I was reading this old interview transcript with Stanley Druckenmiller recently.

In the interview, Stanley was sharing the stuff that he learnt from his mentor. Once of which was this:

You don’t invest in a stock for its earnings today, you invest in a stock for its earnings 18 months from now.

He also went on to say that investing in a stock for its earnings today is about the quickest way to lose a lot of money in markets.

But anyway, this quote really got me thinking.

Let’s fast forward 18 months. Let’s jump to end 2021. What will REIT earnings look like then, and consequently, what will REIT prices look like?

Now I do get that in this kind of markets, earnings don’t necessarily translate into REIT prices. Short term, it’s still dominated by liquidity and funds flow. But let’s do this analysis step by step. We’ll start with earnings, then we’ll look at liquidity and funds flow, and then we’ll put it all together to assemble of framework for how REIT prices may trade going forward.

*Reminder* The GE Promo for the REITs MasterClass ends tomorrow. Sign up now to get 25% off the normal price, and you also get free 3 months access to the highest tier of Patron (worth $150).

Find out more about the REITs MasterClass here.

Basics: Where are we in terms of REIT earnings?

We’ll focus exclusively on S-REITs with Singapore properties in this article. Property is a local business, so property investing in Singapore, is completely different from property investing in Hong Kong for example.

COVID-19 (Temporary Measures) (Amendment) Bill

The really big thing to know about Singapore is the COVID-19 (Temporary Measures) (Amendment) Bill, passed by Parliament in March.

There are 2 big parts to this bill:

- Rental Waiver

- Preventing Landlord from evicting tenants for unpaid rent

Rental Waiver

In other words – free rent.

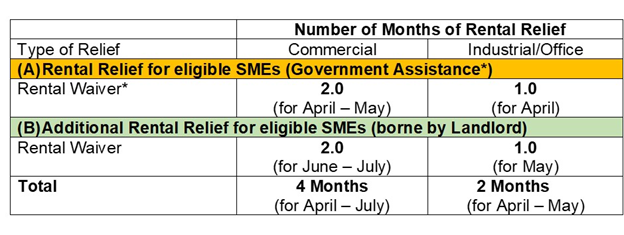

The rental waivers given are set out below:

Basically, if:

- You are an SME – You get 2 months free rent for commercial (retail) leases, and you get 1 months free rent for industrial or office leases.

- You are an “Eligible” SME, you get 4 months free rent for commercial (retail) leases, and you get 2 months free rent for industrial or office leases.

Half of the waiver is borne by the landlord, the other half by the government (via property tax rebate).

In terms of definitions:

- SME is one with ≤$100 million in annual revenue in the Financial Year ending 2018 at the entity level.

- “Eligible” SME is one who:

- Has suffered ≥ 35% drop in average monthly revenue on an outlet level from April to May 2020, compared to April to May 2019; and

- Are SMEs at the group level (≤$100 million turnover based on the latest available accounts).

Preventing Landlord from evicting tenants

The second part of the bill, basically allows tenants to not pay rent for a 6 months period.

If tenants serve a “Notification for Relief” on their landlord, the landlord will be prevented from:

- Terminating the lease on the basis of non-payment of rent.

- Re-entering the premises.

- Suing the tenant or bringing insolvency proceedings.

In simple English, if the tenant cannot pay rent, they can serve a notice on their landlord, and the landlord cannot evict them or sue for rent.

This will last until 19 October 2019, unless the government chooses to extend it.

The key different here though, is that while the tenant can choose to not pay rent up till 19 October 2020, the rent doesn’t get waived. It’s still due and payable after 19 October.

So if the tenant owes the landlord 3 months rent during this COVID period, that 3 months rent will still be payable after 19 October 2020.

Which is funny because if the tenant were truly in financial difficulty, it’s hard to see why that would change by October. But yeah, I get that this gives the tenant time to explore alternatives, and gives them some breathing space.

REIT Tax Transparency Exemption

The other notable change, is on the IRAS tax transparency treatment.

Normally, a REIT is required to pay out 90% of its distributable income on a yearly basis to qualify for tax transparency.

The recent change from IRAS, says that REITs have until 2021 to make this payment, to qualify for tax transparency in 2020.

In simple English – this means that REITs can choose to retain their earnings in 2020 instead of paying it out as distributions to unitholders. So they can save it for working capital requirements, until the end of 2021 – when 2020’s losses have been tabulated, and then they pay out the minimum to qualify for tax transparency.

This is actually good because frankly, nobody knows what the losses this year will look like.

This helps REITs to maintain a capital buffer against such losses, reducing refinancing risk.

What is the impact of these legislation?

COVID19 is a strange crisis because in a way, everything has simply been put on “hold”.

If tenants get free rent, and landlords are unable to evict during this period, then the entire real estate market is in a way just put on hold, so we don’t have true price discovery for rent and property prices.

The market is just frozen at where it was in Jan 2020.

Which is why I wrote in a previous article, I think that we only get to see what the market really looks like maybe in late Q3 or Q4.

In August, all the rent waivers fall away, and tenants need to pay full rent again. In October, all the rent that was due and payable during this COVID would become payable, and failure to pay could lead to eviction. At the same time, a lot of the short term stimulus from the government (eg. payment of staff salaries) will start to fall away.

Once that happens, we’ll start to see what the “natural” rental rates post COVID are like, and how they fare on their own without government support.

We’ll have weaker tenants going bankrupt, we’ll have tenants renegotiating their leases, we’ll have leases that come due and that need to be retenanted. This will give us an idea of what rents look like in the post COVID world.

Personally, I find it hard to see retail or office rents continuing at the pre-COVID levels. It just doesn’t make sense anymore, to be paying the same amounts as pre-COVID. So I do expect we’ll see drops in market rents, the only question is how much.

More Government Stimulus?

I guess you could argue that the government can simply pass a new round of legislation to protect tenants.

That’s tricky though.

Every action has a consequence, and if you prolong the natural process of “price discovery”, it will perpetuate inefficiencies in the market, by allowing weak companies to survive. We may end up with a Japan style economy where the zombie companies just keep going forever.

But more importantly, landlords have already been deprived of 2 months of rent. Any more, and the landlords themselves will start running into trouble.

And if the landlords start running into trouble, the banks start running into trouble too.

So yes – Government stimulus is definitely possible, but there will be consequences.

Personally, I doubt we’ll see anything as drastic as we saw the past few months like rent waivers. If anything, it will be more of structural changes to the rental market like shifting the balance of power, improving transparency in the market etc. But we’ll see.

What does the world look like 18 months from now?

Try as I might, I genuinely have no idea what the world will look like 18 months from now, in late 2021.

It looks like we’ll have a vaccine by then, so perhaps most international air travel can be resumed.

By let’s say optimistically, we get a vaccine in Q1 2021. By the time we get widespread production and immunization, we’re maybe in Q2 or Q3 2021.

By such time, how much of the current economic damage and unemployment would have turned permanent? Once it’s permanent, it doesn’t come back so quickly even if all COVID restrictions are lifted, so that will be a permanent drag on the economy.

Again, tough to say for certain, because much of it depends on government stimulus, and how well COVID is handled in each country.

Earnings impact on S-REITs?

With real estate, you don’t just look at demand, you need to look at supply too.

This cycle though, the supply side has been fairly controlled. We don’t have the massive supply booms that we saw in some of the earlier cycles.

With supply being relatively constant, the key determinant for price will be the demand.

And my personal view, is that the impact on demand (and consequently price) will be:

- Industrial / logistics – Close to current levels, possibly higher

- Data Center – Up (contrained by tight supply as well)

- Retail – Down

- Office – Down

- Hospitality – Down

Feel free to disagree with me on this though, I would love to hear your thoughts in the comments below.

Macro Perspective – Liquidity and Funds Flow

Long story short, there’s just a lot of uncertainty over earnings. No landlord can tell you for certain how much he will be able to lease out the same space 1 year from now. But my personal take is that with the exception of industrial spaces and data centers, it will probably be lower than where it was pre-COVID.

But earnings is just half the story. Because REITs are capital markets instruments, they come with all the quirks of being listed – which is liquidity and funds flow.

Like we saw in April / May 2020, it doesn’t matter if underlying earnings are destroyed, stocks like airlines and cruise operators can still soar if there are more buyers than sellers.

Now I’ve written a lot of articles on this in the past (check out this one from last week for more info), and I think the only practical solution to the COVID crisis is that governments and central banks around the world are just going to inject record amounts of stimulus into the economy.

I truly do not see another way out.

They may deliberate and hesitate (and if they do markets will sell off), but eventually, the only outcome that makes sense here is to flood the economy with liquidity, and hope that is enough to turn things around.

All that liquidity needs a home, and with cash yielding close to 0% these days (the latest SSB has a 1 year yield of 0.27%, how ridiculous is that?), cash or short term bonds are not a good option. So I do expect that eventually all this liquidity is going to find its way into the only assets with decent returns – stocks, REITs, maybe gold.

And never underestimate the power of liquidity to drive capital markets.

Which may give us a strange scenario where REIT earnings drop, but REIT prices go up.

Strange times we live in indeed.

Buy or Sell S-REITs?

For a lot of the blue chip REITs on my personal watchlist, they’re at a price where I don’t think they’re a compelling buy, but neither are they a compelling sell either. They’re just… there.

Take Mapletree Commercial Trust for example. If it drops to $1.5 in its March/April lows, of course I will add. I bought at that price in April when news of the lockdown released, and I would easily buy it again if it goes back there. At that kind of prices, even without all the short term rent, you’re already getting a good price on the underlying real estate.

If it goes up to $2.4 or $2.5 to revisit all time highs, there could be a good argument to sell and lock in short term profits. At such prices, the only way to justify it will be via liquidity, in which case the key will be to watch Fed and central bank movements for timing on the sell decision.

But at it’s current price of $1.9+, the buy or sell decision isn’t that obvious either way.

REITs Investing

Now for obvious reasons, this article cannot cover everything you need to know to invest in REITs, and it only touches on a small portion.

If you want to invest successfully in REITs over the course of a lifetime, you really do need a complete framework to investing.

That’s exactly what the REITs MasterClass is intended to achieve, and it teaches you:

- When is the best time to invest in REITs? And when is the time you should be selling REITs?

- How to make money from real estate? How to identify the best properties to own for a lifetime?

- How does real estate and REIT fit into your portfolio? What is the best percentage of REITs to have in your asset allocation?

- What can we learn from REITs from the US? What does this mean for S-REITs in the next 5 years?

- Unique risks you must look out for before buying REITs

- Growth drivers a REIT must have so you can earn increasing distribution and capital gains every year

- The best type of sponsors and managers a REIT must have to protect your capital and make you money

- The financial and operational metrics a REIT must pass

- How to value a REIT accurately using practitioner level valuation techniques

If you’re serious about REITs Investing, definitely check it out, especially now that the GE promo is on (ends tomorrow).

Sign up now to get 25% off the normal price, and you also get free 3 months access to the highest tier of Patron (worth $150).

Find out more about the REITs MasterClass here.

Closing Thoughts

I think the next 3 to 6 months will give us a lot more clarity into the post COVID earnings impact.

The Q4 earnings will give us some idea of the full earnings impact without government stimulus, but that will only be out in 2021, which is far too late to be of any use to us.

So instead of looking at REITs earnings reports, I think we may need to look at the high frequency indicators on the ground. Find out what kind of prices new commercial leases are being signed at. Walk around a mall and check out occupancy rates. Talk to shop owners to see how their business is doing. Look at footfall at your favourite restaurants.

If earnings rebound stronger than expected, REIT prices may really fly with all the stimulus and liquidity tailwinds. Don’t forget that pre-COVID, Fed Funds rates were in the 1.5% range, and this has been slashed all the way to 0%, which traditionally is a powerful boost for REIT prices.

And don’t forget the impact of liquidity stimulus as well. The Feds have paused their stimulus for now, but if things take a turn for the worse in US, they’ll be forced to reopen the spigots, and in this market, you don’t want to be on the wrong side of the Feds.

Whatever the case, I’ll be sharing on the COVID crisis every weekend on Financial Horse, without fail. So if you haven’t already signed up for our weekly newsletter, please do!

[optin-monster-shortcode id=”id6w866hteea8oefqnvc”]

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi, I think there is a typo error in terms of the year.

“This will last until 19 October 2019, unless the government chooses to extend it.”

Aside, thanks for the great post. Two thumbs up.

Haha you are right, I meant to refer to 2020!