For those of you who bought DBS below $20 in 2020 (like me), we’re sitting on a cool 100% return today.

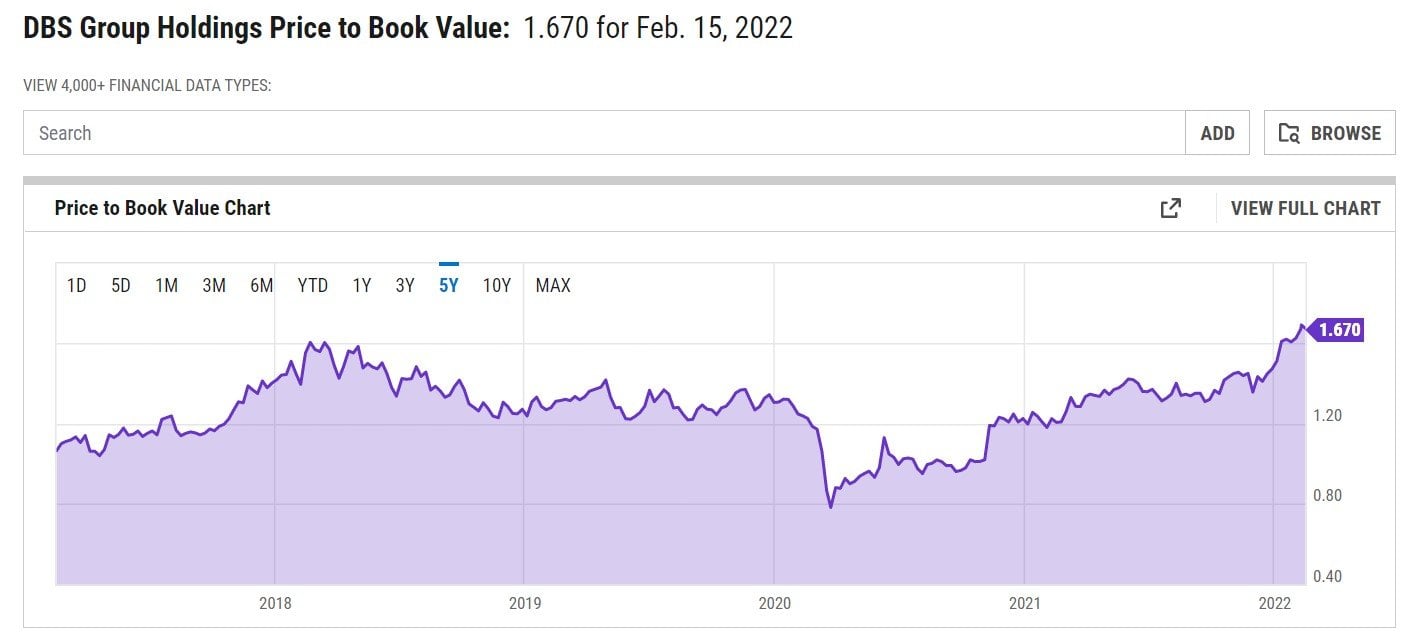

But – with DBS at $36.5 today, that works out to a stunning 1.65x book value.

The last time it was this high?

April 2018.

DBS then fell 45% over the next 24 months.

I mean just look at the long-term chart of DBS below.

Banks are about as cyclical as it gets.

So the million dollar question… is it time to lock in those profits, and sell DBS bank stock?

3 Reasons to sell DBS Bank stock (or UOB or OCBC bank stocks)

1. Banks are cyclical

Banks are about as cyclical as it gets.

Look at the 20 year chart of DBS – if you can sell DBS at the red arrows, and buy it back at the green arrows later, you’ll easily outperform the market many times over.

The hard part though, is trying to identify the red arrows, ahead of time.

So I dug a bit deeper, and these are the times when you want to sell DBS:

Red Arrows (sell)

- May 2007

- July 2015

- April 2018

- Feb 2022?

And these are the times when you want to buy DBS:

Green Arrows (buy)

- March 2009

- Feb 2016

- March 2020

With the benefit of hindsight, the way to identify the red arrows, is to look at the peak in US interest rates (see blue arrows).

For the record, the US Fed Funds Rate peaked at:

- 75% in Sept 2007 (4 months after DBS peak in May 2007)

- 5% in Dec 2015, first rate hike then paused for 1 year (5 months after DBS peak in July 2015)

- 5% in Dec 2018 (8 months after DBS peak in April 2018)

Now for obvious reasons, I get that this is a simplistic analysis. There are many reasons behind a peak in US interest rates, and it may also be linked to slowing economic growth, yield curve inversion etc.

But I encourage you to stay big picture here.

DBS tends to top out about 4 – 8 months before the peak in US interest rates

So in other words, if you think the Fed hiking cycle will peak in late Q3 or Q4, then you might want to start selling bank stocks like DBS in the coming months.

2. Valuations for DBS Bank are back at 2018 peak

When you look at valuations, things are equally worrying.

DBS now trades at 1.67x book value, which is actually an all time high.

The last time it was close to this high?

April 2018 – the high for the previous rate hike cycle (red arrow).

3. If you think the market is mispricing growth stocks or REITs…

Many of you have reached out to share your views that you think growth stocks and REITs are a fantastic buy now.

Your view is that with the market now pricing in 6 rate hikes, any hawkishness from the Feds is completely priced into the market.

And if in the event that Jerome Powell decides to hold back on rate hikes, for example because of a war in Ukraine, or fear of crashing the market.

Then well, growth stocks and REITs are going to fly once the market prices in anything less than 6 rate hikes.

I have my own views on this, but let’s just play it out for now.

If you subscribe to this view, then you probably also think DBS is overvalued.

If the market is valuing DBS on the basis of 6 rate hikes, then if we get anything less than 6 hikes DBS is going to sell-off.

Remember – banks like DBS do well when interest rates go up, because their net interest margin from lending money (their core business) goes up.

3 Reasons to hold (or buy) DBS Bank Stock (or UOB or OCBC bank stocks)

So those are the reasons to sell DBS.

As I was typing those out though, it occurred to me that there are some key flaws in the arguments above.

So let’s present the counterarguments below.

1. Interest Rate cycle has not peaked yet

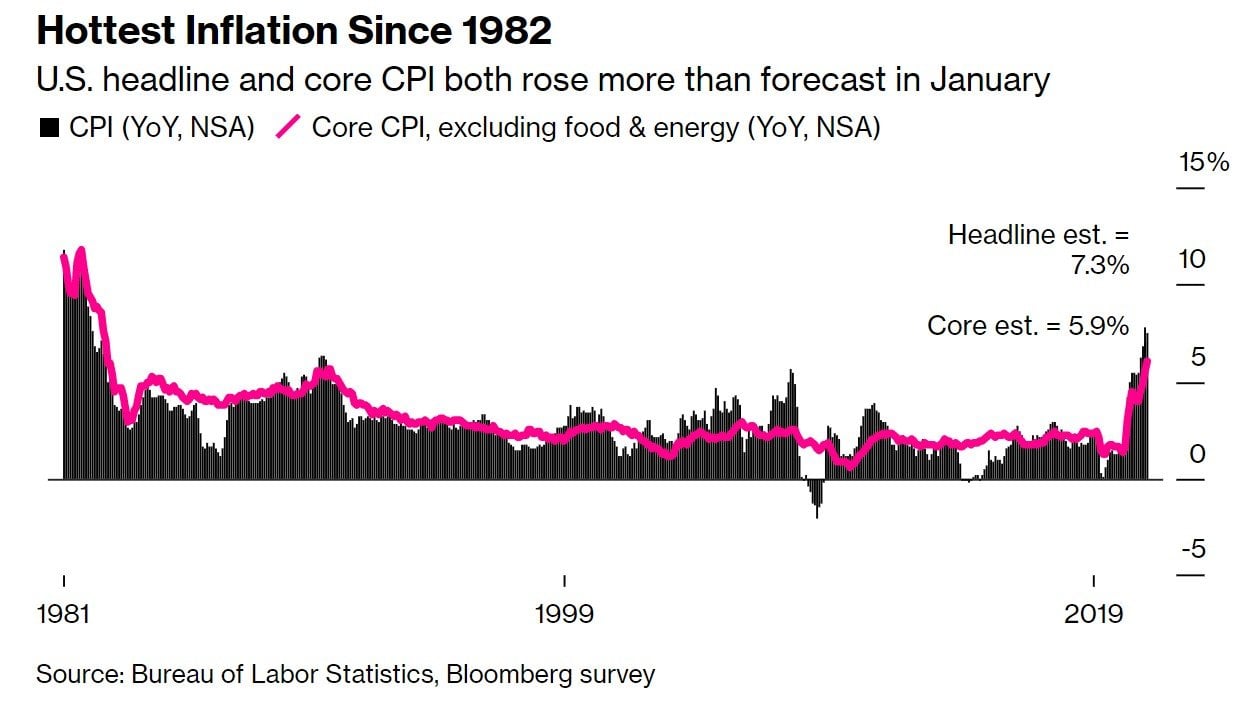

The argument here, is that with US inflation running at 7.5%, and the hottest in 40 years, we are not at the top in interest rates.

Personally for me I subscribe to this view.

I think that with inflation running this hot, the Feds will need to tighten financial conditions by raising rates, and by quantitative tightening.

And because monetary policy has a 6 – 12 month lag time, by the time slowing inflation starts to show in the official numbers, the damage would already be done.

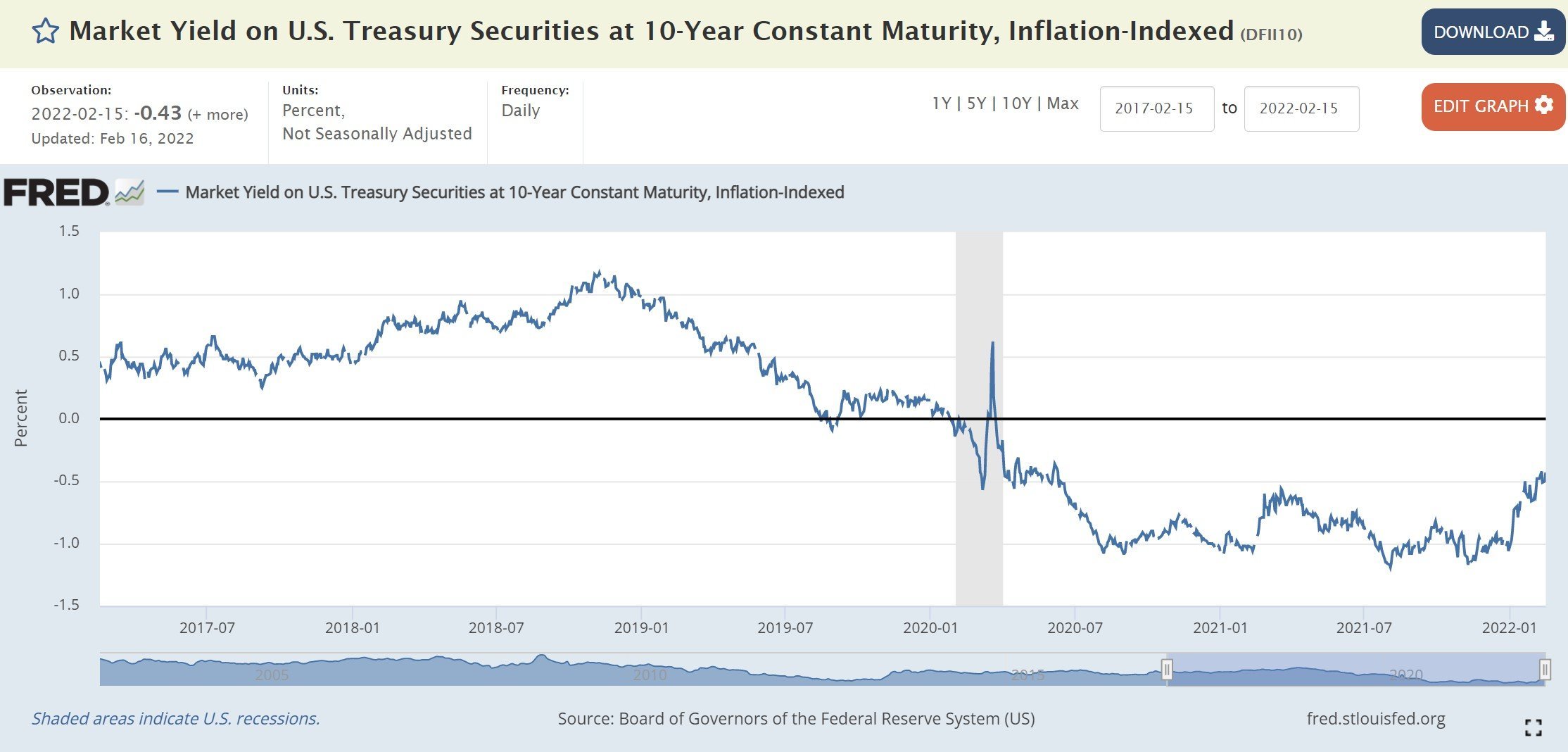

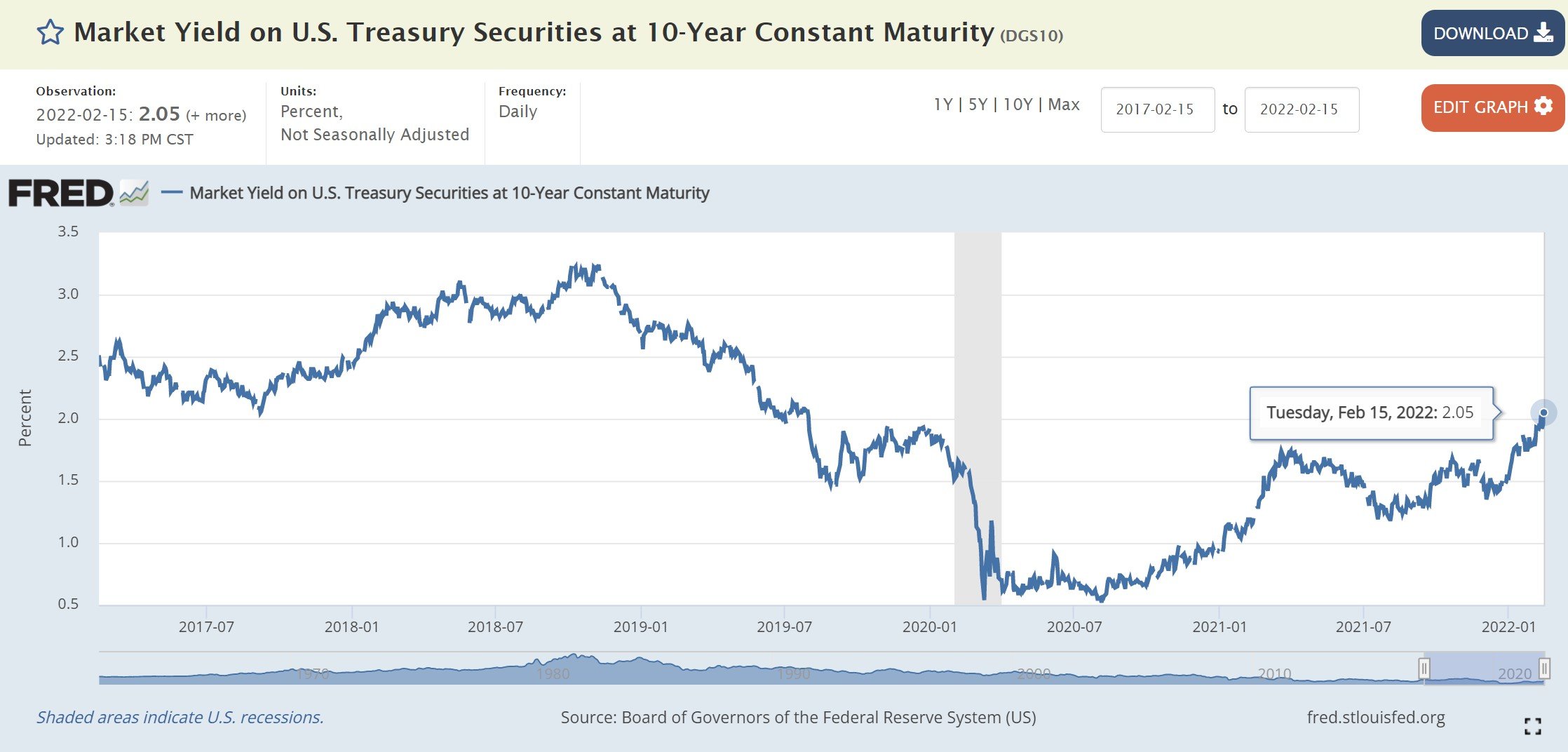

My personal view is that the cycle top this time around is 2.25-2.5% on the 10 year treasury, or 0% real rates.

We are at 2% on the 10 year treasury now, which means we are still 0.25% – 0.5% away from cycle top.

It’s for this reason that I have not started buying growth stocks or REITs, and am still holding onto my bank stocks.

But… market is pricing this in?

Of course, some of you may point out that the market is already pricing in 6 hikes at this point, so any less than that and we get a big relief rally.

The response to this argument is a bit technical.

It’s that for DBS, it really doesn’t matter how many rate hikes the market prices in in 2022, as long as the terminal interest rate is the same.

For the newer investors, the terminal interest rate refers to the long term interest rate that the market believes it will settle at. You can think of it as the number of rate hikes the market thinks is required to tame inflation.

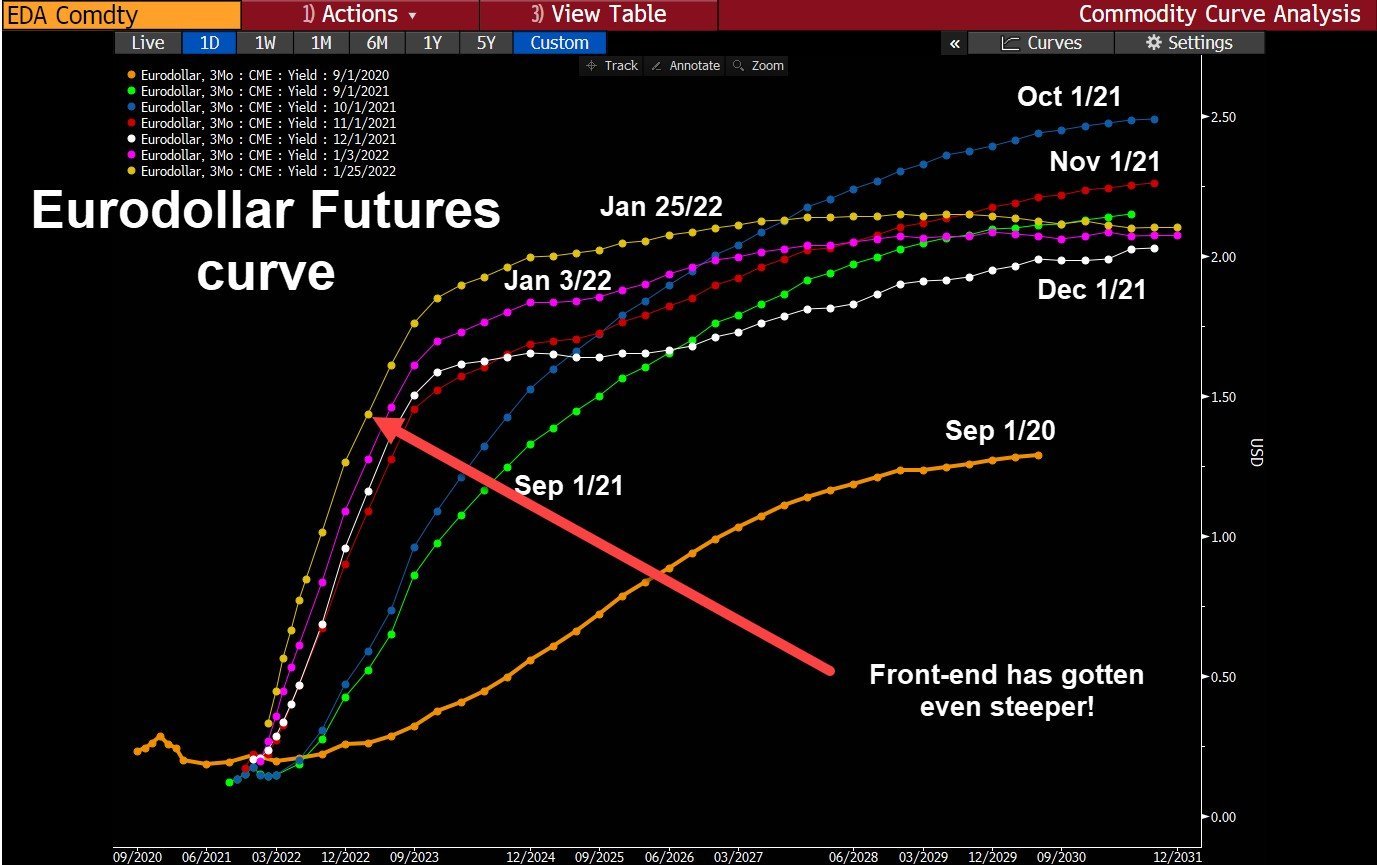

If you look at how the Eurodollar futures curve (basically market prediction for US interest rates) has evolved over the last 6 months, it paints a fascinating story.

In September 2021 (green line), the market believed the terminal rate to be 2%, but it expected us to only get there by 2028.

In November 2021 (red line), the market still believed the terminal rate to be 2%, but expected us to get there much faster by 2026.

By late Jan 2022 (yellow line), the market still believes the terminal rate to be 2%, but expects us to get there as soon as 2024.

To sum up:

- The market thinks that the amount of rate hikes required to tame inflation has not changed a single bit

- BUT – it now expects us to get those rate hikes much faster.

Or in plain English – The market is now pricing in a much faster rate hiking cycle, that will end much earlier.

The reason why this matters for DBS, is that even if you think the market is wrong about 6 rate hikes in 2022, the market is adamant that the total number of rate hikes to control inflation doesn’t change.

The only difference is the time it takes to get there.

Which means that even if the market is wrong on 6 rate hikes, all we may get is a mini sell-off in DBS, followed by a recovery once interest rates continue their march up.

That’s probably not good enough a reason to dump DBS stock.

2. DBS Bank Earnings are rock solid

Okay I get it.

DBS’s latest earnings are rock solid.

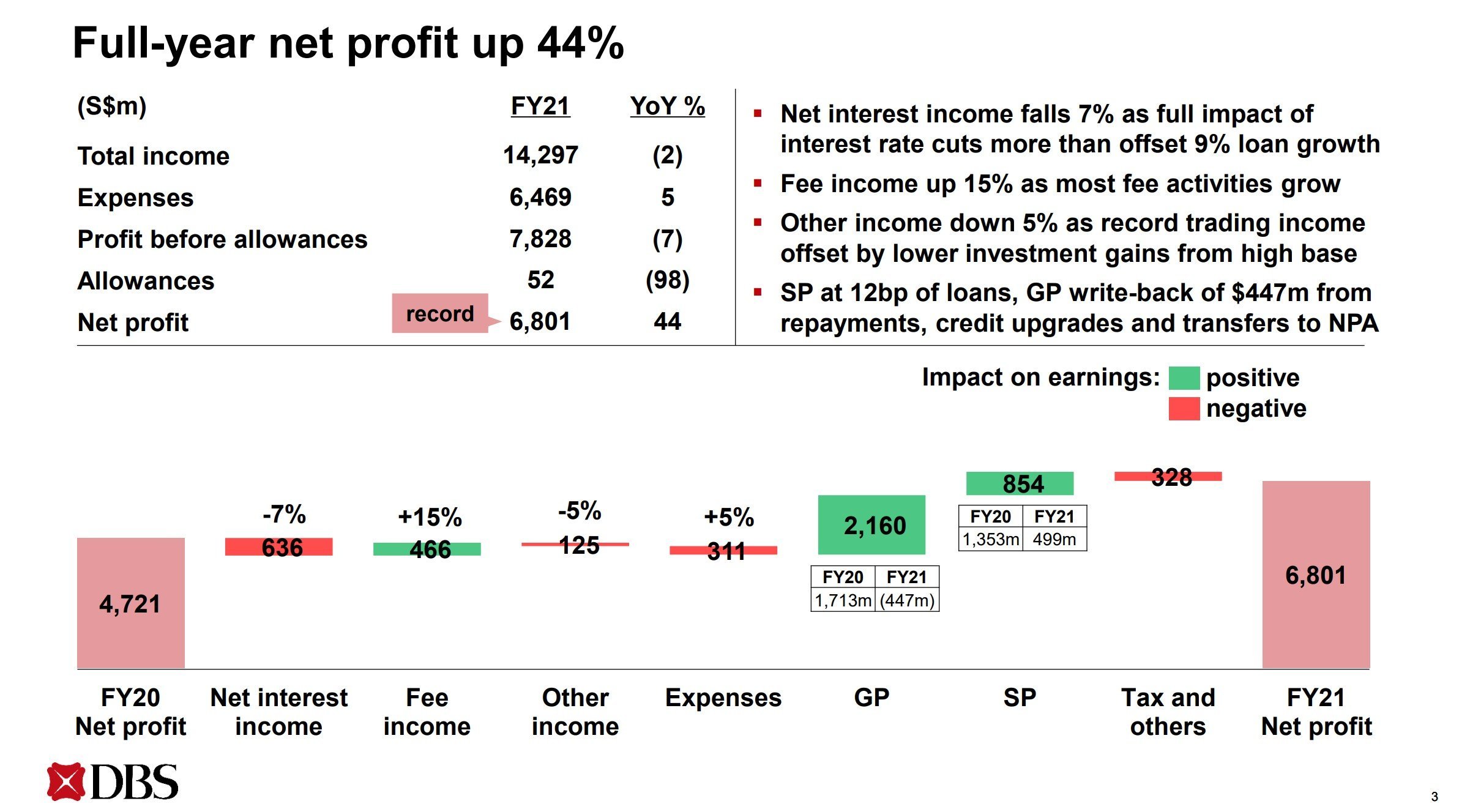

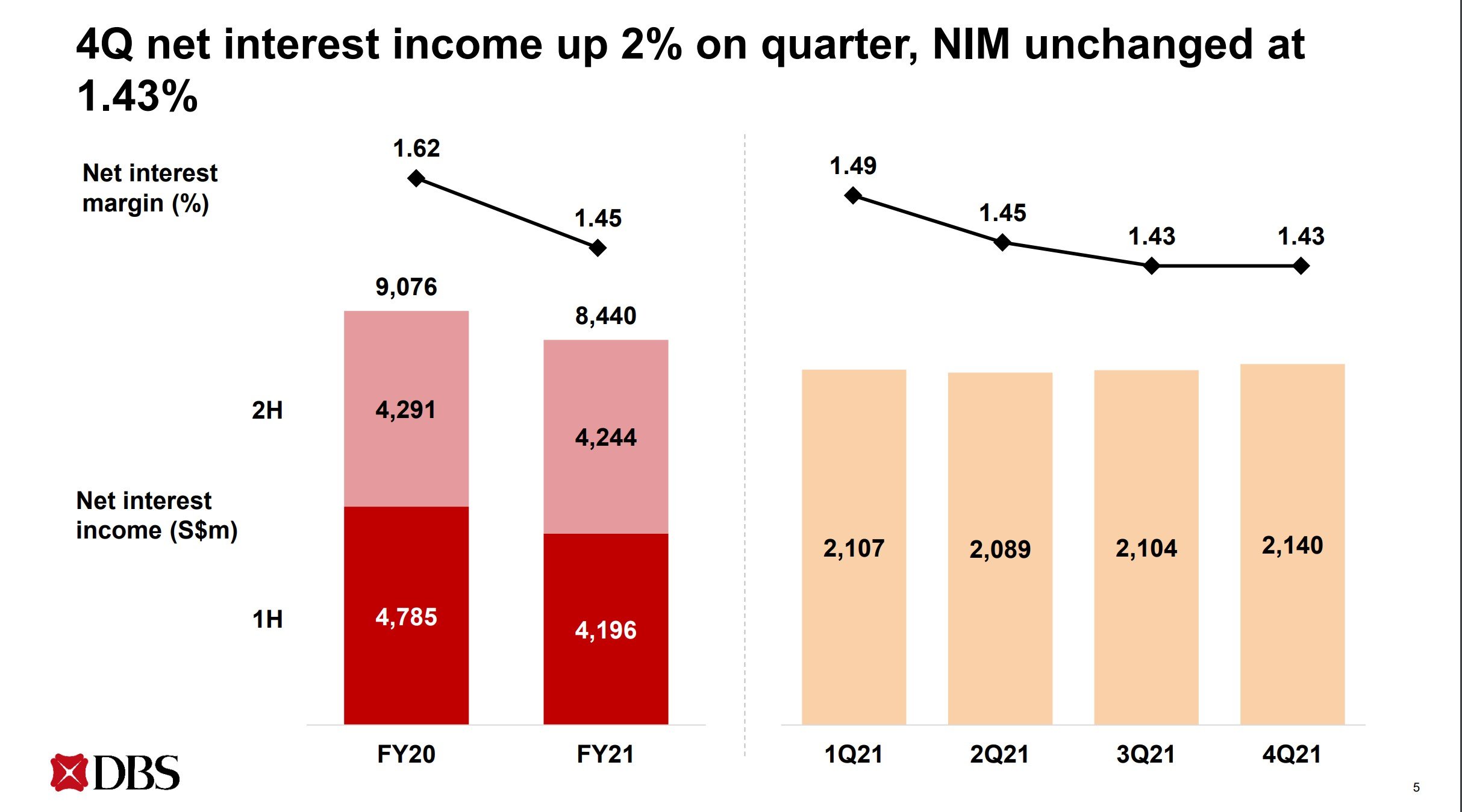

Full year net profit up 44%, loan book up 9% year on year.

And Net Interest Margin is going to fly in the next 12 months in a rising rate environment.

And you get a 3.8% dividend at this price.

I get all that.

But I do want to highlight that earnings are a lagging indicator, and cannot be used to time the top in a macro cycle.

With cyclicals like banks, the earnings are always highest at the top, that’s just how they work.

So yes, I absolutely agree that DBS Bank’s earnings are strong as hell.

But this is of little relevance in trying to time the top.

The equivalent is going back to 2020 and waiting to see earnings recovery before buying DBS bank stock. By the time it shows up in earnings, the opportunity is gone.

Same logic here.

3. What if Economic growth remains strong despite rate hikes?

Now let’s play devil’s advocate.

Let’s say the Fed goes hard and fast with rate hikes in 2022.

Let’s say we have 6 rate hikes this year, and 2 next year.

We’re at 2% by early 2024 and… the economy remains rock solid.

Because of COVID recovery, the world recovers strongly, inflation goes away, and the economy just chugs along at 2% interest rates.

Well, this is the goldilocks scenario for DBS. You get good loan book growth, good net interest margins.

You’ll look like an absolute fool for dumping DBS Bank stock at $36.5.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Do I think this is possible?

My personal view though – I don’t see this as likely.

I see Jerome Powell as a man boxed in.

On one hand he has the highest inflation in 40 years.

On the other hand he has an asset bubble propped up by 12 years of QE and zero interest rates.

Trying to quash inflation with aggressive rate hikes and quantitative tightening, while ensuring the asset bubble doesn’t burst explosively, looks to me like an impossible task.

It’s going to be like walking a tightrope 100m above the ground.

It’s not impossible of course, and if Jerome Powell is a fantastic central banker he might just pull it off.

But my view – is that Powell is human after all. And the chance of him making a mistake here, is very high.

Either he is going to be too dovish and inflation will stick around, or he is going to be too hawkish and risk assets will get crushed.

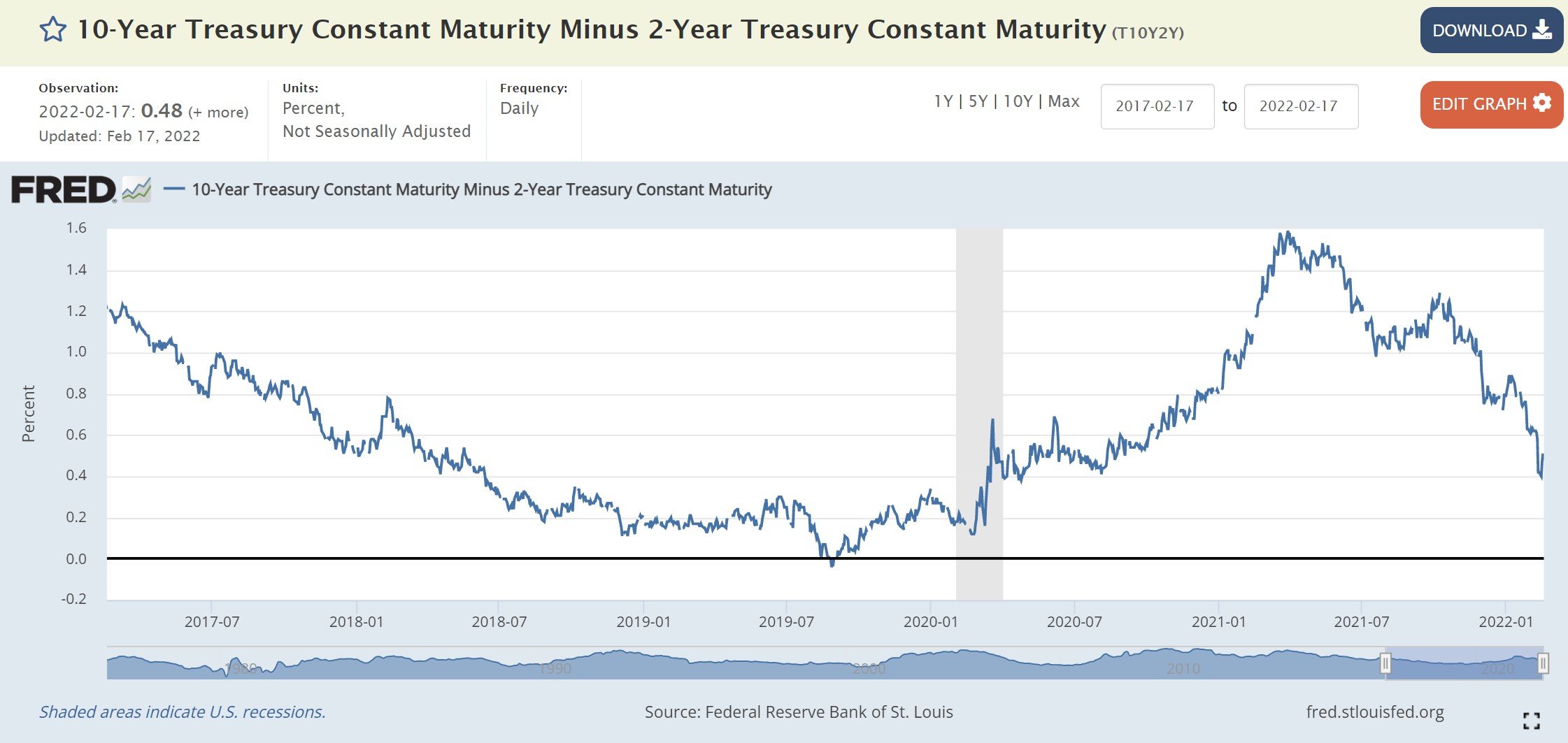

For what it’s worth though, the US yield curve is not pricing in any inversion yet, so markets are not worried about a recession just yet.

Whether that changes in the coming months, we’ll have to wait and see.

Will I sell DBS Bank stock?

Researching and writing this post helped clear my head by a ton.

And my decision is clear – I’m going to hold onto DBS for a short while more, until Q2/Q3 this year.

I’m going to take my cue on when to sell from the market.

If I see the US 10 year yield at 2.25% – 2.5%, or I see a yield curve inversion, or I see signs the Feds will change their mind on rate hikes, I probably start to take profit in DBS.

Why I am not selling DBS Bank stock?

I think the simple reason why is because (1) I don’t think we are at the top for interest rates for this cycle, and (2) there is a chance the economy is strong enough to absorb the rate hikes.

For the same reason I haven’t started buying growth stocks or REITs, I am also not selling banks just yet.

That said – If there is one thing I’ve learnt from my time in markets, it’s that no matter how right you may think you are, always prepare for the possibility that you are wrong.

What if I am wrong about the rate hike path?

Let’s say I am completely wrong here.

What if this is the top in rates, and the rest of the year see Powell turn dovish on monetary policy.

If that happens, I want to be exposed to assets that do well with easy monetary policy.

These are:

- Growth Stocks

- Crypto

- REITs

Growth Stocks or Crypto

The problem with growth stocks or crypto, is what is the downside if the Fed does turn out to be hawkish?

Take Cloudflare for example.

After a 50% sell-off, it now trades at a “bargain” 50 times Price/Sales.

I mean, are you prepared to say that 50 times P/S is the bottom for this growth stock, for this cycle?

Because growth stocks and crypto are so narrative driven and reliant on future earnings, it’s super super tough to call a bottom for them in a year with aggressive monetary policy.

Sure, if you get the call right you look like an absolute genius.

But if you get the call wrong you might just eat a 50% loss.

It’s very similar to China stocks last year, and in hindsight I did buy in slightly too early there.

DBS thinks REITs are a steal now

Which leaves REITs.

DBS came up with a fantastic report on REITs this week.

The long and short is that DBS thinks markets are mispricing interest rate impact on REITs.

The reasons why can be summarised as:

- S-REITs tend to bottom out as we approach the first rate hike

- S-REITs are well positioned against rate hikes because of fixed rate loans and staggered loan expiry profile

- Earnings are strong and should continue to improve as the post-COVID recovery plays out

And I absolutely agree.

I think the key difference between REITs and growth stocks / crypto, is that (1) REITs are backed by physical real estate, that (2) pays you rental income as dividend, year after year.

This allows you to more accurately call a bottom in REITs, because they are anchored by real world assets and dividend yield.

Take Ascendas REIT for example.

At this price it trades at about a 5.5% yield.

The last time it was at a similar yield (excluding March 2020 which was an exception), was 2018, when interest rates were at 2%.

So you can buy Ascendas REIT for the same yield today, as you could back in 2018 at the peak of the previous rate hike cycle.

So I kind of agree with DBS that at these prices, the blue chip S-REITs have basically priced in a big chunk of the hikes.

Sure, REITs may go down 10 – 15% from here if the Feds get really aggressive.

But in that scenario, how much would you be down on with growth stocks and crypto?

But… REITs to trade sideways all year?

That said, the other lesson from 2018, is that REITs will trade sideways for a whole year in a rising interest rate environment.

See the blue box below.

Ascendas REIT traded at that $2.5 range for the entire year, until the Feds changed their mind about rate hikes, and then it soared above $3.

That’s perfectly ok for me though.

As long as REITs don’t go down majorly from here, I’m fine if they trade sideways all year, because if they do I’m probably making money on my DBS and oil stocks. I’m using them as a psuedo-hedge, in case I’m wrong about the path of interest rates.

Closing Thoughts: When to sell DBS Bank Stock?

It’s been a monster of a post, so I want to wrap up.

My thinking here is simple.

Inflation is a real problem, and in an election year the Feds need to be seen getting tough on inflation.

This means they are going to hike and do quantitative tightening, and that is going to impact risk assets across the board.

My view is that the cycle top this time around is 2.25% – 2.5% on the 10 year treasury, which means we’re not at the top just yet. So I will hold DBS a little while more, and then I will sell to buy REITs (or maybe growth stocks or crypto).

BUT, because I could just be completely wrong on this call, I’m also going to start deploying my cash into blue chip REITs.

I’ll buy slowly, but I’ll start adding to REITs at prices that I find attractive.

You can check out my Patreon for the full list of names and prices, but names I like include Mapletree Industrial Trust, Ascendas REIT and Mapletree Logistics Trust. Mapletree Commercial Trust could be a decent pick up too. All are trading at 5%+ yields, very solid Singapore real estate, and backed by a Temasek backed sponsor.

You can also see my full portfolio and how I’m positioned for 2022 on Patreon.

Sure, REITs might drop another 10% from here.

But if that’s the case and Ascendas REIT trades at a 6%+ yield, I’m just going to absolutely back up the truck.

As always – love to hear what you think!

As always, this article is written on 18 Feb 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Even if you’re wrong on DBS, you can always sell at the beginning of the pivot, and still get a nice profit. I doubt we will see the price drop by 10% in one day during the pivot. You would have a week or so to do the selling.

Not necessarily though, it’s very tough to time the top based on price action alone. For example DBS has started to pull back slightly the past few weeks – is this already the top? Best to marry price action with some macro overlay.

All I can say is that you’re playing some serious 3d chess over there

Haha, it’s just me musing out loud to myself. Feel free to share if you think any part of the analysis is flawed.

I think as a business it’s a well run business and I have seen the management team is able to navigate business change well.

Assuming we think it’s a well run business, we can Hodl or take profit. Hodl is easy, no financial calculations involved, just hodl. If one wants to take profit, then it does go into the 3d chess game above.

Take profit, sure, but take profit and do what with it. Risk and reward, who dares win. As with market moves, you can’t just nail the macro, you also have the to nail the direction and timing.

I’m not savvy enough to nail number 2, I’ll just Hodl Dbs. But that was just my thought process

Yes I completely agree with this. Great comment.

Needless to say, I love your commentary and analysis. And I hope it helps other readers to clarify their position and thought process so that they can execute well in the future quarters ahead

Cheers, appreciate the kind words. Just doing my best to share my analysis, hopefully it helps others out there. 🙂

Hello financial horse, I am new to your blog and have been reading up many of your articles. May I ask what are some sg beaten down stocks that I could include in my portfolio?

I actually just updated the FH Stock Watch on Patreon so you can check it out for fuller views: https://www.patreon.com/posts/fh-stock-watch-62795437

General comment is that for SG market right now I like the blue chip REITs, especially the Mapletree/CapitaLand industrial REITs. Sure they can drop another 10-15% from here, but if they do I will likely add heavily.

You don’t made $ by holding stock, you made only when you sold. However it’s not so easy today with the new budget announcement yesterday, think about it, if you have $1m on hand now, where are you going to park it? Propery(cooling measure and more tax)? FD(int too low, can’t beat inflation)? Bond(int too low, can’t beat inflation)? Under your pillow(your spouse will steal it j/k :))? Or a blue chip like DBS which give you tax free 3 to 4% at today’s price? For people who own it at $20, the return is almost double, if the share price keeps going up, there may be stocks splits or bonus share, if the share price goes down, other things will go down as well so the cycle repeats, maybe it’s chance to buy more :p

It’s a good point – where does the money go after you take profit. It’s kinda also why I decided to keep it in DBS for a little while more, and use my cash on the sidelines to deploy into REITs instead.

I hold some DBS shares purchased between $5.42 (rights issue) and ~$26. Like yourself my current plan is to sell sometime in 2Q or early 3Q at the latest. Apart from the adverse side of the rate hikes coin I am thinking about the potential strains from the US congressional elections altho a more immediate worry is this hype about a war in Ukraine.

But on the positive side of the rate hikes coin, I wonder if DBS net profit will caress the $10billion mark in FY22. Simply, if we assume

1) an organic growth rate of 30% on FY21 profit that will add ~$2.1b

2) based on data in its FY21 results, a 0.25% hike in rate will yield ~$1.1b a full year in NII and this goes straight to bottom line for a full year making exactly $10b for a full year. A 2nd 0.25% hike will seal the deal for FY 2022.

And If the Taiwan Citigold acquistion can be completed within the year that’s more topping of cream.

That’s true, earnings for DBS should be very strong going forward given we’re likely to see quite aggressive hikes.

I actually added to my comment later but must had not properly performed the posting procedure. It’s this:

Will DBS and UOB acquisitions of the Citi assets make them be viewed by investors more as International banks and give the 2 much publicity about their superior capital ratios vs other banks. These ratios are well above int’l requirements.

But DBS valued at 1.6x book value is already on the same level as JP Morgan. So it is arguable that the market already values them as an international bank.

I suppose the question is whether the market can value them even higher. I mean it’s not impossible, but valuations are starting to get stretched.

Think it’s mostly baked into the price already. Look at HK listed banks instead like HSBC. PB still low and not so absurb.

The HK listed china banks have recovered a bit though, no longer 7% yields.. 😉

An excellent piece as usual, thank you

Although there seems to be a case to take some profit off the table, the most important question is how to deploy the proceeds to enhance returns? There are no easy answers

I will hold on to all the 3 SG banks and am buying REITS every week on down days

I bought CICT under 2,CLCT Last week and have added to Ascendas, MIT, MCT , FLCT as well

I will add more if there is a further drop

The banks and reit are good counterbalance to assure stability

This is the time to selectively buy the US dip in financials, energy, mega cap tech and sound industrials in the Dow

When rates actually go up, utilities will be appealing although SG offers no choice

Garudadri

It’s true I agree with this. Even if I sell DBS there’s no place to put the money now, which is probably why I decided to hold a while more. Agree on the REITs you named, will likely be adding to my positions there as well.