities for the enterprising investor to go in and pick up the high quality real estate on the cheap. It MUST be active investing though, because passive will get exposure to those poor quality real estate like you mentioned.

Thank you, interesting thoughts as always..

Inspired by your comments FinancialHorse I had a scan through some of the bigger REITs. There was some obvious value around March 23rd, but many have bounced back significantly. Keppel DC REIT is basically unaffected (as you might expect for the sector it focuses on). Do you think at current prices trusts like Mapletree MCT, MLT, MINT are offering value for investors with no exposure to REITs?

Haha to provide some colour, I bought a couple of the Mapletree REITs last Friday when the market prices looked great to me. I’m buying in with a view to averaging in over the course of 2020 though.

What to buy, and when to buy, is ultimately a personal decision. It’s very hard to advise without knowing your full situation. I liked the prices I was seeing last Friday, so I bought some. I like them less at this weeks prices, so I just waited.

Personally though, I suspect that we will see more interesting prices later this year, but I could be wrong on this (hence the decision to buy last week).

Hope that this helps provide some colour into my decision making. Will share more thoughts on REITs this weekend – so do check out that article. 🙂

Dear FH,

Thanks for the in-depth analysis on possible scenarios that could play out over the weeks. It seems that FED has endless bullets, injecting liquidity to wherever deemed necessary. US major indices kept ticking higher. When productivity does not increase (for obvious reason e.g. social distancing & lockdown put in place), would this not point to massive inflation? As markets are forward-looking, companies’s earning will drop precipitously in coming quarters but things will eventually return to normalcy (hopefully as soon as possible), are there plenty of reasons for market to head further south? Would banks & those too-big-to-fail conglomerates ever face risks of bankruptcy given FED’s willingness and aggressiveness to step in ‘whenever necessary’? i.e. Are there anything that are beyond FED’s capability?

Stay safe & healthy!

Haha, yes I see stagflation as a possibility. Just shared some thoughts in today’s article, I think the concluding section will address your query. And yes, Feds ability to print is technically unlimited. 😉