A lot of you have told me that you think the stock market is going to crash.

You see the risks pilling up in global macro, and in market technicals, and you think a big crash is coming.

It’s been forever since I’ve done a proper macro post.

So I figured let’s take the chance to round up my latest macro views.

Is the stock market indeed going to crash?

*Launch of the Stocks MasterClass!*

3 Big Things that Worry me for Stocks

There are 3 big things that really worry me going forward:

- Rising Interest Rates

- Rising Inflation

- Slowing China Growth

Rising Interest Rates – Tightening Monetary Policy

Probably the most immediate, short-term concern – Rising Interest Rates.

The path forward is one of tightening monetary policy.

The Feds are all but set to announce tapering in November 2021, to end in June 2022.

This means that the Feds will slow their buying US Treasuries (QE), from the current $120 billion a month to zero by June 2022.

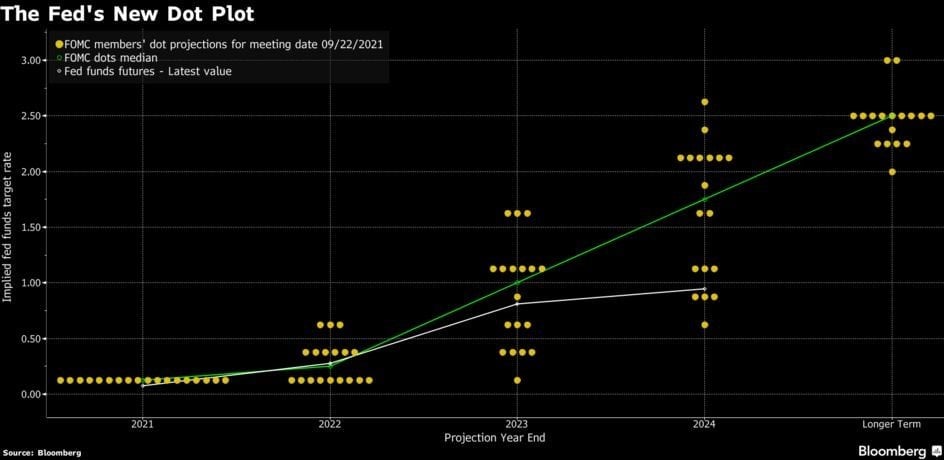

The latest Fed Dot Plot is below. In simple English – most of them are now predicting 1 rate hike by end 2022.

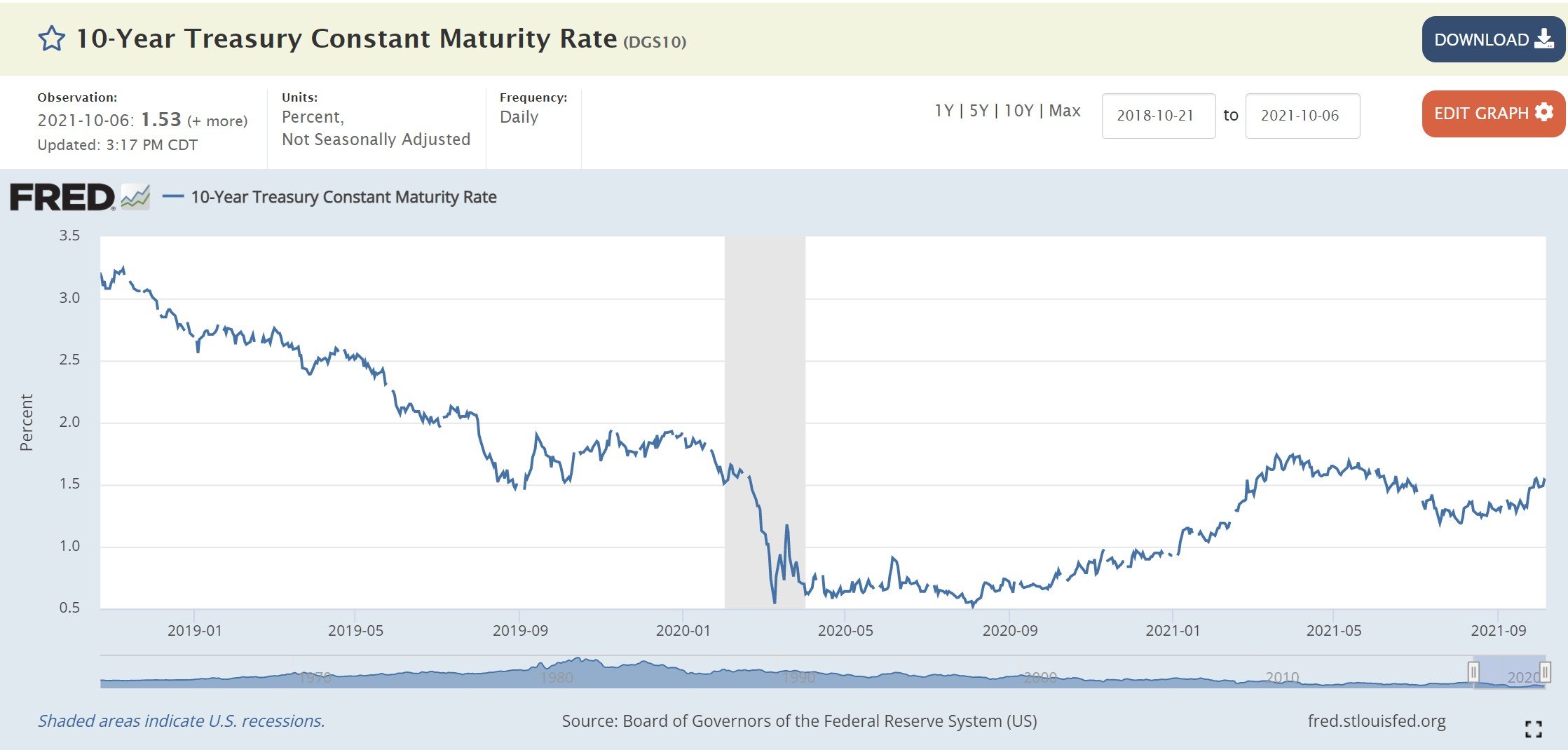

Interest Rates have responded in kind.

The 10 year treasury is back up at 1.6% as we speak.

This is Soc Gen’s CTA (trend following) model, which has flipped to short bonds. If Soc Gen has flipped to shorting bonds, you bet that most other CTA models out there have flipped to short bonds as well.

When institutional money moves like that, we may see a rapid move in rates in short course.

And when interest rates go up quickly, lots of things blow up in the market.

All long duration assets – speculative tech, fixed income proxies (eg. REITs), bonds etc could all be hit badly.

Like we saw earlier this year.

Sideplot – Powell out as Fed Chair

There is a very interesting sideplot on monetary policy though.

Increasingly – it looks like Jerome Powell is not going to be reappointed as Fed Chair when his term is up early next year.

The role of the Fed Chair is becoming increasingly politicised, and Powell’s poor handling of (1) US inflation, and (2) the “insider trading” scandal at the Fed is leaving him very exposed.

If Powell is out, who is going to come in instead?

A lot of people are looking at Brainard, but frankly I don’t think it makes a big difference who Biden picks.

The fact of the matter is – Biden is going to pick someone who will give him easy monetary policy in 2022.

That’s what all politicians want. Even Trump figured this one out.

Pick someone who will keep monetary policy easy, so Biden can spend all the money he wants on infrastructure and revamping the system.

This means that looking forward into 2022, we could actually have easy monetary policy for longer.

Which brings me to my next point – inflation.

Inflation… Transitory or not?

I know the official story is that inflation is “Transitory”.

But as a consumer, if you go out and buy a house, a car, or heck just a bowl of bak chor mee in a food court, I assure you that that prices have already gone up today.

And we all know that when sellers raise prices today, they don’t drop them tomorrow regardless of where inflation goes.

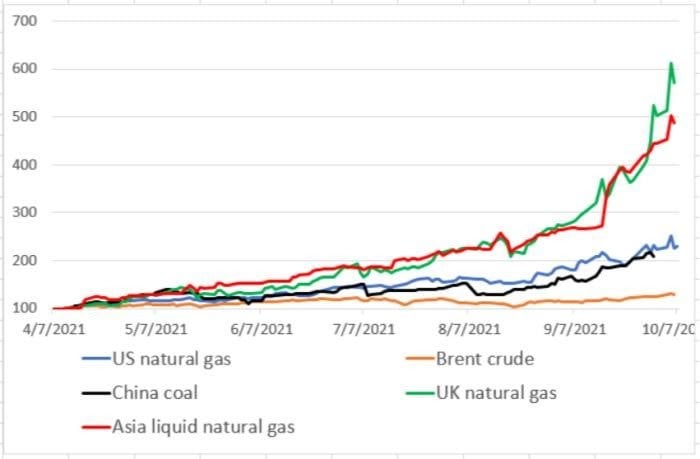

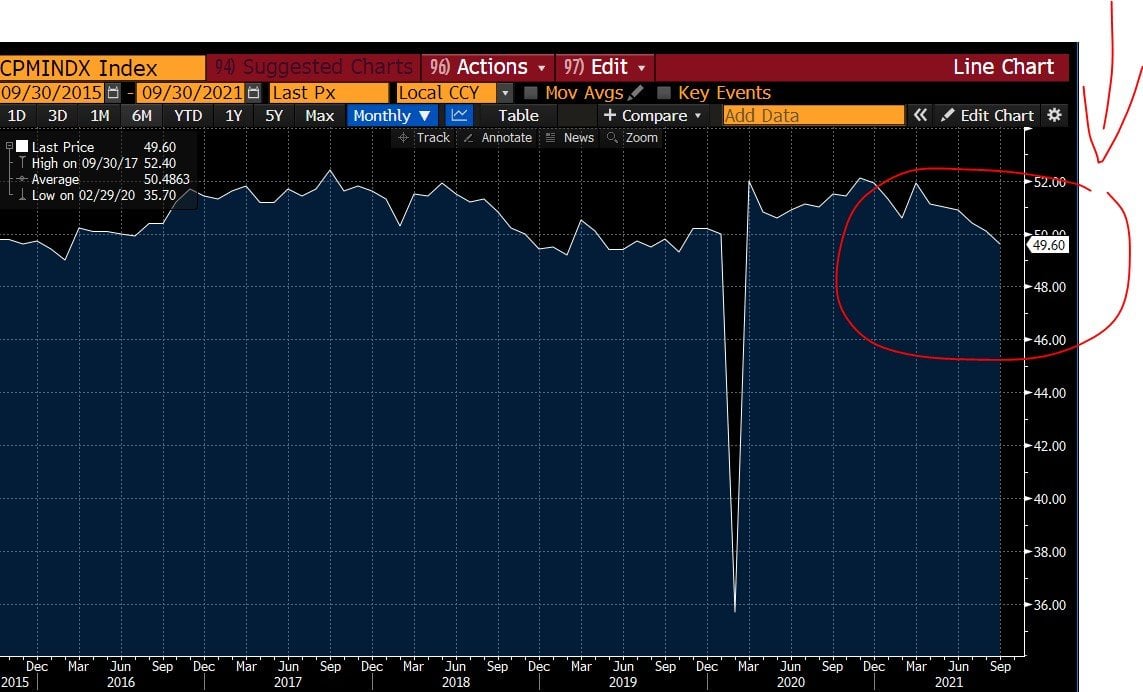

These are year to date numbers for commodities prices, which are just ridiculous.

Baltic Dry Index (freight cost) up 313%. Natural Gas up 124%. Coal up 200%.

Oil’s 59% looks tame by comparison.

If you’ve been following the news, you’ll notice that we currently have an energy crisis in Europe, China, and India.

At the same time.

And it’s not even winter yet – when energy demand goes up significantly due to heating.

Closer to home – even Gan Kim Yong came out this week to say that Singaporeans should “save electricity as costs increase due to fuel prices”

The thing about inflation is that it’s always split into 2 phases: (1) rising prices, then (2) shifting mindsets.

First – prices of stuff go up.

Your house, your car, food. Even Playstations. That’s that we’re seeing now.

Then at some point in time, mindsets start to shift.

The idea of rising prices becomes rooted in society.

As this idea catches on, people start to panic, and they rush to bring forward their spending before prices go up.

That’s when you start to see the really big moves in prices. And that’s also when you start to see the action from central banks and governments.

For now though, we’re still in Phase 1.

Which means there’s more inflation to come in 2022. Really big one to watch.

Jerome Powell recently acknowledged that inflation was stickier than expected, so the narrative is starting to shift: “It’s also frustrating to see the bottlenecks and supply chain problems not getting better—in fact at the margins apparently getting a little bit worse. We see that continuing into next year probably, and holding up inflation longer than we had thought.”

Rising Inflation with Easy Monetary Policy?

Remember how I talked about monetary policy maybe staying easy in 2022 with Powell’s replacement?

What then if we have inflation persisting into 2022?

The problem this time around is that the inflation is due to supply shortage.

OPEC isn’t pumping enough oil, Taiwan isn’t making enough semiconductors, China isn’t making enough toys.

Monetary Policy does absolutely nothing to help with supply shortage.

If you raise interest rates, they’re not going to make OPEC pump more oil, or Taiwan to make semiconductors faster. It’s not going to make wind in the UK blow harder so you generate more wind power.

If you raise interest rates too fast, all you end up doing is crashing financial markets and derailing the economic recovery. Which of course would solve the inflation issue by destroying consumer demand, but that opens up a whole new set of problems.

So when push comes to shove, my hunch is that central banks may be slow to raise rates to respond to inflation in 2022.

Which means inflation could run hot for a while – exactly why this one worries me a lot heading into 2022.

Central banks have been lamenting the low inflation for the past 10 years. Be careful what you wish for.

Slowing China Growth

We talked a lot about Evergrande the past few weeks, so I’m not going to belabour the point.

Simply put – The Evergrande contagion starting to spread. This week saw Fantasia default as well.

My base case scenario is that China’s real estate growth will slow in the coming months.

Real estate is 30% of China’s economy, so if real estate slows, China’s growth slows.

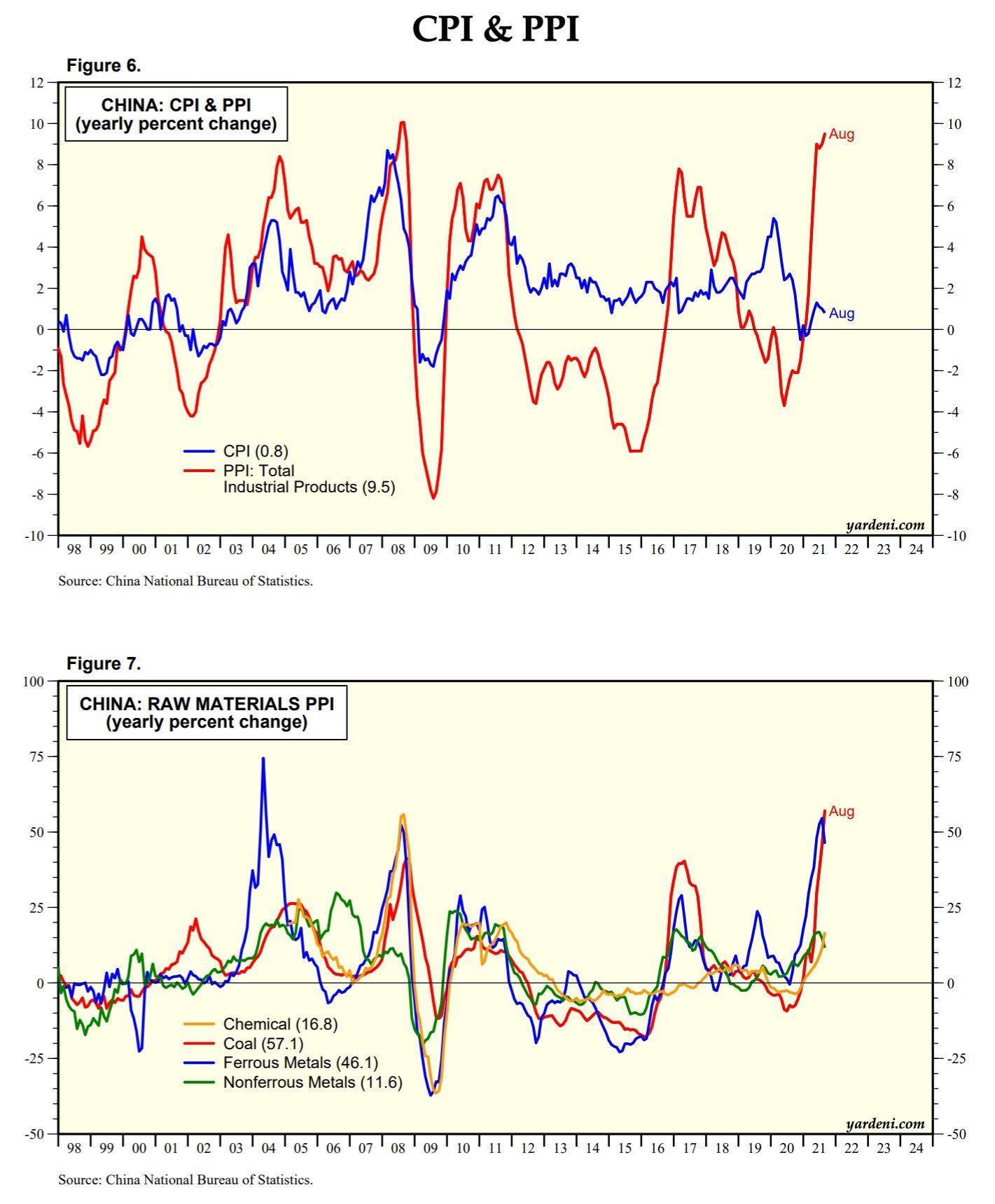

Double Whammy from Commodity Prices

At the same time, China is facing a double whammy from rising commodity prices (see above).

You see, China is poor in natural resources, but rich in manpower.

For now, their economy is all about importing natural resources, adding value to it (manufacturing), and exporting stuff to the world.

What happens then when the price of natural resources goes up?

At the same time, China is going through a big energy crisis because of rising coal prices, and Xi’s decarbonisation goal (which has obviously now been put on hold). The energy crunch has forced Chinese producers to either limit their production hours, or pay a higher energy bill.

The net effect of rising input prices + an energy crisis?

The cost of production increases. By a lot.

For now, China producers are absorbing the cost increase.

This means lower profits, which hits sentiment, which hits growth.

Evergrande + Rising Commodity prices + Energy Crisis is just a triple whammy for China.

A lot of high frequency indicators like PMI and Retail sails are already starting to roll over.

Sidenote – At some point in time, China producers are going to have to raise prices to preserve their margins.

Which is going to spark a wave of inflation globally – because everyone produces in China.

But that’s more of a 2022 story.

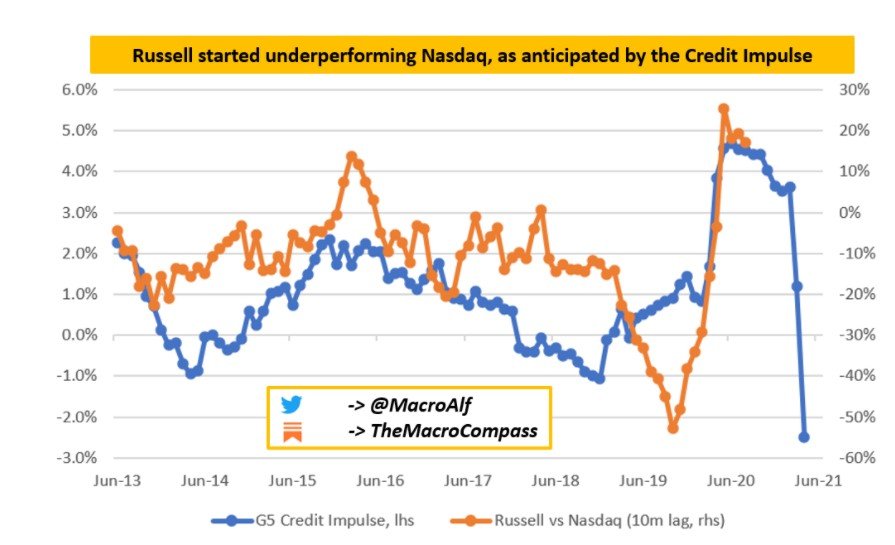

Credit Impulse peaked in 2H2020

The 3 points above are the main issues to me right now, but there are a few other sideplots worth mentioning.

Firstly, G5 credit impulse (basically the rate of growth of credit in the economy), peaked in late 2020.

Credit impulse usually tends to lead by about 12 months, so peaking credit impulse in 2020 should mean we see weakening growth right about now.

Valuations

At the same time, market valuations are very close to all time highs.

But to be fair, valuations are not a useful timing tool.

Expensive can get more expensive.

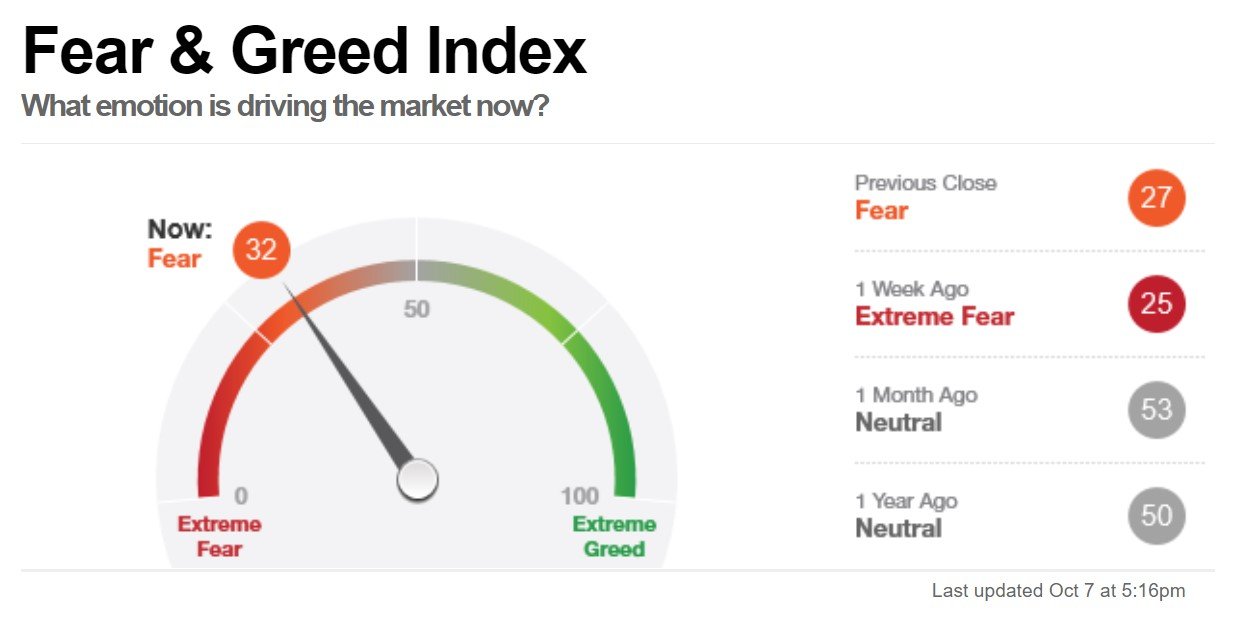

Market Sentiment

Interestingly, the Fear & Greed Index is not showing a complacent market.

Investors in general are a lot more cautious today, and have dialled back on the greed.

Sentiment is a contrarian indicator – so cautious investors is a bullish sign for markets.

So FH… Is the Stock Market going to crash?

Simply put – I think the answer is a lot more nuanced than that.

And the underlying reason to me – is that Cash has a real opportunity cost today.

Let’s say I think the short term risks are elevated, with possibility of a correction.

So tactically I hold more cash for 3 – 6 months.

If there’s a dip great – I deploy all that cash into stocks.

But what if there’s no crash, or if the market goes sideways? At what point do I throw in the towel and start deploying cash again?

Inflation is real. Just take a look at house, car or food prices and you know that if you stick your cash in the bank at 0.5% interest (if you’re lucky) you’re losing money every day to inflation.

So as investors, cash is only useful as a tactical tool – holding for 3 to 6 months as you wait for a better entry price.

But as an investing strategy, holding cash for the next 2 – 3 years is just a very poor investment strategy.

My Macro Views

Based on what I see today, I think the path forward is one of rising interest rates.

But I also think Powell may be replaced with a more progressive Chair, which could keep monetary policy easy in 2022.

I also think inflation will be sticky, and will follow us well in 2022. Those supply chain bottlenecks and energy crunch are not going to go away so soon.

I also think China’s growth will slow in the short term, as they restructure and reposition their economy for future growth.

One of the Toughest Markets to Invest in

All of these factors, combine to create one of the trickiest macro climates we’ve had in a while.

The past 10 years was about being long duration – you buy FAANG, you buy growth, and you win.

Going forward it’s probably not going to be so straightforward.

Rising inflation + Rising rates could spell trouble for growth stocks, and call for exposure to stuff like commodities and dividend stocks.

Rotation rather than a Crash?

The way that financial markets work today, is that money flows from one part of the system to another.

It’s not often you get March 2020 style events where the money flows out of the system entirely.

So instead of a market crash, I think we’re more likely to see a rotation in assets.

Money moving out of fixed income and long duration proxies like growth stocks.

Into inflation favourable asset classes like commodities, banks, cyclicals, dividend stocks. Maybe even crypto.

Growth into value anyone?

Time to Take the Wheel Again

As investors, you can choose to be passive or active.

If you’re passive, you just put the money into an index fund, and you continue putting it in the next 10 years, rain or shine. Really doesn’t matter what happens in the macro environment.

If you’re active, then this is time to shine.

For investors which have been on autopilot since April 2020, now is the time to be looking at your portfolio again.

Time to get your hands back on the wheel, and turn off the cruise control.

The investing paradigm is starting to shift again.

How am I changing my portfolio?

Like I said – this is a tricky one.

Country wise:

I like US in the short term, but 2022 is still a question mark.

I don’t like China short term, but I really like it mid to longer term.

And Singapore – Singapore is just a bunch of REITs and banks. Banks should do well on rising rates, and REITs I will add aggressively if there is any interest rate sell-off.

Industry wise:

I like all the inflation benefitting plays – banks, commodities, cyclicals, dividend stocks etc.

Growth looks tricky short term, but mid term they are still secular growth plays. Software will eat the world.

So for the first time since April 2020, it makes sense to relook my entire portfolio seriously again. Start pruning the names that don’t make sense in this macro environment. And reallocate into the future winners.

As always – you can get access to my full portfolio and stock watch on Patreon if you’re keen.

That said, I would absolutely love to hear your views.

Let me know what you think! Do you think a market crash is coming? How are you positioning your portfolio?

Nice macro post! I like you manage to tie everything together in to one coherent thread. A couple of thoughts.

First, the multiple worries you point out are an unstable equilibrium. While they can exist together in the short run, I think over the medium term, say by H2 next year, something will have to give. I think the policy makers might eventually blink, and this would be the buy signal. For example, the Fed might choose to flip dovish or the Chinese might walk back on their property tightening or world leaders might delay their green plans because people are protesting about lack of electricity in the streets.

Second, it seems no institutional investors wants to touch any of the “dirty” commodity names. This is like the tobacco companies of decades past. What this means is retail investors shouldn’t be expecting big capital gains, and that most of the returns will probably come from dividends. This also means that is not too late now to buy into the oil and gas names. I own shell, but would prefer more of an oil pure play, as most of the majors are trying to transition to green energy. It’s like John Wick wanting to retire to be a car salesman. Possible but not convincing. Been looking at oil producers like Aramco, Rosneft, Gazprom. My discomfort though, is that these are markets I am unfamiliar with.

Third, I would buy the dip in any big tech sell off. I get that higher interest rates = lower PV of DCF. But that is only one part of the equation. The big tech companies have the ability to raise prices (a monopoly is a beautiful thing) and require relatively low capex to scale. So in an inflationary environment, the numerator (the cash flow) also has room to expand. I find this seems to get little attention when people talk about the growth to value rotation.

Fourth, I do not agree that cash is trash. It gives you the optionality to act during corrections or market crashes. It also gives you a certain level of psychological safety, so that you will be less fearful during sell offs. I for one might not have had the conviction to buy more in March last year if I did not have a sizable cash weight in my portfolio. As retail investors, we do not have an obligation to be fully invested and compared against some benchmark, so that is an advantage we have over the institutions. The way I see it, cash is like a shell on the tortoise. Sure it’s going to slow me down when everyone is racing ahead. But it’s going to protect me in the lean times. And ultimately, this helps keep me in the investing race, instead of burning out like the hares 🙂

Fantastic comment Moo Moo. I agree with most of your points.

Some comments from my end:

1. Agree on cash. I myself hold relatively large cash positions, simply because like you said, it gives me peace of mind as an investor, and it allows me to take greater risk with my investments. If this is you then absolutely hold as much cash as you need. My point was more of that apart from all this cash held as a buffer, it doesn’t make sense to hold much cash in an investment portfolio other than as a tactical timing tool.

2. Agree that policy shift might happen. If it happens, then as investors we respond in kind. 🙂

3. I’ve heard a lot of investors say that too, that Oil is only good as a dividend play these days. I’m not so sure though, if the oil crunch continues to play out in 2022 we may see institutional investors change their tune. But yeah I definitely get what you mean.

4. Agree on pricing power of Big Tech. My bigger concern with Big Tech is regulatory crack down. The political narrative is starting to shift against big tech, and the China case study shows us the dangers once political/regulatory climate is no longer favourable. For now they’re still fine, but that’s the biggest risk I would watch for, instead of inflation.

Great comment, loved this one. 🙂

Very comprehensive macro view that is easily understandable. Thanks FH.

One thing which I don’t understand though. Adding REITs aggressively if there is an interest rate sell off. Won’t rising interest rates hurt earnings of REITs? And tt in turn affects EPS.

Thanks Ryan, glad it was useful!

Well it all goes back to timeframe. Sure, short term EPS drops, but for investors who can take a longer term view and hold 3 – 5 years or more, returns will still be good once the cycle shifts again + inflationary pressures kick in on rental and real estate prices.

I added heavily in 2018 when markets were freaking out over the rate hikes, broadly on similar logic.

Nice and well written article. I’m surprised you do not consider European markets. Share prices are not as inflated as in the US and P/E ratios are much lower. As an example consider the S&P 500 dividend of around 1.8% (and minus the 15% US withholding tax) compared to the Ftse with a dividend of close to 5% and no tax on dividends. I’m a lazy investor and only invests in index ETFs and have done pretty well investing in UK and European index ETFs over the past 12-18 months. OK, perhaps the ftse has not done so well and it’s still lower than when I bought it before the crash, but with dividends and the increasing strength of the pound I’m more than even 🙂

Yeah I get what you mean – I’ve been thinking about European markets too. To date I dont have significant investments there though, apart from some RDS shares.

Agree that longer term they could do well, and are a good diversifier.

Thanks for another great post!

Just curious, when you say “relatively large positions” how much cash do you/would you recommend to hold, as a percentage of entire portfolio?

And by the way, I think that the comments section on FH are head and shoulders above what you read on other blogs.

Thanks for the support!

I think this one really depends on your personal situation, for eg. how stable is your job, whats your age, risk appetite etc. As a general note I would say not more than 5 – 10% of your net worth unless you have special reasons to hold more (eg. saving up for a big ticket purchase, income not stable, near retirement etc).

Hi,

Agree in general on the 3 factors that will be dictating overall market sentiments from now into next year. However the first two factors have been over discussed to death. Hope that when it happens there will not be a knee jerk reaction.

Factor 3 on China is the real worry. For reasons unknown – there are just too many activities from the Chinese government that are de-stablising all the markets including HK.

Personally thought Jerome Powell has performed credibly so far. Will be ashamed if he is replaced. When has it been that US is not short of funds, the coming period is no exception.

Yeah I agree that Powell has done well, I’ve been very impressed by his handling. Unfortunately it’s become a political issue, and I think the narrative has shifted against Powell. The Fed Insider Trading issue looks really bad on him.

China was the country that powered us out of 2008, so this time around with China not the growth driver, interesting to see how it plays out.

As always with inflation, just how high and for how long. If price spikes only last 1 year then you might be back to ~2% CPI in 2023/24 because it’s a YoY calculation. But absolute prices, i don’t think they are going to come down anytime soon. As we transition into inflationary economy, it means consumers have to pay more. Will the net effect be more disposable income due to higher wages and fiscal policy? Or actually same stagnant wages and depressed spending, since items are more expensive now? Many many things are unknown, and to be honest we are just waiting for economic data to come out. With so many unknowns, it really comes down to finding stable long term returns. I find bank stocks, consumer discretionary pretty good now, similar conclusions you had. Surprisingly, I don’t think Gold will do well as yields go up. Gold isn’t an ‘inflation’ hedge the way you would hedge it right now

Yup generally agree with this. The way it’s shaping up though, it looks like the Feds will be behind the curve, then have to raise quickly in late 2022, which will crash the economy and force rates back down again. At least that’s what the bond market looks to be pricing in . 😉

Hi FH,

Could I request that you share whatever knowledge you know what type of options we have in Singapore if I am only a retail investor and want to buy bonds for the coupon rate. What is the shortest time frame that I need to lock my funds for bonds?

And I don’t mean the Singapore savings bond. I mean any other bonds, are there any which you would recommend for retail investors which are safer? How to access such investments?

Sure, what kind of time frame and risk are you looking at?

If you want something ultra short term, I would say the money market funds are your best shot – stuff like Endowus Cash or Syfe Cash. 1.5-2% yields depending on how much risk you’re comfortable with.

If you want something higher like 2-3% then I would look at the Astrea / Temasek Bonds series. Liquidity is very poor so it will be hard to build a big position, but worth a shot for smaller amounts.

Anything beyond that and you need to be an Accredited Investor. For Retail Investors I really don’t think bonds outside of the above and SSBs make sense in this climate, yield is too low for the risk you’re taking on. Makes sense for AIs who need some diversification, but for retail investors equity makes more sense to me in this climate. Hold enough cash such that you don’t blow up, and put the rest into equities.

Thank you, FH for your views, much appreciated. Like you, I also believe Alibaba is worth buying since the price had dropped a lot. For Syfe and Endowus, I’m not sure how much are their fees and in fact how the whole thing works and how much their fees eat into the yields. Noted your view that you think equities may be better and keep cash on the side. Though I still think the US stock market is overheated right now though heard that Google just released good earnings results.

I’m wondering if there might be some bad news eventually that will see the US market correct by who knows? 20%? If that does happen, I’m gonna buy into the Vanguard S&P 500 Index. I like that its diversified.

For interest, might like to listen to Cathie Wood talking about her views on deflation coming. Sure hope she’s right.