The humble Singapore REIT. If you had bought and held a broad basket of S-REITs 5 years ago and held them until today, your total return (including distributions) would have been an annualised 8.4%, blowing past the 4.4% annual return had you bought a STI ETF. Given the less than robust nature of the Singapore retail bond market, there is no getting around the fact that to build a core long term portfolio as a Singapore retail investor, the S-REIT must form a cornerstone of your portfolio.

In this Article, I will set out a framework of 5 key criteria to analyse when investing in S-REITs.

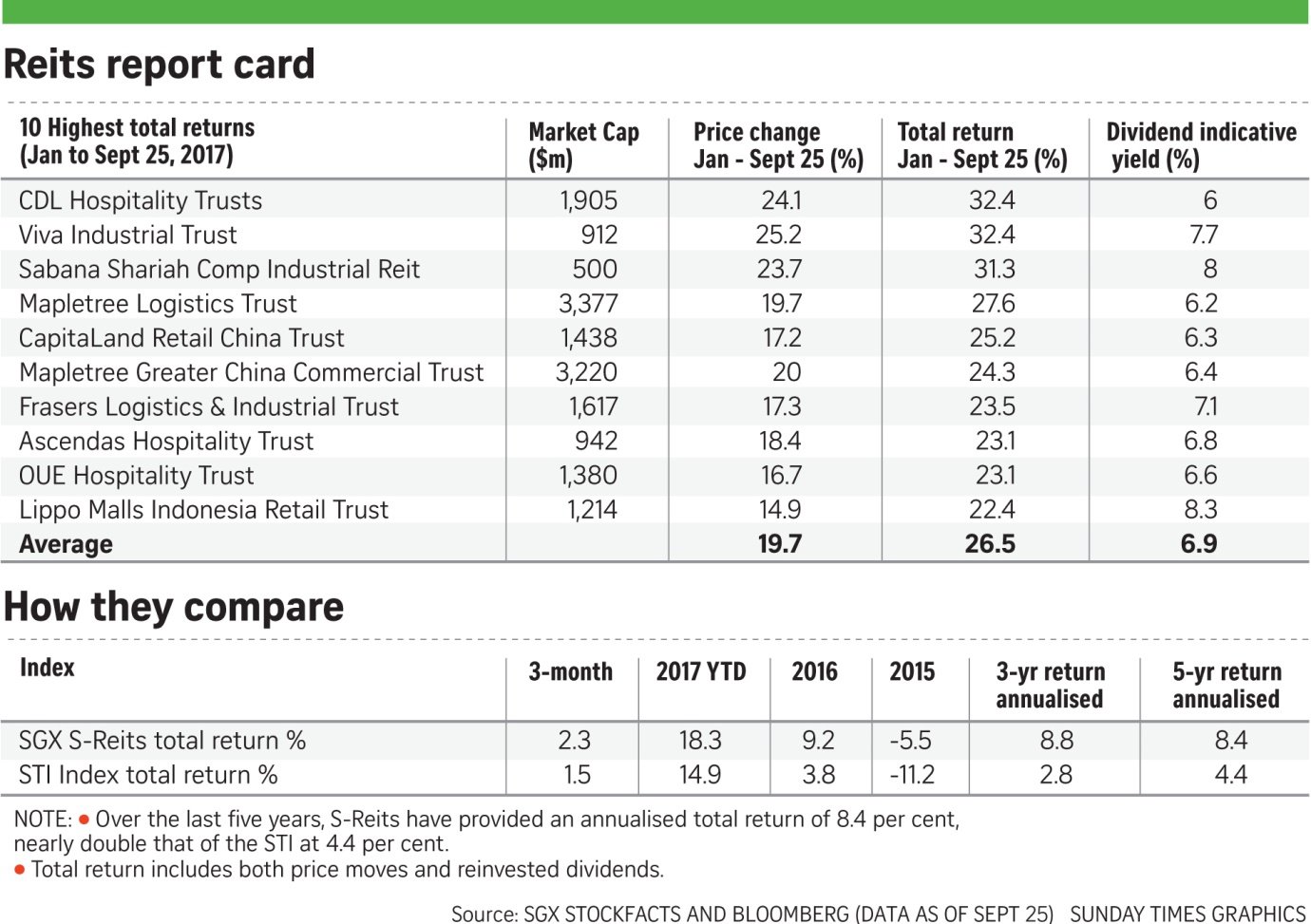

Source: The Straits Times

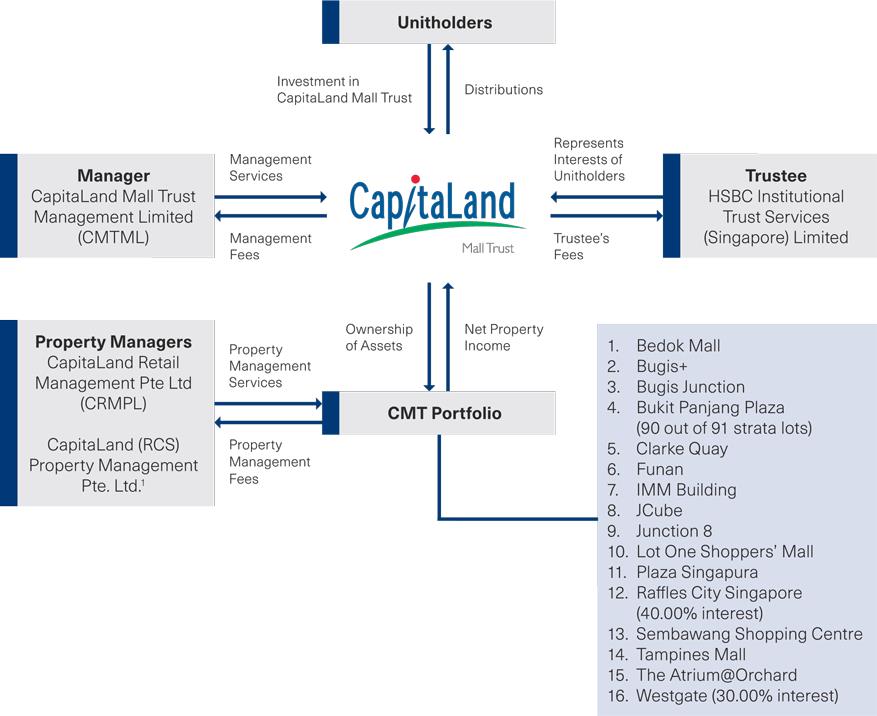

Basics: Structure of a REIT

Source: http://www.cmt.com.sg/trust-structure.html

A REIT, or Real Estate Investment Trust, packages a portfolio of Commercial Real Estate into a trust structure (for tax reasons), which is then listed on the SGX and sold to investors. Investors who hold units in a REIT (Unitholders) are entitled to regular distributions (either semi-annually or quarterly). REITs are required to pay out more than 90% of their distributable income, to ensure that they enjoy the tax transparency.

The legal structure of a typical REIT is set out above, but essentially, these are the key entities:

1. Trustee – The trustee, HSBC Trustee, is the legal owner of the property and holds the title. They act on behalf of unitholders.

2. Manager – The Manager, CMTML, manages the REIT, including the investment, finance and investor relations functions. This is the entity that decides which properties to acquire or divest, and on the method of financing and refinancing. In a Sponsored REIT, the manager is wholly owned by the Sponsor.

3. Property Manager – The day to day management of the property is outsourced to a Property Manager, CRMPL, who is paid property management fees.

4. Unitholders – Given the trust structure of a REIT, shareholders are known as unitholders, and dividends are distributions. As a unitholder, you sit back and let the professionals run the REIT, collecting your distribution and hopefully, capital appreciation.

Tax Implications

The favourable tax regime for S-REITs has contributed massively to the growth of Singapore as a premier destination for REITs in Asia, ahead even of Hong Kong.

If a REIT pays out more than 90% of their distributable income, they enjoy full tax transparency. If you as an individual hold units in the REIT, the distributions that you receive are tax exempt as well. This means no tax is levied by IRAS from the time rent is paid by the tenant to the landlord, until the time it is distributed to you as unitholder.

Marvel at this for a moment. If I buy a 1 million dollar investment property in my name, not only do I pay stamp duty and a 7% additional buyer’s stamp duty (ABSD) on my initial purchase, but I also pay income tax on all rental proceeds received from the investment property. By contrast, if I wanted to invest in Vivocity, all I do is to buy units in Mapletree Commercial Trust. I pay no stamp duty or tax on the purchase of my units, and none of the distributions received are taxable. (Note: If the properties are located in a foreign jurisdiction, eg. CapitaLand Retail China Trust which holds China assets), the REIT would be subject to PRC tax regime on their rental income).

Do note however, that if a corporation holds units in the REIT, this tax treatment no longer applies, and the prevailing 17% corporate income tax is payable. For this reason, I strongly discourage investing in the REIT ETFs (Lion-Phillip S-REIT ETF, NikkoAM-Straits Trading Asia Ex Japan REIT ETF, Phillip SGX APAC Dividend Leaders REIT ETF). Not only do you pay an annual fund management fee, you also pay 17% tax on all distributions, which severely reduces the returns on your investment. For a S$100 distribution from the REIT, you only receive about S$82 after deductions. Until the tax regime changes, you are better off creating your own diversified portfolio of REITs.

Update: Following Budget 2018, REIT ETFs are no longer subject to the 17% corporate income tax. I analyse the pros and cons of REIT ETFs in a separate article here.

What to look for in a REIT

1. Strong Sponsor

The legendary quote by Warren Buffet goes, “Rule No. 1: Never lose money. Rule No. 2: Don’t forget rule No. 1”. The most important rule in investing is to never lose money. As a corollary, you should never make investments in REITs that could potentially go insolvent. 10 years’ worth of distributions can be wiped out overnight if your REIT goes insolvent and you lose most of your principal. Take a look at the case of MacArthurCook Industrial REIT, which went insolvent during the financial crisis, and was acquired by AIMS Financial for cents on the dollar, resulting in huge losses for all existing unitholders.

For this reason, I only invest in REITs backed by a strong Sponsor. For me personally, this includes CapitaLand, Mapletree, Frasers, Ascendas and Far East Organisation. Given the strength of the balance sheet of these Sponsors, including the implicit government links (Temasek) for some of them, I do not see a situation where their Sponsored REITs will ever encounter an insolvency event.

With a strong Sponsor, you also enjoy the following benefits:

1. Corporate Governance – Too many of the smaller REITs have management that abuse their positions by playing around with valuations, or dressing up acquisitions with income support. You do not want to waste time digging through financial results and SGX announcements to understand the true nature of an asset. Stick to blue chip REITs, where there is a robust corporate governance framework in place to limit the potential for abuse.

2. Pipeline – A Sponsor such as a CapitaLand or Mapletree has a deep and robust pipeline of assets ready to be injected into the REIT. This serves as a ready and essential source of growth for the REIT, and allows you access to high quality assets that would not be obtainable via any other means.

3. Size – With a powerful Sponsor such as CapitaLand or Mapletree behind the REIT, the REIT manager has huge bargaining power when it comes to negotiations. This allows the REIT to have first dibs on prized acquisitions, strong negotiating power when negotiating an acquisition and favourable rates when it comes to refinancing.

| Sponsor | REITs |

| CapitaLand | CapitaLand Mall Trust

CapitaLand Commercial Trust CapitaLand Retail China Trust Ascott Residence Trust |

| Mapletree

|

Mapletree Commercial Trust

Mapletree Industrial Trust Mapletree Logistics Trust Mapletree Greater China Commercial Trust |

| Frasers

|

Frasers Commercial Trust

Frasers Centrepoint Trust Frasers Hospitality Trust Frasers Logistics & Industrial Trust |

| Ascendas

|

Ascendas REIT

Ascendas Hospitality REIT |

| Far East | Far East Hospitality Trust |

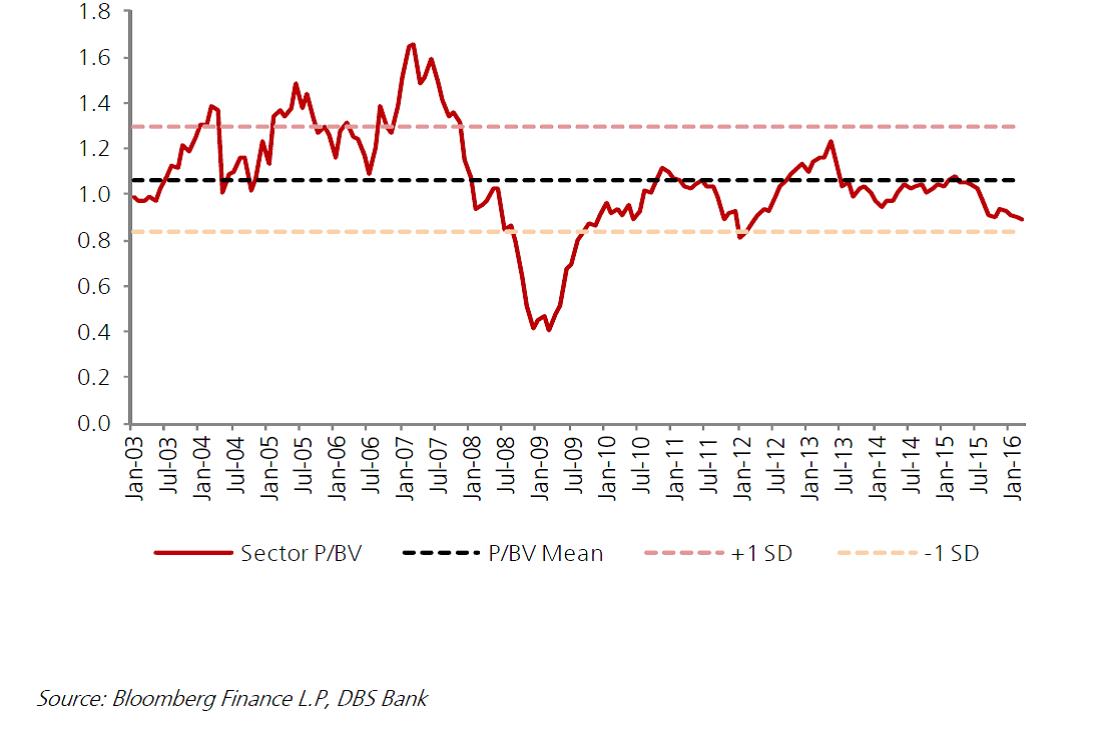

2. Price/NAV, or Book Value

Historically, outside of a financial crisis, REITs in Singapore trade between a range of 0.8 to 1.3 times book value. When buying a REIT, always check its Price/NAV. Great resources I use regularly to check on Price/NAV and Distribution Yield are http://reitdata.com/ and https://sreit.fifthperson.com/. Do be sure to verify the numbers independently though.

Compare the Price/NAV of the REIT you are purchasing against comparable REITs. For the blue chip Sponsored REITs I look at, I will compare them to a REIT in the same geography and asset class from a competing property developer, to determine if it is overvalued. As a general rule of thumb, the price of REITs trade in tandem, and it is hard to get bargains that have not been discovered by the market. If it is trading at a huge premium to book value (eg. 1.3x), the market is typically pricing in higher than expected growth in the future.

Personally however, I will never buy a REIT at 1.3x book value, as I find the upside in terms of capital appreciation to be limited, but the downside may be large. Remember that a 20% drop in the REIT price can wipe out 3 years’ worth of distributions for a 6% yielding REIT. My personal rule is to pick up blue chip REITs aggressively when they are trading close or below book value. In all other situations, I am comfortable paying up to 1.15 times book value if I like the assets and prospects of the REIT, but I will never go beyond 1.15x.

Historical Price/NAV ratios:

3. Sector / Geographical allocation

REITs are broadly split into the following categories, based on their real estate portfolio:

1. Commercial (Offices)

2. Retail (Shopping Malls)

3. Hospitality (Hotels or Serviced Residence)

4. Industrial (Warehouses, factories)

5. Others (Healthcare, Data Centers etc)

The conventional thinking behind a broad, diversified REIT allocation is to diversify risks. If retail is getting hammered due to massive competition from Lazada and Qoo10, your distribution from CMT or Frasers Centerpoint trust may fall, but the theory is that your Commercial, Hospitality and Industrial REITs will pick up the slack.

Of course, this is outside of a financial crisis level event, where global commercial real estate prices fall across the board. Hence while diversification among REITs is important, do remember that at the end of the day, these are all investments in real estate, and they are not an effective hedge in a recession. For this reason, you should always ensure you have a portion of your net worth in risk free assets (see Recommended Net Worth Allocation by Age)

Each industry and geography has their own cycles. For example, retail is having a bad time in recent years due to increase competition form e-Commerce, while office rents are going from strength to strength due to tighter supply and the economic recovery. Unless you are in real estate, it is incredibly hard to pick up on and front run these market movements, as I find that the anticipated future outlook is already priced into the trading price. You are far better off taking a long term view and ensure you are broadly diversified across geography and industries, to maintain a stable distribution.

I personally split my REIT portfolio distribution by the following allocation, while being careful not to be overly concentrated in any one country:

| Category | Allocation |

| Commercial | 25% |

| Retail | 25% |

| Hospitality | 25% |

| Industrial | 25% |

| Others | 0%1 |

1 There are not many S-REITs that within the “Others” category (notable ones are Keppel DC REIT, Parkway Life REIT, NetLink Trust). While I prefer to keep to the traditional classes, feel free to allocate up to 20% of your REIT portfolio to this category.

4. Quality of Assets

The properties held by the REIT are key, since that is what you are investing in. A test I like to use is to imagine whether, if I had sufficient money, I would want to own the property. For example, given a choice to own Vivocity or Aperia Mall, I would take Vivocity hands down. It has a fantastic location with a strong footfall and minimal competition in the region, as well as a potential stream of endless AEIs, that would far make up for the increased valuation. When asking if you like the asset, you can consider the following questions:

Location – Is the property located in a good catchment area? Is there strong competition in the vicinity? Is it centrally located near the CBD? Is the area marked for future redevelopment?

Quality of Asset – How old is the Property? How many years are left on the lease? Is the property an ageing one which will require Capex going forward? Has it just completed a round of AEI that rejuvenated the ageing asset?

Value Add – Value Add is the X factor when evaluating a REIT. After purchasing a property, can the manager improve the asset to increase its yield? A fantastic example is what CapitaLand has done with Plaza Sing in tweaking the tenant mix, the opening of Atrium, and the AEIs, that have contributed shopper stickiness and footfall. Every time I visit Plaza Sing I marvel at the unique tenant mix and the crowds. Viva Business Park is another great example where Viva Industrial Trust took a dingy old industrial building, spruced it up and added Decathalon, Burger King and other F&B, attracting crowds and increasing rental yields. There is no easy, proven way to determine the X factor. You just have to look at all the facts and take a rational position based on what you know. This is the “gut feel”, the “luck” in investing. If you are sufficiently diversified across blue chip REITs however, you have already limited your downside, and chances are, among your portfolio of REITs, a few of them will turn into superstars.

Capitalisation rate – A lower cap rate translates into a higher valuation for the property, and vice versa. Ensure that the cap rates being used are in line with market standards for the country. As at early 2018, the indicative cap rates for developed markets are:

- Singapore: 4-5%

- UK: 4%

- HK: 3%

- Europe: 3.5%

- Australia: 5%

If you are investing in a blue-chip REIT, this is typically less of an issue, as they have an army of auditors, independent directors and internal audit to prevent abuse of valuations.

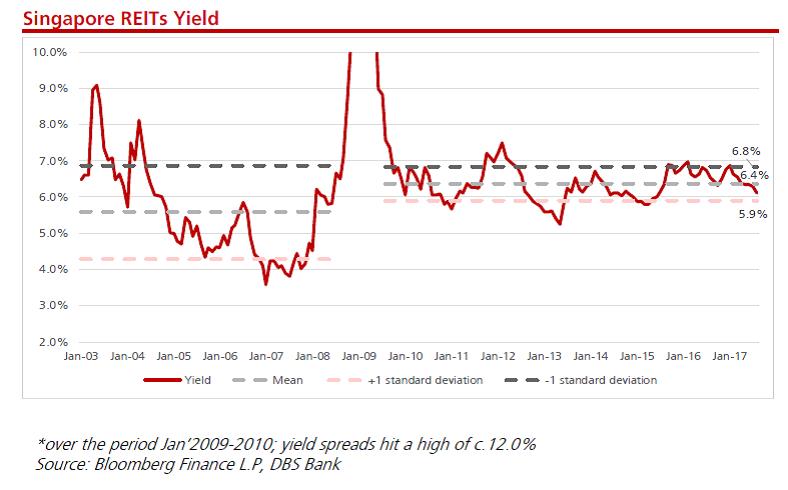

5. Distribution Yield

A bird in hand is worth two in the bush. DPU is real money in your hands; share price appreciation is not. Even if locked in, the tendency is to plough your gains into a new investment to offset the lost income. Eventually when the market corrects, the birds in the bush remain in the bush.

The distribution yield of a REIT fluctuates depending on the stage of the economic cycle we are in. As you can see in the table below, this can go to 12% during a financial crisis, but outside of crisis situations, distribution yield typically trades in a 5.5-7% range.

As a personal rule, for blue chip S-REITs, I will only invest if I get a 5.8% yield or above. This is in addition to the 1.15x book value rule that I have set for myself above.

Beyond the yield, it is important to understand the sustainability of distributions. Whether it’s a company‘s accounts or an investor‘s returns, only one thing is real – cash flow. Everything else can be dressed up. Look at the cash flow from operations, and understand whether cash flow is increasing steadily, whether it is in decline, whether it is erratic, and understand why. If for example CMT’s cash flow is in a slight decline, this is likely due to the competitive retail climate and competition from e-Commerce. This is important so you know whether to hold or to sell, and allows you to be confident in your investment thesis if the REIT price were to fall precipitously.

Consider the following example. Say 5 years ago, you had $1.0 million in the bank earning 4% interest. Today, you have the same $1.0 million in the bank earning 1%. Do u feel poorer? I think most people don’t. Say 5 years ago, you invested in ABC Reit yielding 6% and it has been paying the same DPU annually. But because of macro market sentiments, the “market value” is now $900,000. Yet having looked at the cash flows, the cash flow from operations is steady, with a 0.5% growth. Do you feel poorer? Would you sell the REIT? Once you understand the business and its underlying cash flows, you are freed from the vagaries of market pricing. A fall in prices when cash flows are stable is a buying opportunity, not a cause for panic. As long as you do not sell at the current market price, you have already outperformed the alternative in cash by collecting a constant distribution.

Honorable Mention: Interest rates

REITs, and real estate in general, are a highly levered industry, with a typical gearing of between 30-45%. An increase in interest rates affects the cost of borrowings and refinancing of the REITs. Without a corresponding increase in rental yields, this leads to a fall in your distribution. An increase in interest rates also increases the attractiveness of competing investments, and diverts capital away from REITs. Accordingly, an increase in interest rates impacts REITs significantly, and many financial advisors advocate being mindful of interest rates.

However, one should be mindful of such advice, lest it becomes a fool’s errand. Nobody, apart from the Federal Reserve or President Trump, knows conclusively where interest rates will be 12 months from now. If it were possible, such a movement would already be reflected in the unit price.

Hence while I am constantly mindful of the threat posed by interest rates and keep a watchful eye on them, I do not attempt to trade REITs based off prevailing views on interest rate movement. I prefer to take a long term view when investing in REITs. So long as the distributions remain stable, the REIT does not go insolvent, there is good growth from a robust pipeline, I am a happy investor.

Closing Thoughts

For most investors, owning a portfolio of blue chip REITs is likely to provide the best total returns with the least risk and volatility. The key then, is to manage your emotions. Stick to the rules that I have set out above, and do not deviate from them even when REIT prices are going up 5% a day. The market may be comprised of fools, but it does not mean you have to be one.

Many investors are so afraid of missing out when they see the REIT prices going up. And when the price is going down, they are always hoping to get it cheaper. The key is to do your research to determine if you like the properties, and to buy when you are happy with the price. If prices drop, buy more, as your yield on cost increases. If you have no more resources, then sit tight and wait it out. Nobody can hope to buy at the bottom all the time but the key is holding power. Similarly don’t think that you will buy winners all the time. Ultimately it’s the law of averages, the good, bad and the ugly. If you can just generate a 6-8% annual return in SGD assets overtime for a conservative portfolio, you have already blown past returns from cash, and outperformed your peers who invested in properties.

Ready to put the framework to the test? Find out why Mapletree Commercial Trust passes the Financial Horse test for an S-REIT here.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Hi Financial Horse,

Educative and helpful article. Thanks!

I have a couple of questions if you can please provide your opinion.

1. Which brokerage firm do you recommend to buy REITs and hold for long term? I currently have an account with Saxo.

2. What is the minimum amount you recommend investing in each REIT for the investment to be worthwhile assuming charges & fees for brokerages and how many REITs do you recommend as a minimum for a diversified portfolio?

Hi Red Scorpion,

Welcome to Financial Horse! My responses below:

1. For Singapore stocks, best to use a CDP account. Personally I use DBS Vickers Cash Upfront.

2. I would say stick to about 4-5k per transaction, to reduce transaction costs as a percentage of your investment. Ideally, you would want to cover, retail, office, industrial and hospitality asset classes in your REIT portfolio, across a fairly diverse geography. For me personally, I have 5 REITs that form the core of my REIT portfolio.

What are the core 5 REITs that form your core for your REIT portfolio ?

It’s available on https://www.patreon.com/financialhorse for a small fee (to keep this site running), but I’m just going to share it here anyway since you asked:

MCT, MGCCT, Ascott, MLT and Keppel KBS US REIT.

There are certain legacy reasons why I built it this way though, so don’t copy it blindly!

Cheers!

Hi FH,

Thanks for this extremely insightful article. I’m still very torn about how to invest in REITS right now as I’m only earning less than $2500 a month and can only afford investing around $100-$400 each month (regardless of instrument). Meaning I’m probably looking at only investing $100 each month in REITS / REITS ETF via DCA to start.

Very attracted to REITS given the high dividend income, and I can’t wait to start. But noticed in the comment above that you recommend min $4-5k per transaction. Is my best option to stay out of the REITS market (I would foresee for the next 3 years) to accumulate enough to start?

– On a similar note: Would you recommend DCA or lump sum for REITS? Saw that Maybank KE has a RSP for REITS… any thoughts on this and whether it is worth committing to? They impose clearing fees, SGX trading fees and GST on top of their 1% commission, which sounds a little daunting but I’m not sure.

Hi Virginia!

Welcome to Financial Horse! I think given the sums you are investing, lump sum investing would be the easiest. Save up 2-3k and deploy it into one investment, and when you have another 2-3k and deploy it into another. Over time, you’ll be able to build up your portfolio this way!

The key here is to start early, and build up your financial knowledge and experience in the markets. Eventually as you get older your income will increase, and you can deploy your cash more confidently. 🙂

Hi

In the article, you mentioned : If the properties are located in a foreign jurisdiction, eg. CapitaLand Retail China Trust which holds China assets), the REIT would be subject to PRC tax regime on their rental income).

What does this mean? Does it imply i will have to pay income tax for properties are located in a foreign jurisdiction?

Someone asked investing via DCA. What does it mean? It is workable compared to lump sum investment?

The tax will be done at the REIT level, so there’s no need for you to do anything. It will affect the income from the REIT though, but this is usually already factored into the trailing twelve month yields that you see.

DCA is dollar cost averaging, which is putting investing into a particular stock on a regular basis. It’s really about convenience. For me I can’t be bothered with anything that is regular, so I just save up my money, and when there is enough, or if prices are good, I’ll add to one of my existing positions (or start a new one).

[…] this article, I generally adopted the Financial Horse framework for analysing REITs that I wrote about previously, so do check that out if you want more […]

Hello Financial Horse!

If i were to do a lump sump investment into REIT every half yearly (around $3000 worth) – can i ask how would you advise going into the different REITs to build my own REIT portfolio? In my mind, wouldn’t the fees be quite hefty?

e.g. $600 into MCT, $600 into Ascendas, $600 into MLT, $600 into Frasers, $600 into Netlink = $3000

The fees will be 0.12% at DBS Cash-upfront per counter at min $10, wouldn’t this transction be $50 in fees alone? Or am i mistaken?Any advice on this is greatly appreciated!

Yes that would be quite hefty in terms of fees. If you are only able to invest 3k every half yearly, I would say to buy one 1 REIT each time. So you buy MCT with 3k first, then Ascendas, then MLT etc. This reduces your transaction costs to S$10 each time, and from a long term perspective, shouldn’t hurt your returns too much as long as you keep up the buying.

Hope this helps!