The past week has been a tumultuous time for everyone. Myself included. It’s been the fastest bear market in stocks that we have ever seen (quicker than the great depression).

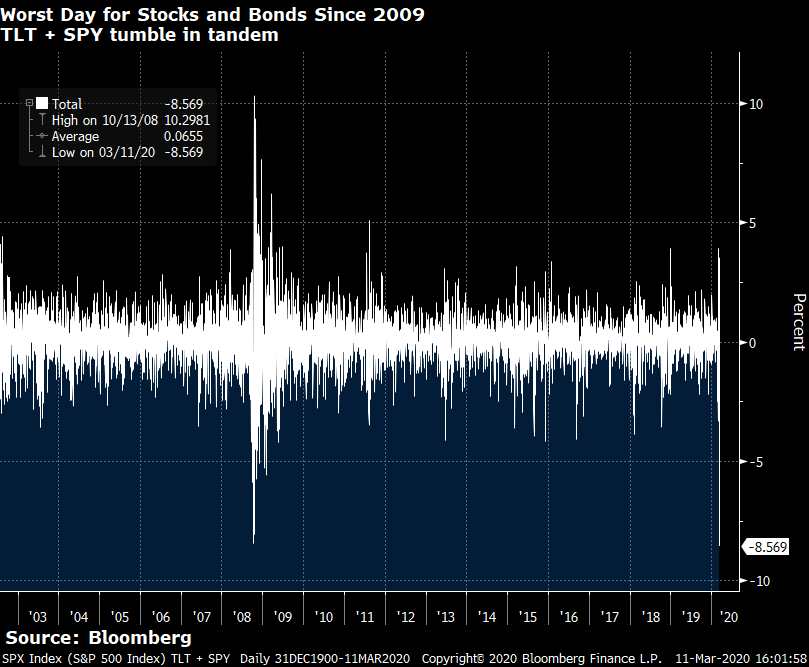

Every single portfolio has been hit. The past week saw cross asset correlations go up. This means that the stuff that investors usually use to hedge (US Treasuries, Gold etc) actually dropped together with stocks. Just take a look at the cover chart – TLT and SPY are tumbling together!

This is really bad because it impacts almost every portfolio strategy out there. Everything that is loosely based on modern portfolio theory – 60/40s, risk parity, the StashAway style funds etc would all have suffered big losses these week.

So hey, take a deep breath, and forgive yourself. Even the professional money managers got wrecked this week.

The only asset class that did well? Cash. And maybe Singapore Savings Bonds (SSBs).

Why do cross asset correlations go up? It’s usually a sign that investors are liquidating. Investors need cash urgently, so they are selling whatever they can get their hands on – and they are instructing their fund managers to do the same.

And why do investors need cash?

Any number of reasons – from meeting margin calls, to raising cash to make up for business cash flow. The past week would have seen big margin calls from anyone using leverage in financial markets, so my theory is that the big liquidation so far is coming from investors needing to meet margin calls. But as this drags on, we’ll start to see the latter reason come into play.

Financial Horse team will be here

So in these tumultuous times, I want you to know that I (and the Financial Horse team) will be here for you.

Every Saturday (or Sunday if I’m tied up), there will be an article on Financial Horse sharing my thoughts on investing and the markets. Rain or shine, no matter how busy I am with work, it will be there. And nothing but my honest opinions and thought process on what’s going on. Whether you believe me, and what you choose to do with it, I leave it up to you entirely.

And if you want my thoughts or you want to share comments or feedback, just leave a comment on the post. I answer each comment personally.

For those of you who haven’t signed up for our mailing list, please do consider signing up, its absolutely free. It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. I do share additional information there sometimes that could be handy (there’s a FH 7 Commandments for Investing you get when you first sign up).

Basics: What happened this week

We usually start these articles with a recap of the past week. Not sure what you guys (and girls) think of that. Do you like this section, or do you prefer we skip and dive straight into my thoughts? Let me know in the comments below.

I’ll keep it for this week, but if you don’t like it I’ll take it out next weekend.

Btw, all charts are sourced as at 13 March 2020. I will not be updating this article going forward. Updated thoughts are on Patron.

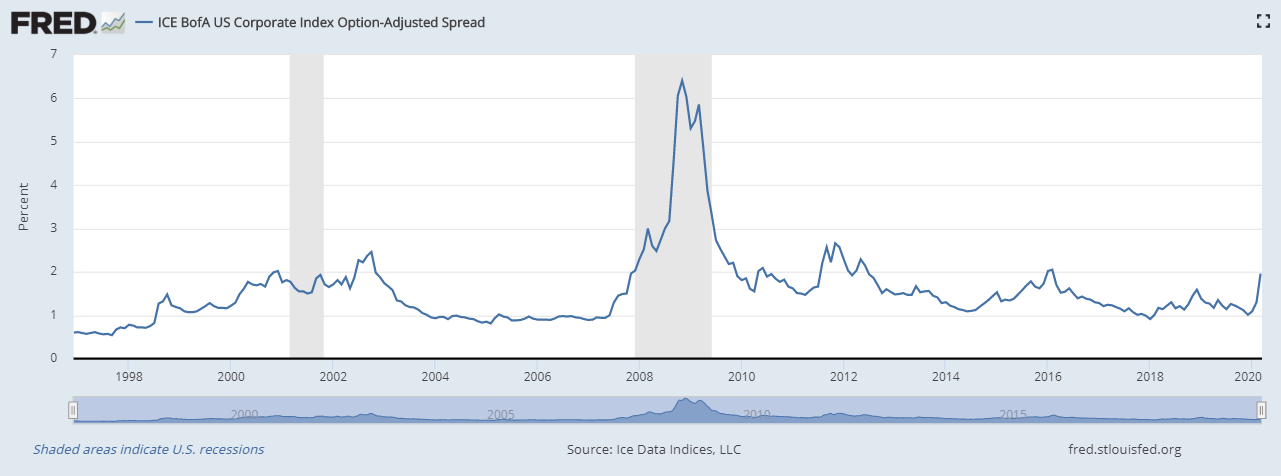

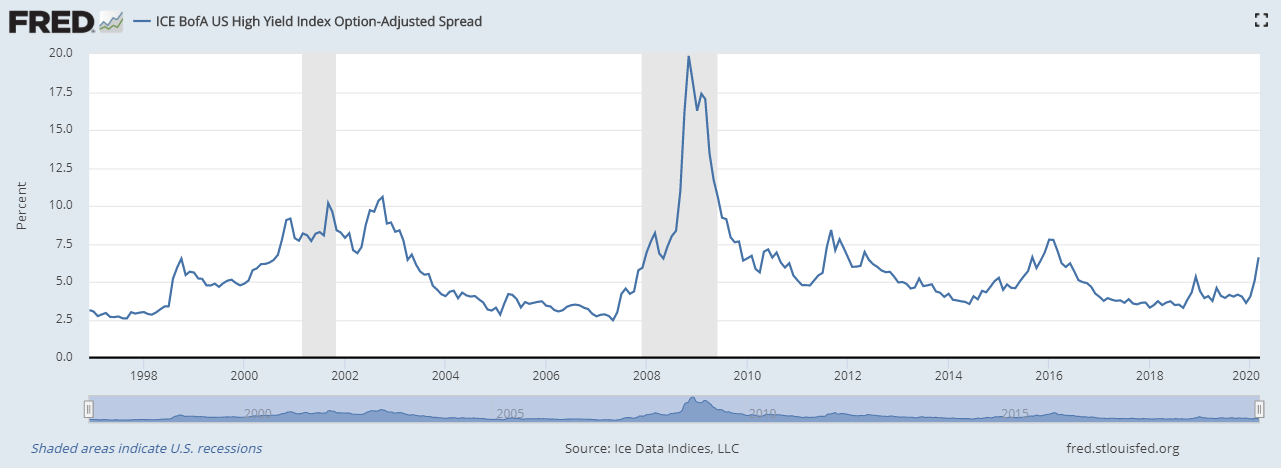

US High Yield and Investment Grade credit spreads are starting to blow up. We’re well above the 2018 highs at this point, but still below the 2016 highs – the 2 other times this cycle where we came close to a recession.

I’m using the 20 year charts here to give you some sense of perspective, because the 5 year charts always induce panic, which doesn’t do anyone any favours.

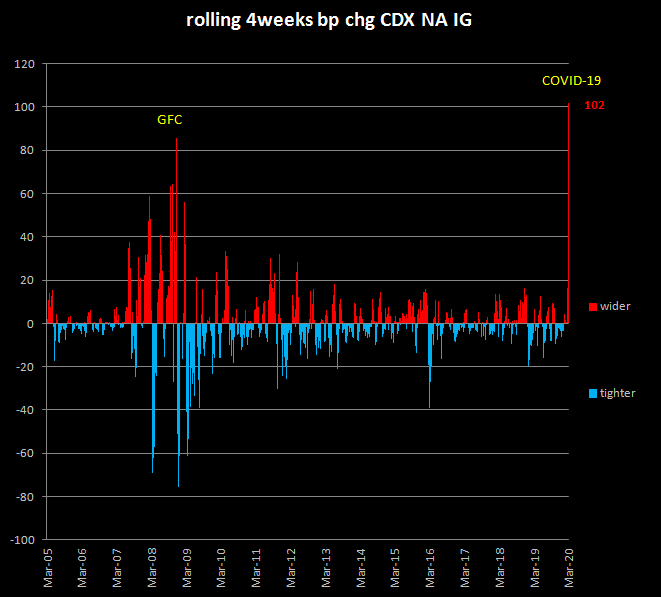

ITRAXX MAIN (corps IG) and CDX NA IG sample set out below. This is the cost of credit default swaps, and reflects widening credit spreads. The 4 week change here is faster than the GFC back in 2008, which shows that investors were caught completely off-guard by COVID-19.

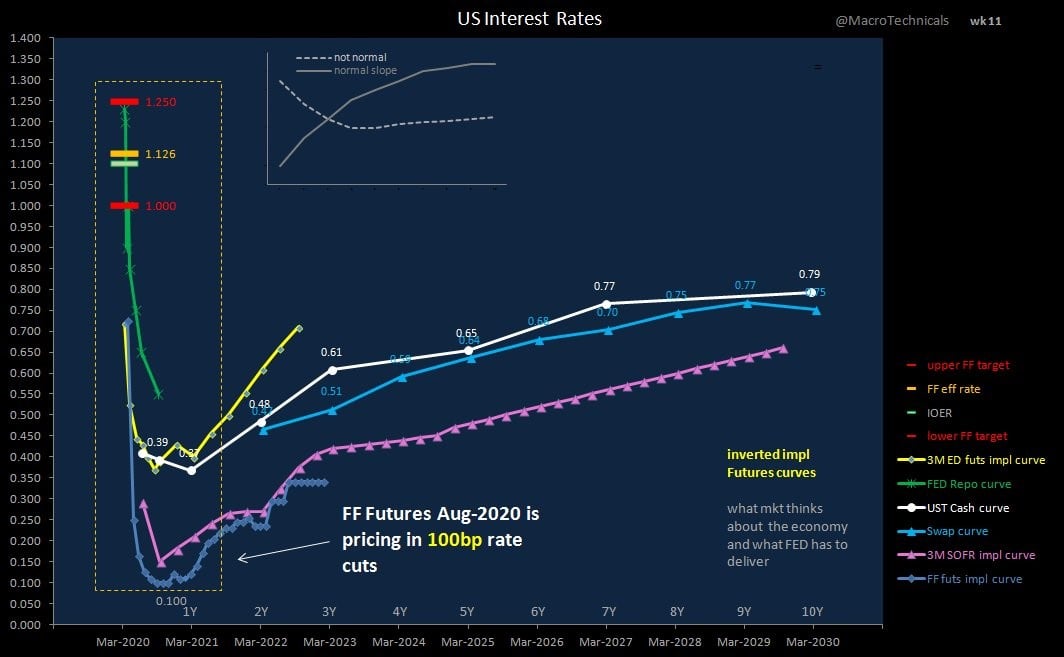

Fed Futures are pricing in 100bps cut now – which takes us to zero bound.

What really didn’t help, was Christine Largarde coming out to promise that “all options are on the table”, and then absolutely disappointing the market with no rate cuts and no big policy moves. That lend to the 10% drop in the FTSE and the 17% drop in Italian Markets. Classy move, Largade.

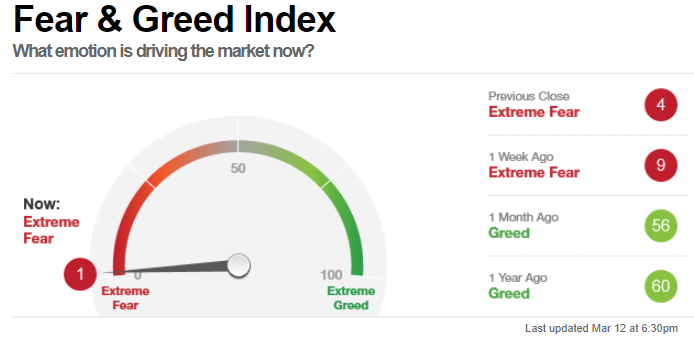

Sentiment

Sentiment has swung from greed 1 month back to complete fear. I don’t think I’ve seen the Fear&Greed this low, ever.

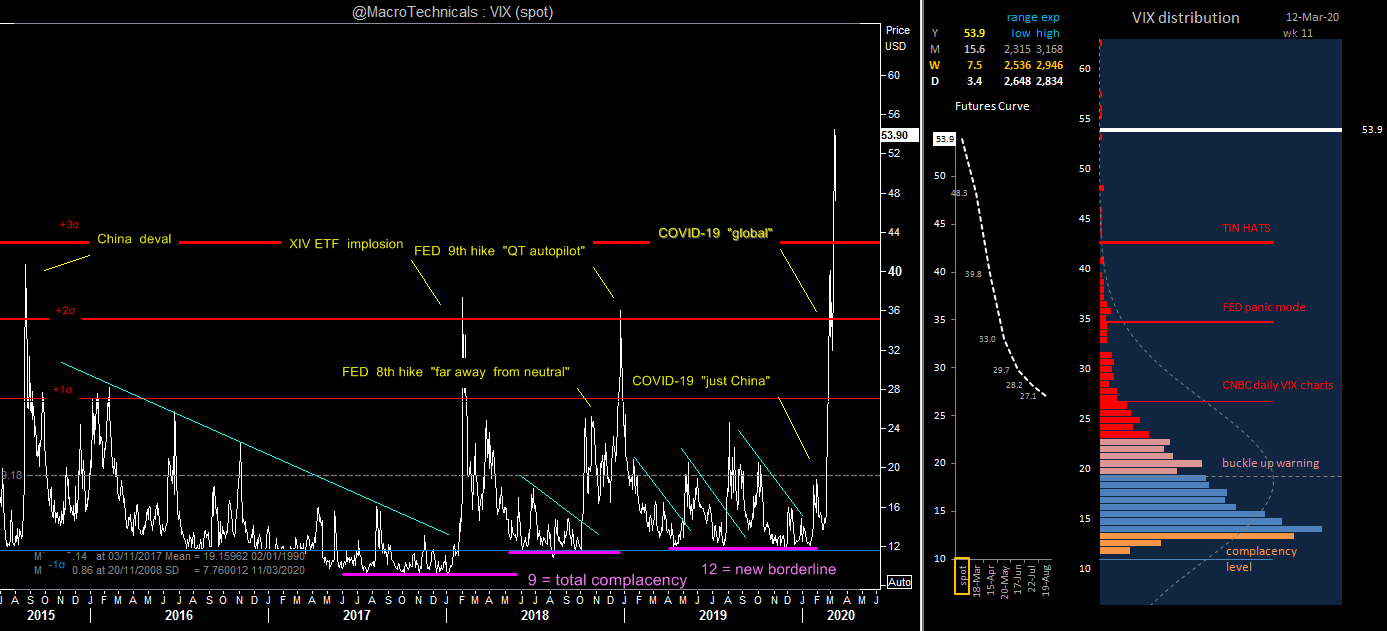

This is what the Vix looks like. Completely blowout, with an extreme backwardation curve. In plain English, what this means is that volatility is at an extreme high – but no one has any clue what the next 30 days will look like.

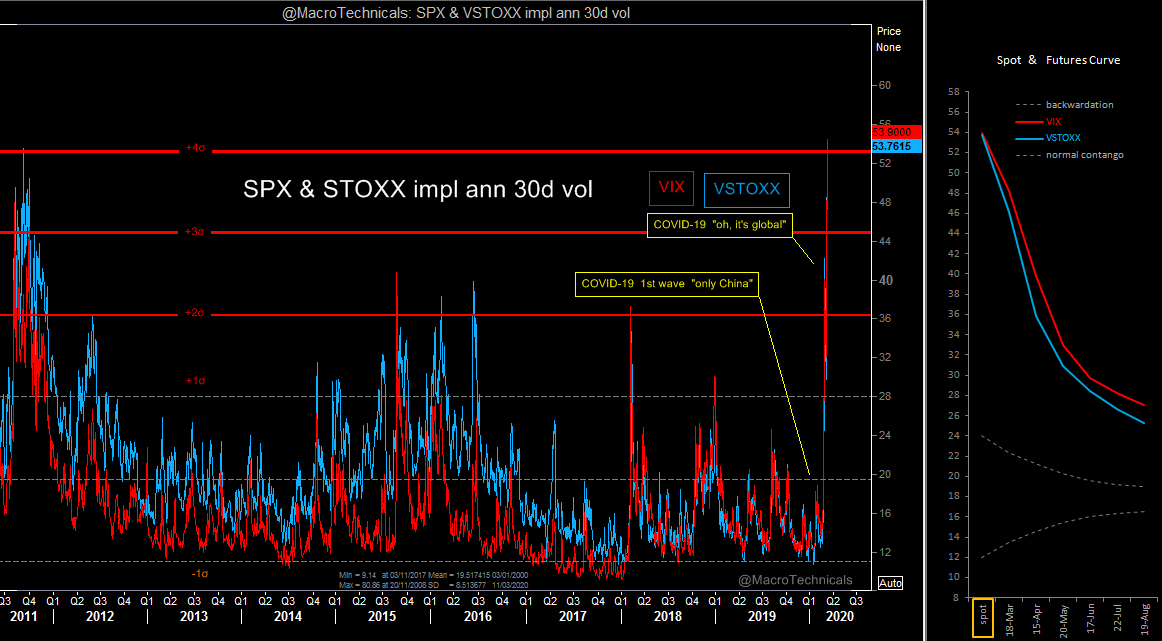

Similar sentiments in SPX and VSTOXX.

What happens next?

Okay, so what happens next? It’s clear that no one, not even the professionals, has any clue at this stage. Everyone is just selling first and asking questions later.

We did a quick poll on the Facebook Group earlier this week – and most of you answered not sure, stay in cash for now. The second most popular answer was buying opportunity, which is actually pretty worrying – more on this later.

What was my original buy signal? When does it trigger?

A couple of weeks back I published an article that set out my entire framework to approaching COVID-19. Do take a look if you haven’t read it already – but the gist is that this crisis is COVID-19 induced, and everything is tied back to the virus. Once the virus goes away, the problem goes away.

I then analysed the Hubei data and found that cases peak about 2 weeks after drastic measures are taken to control the spread. My theory then, was that one waits until drastic global measures are taken to control COVID-19 (lets call this Buy Signal 1), waits 1.5 to 2 weeks, and then buys in.

Note: There’s a really good article which shows that cases actually peak the day that shutdown occurs – but this only shows up in testing cases 2 weeks later. Really good read, well worth your time.

The way things are playing out, with Italy on shutdown, all European flights to US blocked, and US and Spain starting to really ramp up measures, I think we may hit Buy Signal 1 in the coming weeks.

Is the original buy signal still valid?

The problem now, is that the measures being taken to control COVID19 are going to hit the economy. I think we’re pass that at this point. Global air travel has plunged, China was shut for 1.5 months and struggling to recover, Italy is completely shut, Spain looks like it will be shut soon, rumours going around of NY about to be shut. Heck, even the Euros 2020, NBA and La Liga got postponed, and Coachella got cancelled.

So the question now, is whether the measures being taken, will impact the economy to the point where we see a bigger global recession. Because if we do, then the correct buy signal is no longer tied to COVID19, and it will play out like any other recession.

In other words – if COVID19 triggers a recession, then the correct buy signal is not tied to the virus situation, but the policy response from policy makers (that’s how a normal recession is played – let’s call this Buy Signal 2).

Last week I set out my base case for a global slowdown and recession in 2020. Over the past week, we’ve had a lot more information coming out to refine the base case.

I think at this point:

Eurozone

Probably already is in a recession, or will go into one very soon. Italy will be really badly hit. Spain a close second. Germany and France follow closely. Undecided on UK for now – but it doesnt look good.

US

US growth will slow significantly this year. Undecided on whether they have a recession. Bond market says about 60% probability of recession, which I don’t disagree with.

Japan

High chance Olympics will be cancelled / postponed. This will be a big hit to the Japanese economy. Consumption tax from last year really impacted consumption too. I think Japan goes into a recession, but this could be a close one.

China

China by contrast, is far better positioned than the rest of the world. They’ve dealt with COVID19, and now they’re free to restart the economy – albeit very slowly. China is trying to transition to a consumption driven economy, but for now they’re still very manufacturing heavy, and the global slowdown will hit them.

They have room to cut rates and stimulate if they want to, but what’s worrying is that latest commentary from top policy makers are signaling a willingness to accept slower growth. One of the top guys (can’t remember who) just came out to say that GDP growth doesn’t really matter, as long as China avoids instability, and people have jobs.

In China, policy signaling is everything, and the fact that top leadership is trying to shift the narrative to accept slower growth, is really worrying.

I think China may disappoint on stimulus this year, simply because they want to avoid inflating more asset bubbles.

So don’t count on China saving the world this time around. This isn’t 2008.

Rest of the world

Who does that leave us? Africa? Middle East? Latin America? South East Asia? These economies will not be able to pull the world economy out of the doldrums alone. And don’t forget that the oil plunge is going to wreck havoc on a lot of these guys too.

Will this spiral further? What really worries me?

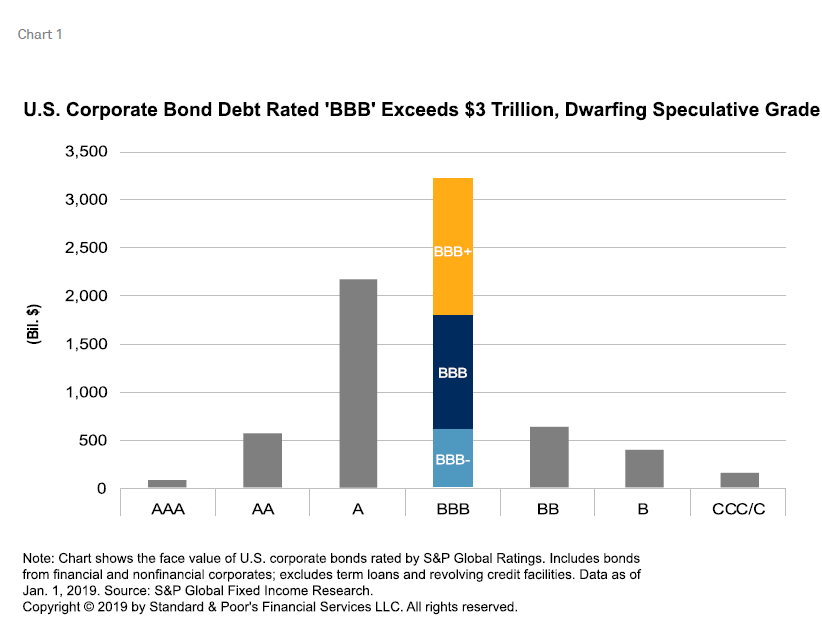

There are 2 points in particular that really worry me: (1) a US BBB corporate debt downgrade, and (2) Eurozone banks.

US BBB Corporate Debt Downgrade

This is what the US debt profile looks like. That huge $3 trillion BBB stack? That’s what worries me.

COVID19 is going to hit cash flow for many companies. Consumers are just going to stop spending. Oil price crashing is going to hit cash flow for many energy companies. Earnings will be impacted eventually (they’re mostly hedged, but refinancing will be tricky).

As this plays out, the credit rating agencies will need to start downgrading some of the BBB debt, in response to deteriorating cash flows and balance sheets. Once BBB debt hits BB, it becomes junk status.

This means that many pension funds and institutional investors are prohibited from holding them (can’t hold junk bonds). So they’re going to be forced to sell.

And when you look at the BBB stack, it’s bigger than the entire junk bond market put together. There is no way the junk bond market is able to absorb enough BBB debt once the downgrade starts happening. And once liquidity mismatches like that start happening, things can go back really quick.

Eurozone Banks

Eurozone banks are in a bad place.

A decade of low interest rates has decimated their balance sheets, and further rate cuts will hit their net interest income (NII). To add insult to injury, non-performing loans from COVID-19 are going to tick up in the coming months.

And these are global systemically important Financial Institutions (ie. Too big to fail).

Regulators will need to cut capital requirements for the banks soon, and that probably won’t even be enough. I think Eurozone banks will need big bailouts from the Eurozone governments in the coming months. That’s going to be tricky because the Eurozone is not the US or China where decisions can be made easily. The Eurozone comprises 27 nations, and it’s de facto leader Merkel has waning political influence in her home country Germany.

I think they will do what it takes eventually, but how we get there, could be a bumpy ride. Any small policy misstep along the way could lead to huge sell-offs.

Which Scenario materializes?

The million dollar question then – does COVID19 end (1) without a global recession, (2) a global recession (but not a huge one), or (3) does one or the above get triggered?

My current thinking for each scenario:

Scenario 1 (no global recession) – then the buy signal is easy. I start buying at Buy Signal 1, and ride it up.

Scenario 2 (global recession (but not a big one)) – then I buy at Buy Signal 2

Scenario 3 (one of the two events above gets triggered and starts playing out in a big way) – then there is a small possibility of a depression, and a huge risk off across all asset classes (bigger than what we’ve seen). I probably still at Buy Signal 2, but the cues to watch are slightly different – I use depression style economic analysis.

No one knows for certain of course. But at this point in time, my base case assumes a Scenario 2 style event.

I no longer think a V-shaped recovery is realistic. China has been instructive to show that once COVID19 is controlled, demand doesn’t spring back. And demand that was lost during the shutdown? It never comes back. COVID19 was bad, but the oil price shock was probably the final nail in the coffin. I have my thoughts on OPEC+ and why they did what they did, but that’s an article for another time.

Buy the dip strategies can be risky in times like this

The past 11 years has been a non-stop bull market – where every time the bull market threatened to end, central banks stepped in to backstop markets. This has bred a generation of traders and investors who are conditioned to buy the dip. After all, when stocks fall, just buy the dip, wait for central banks to backstop, and profit. It’s been the most profitable strategy over the past 11 years.

This kind of thinking can be dangerous. If you trace back to the 1930s great depression, a buy the dip strategy results in horrendous losses.

To be clear, I’m not saying that the 1930s will repeat, all I’m saying is that if you’re buying this dip, you need to at least understand why you think the economy will recover quick.

And I think this time around, central bank ammunition is highly limited. Fed Funds rate is 1 – 1.25%, so they only have 100 bps of cuts left. This probably goes soon. Eurozone is at -0.5 and they’re reluctant to cut any lower (for good reason – it will decimate the banks).

So the real firepower this time, needs to come from fiscal stimulus. But governments don’t act as quickly as central banks, so short term, we still need to wait and see. And the immediate term concern remains COVID19. Controlling COVID19 is the paramount consideration for global governments at this stage – fiscal stimulus can come later. Things like what Germany and the US announced yesterday will help, but it’s probably not going to be enough just yet.

What am I doing?

I exited a lot of positions last week and dialed back on equity exposure (as shared here) last week. I’ve also been reducing equity exposure (shifting to bonds and cash) since early 2019. But even then, but the rest of my equity positions have taken the full force of the selling this week.

Wish I sold more, but hindsight is 20/20!

I’m going to hold off buying the dip on this one. My base case has now switched to looking at Buy Signal 2 (policy response from policy makers) rather than Buy Signal 1 (drastic government action to contain COVID19)- and this being conditional on Buy Signal 1 being triggered.

Very simply – I buy when policy makers reveal large scale policy response (read: Fiscal stimulus, not monetary stimulus rubbish), on a scale that will be sufficient to offset the demand/supply shock from COVID19. And this is conditional on governments having first undertaken drastic public health measures to contain COVID19.

And in the meantime – I will sell into any big stimulus based rally.

I know that’s not saying a lot, but things are very fluid at this stage. I cannot predict with certainty how COVID19 plays out, nor can I predict how governments respond with respect to policy moves. They are all shifting probabilities at this stage – and updating at a rapid pace.

But as this situation plays out, I’ll continue sharing thoughts on Financial Horse, so do check back every weekend for my thoughts.

I could turn out to be wrong though, and COVID19 doesn’t cause any lasting damage. For those of you who think that way, you may want to think about using Buy Signal 1.

But for me personally, I’m worried about this one. I’m going to err on the side of caution here.

Btw for those are want to go back to basics, the FH Course is a great place to start. It’s a complete guide to investing for Singapore investors, covering shares, REITs, bonds, reading the macro cycle etc. Find out more here. We’ve updated the FH Course with exclusive Patron content on the virus, so if you bought the course previously, do check in for the latest materials.

FH Ask Me Anything

Huge shoutout to all Patron members the past week. We did an Ask Me Anything (AMA) series earlier this week, and the questions were absolutely top notch. Answering them was a true delight, and I think the answer could be really helpful to many investors out there. Do check it out here!

If you have any burning questions you want my thoughts on and are not a Patron member, you can also leave a comment on this post (but do consider signing up as a Patron – it’s just $5 a month for the premium articles, and really helps keep the site running).

Please no “Do I buy DBS now or wait for $19” style questions though. And also note that I can’t advise on your personal situation, so keep the questions general.

As always, stay healthy, stay frosty. Health is wealth. Never forget that. Live to fight another day. ?

What do you think? When will you buy into this market? Share your comments below!

Do like and follow our Facebook Page. We share great links and infographics there.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Join our Facebook Group to continue the discussion, we have a great community of people who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors. We genuinely think it’s the highest quality and best value investment course out there today!

Hi Mr Horse,

I’ve been a big fan for a long time, can’t afford the patron fees though but I’m very grateful for all the free analyses you put out. I’m graduating uni this year but I’m not doing anything financial related. Can I ask:

1. Do you mind quickly explain the difference in monetary and fiscal stimulus? I.e dyou mind explaining why trump’s latest stimulus won’t work?

2. I recently met someone from Temasek who recommended buying the dip and then continually buying and averaging down over the course of the recession. I understand this strategy is “safer” but would yield lower returns than “timing the bottom”. Any thoughts about this?

Hi J,

Good to hear from a long time fan like you. Don’t worry about the Patron Fees, it’s no biggie. Just support the site any way you can (share the link with your friends? 🙂

Don’t worry about not being from a finance major. Life is a long journey, just keep learning and improving yourself, it works absolutely wonders.

My replies below:

1. There’s 2 kinds of monetary stimulus. The first is things like interest rate cuts, the second is stuff like QE (Central Bank buys assets like bonds / stocks to prop up asset prices). Fiscal on the other hand, impacts demand directly. It could be government spending money to build roads, giving money to consumers (like what HK did), or student debt reliefs (what US did).

Trump’s latest stimulus help, but my view is that it’s probably too small to move the needle meaningfully. Covid19 will hit demand in a big way, so the fiscal package to restart demand has to be pretty big too. I could be wrong though. Let’s see.

2. Yes that is another way to do it. I would say new investors should go with the DCA approach – as long as they watch their emergency funds and income stream (don’t run out of emergency funds, and ensure you can keep averaging in – don’t lose your income stream). For those who want to try their hand at timing the bottom, the returns would be higher if they get it right. Get it wrong though, and the DCA guy may outperform. It’s a tough choice, but I wouldn’t have it any other way ;).

Hi FH,

Great article as usual. My view is slightly different for what it’s worth.

In my simplistic view, a recession is given. Simply put, there can be no economic expansion vs last year if a city or country is locked down or has significant social distancing for a few months as will happen almost everywhere. This is simple logic and no calculations are really required.

But this recession is tied directly to decreased consumer demand and a supply shock as a result of the virus so the removal of this trigger will allow self recovery of the economy to a large extent. Government measures are important mainly for sustenance of businesses and to avoid credit defaults and credit freezing and so the buy signal for me is still linked more to the state of the virus and the reactions of people to it then government economic intervention. When people feel safe or have mentally adjusted to the risk, they will go out and spend money. If they don’t, no amount of government stimulus will make them do so.

My assumption is that the outsized effect of Covid on daily life (not necessarily the economy) will be over within 2 years. One or a combination of the 3 things below will happen

1. Large proportion of population gets infected during next one to two years with vast majority recovering. People are no longer afraid.

2. Spread is slowed and people are still fearful but adapt to virus as part of life as we did with terrorism. Some norms may change like mandatory 2 week quarantine for visitors to any country which will ha e structural impact on some industries like tourism but large part of life goes back to normal. Humans will not tolerate home quarantine for more than a few months. Even during the Spanish flu, plays and dramas went on as usual with some precautions. Just look at the recovery in activity in Capitaland malls, back to 95% normal based on their data.

3. A vaccine will be invented in 1 year plus and many will have access to this.

The elephant in the room with regards to immediate disease progression and human reaction is the US. Without a functioning public healthcare system, strong central coordination and a fact based government, the disease will spread there in a rather uncontrolled fashion. The high inequality and personal levels of debt mean that many will not have access to affordable healthcare and many will have to work even when sick as they rely on the next paycheck for daily necessities. So situations of chaos, panic and lockdowns are likely. When the peak of this happens in the next 2-3 months, that for me is the time of maximum fear and also the time of entry. Why? Because the disease situation will resolve itself one way or another as stated above and as long as we don’t enter a depression, markets will inevitably recover within the next 3-5 years.

The big caveat is whether there is sufficient economic dislocation and a tight enough credit squeeze during the next 1-2 years to cause enough companies to go into bankruptcy and cause not just a recession but a depression. If credit squeeze and business dislocation is bad enough to cause the next Great Depression, we will have to wait 13.5 years to recover like last time. So don’t bet everything because the risk of this is higher than striking 4D, not negligible.

Your thoughts, especially on the credit situation?

Hi CMC,

Amazing point. I thought about this for a while, and my response below:

1. I think there’s no doubt we’re at the later stages of this debt cycle. Asset prices and leverage ratios are on the high side, and definitely signal late stage credit cycle.

2. The question then, is whether the current drop in asset prices, rise in credit spreads, and drop in earnings lasts for long enough to start triggering the classic deleveraging cycle we see at the end of every debt cycle.

3. If the answer is yes, then we have a classic recession, and normal recession style analysis applies – buy when policy makers step in in a big way.

4. If the answer is no, then I agree with you that we read the virus situation, and invest on that basis.

5. Nobody knows the answer definitively, but I’m inclined to go with a yes (point 3) because this COVID19 hits the entire tourism/hospitality industry, AND the oil industry simultaneously. The impact to earnings is going to be staggering, and none of the policy responses I’m seeing so far looks sufficient to offset this drop in earnings – they’re all targetted at reducing borrowing costs etc. But how are SMEs going to refinance in this market, when cash flows are declining, and credit spreads blowing out? $800b worth of BBB debt is coming due in the US this year, and that’s a lot of refinancing coming up.

It’s all just educated guesses at this stage, but I’ve seen enough to want to sell into any big stimulus rally, unless there is meaningful fiscal stimulus.

Love to hear your thoughts too. Anything I’m missing on this credit point? I think like you said, it all rests on how COVID19 interplays with the credit situation. Which is tough to predict because we don’t even know how COVID19 ends, nor do we know the policy responses from governments.

Hi FH,

Thank you so much for your insightful sharings.

My RM recently introduced me to Equity-linked notes where l get 10-12% annual returns and buy a ELN with basket of 4 shares. He said I’m assured of the monthly returns when if market falls.

After 8 mths, if my none of the stocks goes below ‘strike-in’ price (30% from buy price), I’ll get back my Full principal and keep the returns. However, if it does fall Below strike-in price, I’ll need to buy that stock at the original price when l first entered the ELN.

Appreciate if you can advise if l should go for this product as it seems a gd deal in current choppy markets.

Thank you.

Hi Jeremy,

Welcome to Financial Horse!

My view on exotic products like this – is that they aren’t necessarily a bad thing, as long as one is able to properly evaluate the risk-reward, and how it fits into their risk appetite and investment objectives.

I can’t advise on your personal situation of course, but for me, the considerations of such a product are:

1. Which are the 4 stocks and how would I pick them? What is my reasoning for using the 4 stocks when in this climate, stocks can fall 20% a day.

2. Will I be able to maintain sufficient cash on hand to buy the stock at the original price? Do I get to keep the stock in such an event?

3. Is the risk premium I’m being paid sufficient to compensate me for the risk I’m taking on on this trade?

I don’t have the full details of how this note works, so I’m not able to comment meaningfully. But I do hope that the questions above give you some insight on what to look out for when analysing the product.

The key is to understand exactly how the product works, and then evaluate the risk-reward for this particular product. There’s a nice case study in Korea of a product that seems very similar to this: https://www.thestar.com.my/business/business-news/2020/03/13/south-korean-exotic-notes-face-margin-call-risk

All good points. I think at the end of the day we probably need to think less about trying to buy at the bottom than to protect our downside. Regardless of whether we buy at your buy signal 1 or 3, one will make money when the market recovers eventually whenever it happens. But we must make sure we have capacity to hold when we buy and not be forced to sell if it falls further AND have the money to buy when the buy signals are reached.

On recession, there is no question we will have one. Businesses assess their monthly performance vs previous year by making adjustments for days closed due to public holidays. Even a couple days difference makes it difficult to show year on year growth. When you have a month or two of sales gone, whether it is car sales, property sales, hotel, airline, restaurant etc. you cannot grow for the year. But recessions can be caused by exogenous or endogenous factors and their recovery differs based on cause.

I agree with your assessment of the credit cycle which I need to weigh more in my thinking. Selling equities on the bounce makes sense, I have been doing this as well. Teh Hooi Ling whom I respect seems to hold a different view in today’s papers which I also need to think about. The big danger of selling to buy back later is lacking the guts to buy back when it is time to do so. During the depths of the financial crisis I was telling everyone to buy bank ETFs because while individual banks may fail, banking as an industry could not because it would destroy modern society but still I did not buy myself and take my own advice because of fear. So the head may be rational but the heart may overrule at the time of action and that is a real danger.

I have two important follow up questions

1. Would you also sell bonds – BBB and BB+ at this time?

2. Where would you keep all the liquidated assets? In cash, gold or govt bonds? I was not surprised to see gold down this week. My analysis of how gold reacted during financial crisis which I did before all this happened was that it fell for the initial months before recovering and outperforming the market in the middle stages so my conclusion was that it is not a safe haven in the early stages contrary to what many believe.

All very good, amazing points. Food for thought for me as well, and I will need to reflect on my strategy too. I agree that the key is liquidity, and actually buying back later is easier said than done.

My thinking for now:

1. I think each needs to be evaluated on a case by case basis. If I can get back close to principal, and the maturity is far away, I’m probably selling. If they are deepn underwater, and maturity isn’t too bad, and creditworthiness looks to be alright, I will hold.

2. Really tough one. I’m holding a mix of all 3 right now. I agree that gold goes down in the initial stages, and only comes into its own during the fiscal/monetary stimulus phases. For now, I think the relative safety of SGD looks good, and I’m holding onto a large chunk of the SSBs/cash/money market funds accumulated over the past 2 years.

Keen to hear your thoughts on qn 2. This past week has shown that there is no effective hedge in this liquidation panic.

I am not FH but I would urge great caution with this. You are basically selling the bank a put option to sell you those shares at strike price after 8 months if the prices fall more than 30%.

With the market behaving like this, what do you think are the chances of this happening?

So if you buy, you should be ready to accept the very significant risk that you will have substantial capital losses in excess of 30% and consider if the juicy 12% yield compensates you sufficiently for this risk.

Remember, the bank is out to make money for themselves and not for you by structuring such products. You can do something similar by just selling put options directly on the market and save the large spread the bank is earning from you by structuring this note. They have put all the risk on you and earned a hefty fee for themselves in the process. If shares prices don’t fall 30%, they make money selling the put and paying you only part of it. If they fall more than 30%, you are responsible for the loss, not them. Either way, they win. You win only in the first scenario but you win a lot less than if you simply sold the put directly yourself.

I agree with Chan Mali Chan. Very similar views.

It’s not that you can’t make money off such a product – It’s just that the bank definitely does not care whether you make money. So the burden is on you to ensure you understand this product very well, and understand fully the risk-reward. If you do, then this product could still make sense.

But there’s no denying this is a complex instrument. Many derivative PHDs are going to have big trouble evaluating the risk-reward on a product like that, given the current volatility in markets.

I fully agreed with your analysis and I like your game plan! My only deviation from you is dollar cost averaging based on my game plan. Since everyone’s situation and financial goals are different, there isn’t a “one plan fits all”… Good luck to you and all FH readers. BTW, I read your blogs weekly without fail, thanks very much for sharing your thoughts:)

Thanks for sharing your thoughts! All the best for your investments too. 🙂

I am 30% cash right now and planning to go to 50% by selling assets that are not down much like bonds or can be sold at a significantly lower profit than peak but still not at loss , e.g. sold Keppel DC because price had gone up so much previously and current yield of 3.3% does not justify current risk which shows it behaving totally like stock subject to 7% falls in a day. Started crisis at 25% cash because I had been anticipating one for last few years. Means I could have profited more from last year’s equity rally but also means I don’t have to panic sell now so there are tradeoffs.

Reason why I want to go to higher cash level is so I will have guts to buy when the time is right. If I have 50% cash, I will hopefully feel confident enough that 20% can last me a few years to deploy 30% back into the market. Key to coming out ahead here is to deploy more back than you take out when it is time to buy. Otherwise, you have only locked in your losses or lower profits.

I didn’t sell any shares during dotcom bust or 2008 Financial crisis and both cases worked out well so not selling is also a good strategy. Each time something like this happens, we always worry about Great Depression but so far it hasn’t recurred.

This time I am selling some because unlike previous 2 major crises where one could not predict when upturn would happen, here it is somewhat predictable that it will not happen in next month or two as virus disease pattern is predictable. So selling now is not a big risk. The big risk is not buying back later and it is indeed a real and substantial risk. My mistake in 2008 was not buying when I had the chance to do so. I hope not to repeat that mistake but we never know until it actually happens. Everything else is theory. It is hard to buy when the world seems to be crashing and no one can predict if your job is stable in such situations no matter how well you perform and how strong your company is.

What’s your target equity allocation now? Down from 30% I assume?

All very good points. I will think about them in the days ahead – and hopefully incorporate into future analysis. Equity allocation dropped slightly below 30%, but the more I look at the situation the more worried I am about the days ahead. If there is any stimulus rally this week, I may use it to derisk further.

Hi,

Are you still holding on to your REIT positions? Last we chatted, your strategy was to hold on at least for reit.

Significantly reduced hospitality exposure 2 weeks back. Holding rest of the REITs for now, but my thinking is very fluid – I may change my mind if prices rally slightly!

To sell on panic (= market timing) seems never an appropriate approach to investing. Investing to retail investors should be made up of good (=well diversified), large and very cheap passive indexing stock ETFs bound and a bit (5-10%) physical gold for crisis. Bonds or bond ETFs seemed dangerous and/or expensive for a long time now.

Agreed. No denying that what I’m doing is market timing. Let’s see if this performs better than a plain DCA. 😉

Holy crap that article. 8 billion USD of ELNs in the Korean market betting on low volatility, sold to elderly people. 8 billion!

Yeah! The dangers of using derivative if you don’t know what you’re doing!

Hi Frankie,

You are absolutely right and just buying ETFs and holding is the best strategy without trying to time the market.

In this case, I don’t consider selling now to be timing the market but acting on information before the market does. Bear with me. Previous crises like 2008, 2001, 1987 were caused by economic reasons like subprime crisis, dotcom overvaluation and automatic trading so the direction of the market and when it would rebound was unpredictable.

This time the crash is caused by a real world problem whose evolution is utterly predictable for those who are scientifically trained and we should look to the doctors and scientists to understand this rather than the economists and fund managers who can’t get into the details of this. The virus is expected to increase the number of people infected by ten times every 19 days if spread is not controlled. The problem is not the mortality rate but the ICU rate overwhelming the healthcare system. Between 5-15% of patients infected will need ICU care. There are 45000 ICU beds in the US of which 30000 are usually taken up at any one time. The disease has been spreading uncontrolled in the US so far due to lack of testing. Within a month or at most two, the US will be in the same situation as Europe with health systems under severe strain or overwhelmed. There is no way to stop this now short of severe social distancing measures. Economic activity will be severely curtailed when this happens on a scale not seen in recent memory. Yet the market is down less than 20% after the Friday rebound. So while we can’t predict when the sustainable rebound will happen and there will be unpredictable intermittent rebounds, we can predict with a pretty high level of confidence that the real world situation will get a lot worse in the US, the most important market before it gets better and markets will follow this so markets will go down a lot more before they recover. In this real world rather than financial market induced crash, follow the science and whats happening in the medical world rather than the finance experts. The financial analysis is frankly less relevant than the medical analysis.

The market is still behaving in a schizophrenic fashion because fund managers and traders havent decided yet how bad things will get. But the infectious disease experts and epidemiologists already know the answer to this.

Guess the Fed move on Sunday has just proved my point. Unfortunately, now market will plunge on Monday and likely too late to sell anymore so now just have to hang in for the ride.

As Jon Snow would say… “Winter is coming”.

Feds blew their entire ammo and markets barely budged.

FH, one other thing you can do is short the market with a 3x leverage fund. I am doing this now. But get out after a month because after that we dont know if exponential increase in US cases will continue.

Interesting, how’s the performance been so far?

I think there is a risk short selling is banned in the coming days.

I would advise against short selling using an inverse fund, ESPECIALLY a leveraged one. Remember that even in a bear market, the trajectory is almost never downwards. A massive relief rally, like what happened on Friday can destroy your position. I know this because I was actually holding some SDS on Thursday into Friday. Managed to get out of that position before being burned though. If you do want to take up a short position, I would strongly advise using Put options, at least a couple months out and fairly close to the money. Make sure the IV isn’t too high when you buy in, if not the premiums just are not worth it. You can actually use a relief rally to strengthen your short positions since the premiums on puts will decrease.

Great comment Andrew, thanks for bringing this up. Hope to see more comments from you going forward! 🙂

Chan Mali Chan – Just to add that the leveraged short funds are not designed for longer term holding. They were intended for intra-day trading, and holding for longer than a few days lead to big decay.

Agree that a better way to short would be via put options, especially for longer periods.

Hi FH,

Thanks for your great sharing of insights!

Prices of REITs are battered down by more than 20% from their high, and yields are getting very attractive.

I am looking at US office REITs where properties are mainly freehold and with long leases.

No doubt that their performance will be affected by the stability of their tenants during this crisis – which is very hard to predict.

What is your personal views on REITS with long leases (eg. office REITS) in the current situation?

Personal view is to stay out of the market until things calm down. 😉

Impossible to break down the full economic impact of what is about to happen.

Hi Andrew,

Thanks for your sound advice on shorts. I have always been a long investor so this is new for me. As mentioned, I have never thought one could predict the market direction except in this case given it is driven by a predictable real world phenomenon.

FH,

Just read Ray Dalio’s Big Debt Crisis book and it is terrifying. Looks like this real world crisis is likely to lead to a financial crisis and a non-beautiful deleveraging. This silly Fed keeps surprising the market even after the nice rebound on Friday and their sudden, unexpected actions only stoke fear rather than send relief. Credit markets have frozen because of them, hope we dont see bank runs soon.

So, lets assume a depression is coming. The scenario Ray described about being overly indebted and central bank out of ammo has occured.

What are your next moves now?

I’ve been rereading Dalio’s book recently. Lots of great insights. Looks like the US plays out as an deflationary depression, EM plays out as an inflationary depression.

I’ve been stocking up on gold. But that’s more of a mid term position. Short term, I’m just going to cash and hunkering up. Market is falling apart, unbelievable liquidity mismatch across all asset classes.

With Feds cutting 100bps last night, US Treasuries are no longer a good hedge. They become nothing more than capital preservation – cash. Which means that every single MPT based portfolio strategy now needs to be rethought.

Sorry I meant to say recession. Depression is a by no means guaranteed.

Hi FH,

Read in detail the section in Ray Dalio’s book on the Great Depression and my conclusion at the is that the chance of this happening is pretty low. Both 2008 and Great Depression had in common bank failures and I think we are still some ways away from that although most worrying part of Fed announcement was waiving of Bank capital requirements. Great Depression also had complexity of gold standard and inability to print money. Whole process took a few years to play out so we still have time to react.

Liquidity challenges probably caused by lots of people moving to cash at same time but hopefully impact of QE will loosen this in a week or two. It did when it was applied during Great Depression.

Anyhow, recession is much better than depression. I laugh at those economists or analysts surprised by China’s 22% drop in retail for Jan and Feb and who projected -1%. This comes from looking too much at Excel models and not thinking. If place is locked down, of course drop will be severe. It was probably much worse in Feb if one takes apart the numbers.

Danger is still deleveraging at end of long term credit cycle but virus induced effect will be relatively short lived. For me short lived means 6 months to 2 years. Either most will get it or mankind will adapt. Probably countries who manage to contain keep borders open only to other countries who manage to contain or whose population has developed herd immunity from widespread infections that have resolved. Worse period probably in next couple of months as it soars towards peak in the US and Europe.

There is actually a relatively simple solution to all this. The world just needs to coordinate a 3 week period where the entire population stays home except for essential services. Then virus will be almost completely stopped. Practically speaking don’t think politicians will be able to pull that off so it will be a longer drawn affair country by country.

Anyhow, I view this as overall a great opportunity to rebalance my portfolio towards all those great companies which were too expensive to buy previously once they have been appropriately discounted by 50-70%.

The inflationary recession you mention in EM could play out as a repeat of Asian Financial crisis of 1997 if companies can’t pay USD debt and Asian currencies depreciate.

Reading the book in detail, I understand why the Fed did what they did and think they are good moves but the way they announced it leaves much to be desired. Always bad to surprise investors on a weekend and just scares them.

What about once things stabilise a bit? It looks like this time we have really reached the end of a long term debt cycle. While we may not enter into a depression, it is sobering to think that it took 25 years for Dow to recover that time.

With all the unwinding that still needs to happen, even without a depression, there is a fair chance we end up in a Japan type slowdown in the US which could also last decades. Japan’s stock market hasn’t gone back to its peak since.

In this situation, it may not make sense to buy equity even after things stabilise. Just hold on to cash and as things deflate, they get cheaper. All the negative interest rates, QE etc. hasn’t done a thing to change the trajectory for Japan.

Ray Dalio’s book talks about what governments should do in an unwinding, not so much individual investors.

Thoughts?

I think it’s too early to say with certainty. My thinking for now is to never write off the ingenuity of the human race. With the lessons of Great Depression behind us, I am confident we will eventually recover again. There are massive engines of growth coming from China, ASEAN, Africa and Latam. There’s a new generation of people hungry to be propelled into the middle class. They will want to buy the best electronics, see the world’s best sights, and eat the world’s best food. I wouldn’t write off humanity just yet. 😉

The other question here, is that if you don’t buy equities, what is the alternative? Real estate? Precious Metals are good stores of value, but they don’t generate cash flow over longer periods of time. Bonds are going to have negative real returns going forward. Cash will lose its value to inflation. I think a balanced portfolio still makes sense, and that means some allocation to equities.

True unless there is no inflation but deflation like in Japan. It is hard for us to understand since we only experience it in theory and not practice but my Japanese friends were experiencing flat pay or pay cuts every year and were still better off in real terms because of deflation and were not complaining. After 30 years, the Japan equity market has still not reached its previous peak.

It’s a strange world with negative interest rates. Now Japan, Europe and US have negative real interest rates. Hard to make sense of this new world.

From Ray’s book, it seems that ingenuity of humans could not beat the greed of humans and massive debt write offs had to take place every 50-100 years from Jubilee year of Romans to Imperial China, whatever the culture. Japan handled their asset bubble with 3 decades of deflation, maybe the western world is next. Perhaps we need to look more closely at equity market of China where there is still lots more growth needed to bring GDP per capita to developed world status. On the other hand, US internet giants are making the whole world their market and no one can compete with their scale.

Definitely not Singapore real estate in any case. We are in the middle of our own asset bubble here and we will hear a big pop by 2022/23 if not earlier.

FH

Looks like your buy signal 3 came before buy signal 1. So which one will you follow?

My buy signal 2 was conditional on 1 being triggered first. In any case, not so sure if this package is enough.

So does that mean you are not buying yet? What’s your latest thinking on entry timing? I am starting to nibble very selectively and in small quantities while keeping my war chest tightly locked and monitoring ratio of cases to ICU beds available in the US. Looks like severity of situation has sunk in for everyone now so can’t be certain market will definitely fall further like I was last week.

But if ICU beds overwhelmed and people end up in hospital corridors without treatment, panic could ensue. At this point, think that is still more likely scenario.

I’ll try to see if I can share more thoughts this weekend. 😉

Anyway, thanks for the article on 3 actions to take reminding us to relook portfolio allocation and make sure we were comfortable with it. It helped spur me to actually take action instead of just telling myself to take action which helped save me a tidy sum assuming I have the guts to put it back in market later. I have a bad habit of predicting what will happen and what to do fairly well but not actually taking the actions that I say I should take and suffering the consequences. Inertia is strong.

Really glad that it has come in helpful for you! 🙂

After the week that we’ve had. I really look forward to your weekly post tomorrow!

Should be out tomorrow morning! Just released on early access for Patrons. 🙂