I’ve been hearing a lot of talk about a Fed pivot recently.

It’s been coming from a lot of strategists that I respect, and is also what is being priced into the market now.

So it is probably worth spending some time to discuss this.

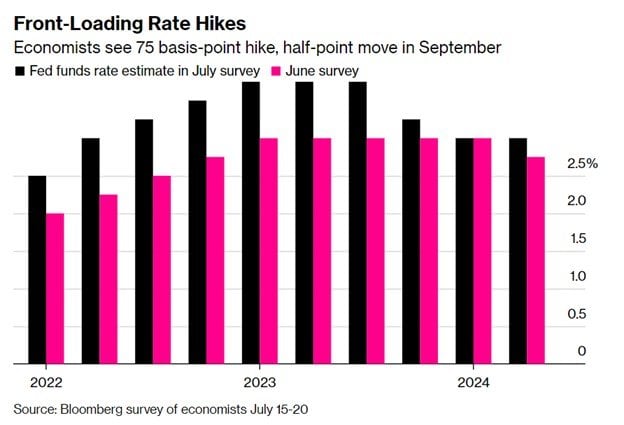

Basics: Fed Pivot coming soon?

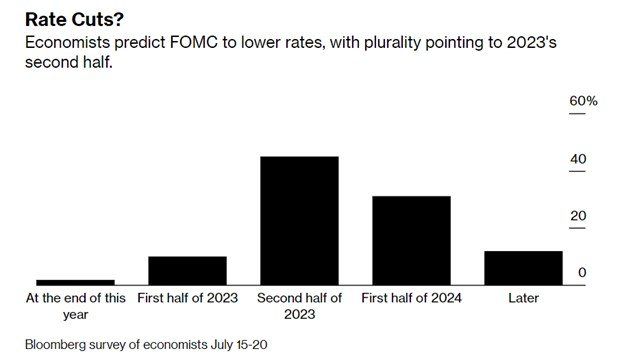

The crux of this view, is that US interest rates will peak at 3.75% in early 2023, following by interest rate cuts in the second half of 2023:

There are 3 reasons why this could happen:

- Equity markets start to melt down

- Credit markets melt down

- Inflation goes away

1 and 2 are not something we need to worry about, because if that happens it indicates the bottom lies in the future, and there is no need to buy yet.

But many commentators, are arguing for 3.

They argue that inflation has peaked, or at least will peak in the next 3 – 6 months.

Which means that by early 2023, a rapidly weakening US economy, coupled with declining inflation numbers, will allow the Feds to turn less hawkish on monetary policy, and start cutting rates in the second half of 2023.

This is basically a soft landing kind of view, where the Feds will succeed in taming inflation without causing a major recession.

If you subscribe to this view (and I know many who do), then you would think we are very close to the bottom in stocks.

And you should probably be buying around now, or at least over the next few months.

My personal view – Fed Pivot will come, but not the way the market is pricing in

For the record, I personally do not subscribe to this view.

I think the calls for a Fed Pivot are a bit too early.

The reason why, can be summed up as follows:

- Inflation is sticky

- Wage growth is strong

- Historical Precedence is not pretty

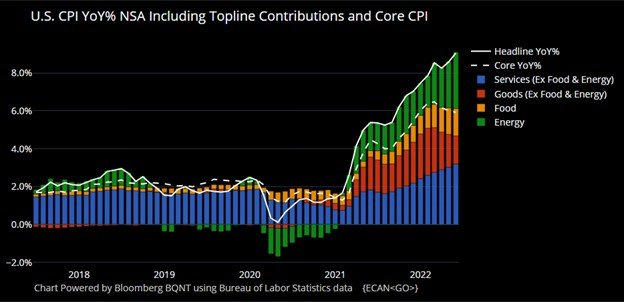

1) Inflation is sticky

You can see the breakdown of the inflation components above.

Oil prices have come down the past month, so we should see energy inflation coming down.

Goods inflation may start to come down too, as supply chain disruptions start to heal.

But both services, food, and rental inflation are unlikely to roll over just yet.

The labour market is very tight, food inflation will stay high due to the Ukraine war, and rental inflation is still going strong because housing supply is tight in the short term.

So yes – we may see inflation coming down from the 9.1% headline number.

But will it go down to 2-3%?

Questionable.

More likely than not inflation stays at an elevated range for a while, say in the 5-6% range.

Will that be enough for the Feds to pivot?

The problem though, is that if financial markets and economic growth do not deteriorate significantly, then why would the Fed turn dovish with inflation at 5%?

The pain is low, so why give up the chance to tame inflation once and for all.

As with government policy, central banks are usually slow to change their mind. They wouldn’t want to change course until it becomes clear that their current path is unsustainable.

So the way I see it, if inflation stays at the 5-6% range, they won’t dial back on hikes until financial markets start to melt down or economic growth deteriorates materially – which we have not seen just yet.

2) Wage growth is strong

At the same time, the labour market is very strong, as are household balance sheets and consumer spending.

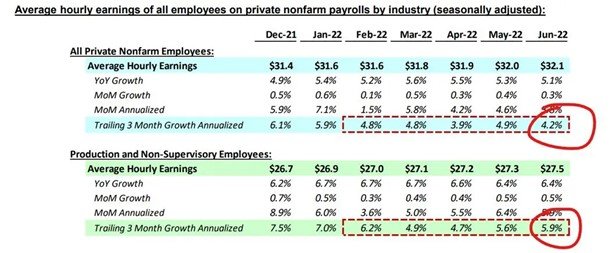

US Nonfarm payrolls in June increased by 372,000, topping the 250,000 estimate.

Average hourly earnings increased 0.3% for the month, which works out to 4-5% annualized wage growth.

In plain English, wage inflation is showing no signs of rolling over just yet.

Employers are still willing to increase salaries to hire new employees, to combat the tight labour market.

Until wage growth starts to roll over, it’s quite hard to see a recession.

At the same time, household balance sheets are very strong, and consumer spending is still holding up very well.

Sure, they’ve come down from the COVID highs, but they’re nowhere near “recessionary” levels.

I agree a recession (or economic slowdown) will come, I disagree on the timing

For the record – I completely agree that all this is coming.

I agree the labour market will slow, and inflation will come down, and economic growth will slow.

Because that is exactly that the Feds want.

The inflation problem is caused by a mismatch between supply and demand.

The Feds cannot do anything about supply.

So they have to crush demand.

If the consumer keeps spending, if the job markets hold up strongly, then that demand doesn’t come down meaningfully.

So the Feds will have to keep hiking and keep tightening, until that slowdown starts to show up in the data.

3) Historical Precedence is not pretty

Stanley Druckenmiller gave an interview recently where he cited a number of interesting statistics:

- Once inflation gets above 5%, it’s never come down unless the Fed Funds rate is higher than the CPI (consumer price index)

- Once inflation gets above 5%, it’s never been tamed without a recession.

With inflation at 9.1%, it suggests Fed Funds rate may have to go as high at 9% to truly tame inflation.

Of course, you can argue that this is crazy talk because the world today is not like the world in 1970s.

The world has a lot more debt today, and if interest rates go above 5% we’re going to have a global economic meltdown.

And I agree.

The question though, is whether a terminal rate of 3.75% is sufficient to tame inflation of 9.1%, as the market is pricing in.

Because of the 2 points shared above, I’m not so sure it will be enough.

I think the Feds may have to go higher than 3.75% if they truly want to contain inflation.

We could see a terminal of 4% – 4.5%.

What if I am wrong?

Could I be wrong on this call?

Absolutely.

When you try to predict the future, you always have to account for the possibility that you could be wrong.

Let’s imagine that I am completely wrong on this.

Let’s say Inflation rolls over in the next 3 – 6 months, and comes down to a very respectable 3% by early 2023.

The Feds dial back in interest rate hikes, and start to cut by mid 2023.

What do I want to own in this scenario?

Short Term (6 – 12 months)

There are many ways to play this trade short term.

You can:

- Short USD

- Long a curve steepener

- Buy long duration equities (REITs, growth tech, crypto)

It’s basically a repeat what worked the past decade, before COVID.

And we’re actually seeing this trade play out over the past week or two, as the market starts to price in this Fed pivot scenario.

Mid to Long Term (2 years and beyond)

In the mid to longer term though, I think if this scenario plays out, inflation may rage strongly in the mid term.

And I would want to own inflation hedges:

- Treasury Inflation-Protected Securities (TIPS)

- Energy (Oil & Gas)

How am I positioning?

I’m not so keen to play the short term trade here.

My view is that the economy proves more resilient than markets are expecting. Which means the Feds need to go higher and longer on interest rate hikes than the market is pricing in.

This trade is the exact opposite of what you want to do if you think the Feds are close to a pivot (which is to bet on rate cuts).

So short term, I’m inclined to just stay out for now, until more data comes to light on which course will play out.

While I hold elevated cash positions, I am not fully out of this market, so I do benefit in the event I am wrong and the Feds do indeed pivot.

But if you shift out into the medium term though, then long inflation (long TIPS or long commodities) starts to become an interesting play which benefits in both scenarios.

If we do have an early pivot from the Feds, it would mean a soft landing. Which means a strong economy, which means demand comes roaring back – as does inflation. Energy should benefit in that scenario.

Whereas if indeed I am right that the economy is more resilient than markets are expecting, then energy may recover as well due to tight supply conditions, given that everyone is pricing in an immediate recession.

So energy could be an interesting add, which could do well even in both scenarios.

Opportunity cost of sitting out of this market has gone down…

With interest rate hikes over the next few months, you could be looking at Singapore Savings Bonds with a 1 year yield of close to 3% by end of the year.

That’s a 3% return, completely risk free.

I could be wrong about this, but with the way the macro is shaping up, I find the opportunity cost of being out of this market much lower than it used to be in the past.

Whereas a lot of warning signs are starting to appear on the horizon.

Fed Funds rate at 3.75% alone could cause a lot of pain for emerging markets, similar to the kind of pain from the Asian Financial Crisis.

Compounded with rising food and fuel prices we could see political instability in many emerging markets. Sri Lanka could just be the tip of the iceberg if this keeps up.

And if the Feds do go higher for longer (beyond 3.75% for 2023), you don’t want to be caught too deep in financial markets when that happens because losses could be horrendous.

That’s the kind of climate where holding a bit more cash isn’t the worst thing in the world.

If I am wrong and the Feds pivot soon, then okay maybe I don’t catch the bottom and buy 10-20% off the bottom. But that’s not the end of the world is it?

If I buy only when the Feds make clear their intention to pivot and cut rates, I should still be able to capture a decent portion of the subsequent bull market.

Ultimately goes back to individual risk appetite

So I’m inclined to err on the side of caution here.

By staying underexposed to markets, the worst case that happens is I miss out on 10-20% of gains, and I just earn my 3% yield on SSBs. Not the end of the world.

But if I am right, I could be sitting out pretty big losses that are to come.

So while I would probably err on the side of capital preservation here, this ultimately has to be a personal decision.

For those who are keen to take risk, there are many opportunities in the market. Cyclicals, commodities, China, I think all of these could be candidates to be traded in the short term.

But don’t forget that a 2023 recession is very likely at this stage – so you do not want to overstay your welcome.