Unless you’ve been living under a rock the past few months, you’ve probably heard about the Hyflux saga. With stories about how retirees placed their entire life savings in Hyflux perpetuals only to watch it go up in smoke, it’s hard to miss this one.

Basics: What happened?

If you don’t know anything about Hyflux, I suggest that you start by reading Olivia Lum’s response to questions posed by SIAS, which was actually pretty informative.

Hyflux was originally a water solutions provider (water filtration). Over time, they evolved to provide more integrated solutions, to cover water, power and waste management needs. Where it all went wrong, was the Tuasspring Integrated Water and Power Project in Singapore. Hyflux was named preferred bidder in 2011, based on their proposal to build a desalination plant with an onsite power plant at Tuasspring. The original thinking was that “with energy cost being the largest cost component of desalination, this integrated solution which allowed the project to take advantage of the energy cost savings from the captive power plant, and apply the same cost savings to the desalination production, enabled synergy and operational efficiency”.

In other words, this plant use the electricity to power the desalination, and it can sell the water, and also the excess electricity. A win win right? Unfortunately, the rest is history, and I quote from Hyflux (emphasis mine):

“it is important to highlight that when the Tuaspring project was first awarded in 2011, the outlook for the Singapore power market was very favorable. The Tuaspring power plant was projected to turn in profits from day one. At that time, new power generation plants were planned to support the country’s projected electricity demand with a reserve margin of 30%. Today, however, due to oversupply of gas in the market, the projection by Electricity Market Authority (EMA) in their Singapore Electricity Market Outlook 2017 showed an increase in reserve margin to 80% in 2018. By way of illustration, the average wholesale electricity price has dropped from about SGD220 per MWh in 2011 when the Tuaspring project was awarded to an average of SGD81 per MWh in 2017, resulting in significant losses from electricity generation.

The operating losses of Tuaspring drove Hyflux to record its first full year of loss in 2017. When losses were also reported in its first quarter 2018 results released on 9 May 2018, certain financiers expressed concerns over their ability to continue with existing credit exposures to the Group. This, coupled with the uncertainty of Tuaspring divestment or entry of a strategic investor, raised a significant spectre of an upcoming liquidity crunch. Accordingly, subsequent to discussions with its legal and financial advisors, the Hyflux Board was advised to proactively take steps to make an application for a moratorium order, which is where events stand today.”

In other words, what went wrong was that Hyflux did their internal projections based on electricity prices in 2011, and they had bet the company on electricity prices being close to those levels. Due to the crash in oil prices in 2015, electricity prices fell drastically, and this affected the earnings from the plant after it went operational. Because of large amounts of debt Hyflux took on to finance the construction, it eventually reached a tipping point where they were unable to repay existing debt (or refinance to repay debt), and the liquidity crunch is where we are now.

Unfortunately, Hyflux offered preference shares to retail investors in 2011, and perpetual securities in 2016, both at 6% yields. That retail element, is what made this case so big, with stories of retirees placing their life savings into Hyflux securities and losing it all.

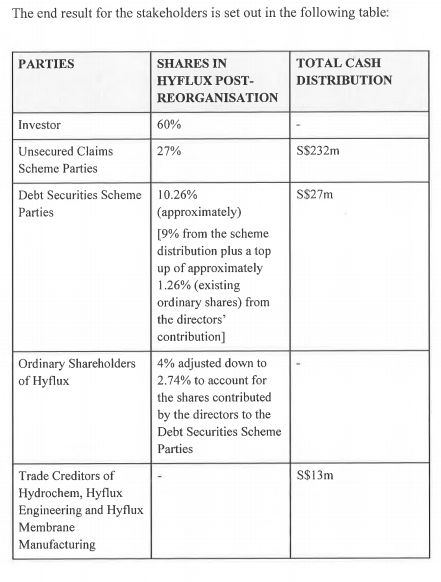

Under the proposed restructuring plan: Holders of Hyflux perpetual securities and preference shares, who are owed $900 million, will receive a total of $27 million in cash and a 10.26 per cent of the company under a long-awaited restructuring plan filed by the embattled water treatment firm with the High Court and posted on the Singapore Exchange website early on Saturday morning (Feb 16).

With S$27 million of cash to cover S$900 million in obligations, you’re looking at 3 cents on the dollar recovery if you’re a perpetual / preference security holder. In other words, for every S$10,000 you invested, you get S$300 back in cash. The rest comes in the form of shares (which is hard to value, but we’ll try later). Any way you look at this, retail investors are going to lose big.

Full disclosure, I am not a perpetual/preference shares holder, but certain family members are. This article is a simple sharing of my personal thoughts, and should not be construed as investment or legal advice. Please also note the disclaimer below:

The information contained in this article has not been independently verified. No representation or warranty expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this article. Neither Financial Horse or any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this article or its contents or otherwise arising in connection with this presentation. If you are in doubt as to the action you should take, please contact your financial advisor, stock broker, or legal advisor.

3 Lessons learnt from Hyflux

1. Government will not bail it out even if its Singapore Inc

Let’s face it. We can say all we want about how Hyflux has been cash flow negative since 2009, but nobody bought into this company based on their financials. Hyflux is Singapore’s equivalent of Tesla. Sure, the business model may not be sustainable if you really think about it, and the cash burn is ludicrous, why does that matter when you have the Singapore equivalent of Elon Musk, our very own Olivia Lum.

![]()

With Olivia Lum appearing on the Forbes cover, being named the EY entrepreneur of the year, appearing as a NMP, Olivia Lum seemed like the quintessential Singapore success story, of how a hard working young woman built an empire out of nothing more than grit and sheer determination.

From the outside, Hyflux would have seemed like a sure thing not only because of the Elon Musk (Olivia Lum) connection, but also because they were in the water industry, which is a strategic sector for the Singapore government (we are an island), and projects such as Tuasspring have key strategic elements. It’s easy to see now what went wrong, but if you backtrack to 2011, it would be a lot harder to predict the problems to come.

What this saga has shown though, is that Temasek, and the Singapore government, is prepared to let big name Singapore homegrown companies fail, even if they are in strategic sectors. The way I see it, just because the sector is strategic, does not mean individual companies within that sector are, and unless you’re a systematically important institution like DBS, UOB or OCBC, don’t count on a government bailout.

There’s also the issue of a moral hazard. If Temasek, or a Temasek linked entity steps in to bail Hyflux out, what kind of signal is this sending to the domestic market? Will future investors automatically expect the government to backstop any failing issuer, simply because they are part of Singapore Inc? I see a lot of parallels between this default, and the China government allowing certain state linked bond issuers to default on their debt obligations.

Key takeaway though, is that going forward, don’t expect Temasek / Government to bail out your bonds, simply because you bought into a big Singapore Inc Company. You do need to take a look at the financials and business model.

2. Cash is king

There’s a saying about cash by Warren Buffett:

“Cash, though, is to a business as oxygen is to an individual: never thought about when it is present, the only thing in mind when it is absent. When bills come due, only cash is legal tender. Don’t leave home without it.”

In other words, cash is king.

You can think of it like building a series of properties. Imagine that you build 3 properties and sold them all in 2011. You booked a nice healthy profit, to be recognised over the next 6 or 7 years, due to accounting practices.

You then take all the cash that you have from the sale, and put it into the construction of a big, swanky new building.

During the construction phase, everything looks ok from a profit angle because you’re still recognising the gain from your sale in 2011. In reality though, all of your free cash is deployed in the construction of the building. In fact, you also took up additional debt to finance the construction. But because dividends are payable out of profits (not cashflow), you’re still able to pay out dividends.

However, at this point you’re cash flow negative, because all of your cash (and new cash) is going into the construction of the building, and the building isn’t generating money yet. You’re betting that once the building is constructed, you’ll be able to lease it out to generate operating income, or you can sell the entire building, to be used to repay the debt you borrowed. Unfortunately, once the building is constructed, the operating income is poor (electricity prices fell), and you can’t sell the building (no buyers). At the same time, you still need to repay all the debt you had borrowed, or at least refinance the loans. By this time everybody knows you’re in trouble, and nobody wants to lend to you. And you have a classic liquidity crunch.

It’s a very simplistic analysis of what happened to Hyflux, but the crux of the issue here is no different from that faced by property developers. When you take on large amounts of debt to finance a big project, you’re basically betting your company on that project. If things don’t turn out as you expect, you really need the cash on hand, and a healthy balance sheet, to tide through the storm until the market recovers.

So yes, Buffett is right here, cash is king. When you need to repay debt to a bank, you can’t pay them with a power plant, you can only pay them with cash.

3. Watch the yields

I’ve always believed that the easiest way to gauge the risk you are taking on with a fixed income product (bonds, perpetuals, preference shares), is to look at the yield you are receiving. Anything above 5% would set my alarm bells ringing, and I would want to take a deep dive into understanding the business model and financials.

I know that it’s easy to say such things like this after it’s happened, but if you apply this rule going forward, it may just help you avoid a future Hyflux.

What can investors do?

If you are an existing investor in Hyflux, what can you do? If you’re an equity investor (you hold ordinary shares), I think it’s pretty simple, you just keep holding your shares, and hope for the best. Shareholders rank absolute last in an insolvency situation, so your best bet is for the restructuring to go through and for shares to resume trading again.

If you’re a preference shares (2011) or perpetual securities (2016) holder though, it’s a bit more tricky. There are 3 possible courses of action: (1) take legal action, (2) vote yes, (3) vote no.

1. Take legal action

Very simply, legal remedies include bringing a claim for unfair preference, transaction at an undervalue, insolvent trading or fraudulent trading.

Unfortunately, none of the above are easy to prove in court. If you go down this route, you need to (1) foot the legal bill which is likely to run into millions, (2) spend years digging up the information necessary to present a case, filing in court, going through appears etc. And even if you go through all this, and you eventually win the lawsuit, the amount recovered goes to Hyflux, and is split among all creditors in an insolvency. Long story short, I wouldn’t be optimistic on legal action, unless you have compelling evidence of wrongdoing by the company officers. Otherwise, it’s just going to drag you down.

So that leaves you with the current Scheme of Arrangement to restructure the company. As a preference shares/perpetual securities holder, you get to vote to approve or reject the scheme. All classes of creditors must approve the scheme for it to proceed. Preference shares/perpetual securities rank in the same class, so Hyflux needs 75% approval from this class to proceed.

2. Vote yes

If you vote yes, and the restructuring proceeds, recovery amounts are not fantastic, to put it mildly.

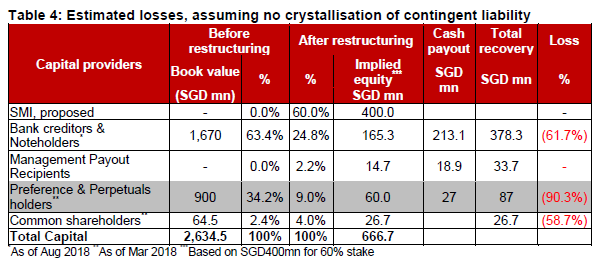

As mentioned above, the cash amount works out to 3 cents on the dollar. There’s an additional 10.26% of Hyflux shares to be redistributed, but unfortunately, nobody knows how much Hyflux will be worth post-reorg. If we take a simplistic view that SMI (the new investor) is coming in with S$400 million for a 60% stake, that would value the restructured Hyflux at S$666.7 million. A 10.26% stake would then be worth S$68.4 million, which works out to 7.6 cents on the dollar.

In other words, based on this rough calculation, if you vote yes and restructuring goes ahead, you get back about 10.6 cents on the dollar, of which 3 cents is cash. So for every S$10,000 invested, you get back S$300 in cash, and S$760 in shares. The share component is a big if though, because no one really knows what the company will be worth post-reorganisation. There’s a good chance that when shares resume trading, there’s a huge rush to the exit and share price collapses, and it never recovers for years, which means that the 7.6 cents on the dollar in shares that you received, could be worth a lot less in reality.

3. Vote no

The other option, is to go to the creditors meeting, and vote no. Under this scenario, you’re so outraged that Preference and Perpetual holders are getting 10 cents on the dollar when senior creditors are getting 39 cents on the dollar, that you’re prepared to risk getting nothing back at all, in the hopes of forcing a new deal.

Let’s assume that you get enough people on your side to support this plan, such that Hyflux cannot get the 75% majority from the junior creditors required to proceed. Under this scenario, there are 2 possibilities.

Firstly, is that Hyflux, SMI, and senior creditors recognise that they need to consider Preference and Perpetual holders more fairly. They come back with a proposed new plan that gives more money to the junior creditors (Preference and Perpetual holders). This gets approved, and retail investors are happy. This is a win.

The other possibility, is that SMI balks at the new terms. They pull their support for Hyflux. Hyflux goes into insolvency. Because Preference and Perpetual holders rank second last in an insolvency, retail investors get almost nothing back in an insolvency. This is a lose.

So yes, this is definitely the high risk-high reward kind of play. How you decide to vote, will say a lot about the kind of investor you are (and also how much you have invested). I’m pretty sure there are people out there who will vote no as a matter of principle, and risk taking down the entire company simply because they are outraged. At the same time, there are going to be investors who think that a 10 cents on the dollar recovery is still better than nothing, so they’re going to vote yes.

What is fair here?

OCBC did a fantastic report where they tabulated the estimated losses faced by each class of creditors. Based on this, it seems like the senior creditors (banks and noteholders), will take a much lower loss than preference and perpetual securities – they get about 40 cents on the dollar.

Of course, senior creditors rank higher in an insolvency situation anyway, so I get that they would get more money back, but the key question here is: do the senior creditors deserve so much more? There’s no real prefedence to fall back on here, because as OCBC says:

…though fairness is difficult to judge given lack of precedence: However, it is hard to judge whether the gap in recoveries are consistent with the relative bargaining power. There are no precedent cases or standards in the SGD bond market for us to say whether or not the difference in recoveries is within market norms. It is also ultimately subjective and a matter for the senior and junior creditors to negotiate in order to get the restructuring to pass. On one hand, senior unsecured creditors will say it is fair because by right the junior creditors should get nothing (in liquidation). On the other hand, it will likely not be seen as fair for the junior creditors as they suffer a very significant quantum of losses. In any event, this is the first time in the SGD bond market that we are seeing a situation where there are a myriad class of creditors, in terms of seniority of ranking and investor profile with a large gap in bargaining power (in part due to large number of investors). Past restructurings usually involved fewer stakeholders (i.e. just bank lenders and bondholders), which are more similar in ranking and homogenous within their groups. The key difference between the two was the ability and willingness of bank lenders to provide short term liquidity (that helps companies continue as going concerns) at the expense of bond holders. In HYF’s case, SMI is the expected liquidity provider, rather than bank lenders.

In other words, whether this is fair, depends a lot on the facts. There’s no easy precedence to fall back on here, and it’s really for the senior and junior creditors to negotiate. Perhaps SIAS and the townhall sessions can come to some fruition here.

What would I do?

For the record, I agree with OCBC when they say (emphasis mine):

- For senior unsecured creditors, the preliminary terms are hard to reject given that recoveries are significantly higher than liquidation with the potential for further upside.

- Conversely for junior creditors (ie: perpetual security and preference share holders), the terms are hard to accept given the substantial write-down of principal and equitisation of claims.

Based on OCBC’s estimates, in an insolvency situation, senior creditors are looking at around 24.7 cents on the dollar recovery, whereas they’re getting 39 cents on the dollar under this restructuring.

The easiest way out is probably to negotiate an outcome with the Senior Creditors, because in an insolvency everyone is worse off. Such negotiations are tricky to handle though. There’s always a chance that the Senior Creditors call your bluff, and bet that you wouldn’t want to take your chances in an insolvency too. So it may come down to a Brexit style situation. Do you YOLO vote no and have a hard brexit, and risk everything go to shit, just for the hope that Senior Creditors (ie the EU) will give in?

Of course, there’s no right or wrong answer here, and the decision you make, has to be yours and yours only. Please don’t make your decision based on what I would do, because I don’t have skin in the game.

When the finalised terms come out, we’ll have more information on the restructuring. Depending on the level of interest, I’ll see if I can do an update post then (leave a comment below if you think this would be helpful). Would love to hear thoughts from other readers and investors out there. Do you think that this proposed restructuring plan is fair for retail investors? Are you inclined to vote yes or no in favour of the restructuring plan?

Update: Following this article, a slightly amended scheme has been proposed for retail investors, and I have covered it in a more recent article. Read it here for more info.

It also turns out there is a petition making its way around, that petitions the Singapore Government to buy out TuasSpring and save Hyflux. It’s basically a psuedo “bailout”, so do check it out if you’re keen. Link is here.

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Excellent analysis and great numbers crunching. I am a Perp & Pref holders and would like to share from an emotional perspective that retail junior creditors felt a huge sense of injustice and mis-placed trust :

1) Retail investors are in the main not financial savvy and relied heavily on government linked agencies for endorsements (even if implied) such as CPF, SRS approved.

2) Hyflux final year results will not be released until June 2019, while voting will be called on 5 April. Hence, will be Voting Blind.

3) 3% cash is insignificant, irrespective of the capital principle. If $1000 investment is lost and is painful, would losing $970 make it any less painful? If I had invested my entire retirement saving of $100,000, could getting back $3000 pay for my living expenses for the next 10 years of my life ?

4) It is difficult to take the 7% shares seriously as the share could remain depressed and nothing could stop SMI to take the company private at cheap valuation.

After all, we are all human and are emotional creature.

Thank you for taking time to read.

Thanks for sharing your thoughts. I too, agree that the 3 cents recovery is low. Let’s hope that they provide more up to date numbers in the upcoming documents. As at right now, we don’t even have information on the latest financials.

Very good write up…

Thanks, hope it has been helpful!

Look like a “daylight robbery” proposal where the rich get richer. Creditable owners or shareholders (exist or new) should bear full responsibility of any debt owned. A “robinhood” proposal will target to offer capital protection by looking forward. Since Hyflux aimed to be profitable from year one, proposal should target to pay back progressively. Ie. Should propose to cut interest rate proportionally depending on obligation and aim to fully repay capital eventually as a responsible owner even if it takes 10 years or longer. It will not be difficult for a glc to counter propose as the deal is a great lost of precious assets to “foreigners”. Is Singapore being “invaded”? Just my two cents feeling.

Thanks for sharing your thoughts!

Thanks for your analysis. The one thing I would like to contest is the parallel drawn between Olivia Lum and Elon Musk – the latter is changing the world and will further change the world (with Tesla, Solar City, Space X, Boring Company) and Olivia is only invested in the water desalination/utilities space in some parts of the world. Olivia, for all her commendable efforts will not change even the desalination/utilities industry, mucch less Singapore, and even less the world. Musk has catalysed both autonomous driving and the electric vehicle technology space affecting every single human being on the planet. If 2019 is the tipping point for electric cars with Hyundai, Kia, Daimler, Audi, BMW, Porsche in the electric car space – its because Tesla has moved and pushed forward for 10 years. Musk has revolutionised the technology and economics of space shutting – reusing rockets and dramatically reducing the costs of space travel for the future of humanity. In 100 years, there’s a fair chance that we will remember Musk for his engineering ambitions. You can hardly suggest one can do the same for Olivia. So please, a sense of perspective please.

Haha thanks for the comment. I totally get where you’re coming from. Let’s not mention Elon Musk and Olivia Lum in the same sentence then. 😉

Thanks FH for the insightful post. I lived under a rock and learned a lot from you 🙂

No problem, glad that it has been helpful.

Great write. Yes, I will vote no.

Good luck! I do hope that retail investors eventually get more back than what is currently proposed. The current recovery is pretty pathetic, to put it mildly.

I am holding less than 10 lots of Pref share. Will it make a difference if I don’t attend the voting. I will vote No if need to. Thank you.

-Edited-

Please ignore my original comment. As the reader below commented, every vote counts due to the way Scheme of Arrangements work. 🙂

Hello FH,

In relation to this particular response, I beg to differ. My personal opinion is that – Every single vote counts in a scheme of arrangement, regardless of the size of the stake held by the stakeholder.

Based on my layman understanding, the scheme must be approved by (1) majority in number of each class of creditors AND (2) at least 75% in value of each class of creditors. Both conditions 1 and 2 must be met. The vote of even the smallest investors may make a difference for condition (1). For simple illustrative purposes, if 100 retail investors (holders of pref shares/PCS) vote on the scheme and 50 of them vote NO, the scheme will NOT be approved. At least 51 of the 100 who voted (ie. “majority”) must have voted YES in order for condition (1) to be met. The size of the stake held does not matter when computing the condition (1) threshold.

Further, for retail investors who are unable to attend the scheme meeting for whatever reasons, there is always the proxy vote avenue. All they need to do is complete the proxy form (indicate FOR or AGAINST vote – just like typical AGM and EGM proxy forms) and post the form via mail. Proxy form votes are as good as votes in person last I heard.

Thank you for the write-up. 🙂

Hi,

Thanks for the correction, you are absolutely right. I had forgotten about the first condition. Yes, in that case all retail investors should at least fill up their proxy form to indicate their votes.

Am really heartened by the great comments and engagement (including yours), will try to do an update post when the full details of the scheme of arrangement is out.

Cheers.:)

Senior creditors will only negotiate if they can lose some money in liquidation so junior creditors can press for a fairer deal. The difference in what these senior creditors got under the proposed scheme and liquidation amount should be shared 50 50.

Great post, keep it up!

Thanks! Glad it has been helpful!

[…] been following the Hyflux saga on and off since my original article a while back, but this last weekend, things really started exploding after the […]

[…] been following the Hyflux saga on and off since my original article a while back, but this last weekend, things really started exploding after the […]