The very first article I wrote for Financial Horse was on the ideal net worth allocation by age for Singaporeans. Many times, we as investors fret over which stock or which REIT to buy, when actually what matters far more is the asset allocation. Each asset class comes with its own risk and reward, and a unique mix of each is required to achieve financial goals at each point in our life.

With this in mind, I decided to revisit my asset allocation article, and rewrite it from the ground up. Do share your thoughts on whether you agree, or disagree, with my proposed allocations.

Key Assumptions

In the long run, your performance will normalise

I get that many investors out there think that they can outperform the market. Perhaps they have attended a “technical trading” course, and can’t wait to try out their new candlestick charts or spot a bearish head and shoulders pattern. But the simple fact of the matter is that it is incredibly hard to outperform the market for an extended, 10 to 20 year period.

This is because the index, such as the S&P500 or the STI, is the average performance of all investors investing in such stocks. By buying an index, you have instantly guaranteed yourself a 50 percentile performance of all investors. And don’t forget, many investors who outperform are actually hedge funds or unit trusts, so their final performance net of fees may actually underperform the index.

When I first started in investing, I was always out to chase the next hot stock. Over time, I came to realise that if I had simply bought and held a simple index fund, I would have far outperformed my active trading, with far less work.

Once investors accept that they cannot outperform the index, it actually frees up a lot of time to focus on asset allocation, which to me matters far more for retail investors. If you can outperform an index consistently over a 10 to 20 year period, you really should be running a hedge fund with S$100 billion AUM. I am also sure that Temasek would have use for your talents ;).

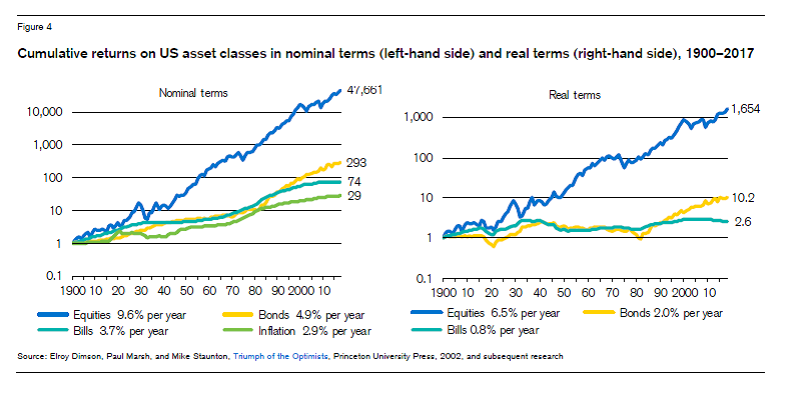

Equity outperforms bonds over the long run

The long term historical returns for equities (stocks) is about 9% versus 5% for bonds. Adjusting for inflation, the returns are about 6% vs 2%. There are numerous studies that back up this fact; that over the long run, no other asset class outperforms equities (although real estate does come very close, and outperforms in certain situations).

The problem with equities however, is the volatility. There’s a great article here that talks about why investors need bonds, and the reason given do not relate to portfolio returns. Everybody knows that equities outperform bonds in the longer term. However, bonds have an important stabilising effect on your portfolio as they are less prone to drawdowns during a recession. Not many people can sit by and watch their net worth take a 50% hit while their neighbours and friends are getting retrenched, and not sell their stocks.

Your goal is to maximise wealth, then preserve wealth

When you are young, the overriding goal is to build wealth. You want to accumulate wealth and assets as aggressively as you can, and enjoy the compounding effects of wealth generation. Once you have achieved your financial goals however, there is no longer any need to take unnecessary risk. Sure, another million on your retirement nest egg is nice, but never forget that risk and reward go hand in hand. By leaving your portfolio in high risk equities for the potential returns, you are exposing yourself to the risk of capital loss. And as you get older and your risk appetite changes, there is less and less need to expose yourself to such risks.

You will live at most 100 years

Statistics say the median life expectancy in Singapore is 82 years old. Less than 1% of the 6 billion people on earth live past 100 years old. As a result, you must plan for roughly 80-90 years of life after starting work. We never know what the retirement age will be in the future (or what the CPF retirement sum will be), so its always good to plan for a longer retirement and have money left over to give to others than come up short.

A financial crisis will come eventually

To be fair, I am probably guilty of this myself. As a millennial investor who started investing post-GFC, I have never experienced a true financial crisis in all its glory. But I’ve spoken to many fellow investors and businessmen who have. A financial crisis will come around eventually. It is part and parcel of the economic cycle, and is healthy for the economy. But that doesn’t make it less frightening. There’s a Buffet quote that I really like on this:

“Cash is like oxygen. When you don’t need it, you don’t notice it. When you do need it, it’s the only thing you need.” – Warren Buffett

Don’t forget to always maintain a liquidity buffer and emergency fund to cover your expenses. When you do need to tap on it, it’s the only thing that matters.

Asset classes

Stocks/REITs

This is the equity component in your asset allocation, which I have defined to include stocks (across all countries) and REITs. The REIT component could actually go under Real Estate instead, but I decided to keep them here because they are capital market instruments exposed to market volatility, and experience much of the pros and cons of an equity investment.

The main qualities of this asset class are high returns, high volatility, low transaction fees, relatively liquid, and large drawdowns during a recession. The rest of this blog is dedicated to discussion on stocks or REITs, so I will not go too heavily into which stocks/REITs to pick. If you are unsure, you can just split your assets among US equities (S&P500 (SPY), NASDAQ (QQQ), some people really like IWDA for the withholding tax treatment), Singapore Equities (STI), and an asian stock ETF such as (VWO).

Note: I received a great question from a reader that I felt really builds on this Stock vs REIT distinction. His question, and my response, replicated in full below.

FH, I noticed you put REITs and other equities into the same asset class. while I understand why, I’m curious as to how the differences between them in terms of risk/return would impact the allocation to each within the class. for example, would 70/30 into REITs/other equities be considered more conservative than 30/70? to what extent would current market conditions affect the preferred ratio, given that REIT prices are (supposedly) more stable than that of other equities?

Response: That’s a really interesting question, and one that I’m still trying to figure out myself. I’ve seen a lot of commentary on this, with pundits recommending limits for REITs anywhere from 25% to 40% of the equity component.

I guess one way to look at it is as diversification within the equity asset class. Just like you wouldn’t put 50% of your portfolio into tech stock (or any specific industry), one’s portfolio should also not be overly concentrated in REITs. Personally for me, I try not to allocate more than 40% of my equity component into REITs, even though within REITs, I diversify across asset classes.

Bonds

The bond component is slightly tricky for Singaporeans. US investors have access to a large pool of highly liquid, risk free treasury bonds. For Singapore investors, investing in treasury bonds exposes us to withholding tax and forex risk that really affects the analysis.

The key characteristics we look for in this asset class are risk free, stable returns and an inverse relationship with equities (ie. they go up when stocks fall). A lot of the retail bonds available to Singapore investors today are most definitely not risk free (hyflux for example). These junk rated bonds, where the yield is high but there is a genuine risk of capital loss, should be grouped under the equity portion of the portfolio.

For Singaporeans, my personal choice for the bond component will be a mix of Singapore Savings Bonds, Nikko AM Bond ETF, and a small amount of US Treasuries. Some people like to use their annuities or endowment plan as their bond component. That’s fine as well, but do be careful of any lock up periods, hidden charges, and understand the baseline returns you are entitled to (not the discretionary returns).

If you are Singaporean, don’t forget that your CPF can technically count towards the bond component as well. Personally I view my CPF OA as a mix of the bond and cash component, since its risk free with stable returns, and can be tapped on any time to cover mortgage payments or buy another house.

Cash

I wrote a previous article here on the thought process behind an emergency fund. Simply put, it’s a fund to cover about 12 months’ worth of your expenses. Calculate the number that you need, and lock it away in high yielding account such as DBS multiplier or UOB One. Fixed deposits are fine as well, as long you recognise the small time lag to access your money.

Key characteristics of this asset class are liquidity, risk free, and low returns.

Real Estate

Real Estate will include your HDB or Condo, and your investment properties.

Key characteristics of this asset class are illiquidity, medium returns and volatility, and require constant maintenance and upkeep costs (property tax, repair costs etc). It can be used to generate rental revenue, but this revenue can fluctuate greatly depending on the strength of the rental market.

Alternative investments

Alternative investments includes everything from bitcoin to a side business, private equity, a property in Vietnam, fine art, wine, watches.

Key characteristics of this asset class are illiquidity, uncertain returns, and niche target audience. Returns can be high if you get the trade right.

Recommended Asset Allocation by Age

With the above in mind, I have set out below 3 different asset allocations, which varies based on your risk profile and financial goals. This will only apply to the positive side of your balance sheet (net of debt).

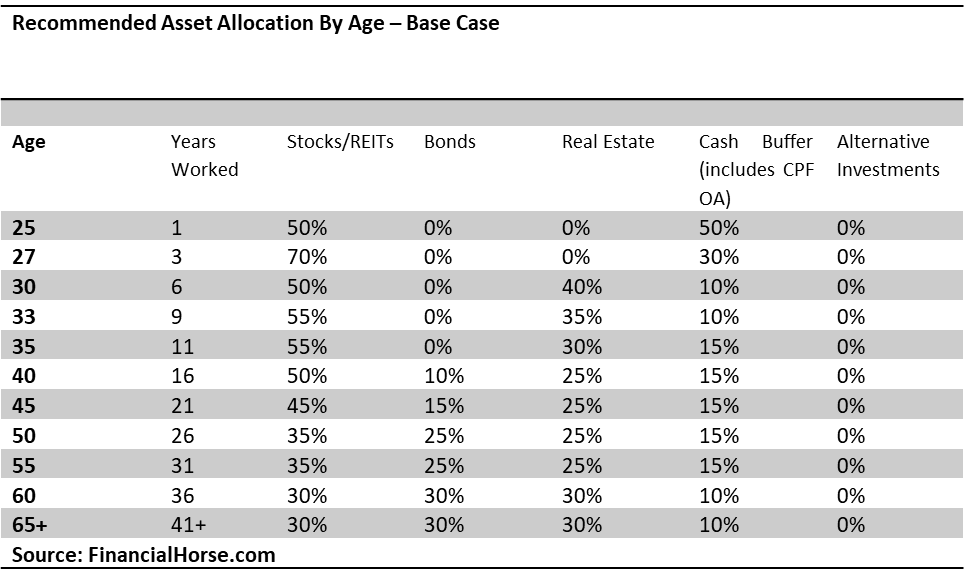

| Recommended Asset Allocation By Age – Base Case | ||||||

| Age | Years Worked | Stocks/REITs | Bonds | Real Estate | Cash Buffer (includes CPF OA) | Alternative Investments |

| 25 | 1 | 50% | 0% | 0% | 50% | 0% |

| 27 | 3 | 70% | 0% | 0% | 30% | 0% |

| 30 | 6 | 50% | 0% | 40% | 10% | 0% |

| 33 | 9 | 55% | 0% | 35% | 10% | 0% |

| 35 | 11 | 55% | 0% | 30% | 15% | 0% |

| 40 | 16 | 50% | 10% | 25% | 15% | 0% |

| 45 | 21 | 45% | 15% | 25% | 15% | 0% |

| 50 | 26 | 35% | 25% | 25% | 15% | 0% |

| 55 | 31 | 35% | 25% | 25% | 15% | 0% |

| 60 | 36 | 30% | 30% | 30% | 10% | 0% |

| 65+ | 41+ | 30% | 30% | 30% | 10% | 0% |

| Source: FinancialHorse.com | ||||||

Note: The table above doesn’t display properly for all devices, so I added a picture version below as well:

The base case is for plain vanilla investors (there’s no shame in this, I am one myself). At 25 when you join the workforce, you split your net worth equally among cash and stocks, because you are young and are still learning the ropes when it comes to investing. Mistakes are okay at this stage because you have at minimum, a 30 year investing horizon and income ahead of you. Accordingly, there is no need for bonds because your future income is high, and the main priorities at this stage are to learn about financial markets, and to accumulate wealth aggressively.

At 30, you are ready to move on to the next stage of your life and start a family. You sell a portion of shares and tap on your cash to purchase your first property. This is a period of large expenses from your wedding, your house, and ancillary costs. Your investing journey can take a small pause here.

In your 30s, the focus is on advancing your career, and paying off the mortgage. You are still relatively young, so there is no need to touch bonds yet. At the same time, there is still a need to accumulate wealth aggressively, so the allocation to stocks remains high.

Once you hit 40, you have accumulated sufficient assets such that real estate as a portion of your net worth is reduced significantly. By this time, your stocks should have enjoyed healthy returns and grown your net worth significantly. With that in mind, you can start taking some risk off the table, and reduce your equity exposure while increasing your bond exposure.

In your 40s to 50s, you may also consider using some of your equity returns or cash to purchase an investment property for income and capital gains. This would further diversify your portfolio, and gives you better control over your investment (you can visit your house).

The end goal here is to have an equal 30% split between each of stocks, bonds, and real estate, while maintaining about 10% net worth liquidity to meet emergency expenses.

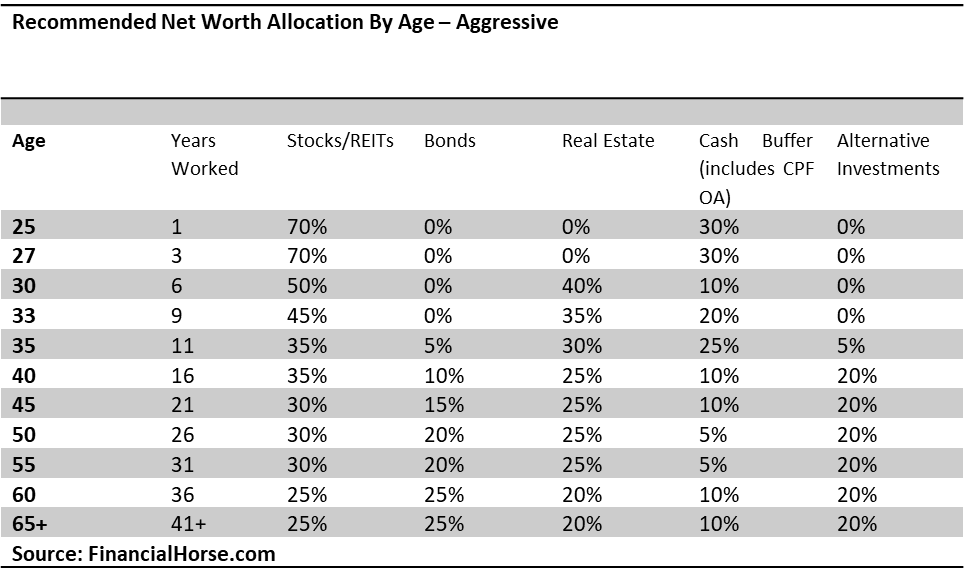

| Recommended Net Worth Allocation By Age – Aggressive | ||||||

| Age | Years Worked | Stocks/REITs | Bonds | Real Estate | Cash Buffer (includes CPF OA) | Alternative Investments |

| 25 | 1 | 70% | 0% | 0% | 30% | 0% |

| 27 | 3 | 70% | 0% | 0% | 30% | 0% |

| 30 | 6 | 50% | 0% | 40% | 10% | 0% |

| 33 | 9 | 45% | 0% | 35% | 20% | 0% |

| 35 | 11 | 35% | 5% | 30% | 25% | 5% |

| 40 | 16 | 35% | 10% | 25% | 10% | 20% |

| 45 | 21 | 30% | 15% | 25% | 10% | 20% |

| 50 | 26 | 30% | 20% | 25% | 5% | 20% |

| 55 | 31 | 30% | 20% | 25% | 5% | 20% |

| 60 | 36 | 25% | 25% | 20% | 10% | 20% |

| 65+ | 41+ | 25% | 25% | 20% | 10% | 20% |

| Source: FinancialHorse.com | ||||||

Note: The table above doesn’t display properly for all devices, so I added a picture version below as well:

The aggressive case is for more confident investors. You are born knowing how to read an income statement, and every purchase you make reaps 20% returns minimum. With this in mind, there’s really no need to hold yourself back, and a 70% to 80% allocation to stocks is comfortable for you.

At 30, you decide to reap your handsome returns on stocks to invest into your very own property. With your midas touch, your hopes are high that this will double its initial investment in 10 years.

In your 30s, you tire of the traditional asset classes of stocks, bonds and real estate. You decide to try something more exotic, such as a property in Cambodia, or trading fine art or whisky. Given the high risk nature and illiquidity of such investments, you have to take some risk off the table, and move some of your equity portfolio into safer bonds.

This continues into your 40s and 50s, with a gradual derisking by moving equities into bonds. In time to come, if you are successful in your alternative investments, they can play a significant role in your net worth, and even be enough for you to leave your day job and focus on it entirely.

The end goal here is a fairly even split between stocks, bonds, real estate and your alternative investments.

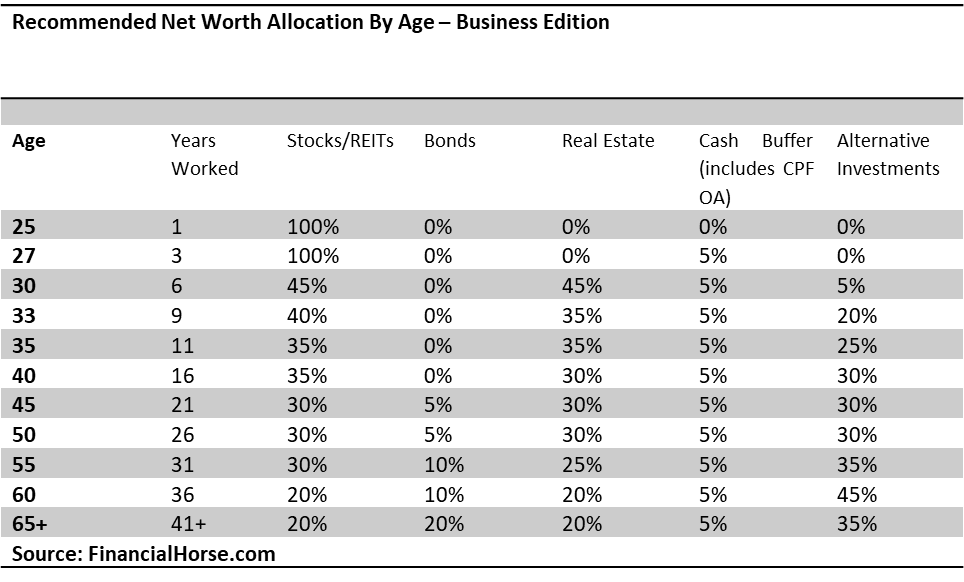

| Recommended Net Worth Allocation By Age – Business Edition | ||||||

| Age | Years Worked | Stocks/REITs | Bonds | Real Estate | Cash Buffer (includes CPF OA) | Alternative Investments |

| 25 | 1 | 100% | 0% | 0% | 0% | 0% |

| 27 | 3 | 100% | 0% | 0% | 5% | 0% |

| 30 | 6 | 45% | 0% | 45% | 5% | 5% |

| 33 | 9 | 40% | 0% | 35% | 5% | 20% |

| 35 | 11 | 35% | 0% | 35% | 5% | 25% |

| 40 | 16 | 35% | 0% | 30% | 5% | 30% |

| 45 | 21 | 30% | 5% | 30% | 5% | 30% |

| 50 | 26 | 30% | 5% | 30% | 5% | 30% |

| 55 | 31 | 30% | 10% | 25% | 5% | 35% |

| 60 | 36 | 20% | 10% | 20% | 5% | 45% |

| 65+ | 41+ | 20% | 20% | 20% | 5% | 35% |

| Source: FinancialHorse.com | ||||||

Note: The table above doesn’t display properly for all devices, so I added a picture version below as well:

I recognise that not everyone is born to work a 9 to 5 job for their entire life. Some people just cannot stand the idea of a desk job. For such people, the business edition is for you.

You are comfortable with the concept of risk, in fact, you live for it. In your 20s, you can go almost 100% stocks. You are confident in your ability to find work even in the most difficult circumstances, so there is no need to maintain a large cash account as you will always have an income.

At this stage in your life, you are also busy honing your craft, picking up vital skills and contacts and familiarising yourself with your industry, as you prepare for the transition into entrepreneurship.

At 30, you purchase your first house (although if you are really aggressive, you can allocate all the real estate portion into your business). You have also learnt enough to try your hand at your own business, and you begin routing funds into your business. This continues for the next 10 to 15 years, as you focus relentlessly on growing your business, while leaving the rest of your wealth in stocks for it to grow aggressively. At a certain point, your business and your net worth will become closely intertwined such that there is no longer a need for a personal cash buffer. Any spare cash you have will be going into your business, and if the business fails, you are likely bankrupt anyway due to the personal guarantees given on bank loans. At this stage, you may even refinance the mortgage on your house to pump the money into your business, due to lower interest rates.

If you are successful at your business, it will eventually come to dominate your net worth. Once that is the case, it makes sense to derisk, because your net worth is now so large than even the 2-3% income from bonds is sufficient for retirement.

The end goal here is to diversify away from the business, with 20% each in stocks, bonds and real estate. However, there is no getting away from the fact that at the end of the day, your net worth and financial health is closely tied to your business.

Closing thoughts

Money is not everything in life. But not having enough money makes it a lot harder. The number 1 reason cited for marital problems is financial problems. While you are young, it is vital to focus on seemingly small things like asset allocation, because in time to come, it may be all that you think about. If you can eliminate financial stress from your life, you are freeing up a lot of time for other pursuits.

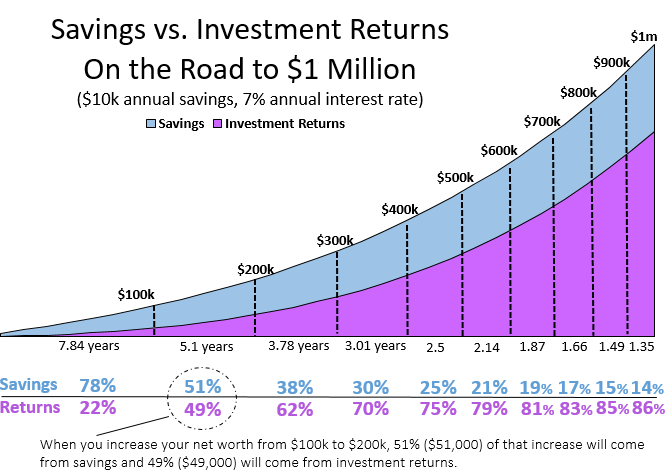

I really like this chart, because it really illustrates the twin powers of saving and investing. When you are young, the only thing that matters is saving. But as you get older, your returns on your investments will dwarf your savings by many multitudes. Yet this is not be possible without proper savings when you are young, and a sound understanding of investments.

If you start young and enjoy the powers of compounding, you are setting yourself up for a great financial future.

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Hi love your articles! wondering how do you calculate the real estate portion of the portfolio? is that an property acquired purely for investment or for own stay as well. Also, would that consideration be for the current price, purchased price or simply how much you’ve paid for the property so far.. Thanks for clarifying!

Hi Kit,

Welcome to Financial Horse! For me personally, I would count both investment properties and my residential dwelling. I would use the NAV, being the approximate market value, less the amount of debt outstanding (ie. the mortgage left on the property).

Hope this clarifies, cheers!

Hi sir,

Will you recommend IT company US stocks and spdr 500 for beginners?

Hi FH, brilliant guide. I’m currently 25, looking to get into investing and this has been super helpful. Just curious: Noticed that you mentioned how bonds are a great portfolio stabilizer in times of downturns. However, based on your asset allocation, you didn’t recommend us to get bonds till we’re 40. Would this be a cause for concern for young people like us, during downturns then?

Also, for the 50%-70% investment into stocks/ REITs, how should I decide how to split that between STI ETF / Roboadvisors? Don’t have much time to analyse and invest into individual stocks, and not that confident in investing either. Hence, seemed like ETFs and Roboadvisors are the way to go. Any suggestions for someone like me?

Thanks so much.

Hi great questions! Yes, for young people like us, the solution is to keep calm and just keep buying more stocks, because frankly, as long as we don’t lose our jobs, we still have decades ahead of us in terms of earning power.

I really do not like robo advisors, because I feel that they don’t add much value. If you’re not into stock picking, you can actually just buy ETFs purely (one way is to see what the ETFs buy, then buy those directly). I like the S&P500, the NASDAQ, the Hang Seng Index. You can also check out the recent Philips Sing Income ETF, I thought that was a good index as well (but expense ratio is high).

If you do use robo-advisers, you have to be careful because sometimes they have a bond/gold component as well, so that will affect your tactical asset allocation.

Cheers!

Hi I was wondering what your savings vs investment returns mean? I’m currently 28 and earning about 140k a year, just starting to touch investment but I don’t know how.

Hi!

Savings is the amount you save from your day job, investments is the amount you make from your returns. The older you get, the more you should make from investments vs savings.

Welcome to FH btw! You can check out our guide to investing for a starter: https://financialhorse.com/guide-to-investing/

Once you’ve read the free stuff on this site, you can also check out the FH Course. It’s probably the best and most comprehensive investment course out there today: https://financialhorse.com/fh-course/

Hope this is helpful!

Hi, thanks for the excellent piece! Just wondering if I’m understanding this right – if a regular 30 year old has 500k in assets, does this guide imply (with a 75% LTV ratio) that the max price for his first property should not exceed 800k (500k*0.4/0.25) if he wants to maintain a sensible allocation of assets? Seems a little on the conservative side, so I was wondering if you had any thoughts on what a reasonable range for the initial allocation of capital into real estate might be?

Well this is designed as a guide for the average Singaporean, which would likely be going with a BTO (80% of the population right?).

For certain individuals, I get that this allocation wouldn’t make sense, in which case I think some of the allocation into equities/bonds can go into real estate instead. Exact mix would depend on risk appetite. 🙂

I would say keeping allocation to real estate at less than 50% of net worth is probably a more balanced approach. And this would count only equity in the real estate (ie. net off debt). Rest can go into a mix of cash + equities + bonds. In this market, bonds no longer make a lot of sense unless the individual is v high net worth.