I had a couple of great questions from readers the past week:

Hi FH, thanks for sharing. Would like to check with you recently markets are charging and stock price shooting up. Do you see this as a V shaped recovery?

Or, especially for SG stocks is this a temporary euphoria due to end of CB, but it may be dampened soon as the market will realise it’s overly optimistic about the restart similar to Chinas reopening.

…

Thanks for the great article. Would like to get your views on the unprecedented levels of government aid (achieved in days, what took months to achieve during the GFC – probably good timing due to upcoming elections) globally and if there will be a meaningful impact on LT earnings. While the key aim is to keep companies and workers afloat, it seems likely that these low-interest government loans and/or equity injections may lead to an extended period of earnings growth and a bull run, similar to what we’ve seen in the past decade

Higher equity prices have enabled companies to efficiently raise larger amounts of equity, which adds to the above

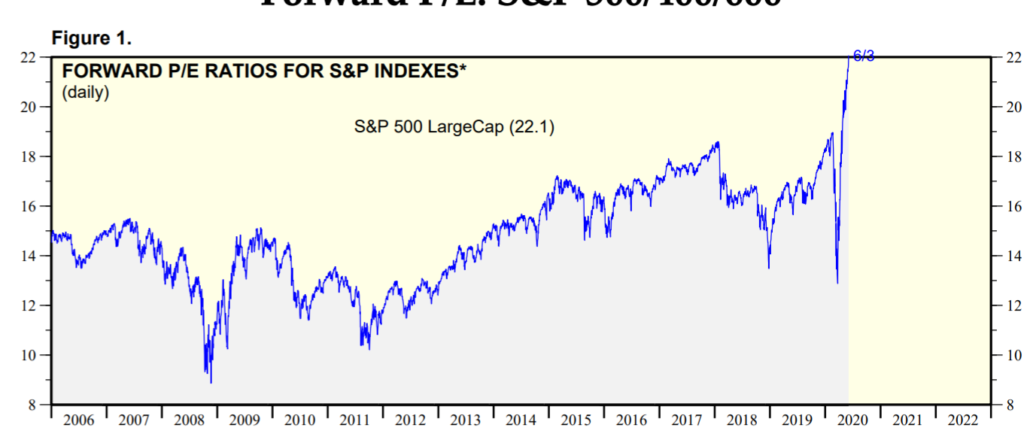

Current valuation multiples are almost back to pre-Covid-19 levels (after assuming perhaps a 10% hit to earnings), which are a result of years of multiple expansions for most sectors at least. From current prices, do you see more multiple expansion upside, or will earnings growth be the main driver of prices?

Those are some great questions, so let’s approach them individually.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

Basics: Price Actions from the market

We’ll start by taking a look at what the market is telling us.

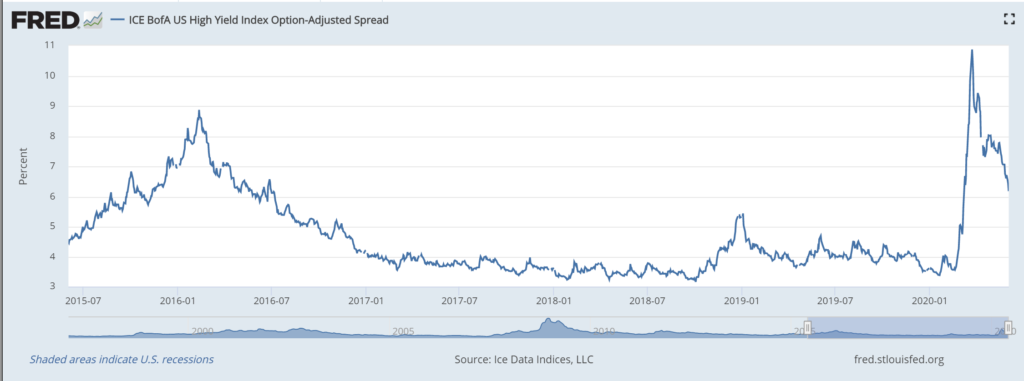

US High Yield and Investment Grade spreads are set out above, and they’ve come down significantly from their March highs.

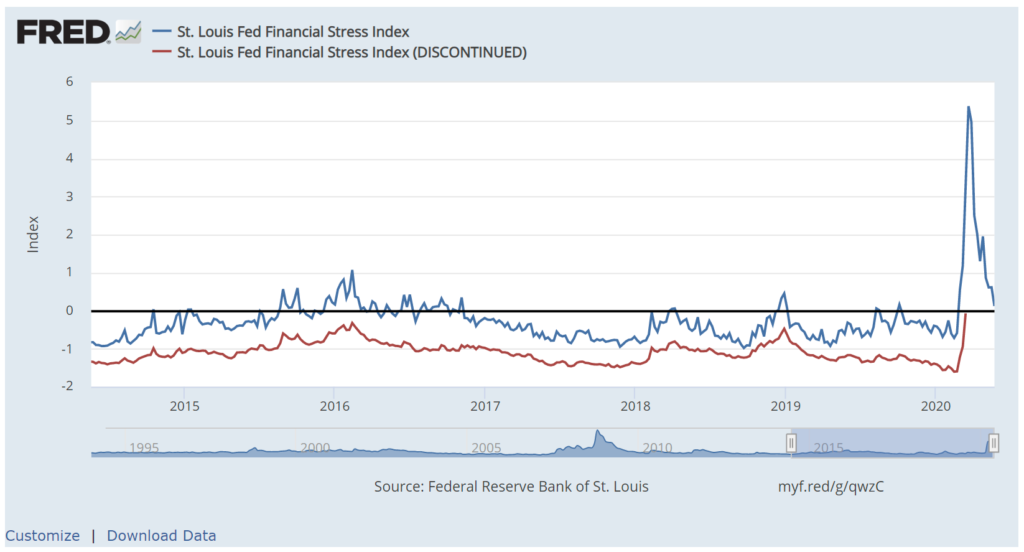

The Fed Financial Stress Index has also come down significantly, almost back to “normal” levels.

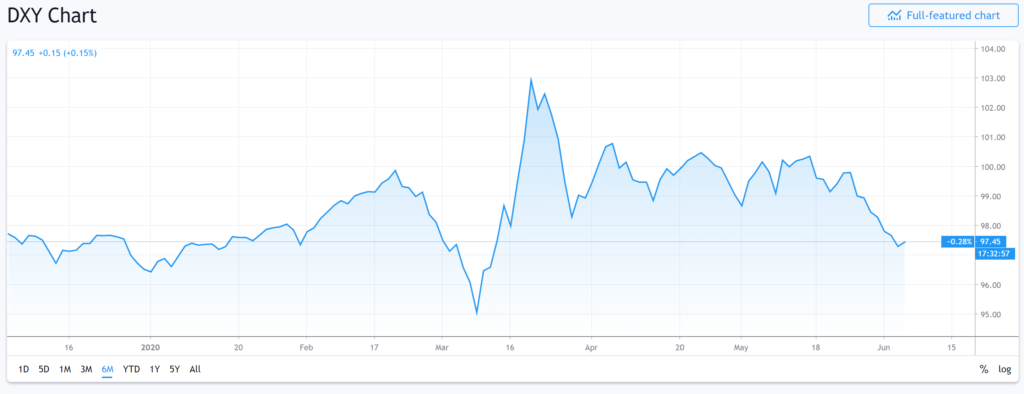

Interestingly, US dollar has also stabilized since the March liquidity stress, and since about late May has been starting to break out of the range it was in. A weak US dollar is great for global risk assets, as we’ve seen the past week.

US cyclicals have been leading US defensives the past 6 weeks, a reversal of the trend we saw in Feb / March. Interestingly, this is a very bullish signalling from the markets.

So in some ways, the market is really pricing COVID19 like it’s over!

Impact of Stimulus and Liquidity – It works

So regardless of what your views are on global central bank stimulus and liquidity, it’s clear that whatever the Feds have done are working.

Financial stress has come down significantly from March levels, they’ve succeeded in weakening the USD (at least short term), and accordingly risk assets have gone up.

Multiple Expansion vs Earnings Growth

So coming back to the question from the reader:

Current valuation multiples are almost back to pre-Covid-19 levels (after assuming perhaps a 10% hit to earnings), which are a result of years of multiple expansions for most sectors at least. From current prices, do you see more multiple expansion upside, or will earnings growth be the main driver of prices?

Now for those who are newer to stocks, there are 2 things that can drive share prices: Earnings and Earnings Multiple.

Think of it as a company that earns $10 a year. If the market values the stock at a 10 times Price to Earnings multiple, the stock will be at $100.

How then can the stock go up?

2 ways – Either the (1) underlying earnings goes up, or (2) the earning multiple goes up.

So under (1), if earnings goes up to $200, the same 10x multiple gives it a share price of $200.

And under (2), if earnings stays the same, but the multiple goes up to 20x, the share price also goes up to $200.

Same outcome, completely different process.

Source: https://www.yardeni.com/pub/stockmktperatio.pdf

As the reader has pointed out, a huge bulk of the driver of share prices the past 10 years was multiples driven.

In fact, the bulk of the rally since March was pure multiples drive, because quite clearly earnings have come down due to COVID lockdowns, so for stocks to go back to pre-COVID highs requires multiple expansion.

What about earnings growth?

Short Term Earnings

So this is what I wrote for Patrons earlier this week:

And earnings is the one that puzzles me.

It’s really hard to predict whether earnings will bounce back, because most economies right now are still juiced up on the effects of stimulus.

Take Singapore for example – when the government pays 75% of your payroll, as a business owner you’ll be pretty ok right? But what happens when that stimulus wears off? If your earnings don’t come back, you’re not going to be able to afford to keep the same number of staff without the government support.

Same for the US. People on unemployment benefits are earning more money than they made employed. So they’ve basically had a pay raise to sit at home. So consumer demand does go up for certain companies, because this guy now makes more money, and he can’t go out and spend, so he uses that money on other things. So this has created big winners (like Amazon). What happens when all this wears out? Does that demand come back?

So I think we’ll only be able to really decipher the earnings effects in September / October when the stimulus wears off, and a potential second wave comes into play.

If demand is going to bounce back to pre COVID levels quickly (V shaped recovery), stocks are looking cheap. We’ve cut rates to zero, there’s massive stimulus overhang, Feds are on unlimited QE, credit markets are unfreezing – so if demand bounces back, stocks could go even higher.

If demand doesn’t bounce back, then it gets tricky. With rates at zero, monetary stimulus globally is exhausted. A fair bit of fiscal stimulus has already been blown on salaries (most countries at 10% to 20% of GDP).

So short term earnings are tricky. If you look at the high frequency data and quarter on quarter numbers, no doubt they will bounce back in a big way.

It’s not rocket science, when the economy goes from a complete shutdown to a reopen, GDP and corporate profits are going to recover in a big way on a % basis from the trough.

The big question though – is what happens after that initial burst of recovery. What happens after the economy reopens, and everyone goes back to their daily life.

Do we see spending at the same levels as Jan 2019? Or do we see consumers cut spending.

Just run the example for yourself. Imagine it’s 3 months from now, the Singapore circuit breaker has been lifted completely. Are you still spending the way you used to in Dec 2019?

I don’t know the answer for certain, but I do think some caution is warranted. A complete V-shaped recovery in corporate profits to me looks very optimistic. I’m happy to be proven wrong though.

Long Term Earnings

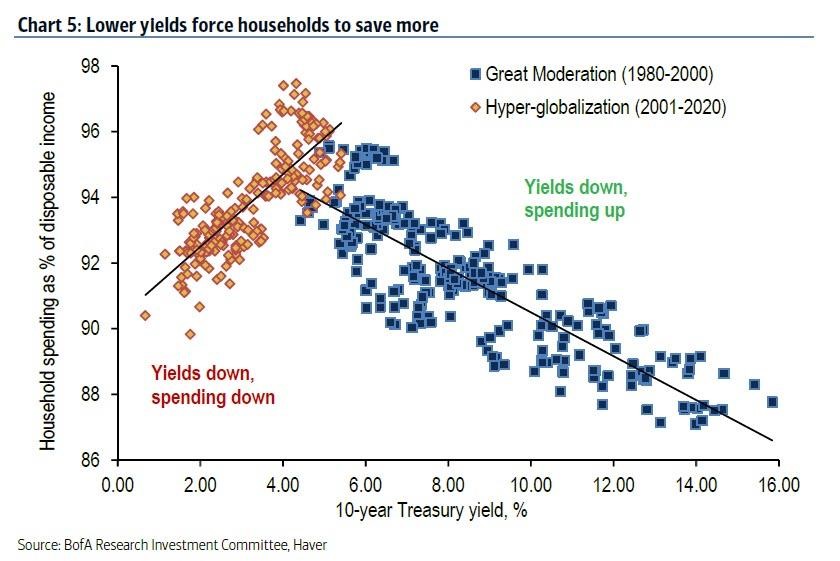

I came across this chart the past week that completely blew my mind:

It basically splits the past 40 years into 2 different Phases. The 1980 – 2000 phase, when lower yields resulted in higher spending, and the 2001 – 2020 phase, where lower yields led to lower spending.

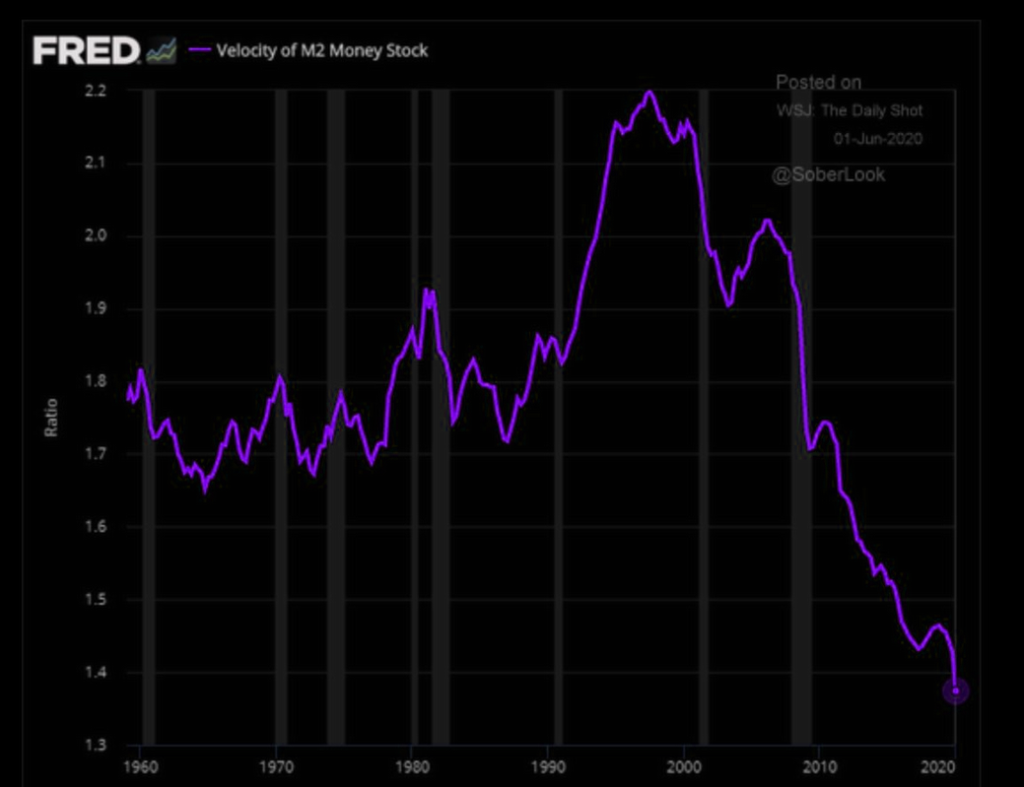

If you look at M2 money velocity, it tells the exact same story.

Correlation isn’t causation though, so we don’t exactly know why this is the case. But either way – something big has changed in the global economy post 2001, that has changed the relationship between interest rates and consumer spending / money velocity.

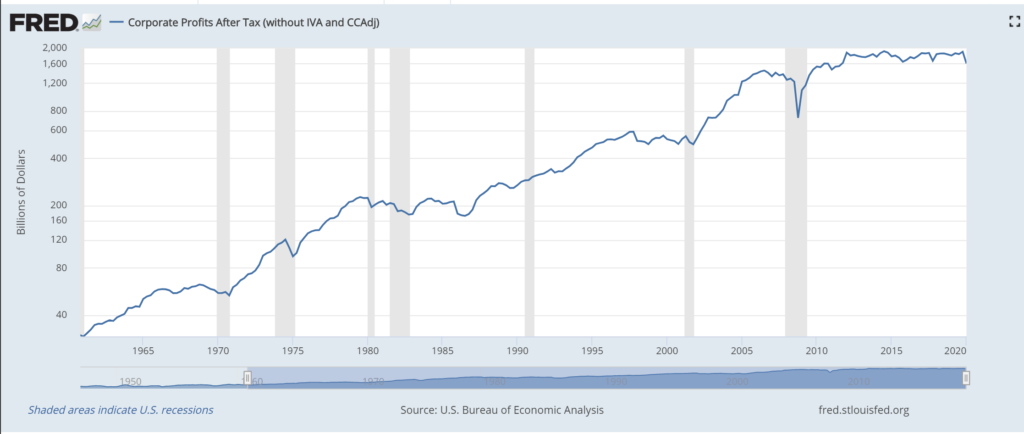

I also pulled up the 60 year corporate profit chart (log chart) for the US below, and it tells a fascinating story.

The shaded parts are recessions, and you can see that between every recession, there has been meaningful growth in corporate profits.

The only exception? The 2009 to 2020 bull market.

There was big corporate profit growth in the early phases of this bull run, from 2009 to 2012, but some time after that, corporate profit growth stalled, and has been stagnant pretty much since.

My Personal Interpretation

Now there are many ways to interpret the data above, and really your guess is as good as mine. I’ll share my personal view below, but feel free to share yours in the comments section.

I see a lot of the corporate profit and margin gains over the past 20 years as coming from offshoring manufacturing and global supply chains to China. China joined the WTO in 2001, and since then they’ve grown to become the factory of the world. Most global MNCs shifted their manufacturing to China (or Asia), reducing their costs base, while retaining the high value segments such as design, marketing and consumer sales.

And a lot of earnings growth over the past 8 years (after corporate profits started to slow in 2012) has come from:

- Redivision of the pie – Tech has grown strongly the past 10 years, and they’ve taken a fair bit of earnings away from the old world companies. Take Amazon for example – A lot of their market share growth has come at the expense of old world retail companies.

- Cheap debt fuelling share buybacks – At the same time, companies loaded up on cheap debt to fund share buybacks, fuelling their EPS growth.

- Tax Breaks – This one only came into play post – Trump, but Trump’s tax breaks did lead to meaningful growth corporate profits for US companies. The problem though, is that the benefits from tax breaks is one off.

At the same time, inequality has gone up massively. A lot of the policies set out above have led to meaningful redistribution of wealth from the lower and middle class to the 1%-ers. And the Fed’s responses to COVID19 has definitely exacerbated the problem.

What happens going forward?

So what happens to earnings going forward?

A lot of the factors above are one-off, and the same tailwind for corporate profits cannot be replicated going forward.

Offshoring manufacturing to China is one-off, and growing US-China conflicts will reverse this trend, driving up manufacturing costs short term.

Tech will continue to grow, and I’m quite bullish on that, but a lot of that growth comes at the expense of old world companies. At some point, regulation will also come into play to impact margins. We’re already seeing that with talk about regulating the likes of Amazon and Facebook.

Share buybacks will probably continue, but at some point companies may start to look excessively leveraged (if they haven’t already).

Tax breaks are one-off, so you can’t get that meaningful boost again, especially with government spending going up drastically.

So again – a lot of the tailwinds cannot be replicated, and meaningful growth to corporate profits going forward needs to come from another avenue.

What do we need for meaningful corporate profit growth?

And I think that to really see meaningful corporate profit growth going forward (leaving aside growth via inflation), it probably has to come via one of two means:

- Population Growth (Demographics) – Increase in population size / growing young population.

- Growth in consumer incomes – Reducing the income inequality will really drive corporate profits. If you give Jeff Bezos a billion dollars more, he’s probably not going to go out and eat another 1 million restaurant meals. But if you give the lower income $500 more per month, I’ll bet you see meaningful growth in consumer spending.

Applying this framework

So applying this framework to corporate profits by region:

- Asia – Asia ranks the best of the regions, and it’s why I’m so bullish on Asia. It’s a very young region comparatively (by age), and with meaningful population growth going forward. As the region grows, the number of middle class will explode, and that’s a lot more TVs, Laptops and Chanel bags they’re going to buy.

- Europe – Probably the worst of the lot. Demographics are poor, inequality is bad and unlikely to change near term.

- US – Somewhat neutral. Demographics continue to be attractive, but inequality is soaring, and we don’t see meaningful steps from government to tackle the inequality.

Coming back to the reader questions

So it’s been a really long article, and let’s come back to the reader questions. I’ll try to answer them as succinctly as possible (responses in bold):

Hi FH, thanks for sharing. Would like to check with you recently markets are charging and stock price shooting up. Do you see this as a V shaped recovery?

Personally, don’t see a V shaped recovery in earnings. Probably takes till 2021 or 2022 (or beyond) to recover to pre COVID earnings. The exact timing will depend on how supportive government policies are. Some companies in particular, are just not coming back after this, so I do still expect insolvencies as 2H2020 plays out.

Stocks though, are different. Depending on how the liquidity injections and stimulus plays out, stocks can continue to be detached from fundamentals short term.

Stocks cannot stay detached from fundamentals forever though, so if earnings don’t come back, at some point in the future stock prices will need to come down. Again – exact timing depends on central bank policies, it can be anywhere from 3 months to 2 years.

Or, especially for SG stocks is this a temporary euphoria due to end of CB, but it may be dampened soon as the market will realise it’s overly optimistic about the restart similar to Chinas reopening.

Again – not optimistic on earnings, so the key to watch short term is the liquidity and stimulus.

…

Thanks for the great article. Would like to get your views on the unprecedented levels of government aid (achieved in days, what took months to achieve during the GFC – probably good timing due to upcoming elections) globally and if there will be a meaningful impact on LT earnings. While the key aim is to keep companies and workers afloat, it seems likely that these low-interest government loans and/or equity injections may lead to an extended period of earnings growth and a bull run, similar to what we’ve seen in the past decade

Agree on governments propping up the economy.

Take Singapore for example. If companies lose x dollars of revenue due to COVID, and the government takes x dollars to pay the company’s payroll, the company is back in the same situation as it was pre-COVID.

If governments can keep this up until spending and earnings recover, that could be meaningful.

Long term earnings growth though, really goes back to the issues we discussed above. The same tailwinds are no longer in place for certain regions.

Higher equity prices have enabled companies to efficiently raise larger amounts of equity, which adds to the above

Yes, same for debt. Credit markets have unfrozen for the biggest companies – Amazon raised $10 billion for almost as low as 0.4%, which is unbelievable.

This goes back to the inequality we talked about, where big companies access cheap debt, while small companies are frozen out of funding because of poor creditworthiness.

The rich do get richer, and the poor are left to struggle. It’s not hard to see why there are protests in US and Europe right now, and why this will likely get worse going forward.

Current valuation multiples are almost back to pre-Covid-19 levels (after assuming perhaps a 10% hit to earnings), which are a result of years of multiple expansions for most sectors at least. From current prices, do you see more multiple expansion upside, or will earnings growth be the main driver of prices?

Short term, really goes back to responses from central banks.

And longer term, really differs by region and company, as we discussed above.

This will be an uneven recovery. Some regions will have real earnings growth (eg. Asia), and some companies will have real earnings growth (eg. Tech and Cloud players). But there will be big losers as well. Again, there are some companies that I think are just not coming back after this, despite what the market is pricing in.

That’s why I believe the case for active investing has increased and will continue to going forward.

Closing Thoughts

Today’s article has been a bit more of a high level one, looking at secular trends as they play out over multi-decade periods. Not sure if you guys like it, so feel free to share any feedback below – including what you want to read about going forward.

In terms of my personal investing strategy, no big change since end March when I wrote that the 3 buys signals had been triggered. I’ll just continue to average into this market over a 12 to 18 month period, but I will make tactical adjustments to the pace at which I average in, and the amounts that I use, based on macro conditions.

For those who are keen, my personal portfolio and personal stock watch list are set out on Patron.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

On TOP of earnings growth recovery, let’s also put the consumer sentiment. As companies tighten their belts ( most of them are on hiring freeze, salary downgrade or best case no increase, no promotions etc.) consumers will downgrade quick. Which means discretionary spends will be impacted much more than essentials. In a couple of years, most countries will need to raise taxes to tackle debt ratios. Again, will force most corporates to keep costs on tight leash.

Yeah! This is the million dollar question that I’ve been trying to figure out.

If what you said plays out, the recovery will be poor. But if the government stimulus can convince consumers to spend again, we’ll have a strong recovery. FOr now it’s not so clear which way things will play out.

thanks for the response! appreciate the holistic views

Well, nobody knows the answer for certain, this is just my thinking – that I’m happy to change over time as facts evolve. Love to hear your thoughts on the issue too.

Great article as always. I agree that short term wise is all about liquidity (Stimulus and FOMO) while long term is about earnings.

1. Lower Yields force household to save – Many possible reasons (could be correlation instead) – China became the factory of the world since 2000 + technology advances leads to consumer items getting cheaper over time (lower spending required) while income increases moderately.

Recovery largely depends on household spending (which depends on Govt stimulus and whether they have a job). While companies has reduce prices (F&B having promo, Apple cut phone prices in China), I would think that consumer will start spending when things on more stable.

2. Earning Growth – Agree with the Asia/Europe/US region view – however, all Europe/USA companies are more globalised than Asia companies, they will surely participate in it. One need not just invest in Asia companies to have that upside.

3. Winners/Losers – I would like to hear from you what sector would be the losers:-

i) Retail – Pre/post covid19 – their business is challenged – I like to hear from you what you think the new landscape will be between retailers and their landlord (the reits)?

ii) F&B – Most restaurants needs 2 turns in the evening at full capacity to make a decent profit. What now with max 5 sittings?

Given the above, wouldn’t one expect the rental income of reits to be reduce. I guess my question is will valuations come down, if yes, what you guess with be the drop?

Also, what other sector do you think will end up as big loser?

Hi App Shadow, great comments, thanks for the share! Some thoughts below:

1) Perhaps it could be a function of rising inequality too. Just a thought that we can explore more in future.

2) Landlords had a lot of power the past few years, but that probably erodes going forward. It’s going to be a renters market out there the next year or two, especially for things like retail, so I do expect rents to moderate and the balance of power to shift.

3) Yes, agree that rental reversions will come down. Valuations are tricky though, because the other factor is interest rates. As interest rates come down, technically real estate cap rates should come down too, boosting valuations. We also havent that the typical supply boom leading into this crisis, so I wouldn’t say that supply-demand dynamics are grossly mismatched.

A really interesting point is whether all the government stimulus and rent waivers etc can serve to shortcut the temporary pain, such that we only see a small decline in real estate valautions. For now I think the answer is no, but if we continue to see stimulus going forward, it’s not impossible too.

4) All old world industries that fail to embrace tech will be big losers. As will companies that fail to adjust to the new paradigm (deglobalisation). These trends were in play pre-COVID, all COVID did was to accelerate the timeline.

Just to elaborate on point 4 – take retail for example. You have a shop A that operates at a mall, and closes for 3 months no sales. You also have a shop B that operates at a mall and is now closed, but pivtors to selling via Facebook streaming, bringing in more revenue than pre-COVID. The fortunes of both shops can be very different, even though they are in the same industry.

So in some ways COVID19 is a period of great opportunity – for those who are ready to seize it. It’s easy to say that the entire retail industry will suffer, but that’s just not true. Agile business owners who can pivot quickly in these times and adapt to the new paradigm will still survive and thrive.

Hello Financial Horse,

As usual, another great article from you. Thank you.

I have heard & read many ppl, article say that there will be a new norm post covid and there will be business model that will be change completely or cease to exist going forward. However none have been more specific which type of business belongs to this catagory that will be totally change or cease to exists? What your view?

Thank you.

My rough thought is that travel agency, movie hall are the 2 such candidate. They have been hit quite badly by other factor even before COVID happen. COVID just made it more painful for them OR might even be the final fatal blow

I wrote an answer to App Shadow above that would address this somewhat.

I really do see COVID19 as in some ways accelerating the structural trends in place pre-COVID.

Take travel for example. I have no doubt that travel will come back when COVID goes away, because as humans we want to travel and see the world. But travel agencies as a business model – is that coming back? Maybe, but definitely not to the level it was pre-COVID when it was already in decline, because these days people prefer to tailor their own journey.

Same for retail as per reply above. After this, any retailer simply must have an online presence to remain viable, the days of just opening a store at a mall and thriving there are probably gone.

So all the industries like travel, retail and movies will continue to exist. They just need to adapt to the changing times and consumer tastes (much bigger emphasis on tech and personalisation). It is those companies / business models that fail to adapt that will be left behind. But the industry as a whole will still recover and go on to new heights.

One only need to head over to the hawkers united Facebook group to see how they have innovated! For some, being forced to go online has raised their profile and improved business.

https://finance.yahoo.com/video/why-unemployment-rate-head-fake-153949029.html

Wonderful Interview with El Erian on the latest US job numbers. His last comment at the end really resonates with me nicely summarizes my current thinking.

“MOHAMED EL-ERIAN: We are. But again, if it turns out that the financial markets are good forward predictors, and if it turns out that they have priced in a growth spurt that avoid bankruptcies, markets will be proven to be right. I’m not comfortable making that bet. I’m really not comfortable doing it.

And I’m so happy I’m not managing other people’s money, because I would be so torn right now between simply following the herd, because after all, technicals are very favorable, and on the other hand, being influenced by fundamentals. As a personal investor, I’m fundamental based. I don’t like moral hazard. I don’t like betting on things I don’t understand. But I completely understand why others that are managing people’s money feel that they need to be part of this herd.”

Haha I saw this interview as well, and yes, definitely agreed!

I think travel agencies still have their place, except they will need to shift their business strategy from B2C to more B2B. Like in my industry, we have symposiums for a few hundred doctors in Asia, we still need the travel agencies to recommend the hotel, get the entertainment for the welcome dinner, webcast, printing in local countries like display banners, etc. We won’t be able to do this all on our own, esp. when we don’t have a local office in that country.

Thanks, and absolutely agreed. Those who can pivot and adapt will still go on to survive and thrive!